How Much Is Umbrella Insurance A Cost Breakdown

Umbrella insurance provides extra liability protection when your standard policies reach their limits. Many homeowners wonder how much is umbrella insurance and whether the cost justifies the coverage.

We at Direct Insurance Services break down the pricing factors and average costs to help you make an informed decision. The answer depends on your coverage needs and risk profile.

Why Umbrella Insurance Matters More Than You Think

Umbrella insurance steps in when your home insurance policy hits its $300,000 liability limit and someone sues you for $2 million after a pool accident at your house. Standard homeowner policies typically cap liability coverage between $100,000 and $500,000, while auto insurance liability limits often range from $25,000 to $100,000 per person. These amounts fall short when you face serious lawsuits, which can reach significant judgments in severe cases.

Legal Protection That Standard Policies Miss

Umbrella policies cover scenarios your primary insurance excludes entirely. Slander lawsuits, false imprisonment claims, and libel cases all fall under umbrella coverage but remain absent from typical homeowner policies. Legal defense costs alone can drain your savings even before any settlement occurs.

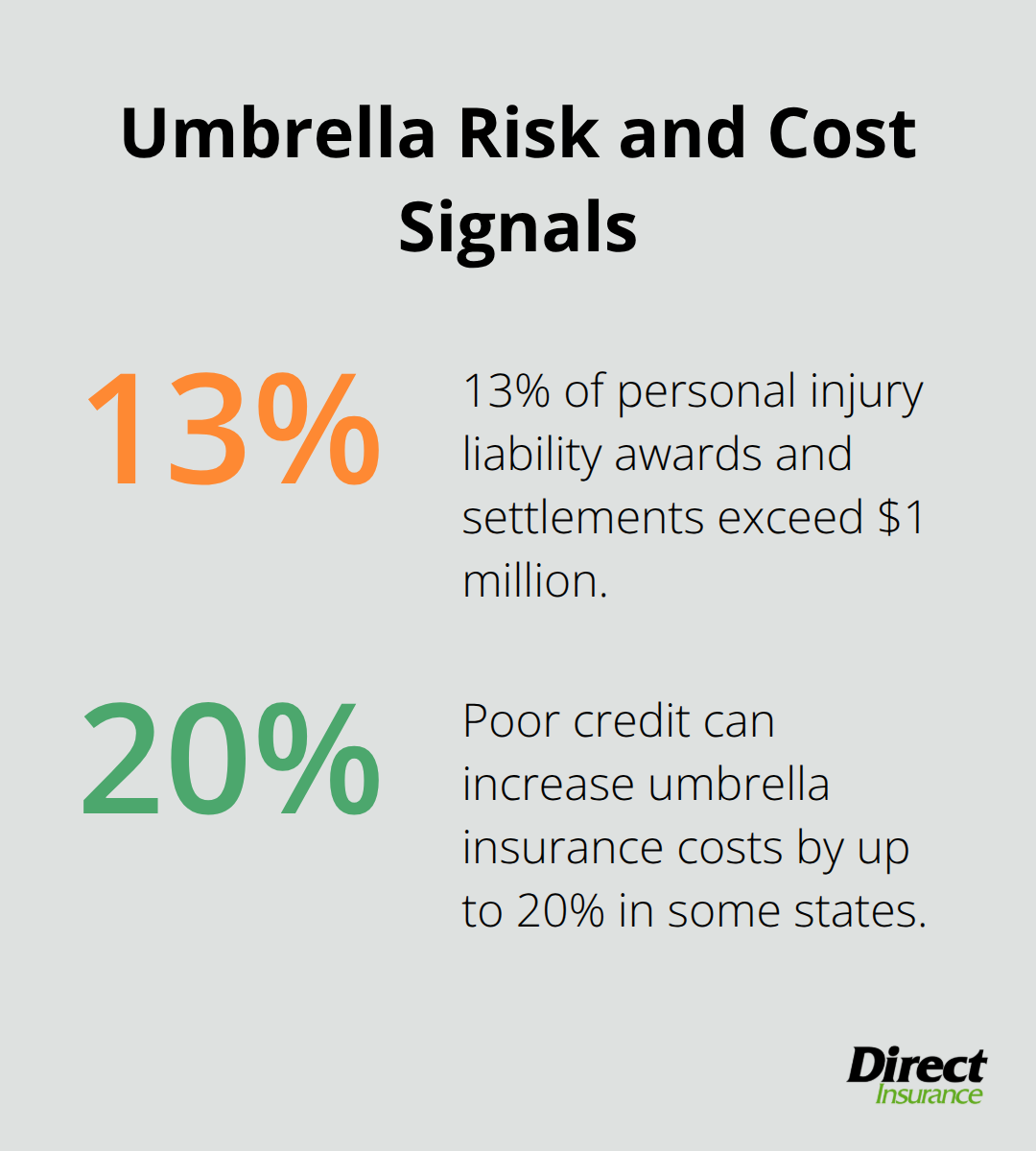

About 13% of personal injury liability awards and settlements exceed $1 million, making standard policy limits inadequate for many situations.

