Will Home Insurance Cover Fire Damage?

House fires devastate families across America every year, leaving homeowners wondering about their financial protection. Will home insurance cover fire damage when disaster strikes your property?

We at Direct Insurance Services see these questions daily from concerned homeowners. Understanding your fire damage coverage can mean the difference between swift recovery and financial hardship.

What Fire Damage Home Insurance Typically Covers

Standard homeowners insurance provides comprehensive fire damage protection that covers far more than most homeowners realize. Fire damage accounts for a significant portion of homeowners insurance claims in the United States, making this coverage absolutely essential for protecting your largest investment.

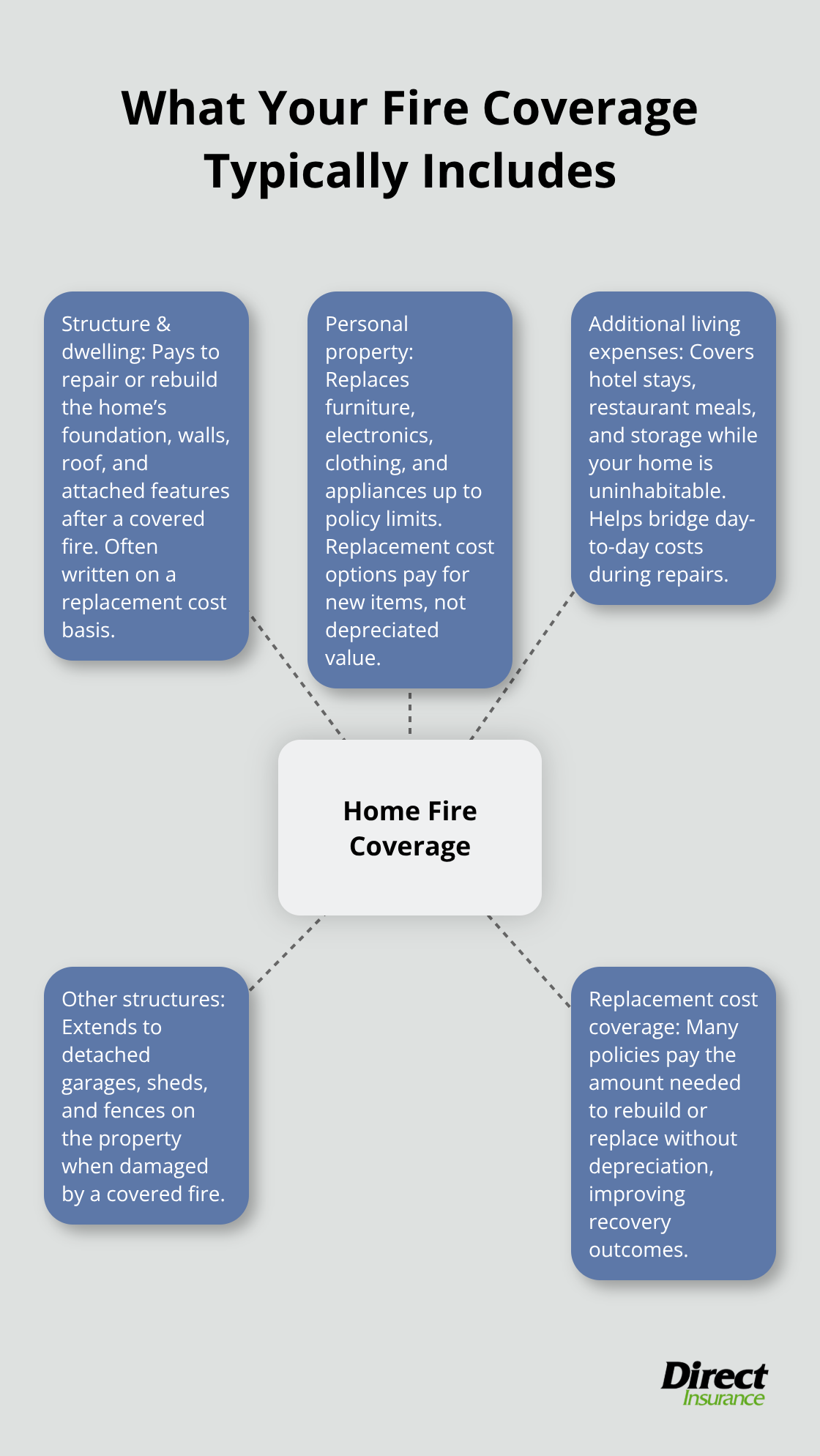

Structure and Dwelling Protection

Your dwelling coverage pays for structural repairs to your home’s foundation, walls, roof, and attached features like garages and porches when fire strikes. This protection extends beyond the main structure to include other buildings on your property such as detached garages, sheds, and fences. Most policies provide replacement cost coverage, which means insurers pay the full amount needed to rebuild rather than the depreciated value of damaged structures.

