What Does Landlord Insurance Typically Cover?

Property owners face unique risks that standard homeowners insurance simply won’t cover. When you rent out your property, you need specialized protection.

We at Direct Insurance Services help Utah landlords understand what landlord insurance covers and why it matters. This coverage protects your investment property, rental income, and shields you from tenant-related liabilities.

Why Landlord Insurance Differs from Homeowners Coverage

Landlord insurance protects rental properties from risks that homeowners insurance never addresses. Standard homeowners policies cover owner-occupied residences and assume you live in the property full-time. The moment you rent out your home, your homeowners policy becomes inadequate because it excludes commercial activities like renting. According to the Insurance Information Institute, 5.3 percent of insured homes had a claim in 2023, with property damage accounting for 97.3 percent of homeowners insurance claims.

Rental Properties Face Higher Risk Exposure

Rental properties face increased claim frequency compared to owner-occupied homes according to insurance industry data. Tenants treat properties differently than owners, which leads to more damage from neglect, accidents, and intentional harm. Your homeowners policy won’t cover tenant-caused damage, theft by tenants, or liability when visitors get injured on rental property.

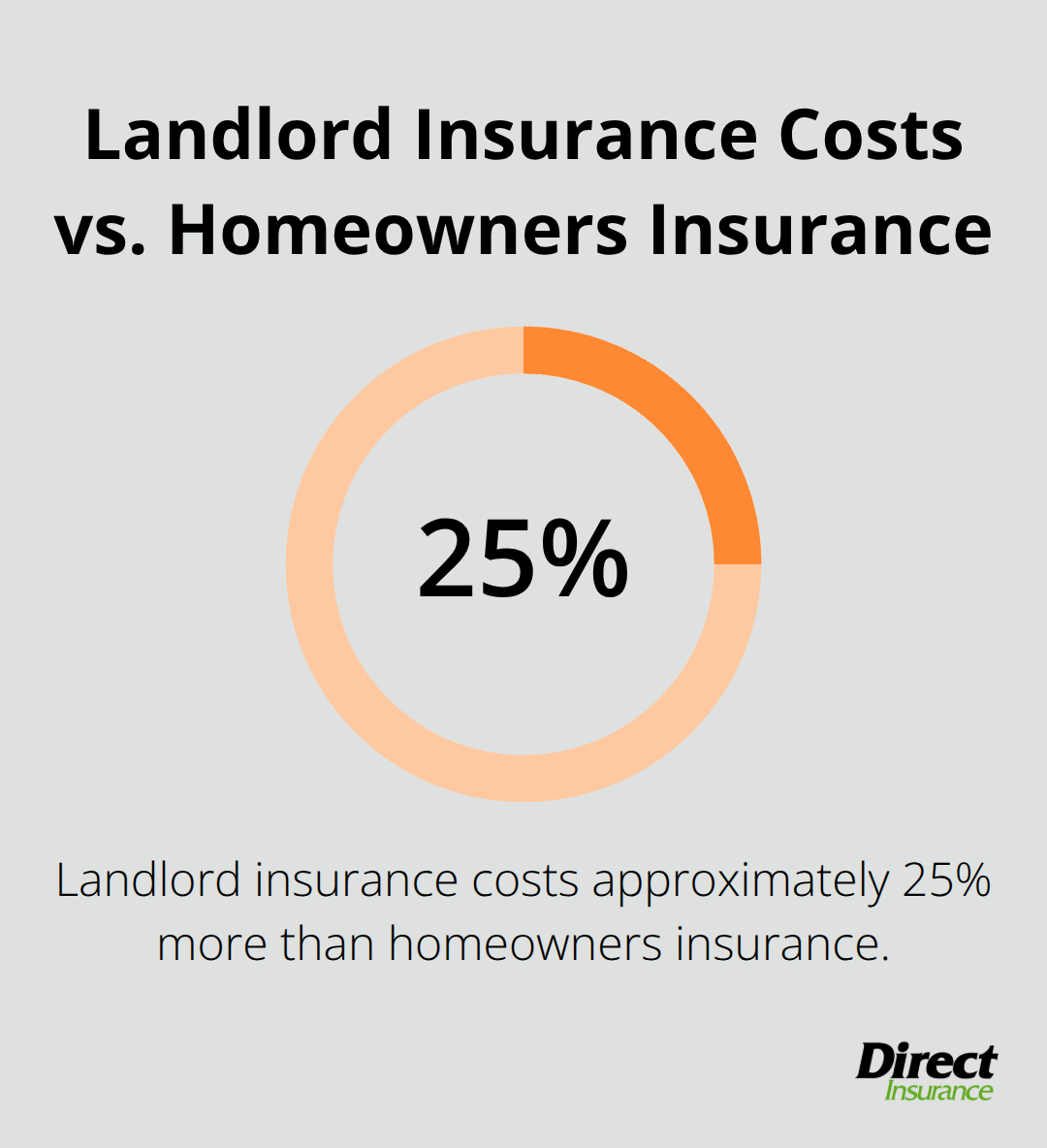

Landlord insurance costs approximately 25% more than homeowners insurance, with average annual premiums around $1,478 compared to $1,192 for homeowners coverage. This higher cost reflects the increased risk insurers face with rental properties and the additional coverage features landlord policies provide.

Who Must Switch to Landlord Coverage

Property owners need landlord insurance the moment they rent their property for one month or longer. Short-term rentals under 30 days might qualify for homeowners policy endorsements, but long-term rentals require dedicated landlord coverage. Accidental landlords who temporarily rent their homes while they relocate often make the costly mistake of keeping homeowners insurance.

Even vacant rental properties need specialized coverage since standard policies don’t protect empty homes. The National Association of Insurance Commissioners emphasizes that inappropriate coverage can result in denied claims and significant financial losses.

Commercial Activity Changes Everything

Insurance companies classify rental properties as commercial ventures regardless of property size or tenant count. This classification fundamentally changes your risk profile and coverage needs. Standard homeowners policies explicitly exclude business activities, which makes them useless for rental situations. Property owners who ignore this distinction face coverage gaps that can cost thousands in out-of-pocket expenses when claims arise.

These coverage differences become even more important when you examine what landlord insurance actually protects.

