The Best Landlord Insurance Companies Reviewed

Rental property ownership comes with significant financial risks that standard homeowner’s insurance won’t cover. Property damage, tenant lawsuits, and lost rental income can devastate your investment returns.

We at Direct Insurance Services have analyzed the market to identify the best landlord insurance providers that offer comprehensive protection. The right policy protects your property value and rental income streams.

Which Companies Lead Landlord Insurance

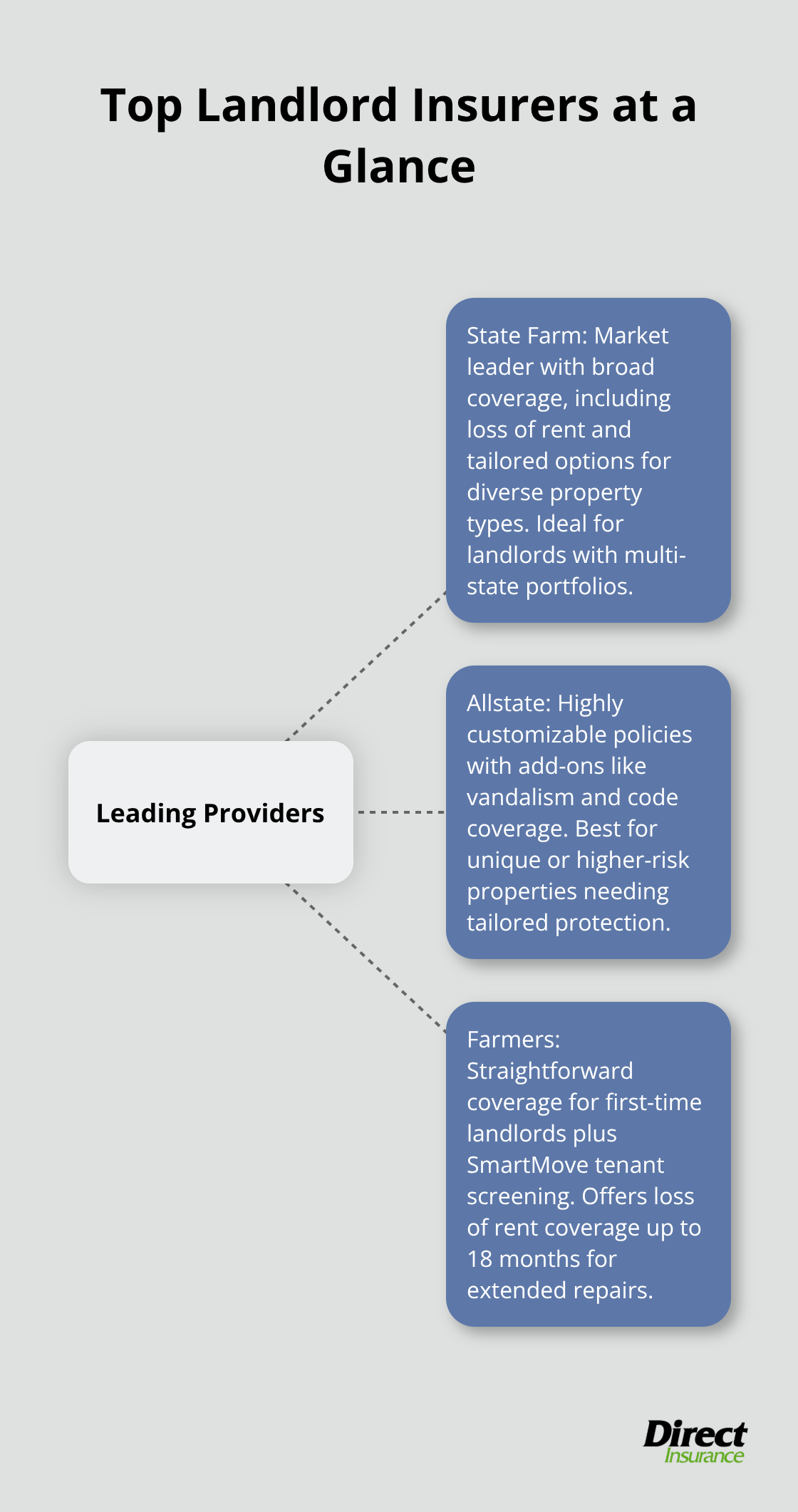

State Farm dominates the landlord insurance market with the largest market share in the U.S. insurance industry. Their comprehensive coverage includes specialized policies for homes, condos, and apartment owners, all with loss of rent coverage that compensates landlords when properties become uninhabitable. State Farm addresses different property types with tailored solutions, which makes them the strongest choice for landlords with diverse rental portfolios.

State Farm Sets the Industry Standard

State Farm’s market leadership stems from their proven track record and extensive coverage options. Their policies include property protection, liability coverage up to $1 million, and loss of rental income for extended periods. The company processes claims efficiently and maintains a widespread agent network that makes them particularly valuable for landlords who manage multiple properties across different states.

Allstate Offers Personalized Protection

Allstate excels in customizable landlord insurance with add-ons like vandalism coverage and code coverage that other providers often overlook. Their personalized approach allows landlords to tailor policies to specific property risks, though they don’t provide online quotes (which can slow the process). Allstate’s strength lies in their comprehensive protection options for high-risk properties and their willingness to adapt coverage to unique situations.

Farmers Insurance Supports New Landlords

Farmers Insurance provides an ideal entry point for first-time landlords with their straightforward policy structure and loss of rent coverage that extends up to 18 months. Their unique SmartMove tenant screening service helps landlords reduce risks before they become insurance claims. This combination of basic coverage with practical risk management tools makes Farmers particularly valuable for landlords who just start their rental property journey.