Personal Belongings and Contents Coverage

Personal property coverage replaces your damaged belongings (furniture, electronics, clothing, and appliances) up to your policy limits. Most policies offer replacement cost coverage, meaning you receive the full amount needed to buy new items rather than their depreciated value. According to the Insurance Information Institute, property damage accounted for 97.3 percent of homeowners insurance claims, which highlights why adequate personal property limits matter. High-value items like jewelry, artwork, and collectibles often require additional coverage beyond standard limits to receive full protection.

Additional Living Expenses During Repairs

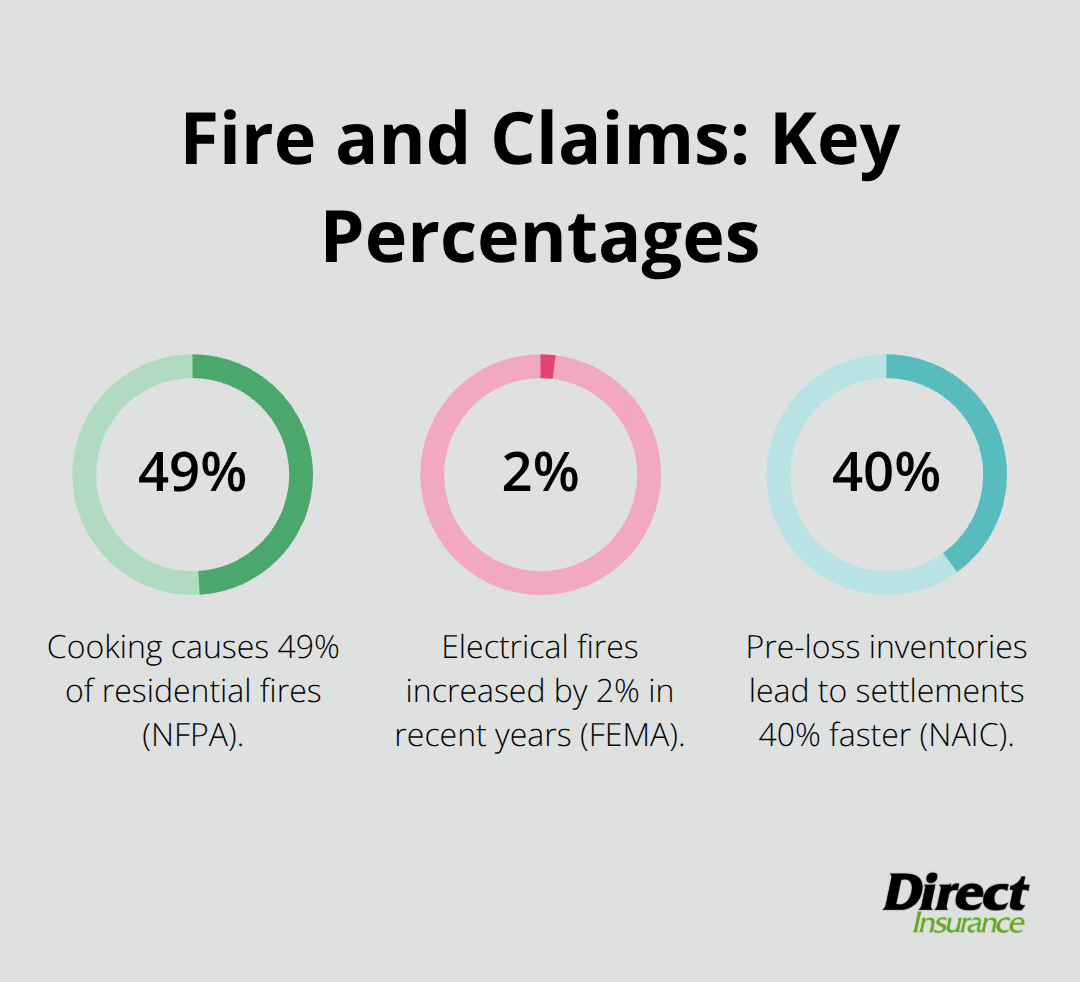

Additional living expenses coverage pays for temporary housing, meals, and other necessary costs when your home becomes uninhabitable after a fire. This protection typically covers hotel stays, restaurant meals, and storage fees for your belongings during the repair period. The National Fire Protection Association found that cooking causes 49% of residential fires, which makes this coverage particularly valuable since kitchen fires often create extensive smoke damage throughout homes. Coverage usually lasts until repairs finish or you find permanent housing.

