Comprehensive Home Insurance Coverage Guide

Home insurance protects your most valuable asset, but choosing the right policy can feel overwhelming. With average homeowners paying $1,383 annually according to the National Association of Insurance Commissioners, getting comprehensive home insurance that fits your needs and budget matters.

We at Direct Insurance Services see too many homeowners discover coverage gaps only after filing a claim. This guide breaks down everything you need to know about selecting adequate protection for your property and belongings.

What Coverage Types Protect Your Home

Home insurance policies contain three fundamental coverage types that work together to protect your property and finances. Dwelling coverage forms the foundation, typically represents 80-90% of your total coverage amount, and protects your home’s structure including walls, roof, floors, and built-in appliances. The Insurance Information Institute reports that dwelling coverage should equal at least 80% of your home’s replacement cost to avoid coinsurance penalties that reduce claim payouts.

Structure Protection Beyond Your Main Home

Standard policies extend beyond your primary home to cover detached structures like garages, sheds, and fences at 10% of your total coverage amount. This coverage proves inadequate for expensive outbuildings – a detached three-car garage costs $20,000-$40,000 to rebuild, yet most policies cap other structures coverage at $30,000-$50,000. Smart homeowners increase this limit when they own valuable detached structures.

Personal Property Coverage Limits

Personal property coverage protects your possessions at 50-70% of your home coverage, but standard policies impose sub-limits that catch homeowners off-guard. Electronics face $1,500 limits, jewelry caps at $1,000, and business equipment receives minimal coverage. These restrictions mean a stolen laptop collection or jewelry theft could leave you with significant out-of-pocket expenses.

Liability Protection Requirements

Liability protection starts at $100,000 minimum, though legal experts recommend $300,000-$500,000 to protect against lawsuit settlements that averaged $31,000 in 2023 (according to the National Center for State Courts). Medical payments coverage handles immediate expenses for injured visitors regardless of fault and prevents small incidents from escalating into liability claims.

Understanding these coverage types helps you identify potential gaps, but the cost of your policy depends on several key factors that insurers evaluate when they calculate your premium rates.