These three major providers represent different approaches to landlord insurance, but coverage types remain consistent across the industry. Every landlord needs specific protection categories regardless of which company they choose. Property owners should also consider water leak damage risks when selecting coverage options.

What Coverage Must Every Landlord Have

Landlord insurance requires three non-negotiable coverage types that protect your investment from the most common financial threats. Property damage coverage forms the foundation, with home insurance rates having increased 48% over the past five years. This coverage protects your building structure, attached fixtures, and any appliances you provide to tenants. The key difference lies in choosing replacement cost over actual cash value coverage, which pays current rebuilding costs rather than depreciated values that leave you financially short.

Property Damage Coverage Protects Your Investment

Dwelling protection covers fire, windstorm, vandalism, and other named perils that can damage your rental property structure. Most policies offer three tiers: DP-1 covers basic named risks at actual cash value, DP-2 adds broader named risks with replacement cost, and DP-3 provides open perils coverage with replacement cost protection. DP-3 policies cost more but cover all risks except those specifically excluded (which gives landlords comprehensive protection against unexpected property damage).

Liability Insurance Shields Against Lawsuits

Liability coverage protects landlords from legal claims when tenants or visitors suffer injuries on the property. Standard policies provide $100,000 minimum coverage, but experienced landlords carry $1 million in liability protection to handle serious incidents. Property managers and landlords need minimum $300,000 liability limits to protect against tenant lawsuits and third-party injury claims. American Family offers enhanced liability coverage with commercial umbrella protection, while BiBerk provides $2 million per claim according to Investopedia research. Property owners face higher liability risks than regular homeowners because tenant behavior creates unpredictable situations that can lead to expensive lawsuits.

Loss of Rental Income Maintains Cash Flow

Lost rental income coverage compensates landlords when properties become uninhabitable due to covered damage. Farmers Insurance provides this protection for up to 18 months, while other carriers typically offer 12-month coverage periods (which may not cover extended repair timelines). This protection maintains mortgage payments and property expenses when tenants cannot occupy damaged units, preventing financial strain during repair periods.

These coverage types work together to protect your rental property investment, but selecting the right insurance provider requires careful evaluation of multiple factors beyond basic coverage options. Landlords should also consider purchasing an umbrella insurance policy to protect their assets and have an extra layer of protection.

How Do You Select the Best Landlord Insurance Provider

Landlord insurance provider selection requires systematic evaluation of coverage limits, premium costs, and service quality. Start with coverage limits because inadequate protection costs more than higher premiums when claims occur. Standard liability coverage at $100,000 leaves landlords exposed to serious financial risk, while $1 million coverage provides adequate protection for most rental properties. BiBerk offers the highest liability limits at $2 million per claim, which makes them superior for high-risk properties. Property coverage should always use replacement cost rather than actual cash value (which typically pays 20-30% less after depreciation factors reduce claim payouts).

Premium Costs Vary Dramatically Between Providers

Landlord insurance premiums average 15-25% higher than homeowners insurance according to ValuePenguin research, but rate differences between companies can exceed 50% for identical coverage. BiBerk provides policies up to 20% cheaper than competitors while it maintains comprehensive coverage options.

Request quotes from at least four providers to identify significant rate variations, and always compare identical coverage limits and deductibles. Property deductibles between $500 and $1,000 represent the sweet spot for most landlords (which balances premium savings with manageable out-of-pocket costs during claims).

Claims Processing Speed Determines Real Value

Customer satisfaction ratings reveal dramatic differences in claims handling among major providers. American Family leads with a 4.8 out of 5-star rating from Investopedia research and receives fewer complaints than statistically expected according to National Association of Insurance Commissioners data. Liberty Mutual processes claims in under 10 minutes on average, while other providers may take weeks for similar situations. State Farm scored 873 out of 1,000 in J.D. Power customer satisfaction surveys, which demonstrates their commitment to efficient service. Avoid providers with complaint ratios above industry averages, as poor claims processing negates premium savings when you need coverage most.

Financial Stability Protects Your Investment

Insurance company financial strength ratings from AM Best, Moody’s, and Standard & Poor’s reflect each provider’s ability to handle claims during economic downturns. Companies with A+ ratings represent AM Best’s independent opinion of an insurer’s financial strength and ability to meet ongoing insurance policy obligations. Travelers receives recognition for its financial strength, which provides landlords confidence that it can meet its claims obligations. Weaker financial ratings indicate potential problems with claim payments during market stress (particularly important for landlords with multiple properties and higher exposure levels). For personalized guidance on selecting the right coverage for your rental property, consider consulting with a licensed insurance agent who can assess your specific needs and risk factors.

Final Thoughts

State Farm emerges as the best landlord insurance choice for most property owners with their market-leading coverage and extensive agent network. American Family provides superior customer satisfaction ratings at 4.8 out of 5 stars, while BiBerk offers the most affordable premiums with policies up to 20% cheaper than competitors. Farmers Insurance serves first-time landlords well with their straightforward policy structure and 18-month loss of rent coverage.

Premium costs matter less than adequate coverage limits when serious claims occur. Always choose replacement cost over actual cash value coverage, maintain at least $1 million in liability protection, and verify your provider’s financial strength through AM Best ratings. Compare quotes from multiple carriers because rate differences can exceed 50% for identical coverage (which can save thousands annually).

We at Direct Insurance Services shop multiple top-rated insurance companies to find you comprehensive coverage at competitive rates. Our team provides personalized service and flexible payment options that fit any budget. Contact Direct Insurance Services today to secure protection for your rental property investment and maintain your peace of mind as a landlord.