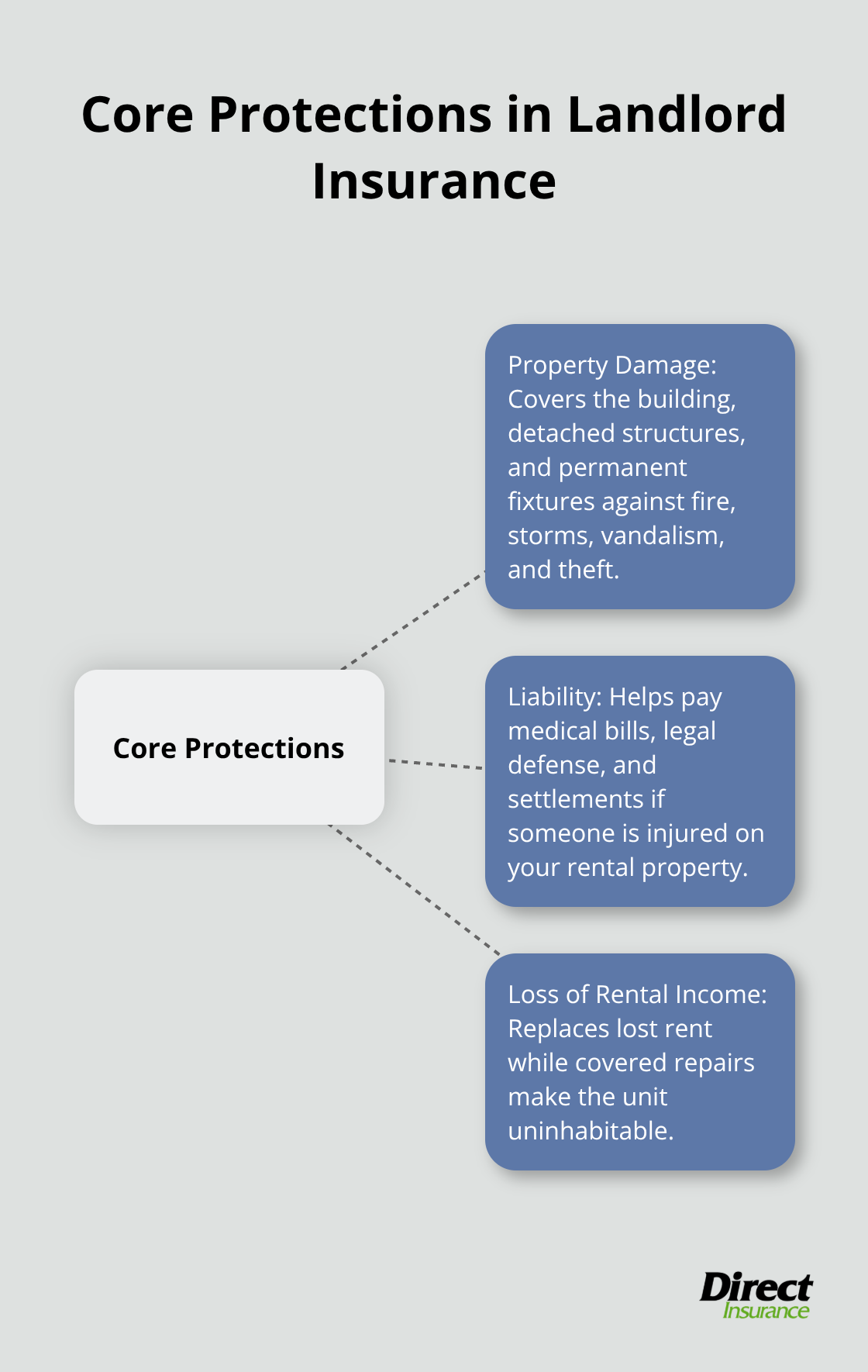

What Core Protection Does Landlord Insurance Provide

Landlord insurance delivers three fundamental protection areas that safeguard your rental property investment. Property damage coverage protects your building structure, attached garages, fences, and other permanent fixtures from fire, storm damage, vandalism, and theft. The Insurance Information Institute reports that property damage claims occur frequently among landlords, which makes this coverage essential for your physical investment protection.

Building and Structure Protection

This coverage typically includes replacement cost protection for the building itself, though you should verify whether your policy offers actual cash value or replacement cost coverage. The difference can mean thousands in claim payouts when damage occurs. Most policies cover the main dwelling, detached structures like garages and sheds, and permanent fixtures such as built-in appliances. Fire damage represents the most common claim type, followed by storm-related damage and vandalism.

Liability Protection Against Injury Claims

Liability coverage shields you from lawsuits when tenants or visitors get injured on your rental property. Standard landlord policies provide $1 million in liability limits, which covers medical expenses, legal fees, and settlement costs if someone sues you for injuries sustained on your property. This protection extends beyond basic slip-and-fall accidents to include dog bites, swimming pool accidents, and injuries from defective property conditions.

Rental Income Replacement During Repairs

Loss of rental income coverage compensates you for lost rent when your property becomes uninhabitable due to covered damage like fire or severe storm damage. This protection typically covers your normal rental income for the time needed to complete repairs, which helps maintain your cash flow during property restoration. The coverage amount should match your monthly rental income, and policies often include fair rental value provisions that account for market rate increases.

Smart landlords verify their income protection limits annually since rental rates change and inadequate coverage leaves gaps in financial protection during extended repair periods. Beyond these core protections, landlords can enhance their policies with additional coverage options that address specific risks.

Which Additional Coverage Options Protect Your Investment

Standard landlord insurance provides solid foundation coverage, but smart property owners enhance their policies with targeted add-ons that address specific rental property risks. These optional coverages fill gaps that basic policies leave open and protect against scenarios that standard coverage excludes.