What Drives Your Home Insurance Premium

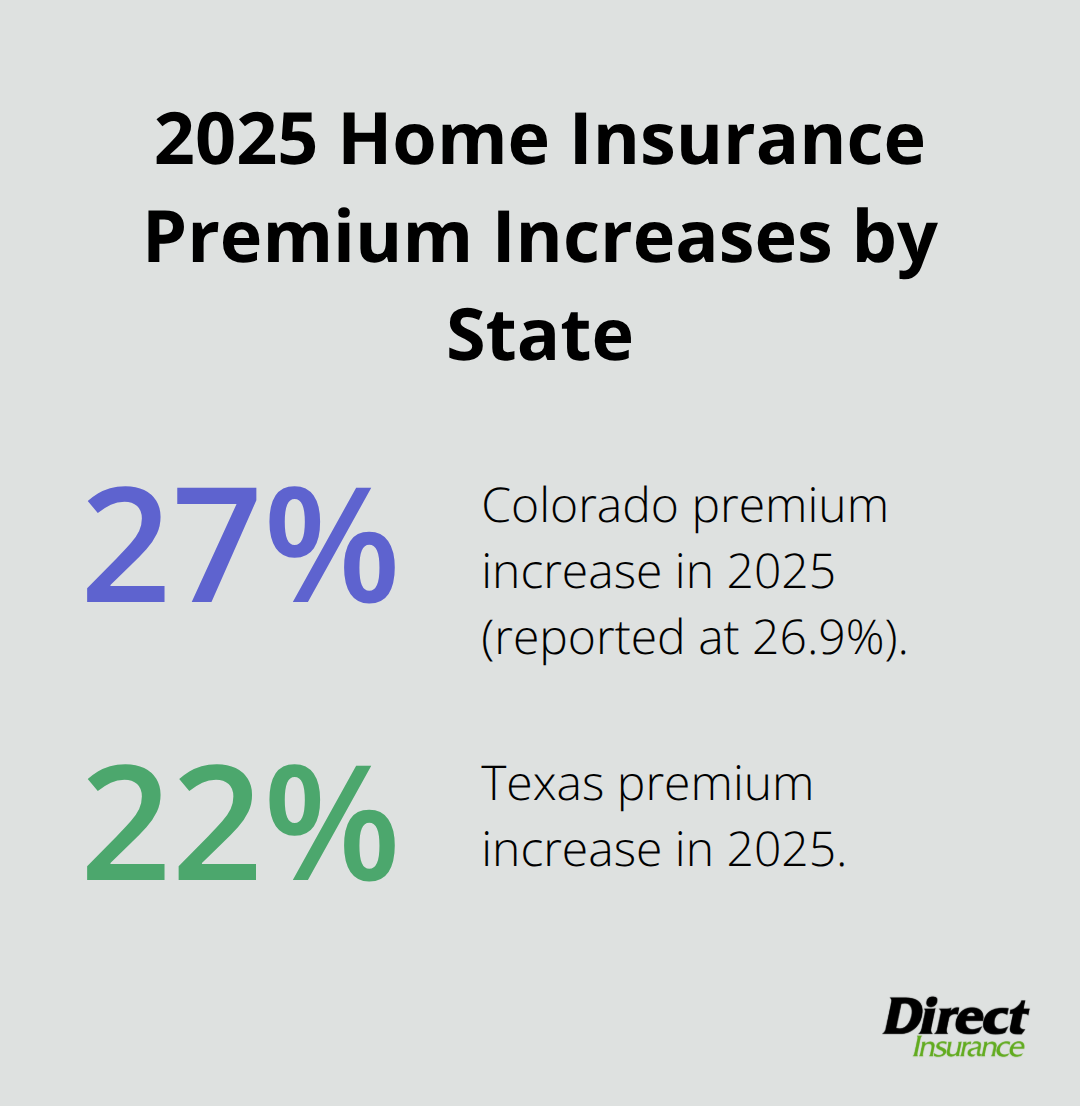

Your insurance premium depends on three major cost drivers that insurers evaluate with mathematical precision. Location dominates price decisions – Mississippi homeowners pay $3,306 annually on average while Hawaii residents pay just $610 according to recent industry data. Colorado leads premium increases at 26.9% in 2025, followed by Texas at 22.0%, which reflects severe weather patterns. In 2024, global natural perils cost $417 billion, with $154 billion insured. Wind and hail damage alone generated $31 billion in roof claims during 2024, which pushed insurers to scrutinize properties in tornado-prone regions more aggressively.

Construction Age Creates Premium Penalties

Homes over 40 years old face automatic premium increases because outdated electrical systems, plumbing, and roof materials create higher claim risks. Insurers now require roof inspections for properties with roofs older than 15 years, and many companies switch older roofs from replacement cost coverage to actual cash value coverage that factors in depreciation. Wood frame construction costs 15-25% more to insure than cement or steel frame homes due to fire vulnerability. Smart homeowners offset age penalties through strategic upgrades – modern electrical panels, updated plumbing, and impact-resistant roof materials can reduce premiums by 10-20%.

Deductible Strategy Impacts Annual Costs

Deductibles rose 24.5% from 2024 to 2025, with high-risk states that see the steepest increases. You can reduce premiums by 15-30% when you raise your deductible from $1,000 to $2,500, but this creates higher out-of-pocket costs for claims. Coverage limits directly correlate with premium costs – you add approximately $200-400 annually when you increase coverage from $300,000 to $400,000 (depending on your location and risk factors). The key lies in balance between adequate protection and manageable premium costs through strategic deductible selection.

These cost factors help you understand premium calculations, but smart policy selection requires you to evaluate your specific coverage needs and compare options from multiple insurers.

How Do You Select the Right Home Insurance Policy

Property value calculation forms the foundation of smart policy selection. Professional appraisals cost $300-500 but provide accurate replacement costs that prevent underinsurance penalties. The National Association of Realtors reports that 64% of homeowners underestimate rebuilding costs by 20-40%, which triggers coinsurance clauses that reduce claim payments proportionally.

Calculate Your Home’s True Replacement Cost

Calculate your home’s replacement cost when you multiply square footage by local construction costs – currently $150-250 per square foot in most markets according to HomeAdvisor data. Add 20% inflation buffer to account for material cost increases that reached 19% in 2024. Personal property requires separate evaluation through room-by-room inventory that captures electronics, furniture, and valuable items often worth 40-60% of your home’s value.

Quote Comparison Strategies That Save Money

Obtain quotes from five insurers minimum because premium variations reach 40-60% for identical coverage according to Consumer Reports analysis. Focus on coverage limits rather than premium amounts during initial comparisons – some insurers quote artificially low limits to appear competitive. Request identical deductibles and coverage amounts from each company to enable accurate comparisons.

The Insurance Information Institute found that homeowners who compare quotes save $400-800 annually versus those who accept renewal offers automatically. Consider bundling auto and home insurance to maximize savings potential. Timing matters – request quotes 30-45 days before renewal to allow adequate comparison time without coverage lapses.