However, not all fire damage situations receive coverage, and certain exclusions can leave homeowners vulnerable to significant out-of-pocket expenses.

When Does Home Insurance Deny Fire Claims

Insurance companies reject fire damage claims more often than homeowners expect, and these exclusions can create devastating financial surprises. Negligence stands as the primary reason for claim denials, particularly when homeowners fail to maintain electrical systems or ignore obvious fire hazards. The Federal Emergency Management Agency reports that electrical fires have seen a 2% increase in recent years, yet many insurers deny claims when outdated systems spark blazes that proper maintenance could have prevented.

Intentional Acts and Arson Allegations

Insurers automatically deny coverage for intentionally set fires, which includes arson committed by the homeowner or family members. Insurance companies investigate suspicious fires thoroughly and examine burn patterns while they interview witnesses to determine cause. Even innocent homeowners face claim denials when evidence suggests intentional ignition, which forces them to prove their innocence through expensive legal proceedings. Cooking fires account for 49% of home fires according to the National Fire Protection Association, yet insurers may deny claims when homeowners leave food unattended for extended periods or fail to clean grease buildup properly.

Coverage Limits and High-Risk Exclusions

Standard policies exclude certain fire sources (earthquakes, floods, and nuclear incidents), which leaves homeowners vulnerable to specific disaster scenarios. Wildfire coverage varies dramatically by location, with insurers in high-risk areas like California often excluding wildfire damage entirely or charging prohibitive premiums. Deductibles typically range from $500 to $5,000, which means homeowners pay significant out-of-pocket costs before coverage begins. The Insurance Information Institute found that average fire damage claims exceed $70,000, yet many policies cap personal property coverage at inadequate levels that fail to replace modern electronics and furnishings at current market prices.

Poor Documentation and Maintenance Issues

Insurers frequently deny claims when homeowners cannot provide adequate documentation of their losses or fail to maintain their properties properly. Missing smoke detectors, expired fire extinguishers, or delayed repairs to known hazards give insurance companies grounds to reject claims entirely. Homeowners must document their belongings before disasters strike and maintain detailed records of home improvements and safety measures to support future claims effectively. Claims history impacts future premiums with homeowners insurance claims staying on your CLUE report for five to seven years.

The claims process itself presents additional challenges that can complicate your recovery efforts.