Asset Protection for Your Wealth

Your net worth determines your umbrella insurance needs more than any other factor. Financial advisors recommend coverage that matches or exceeds your total assets, including home equity, retirement accounts, and investment portfolios. Many individuals with significant wealth lack umbrella coverage, leaving substantial assets vulnerable to lawsuits. The average annual cost of $380 for $1 to $2 million in coverage makes this protection remarkably affordable compared to potential losses.

High-Risk Activities Demand Extra Coverage

Pool ownership, teenage drivers, and rental properties multiply your liability exposure significantly. Families with teen drivers face higher accident involvement rates, creating substantial lawsuit risks that basic auto coverage cannot handle. Property owners who manage rentals encounter tenant-related liability issues that standard landlord policies may not fully address (these risk factors make umbrella insurance essential rather than optional for many households).

Understanding these coverage gaps helps you evaluate how much protection you actually need, which directly impacts the premium costs we’ll examine next.

What Drives Your Umbrella Insurance Costs

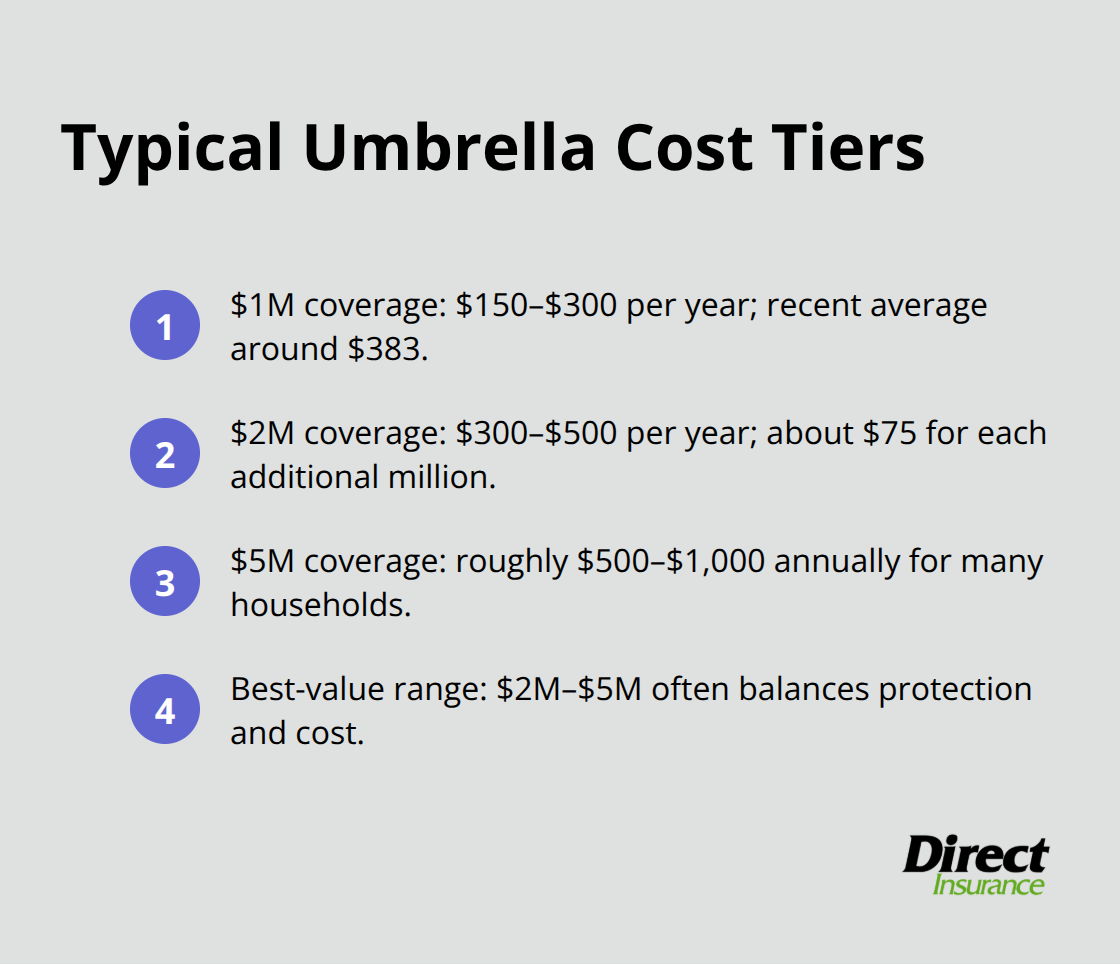

Your umbrella insurance premium depends on three primary factors that insurers evaluate when they calculate your risk exposure. Coverage amounts represent the most straightforward element in the price structure, with $1 million policies that average $150 to $300 annually, while $2 million coverage typically costs $300 to $500 per year. The rate structure follows a pattern where each additional million costs less than the first million, which makes higher coverage limits more affordable than many people expect.