Critical Coverage Gaps Most Policies Miss

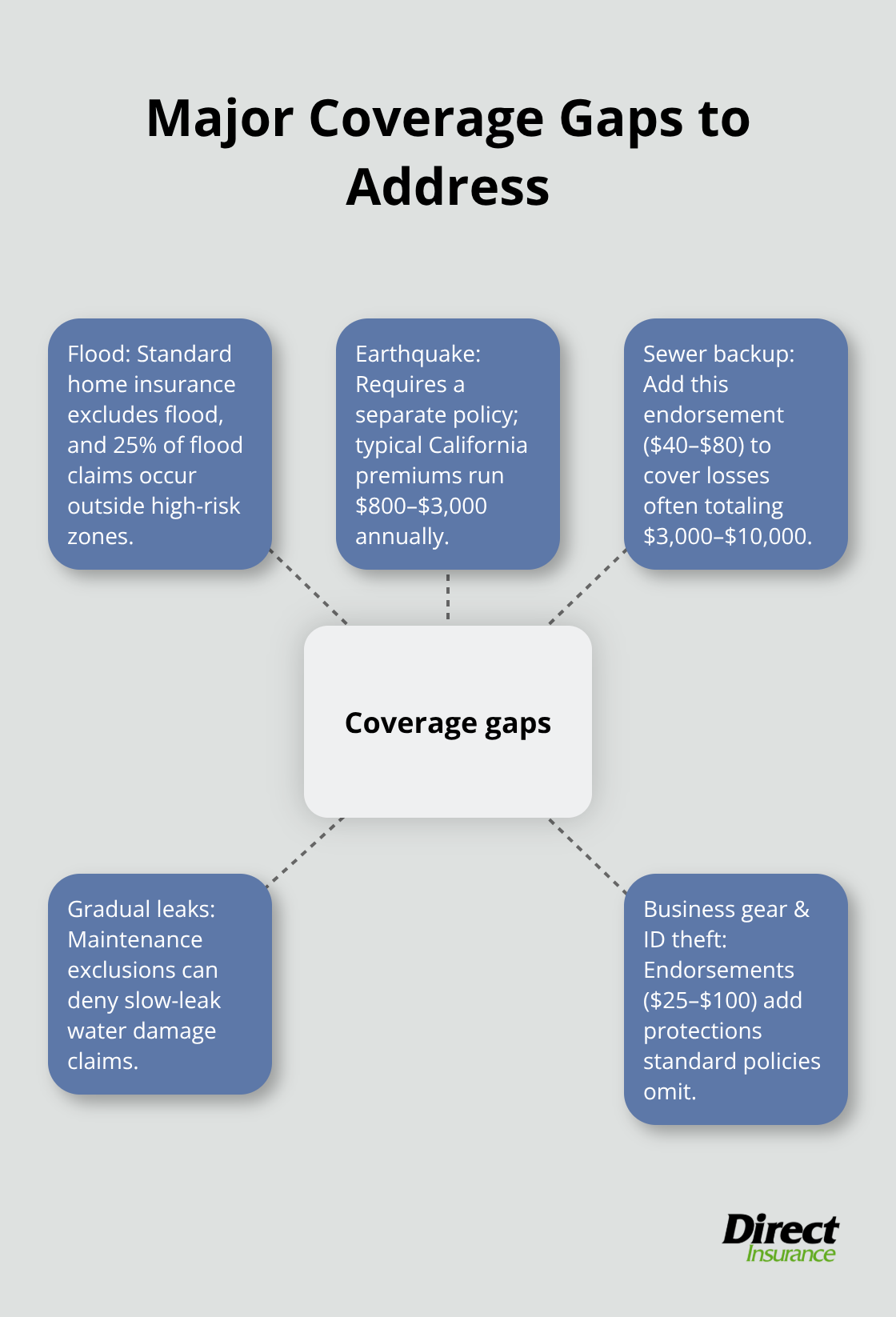

Standard policies exclude flood damage entirely despite Federal Emergency Management Agency data showing 25% of flood claims occur outside high-risk zones. Earthquake coverage requires separate policies in seismic regions – California homeowners pay $800-3,000 annually for earthquake insurance through the California Earthquake Authority.

Sewer backup coverage costs $40-80 annually but covers damage that averages $3,000-10,000 per incident according to Institute for Business and Home Safety research. Water damage coverage from burst pipes receives coverage, but gradual leaks face exclusion under maintenance clauses. Business equipment and identity theft protection require endorsements that cost $25-100 annually but provide coverage standard policies omit completely.

Final Thoughts

Comprehensive home insurance demands strategic decisions beyond basic coverage requirements. The average homeowner pays $1,966 annually, but smart policy selection reduces costs while it improves protection. You must focus on accurate replacement cost calculations, compare quotes from multiple insurers, and address coverage gaps through targeted endorsements.

Policy reviews matter more than most homeowners realize. Insurance markets shift rapidly – Colorado saw 26.9% premium increases in 2025 while coverage options evolved (and similar changes affect other states). Annual reviews help you capture new discounts, adjust coverage limits, and identify new risks that standard policies miss.

We at Direct Insurance Services help homeowners navigate complex insurance decisions. Our independent agency approach means we shop multiple top-rated companies to find optimal coverage at competitive rates. Contact our local team to review your current policy and identify potential improvements.