How to File a Fire Damage Insurance Claim

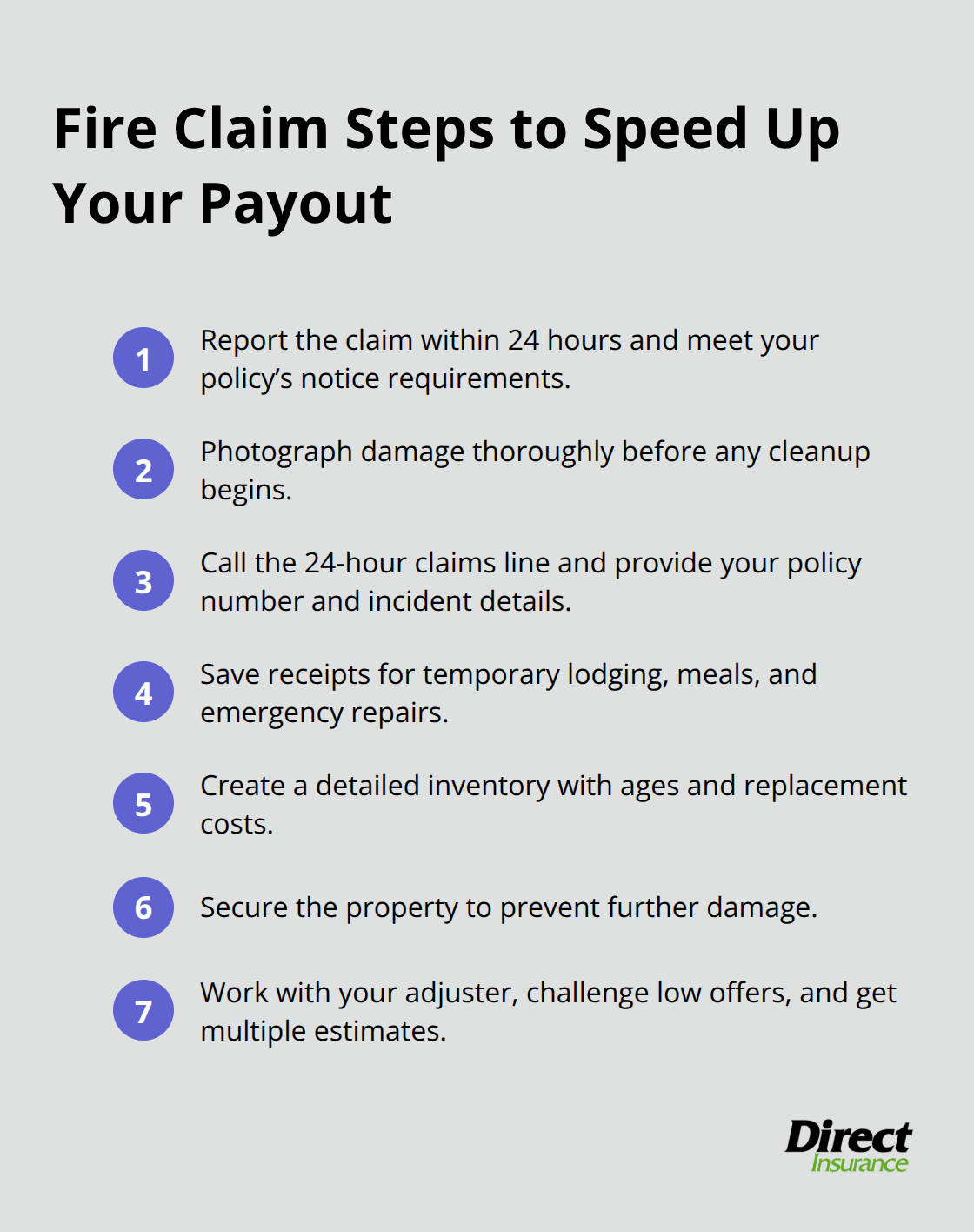

Contact your insurance company within 24 hours of the fire incident to report the damage and start your claim immediately. Most insurers require notification within 30 days, but delays can complicate your claim process and potentially reduce your settlement. The Insurance Information Institute reports that prompt reports lead to faster claim resolution, with most fire damage claims processed within 15-30 days when homeowners provide complete documentation. Take photographs of all damaged areas before cleanup begins (wide shots of rooms and close-ups of specific items), as adjusters use this visual evidence to calculate settlement amounts.

Report the Incident Immediately

Call your insurance company’s 24-hour claims hotline as soon as you reach safety after the fire. Provide your policy number, the date and time of the fire, and a brief description of what happened. The insurer will assign a claim number and schedule an adjuster inspection within 72 hours. Document the fire department’s response and obtain a copy of their incident report, as this official documentation supports your claim and establishes the fire’s cause.

Document Everything Before Cleanup

Create a detailed inventory of damaged personal property with descriptions, approximate ages, and estimated replacement costs before you touch anything. Save all receipts from temporary expenses, emergency repairs, and replacement items since additional expenses coverage reimburses these costs. The National Association of Insurance Commissioners found that homeowners who maintain pre-loss inventories receive settlements 40% faster than those without proper documentation. Secure your property with tarps or boards to prevent further damage, but avoid permanent repairs until your adjuster completes their inspection.

Work Directly With Your Adjuster

Your insurance adjuster will schedule an inspection within 72 hours of your claim report and assess structural damage while they review your personal property inventory. Challenge low settlement offers immediately if repair estimates exceed the adjuster’s assessment, as initial offers typically fall 15-20% below actual repair costs according to industry data. Get multiple contractor estimates for structural repairs and present them to your adjuster as evidence if their assessment seems inadequate.

Independent adjusters work for you rather than the insurance company and can provide second opinions when settlements appear insufficient (though they typically charge 10-15% of your claim amount). Many homeowners discover coverage gaps only after filing a claim, so review your policy carefully during this process.

Final Thoughts

Will home insurance cover fire damage? The answer depends on your specific policy terms and the fire’s circumstances. Standard homeowners insurance covers structural damage, personal belongings, and additional living expenses when fires result from covered perils like electrical malfunctions or cooking accidents. Coverage gaps exist for negligence-related fires, intentional acts, and certain high-risk scenarios like wildfires in designated zones.

Adequate protection requires you to understand your policy limits and exclusions before disaster strikes. Review your coverage annually to account for home improvements, new purchases, and area risk factors. Document your belongings with photos and receipts, maintain proper safety equipment, and address electrical or structural issues promptly to avoid claim denials.

We at Direct Insurance Services help Utah homeowners navigate fire damage claims. Our independent agency shops multiple top-rated insurers to find comprehensive coverage that fits your budget and specific needs (we compare options from leading carriers to secure the best protection). Contact our local team today to review your current policy and identify potential coverage gaps before they become costly problems.