Your Personal Risk Assessment Determines Premium Rates

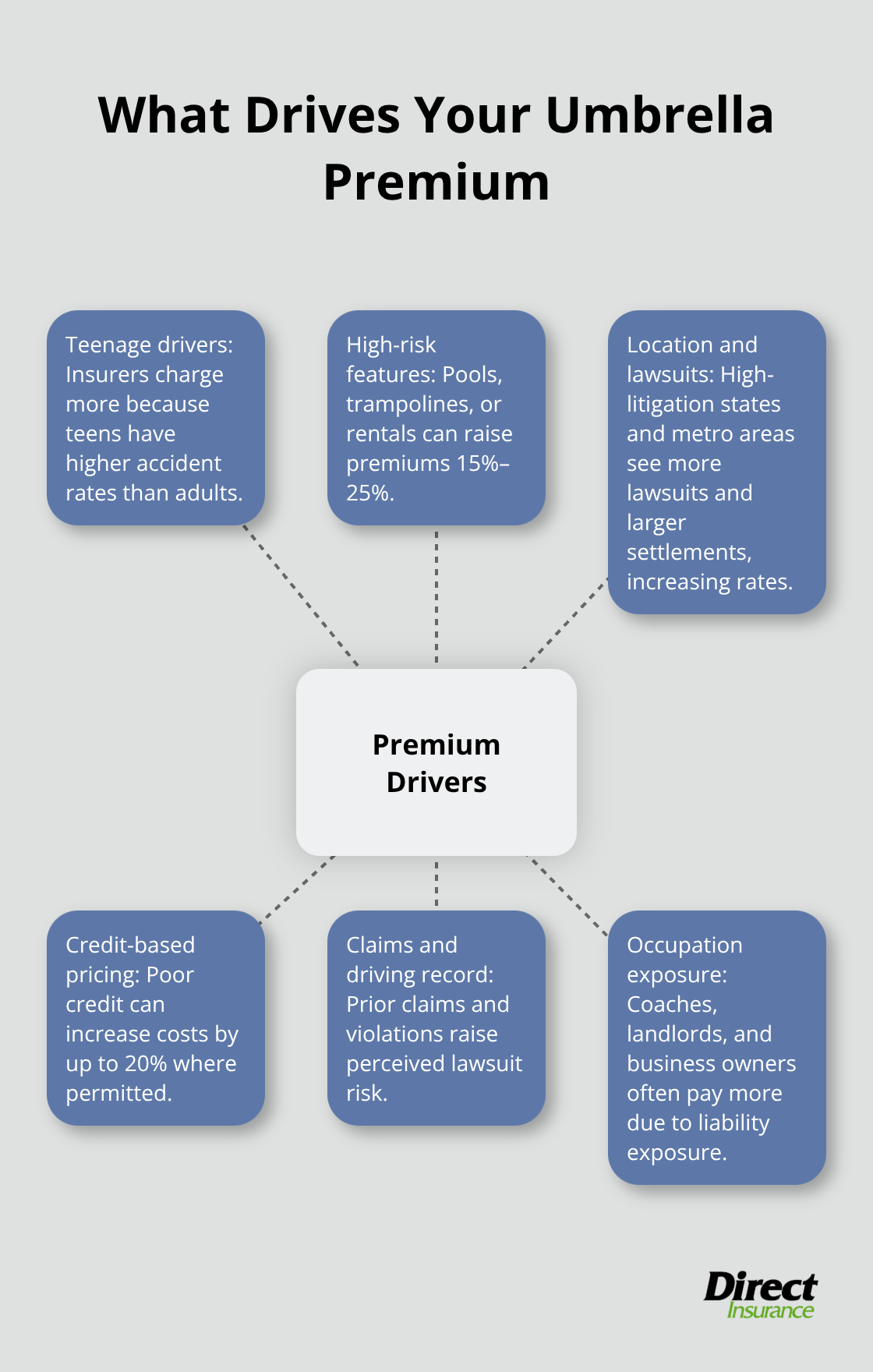

Insurance companies examine your claims history, record behind the wheel, and lifestyle factors to determine your likelihood of facing a lawsuit. Households with teenage drivers pay significantly higher premiums because teens cause accidents at rates significantly higher than adult drivers, with drivers 16 to 19 years old involved in 4.8 fatal crashes per 100 million travel miles compared to 1.4 for older drivers. Property owners with pools, trampolines, or rental properties face premium increases of 15% to 25% due to elevated liability risks (these features create additional exposure that insurers must account for in their calculations).

Poor credit scores can increase your umbrella costs by up to 20% in states where insurers use credit-based models to set rates. Your occupation also influences premiums, with coaches, landlords, and business owners often paying more due to increased liability exposure from their professional activities.

Location Impacts Your Premium Structure

Geographic factors play a decisive role in umbrella insurance costs, with states like California and New York that command premiums 40% to 60% higher than rural areas due to higher lawsuit frequencies and larger settlement amounts. Louisiana residents often face the highest umbrella insurance costs nationwide because of the state’s legal environment and high litigation rates.

Local court systems that historically award larger settlements drive up premiums for all residents in those areas, regardless of individual risk factors. Insurers analyze county-level lawsuit data and average settlement amounts when they set rates (this makes your zip code a significant cost factor that you cannot control but must consider in your budget).

These cost factors work together to create your final premium, but the actual dollar amounts vary significantly based on coverage levels and insurance company policies.

What Does Each Coverage Level Actually Cost

The pricing structure for umbrella insurance follows predictable patterns that make higher coverage limits surprisingly affordable. A $1 million umbrella policy costs between $150 and $300 annually for most households, with the average of $383 according to recent industry data. This baseline coverage works well for families with net worth under $1 million, but the real value emerges when you examine higher limits.

Standard Coverage Costs Most Families Choose