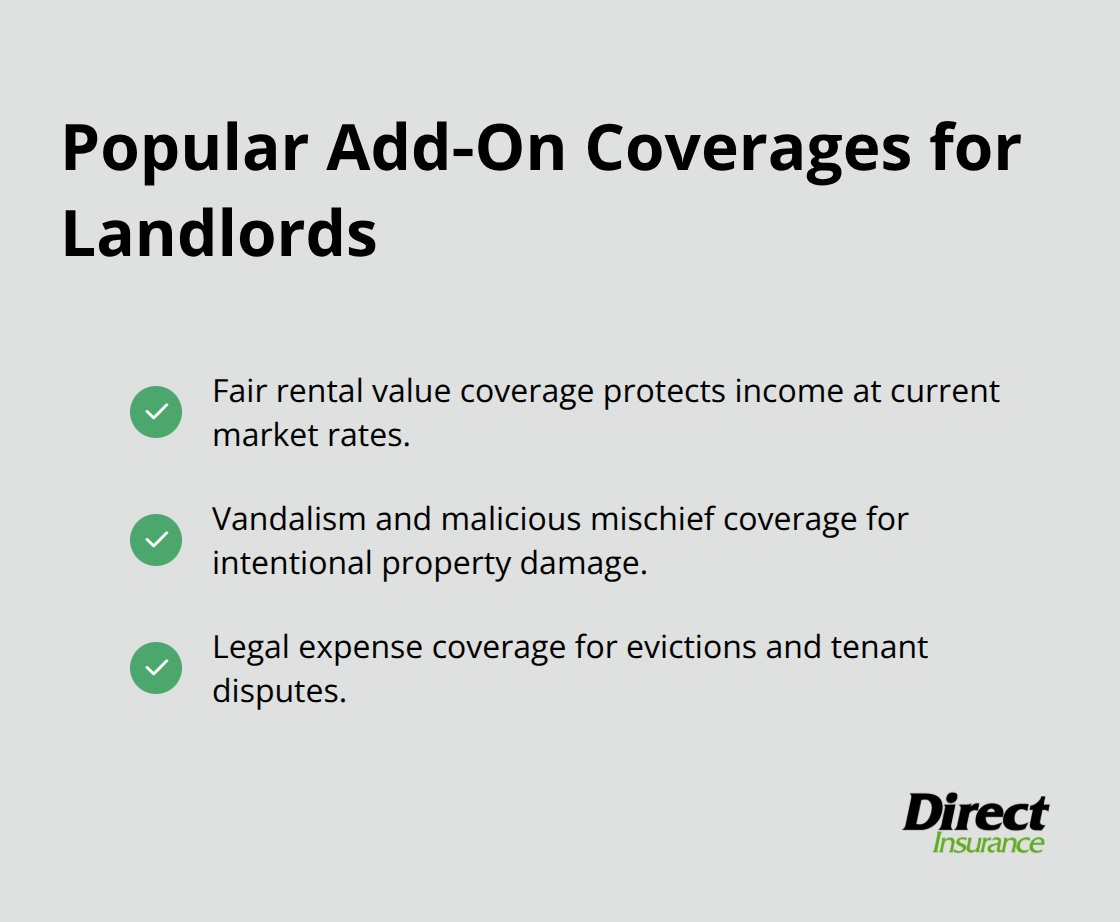

Fair Rental Value Coverage

Fair rental value coverage extends your income protection beyond basic loss of rent provisions. This enhancement covers market-rate rental income rather than your contracted rent amount, which protects you when your actual rent falls below current market rates. Property owners who locked in below-market rents years ago need this coverage because standard policies only compensate for your actual rental income, not what you could earn at current market rates.

This coverage becomes particularly valuable during extended repair periods when you lose months of rental income. The difference between your contracted rent ($1,200) and current market rates ($1,500) can cost you $300 monthly during repairs without this protection.

Vandalism and Malicious Mischief Protection

Vandalism and malicious mischief coverage becomes essential when you rent to higher-risk tenants or own properties in areas with elevated crime rates. Property damage claims affect many landlords each year, with vandalism representing a significant portion of these incidents.

This coverage protects against intentional property damage that goes beyond normal wear and tear, including graffiti, broken windows, and destroyed fixtures. Standard policies often limit vandalism coverage or exclude certain types of malicious damage, which makes this add-on valuable for comprehensive protection.

Legal Expense Coverage for Tenant Disputes

Legal expense coverage for tenant disputes provides financial protection for eviction proceedings, lease violations, and tenant-related legal issues. Eviction costs can be substantial, and this coverage handles attorney fees, court costs, and related expenses.

Property owners in tenant-friendly states benefit most from legal defense costs since eviction processes take longer and cost more. Try to secure legal expense coverage limits of at least $10,000 per incident to handle complex tenant disputes effectively. This protection proves invaluable when tenants refuse to pay rent or violate lease terms repeatedly.

Final Thoughts

Property damage protection, liability coverage, and loss of rental income form the foundation that answers what landlord insurance covers for Utah property owners. These three core components work together to shield your rental investments from the most common risks. Annual policy reviews help you maintain adequate coverage as property values and rental markets shift.

Coverage limits and policy exclusions demand regular attention because many landlords discover gaps during claim situations. Flood and earthquake damage typically require separate policies, while tenant-caused damage may face specific limitations. Utah property owners should evaluate their current coverage against actual replacement costs and rental income potential (especially after market changes).

We at Direct Insurance Services shop multiple top-rated insurance companies to find the best landlord coverage for your specific property needs. Our team understands Utah’s unique risks and helps landlords secure appropriate protection at competitive rates. The investment you make in proper landlord insurance coverage protects years of property appreciation and rental income.