A $2 million policy typically ranges from $300 to $500 per year, with costs increasing by approximately $75 per additional million in coverage. This means the second million costs only about $75 more than the first million. Coverage between $2 million and $5 million represents the optimal range for middle to upper-middle-class households (this sweet spot balances comprehensive protection with reasonable premiums).

Premium Patterns Across Major Insurers

State Farm, Allstate, and GEICO consistently offer competitive rates in the $2-5 million range. State Farm often provides the lowest premiums for customers who bundle with auto and home policies. Different insurers price their policies with varying structures, making comparison shopping essential for finding the best rates.

Higher Limits Deliver Exceptional Value

A $5 million policy costs approximately $500 to $1,000 annually, making each additional million beyond the second one cost roughly $75 to $100. The cost efficiency becomes clear when you consider that $5 million in coverage costs less than most families spend on their monthly auto insurance payment.

Complex Households Face Higher Premiums

Households with multiple properties, teenage drivers, or high-risk assets may pay significantly more for higher coverage limits. This still represents exceptional value when measured against potential lawsuit exposure, as serious lawsuits can lead to substantial judgments that far exceed standard insurance limits.

Final Thoughts

Umbrella insurance delivers exceptional value when you consider the annual cost versus potential lawsuit expenses. At $150 to $300 annually for $1 million in coverage, this protection costs less than most families spend on monthly streaming services yet shields your entire financial future from devastating legal judgments. The question of how much is umbrella insurance becomes irrelevant when you face a $2 million lawsuit with only $300,000 in standard coverage.

The key to affordable coverage lies in bundling with your existing auto and home policies, maintaining clean records, and working with experienced agents who understand your specific risk profile. Geographic location and lifestyle factors influence premiums, but the cost remains remarkably low across all coverage levels (making this protection accessible to most households regardless of income).

We at Direct Insurance Services help Utah families secure comprehensive umbrella coverage as an independent agency that shops multiple top-rated insurance companies. Start by evaluating your net worth and risk exposure, then request quotes from multiple insurers to compare options. The peace of mind that comes from knowing your assets are protected makes umbrella insurance one of the smartest financial decisions you can make.