Home Insurance and Water Damage Protection

Water damage ranks as the second most common homeowner’s insurance claim, affecting 1 in 50 homes annually according to the Insurance Information Institute.

At Direct Insurance Services, we see Utah homeowners face unique water damage risks from winter pipe bursts to sudden flash floods. Understanding your home insurance and water damage coverage can save you thousands in unexpected repair costs.

This guide breaks down what’s covered, common scenarios, and prevention strategies to protect your investment.

What Water Damage Does Your Home Insurance Actually Cover

Home insurance covers sudden and accidental water damage, but the source determines your claim’s success. Standard policies pay for burst pipes, appliance malfunctions, and roof leaks from storms. The Insurance Information Institute reports water damage claims average $13,954, which makes coverage knowledge vital for homeowners.

Your policy covers washing machine hose failures, toilet overflows, and water heater ruptures when they occur without warning. Storm damage receives coverage when wind drives rain through damaged roofs or broken windows. Fire departments that use water to extinguish blazes also trigger coverage under most policies.

Weather Events That Activate Coverage

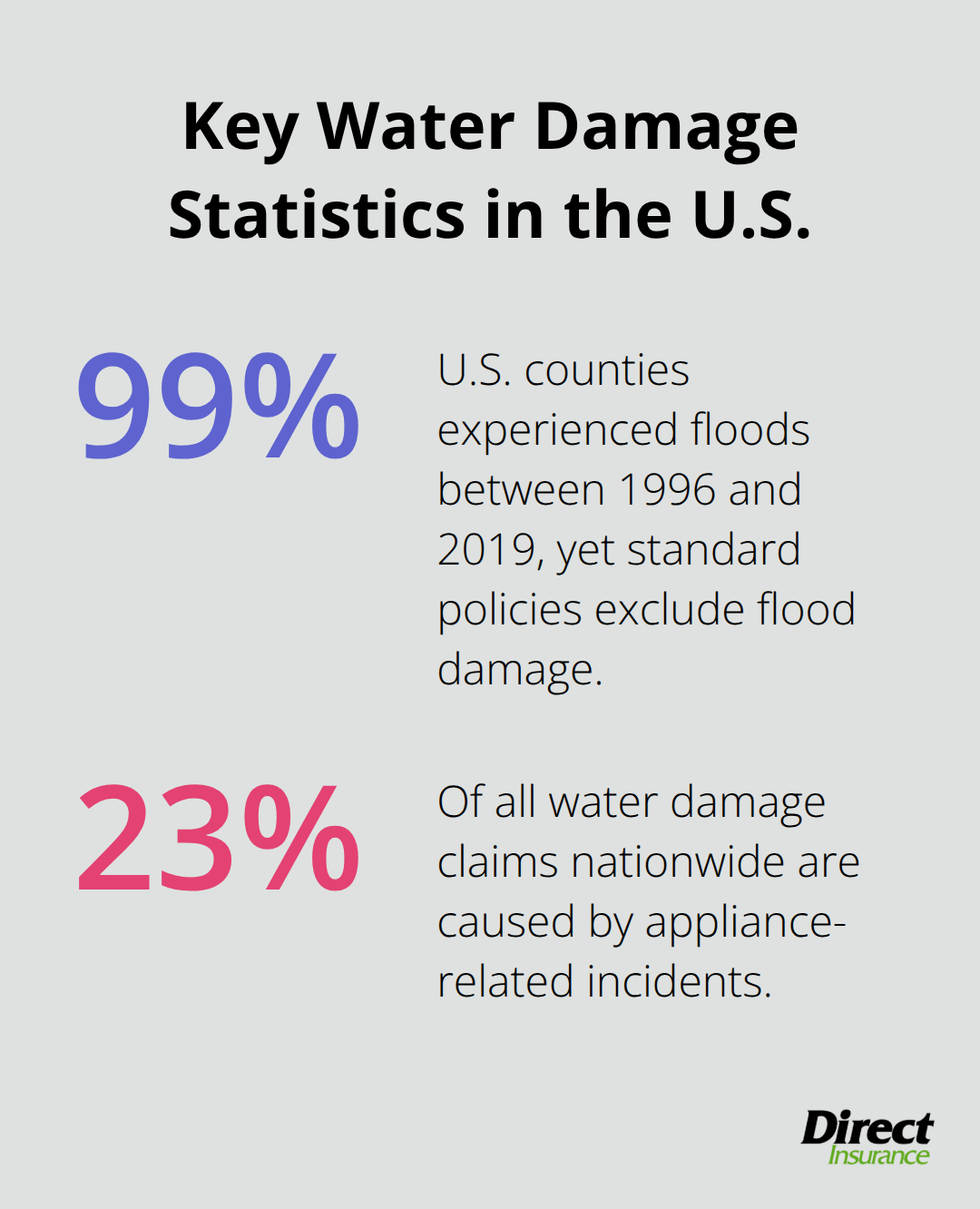

Wind-driven rain through storm-damaged roofs activates immediate coverage, but standing floodwater from rivers or storms requires separate flood insurance. The National Flood Insurance Program shows 99% of U.S. counties experienced floods between 1996 and 2019, yet standard policies exclude all flood damage.

Hail damage to roofs that allows water penetration receives coverage under your dwelling protection. Ice dam water damage from winter storms qualifies for claims, but gradual seepage from poor drainage does not qualify for compensation.

Major Exclusions That Create Coverage Gaps

Gradual leaks, maintenance issues, and floods represent the biggest coverage gaps that catch homeowners off guard. Sewer backups cost thousands but standard policies exclude them unless you purchase additional coverage (which many insurers offer as an endorsement).

Groundwater seepage through foundations falls outside standard coverage boundaries. Neglected maintenance like failure to heat your home properly during winter can void water damage claims entirely. Mold damage typically gets excluded unless it results from a covered water damage event.

Additional Coverage Options Worth Considering

Smart homeowners add sewer backup coverage for protection against costly drain failures. This endorsement typically costs $50-100 annually but covers thousands in potential damage. Flood insurance becomes essential in high-risk areas (even moderate-risk zones see significant flood events).

Water backup coverage protects against sump pump failures and drain overflows that standard policies exclude. These scenarios become increasingly common as Utah experiences more extreme weather patterns and infrastructure strain.

Most homeowners policies include sub-limits for personal property damaged by water, often ranging from 50-70% of your total personal property coverage. Your deductible applies to all water damage claims regardless of the source.

Now that you understand what your policy covers and excludes, let’s examine the specific water damage scenarios that Utah homeowners face most frequently.

What Water Damage Risks Do Utah Homes Face

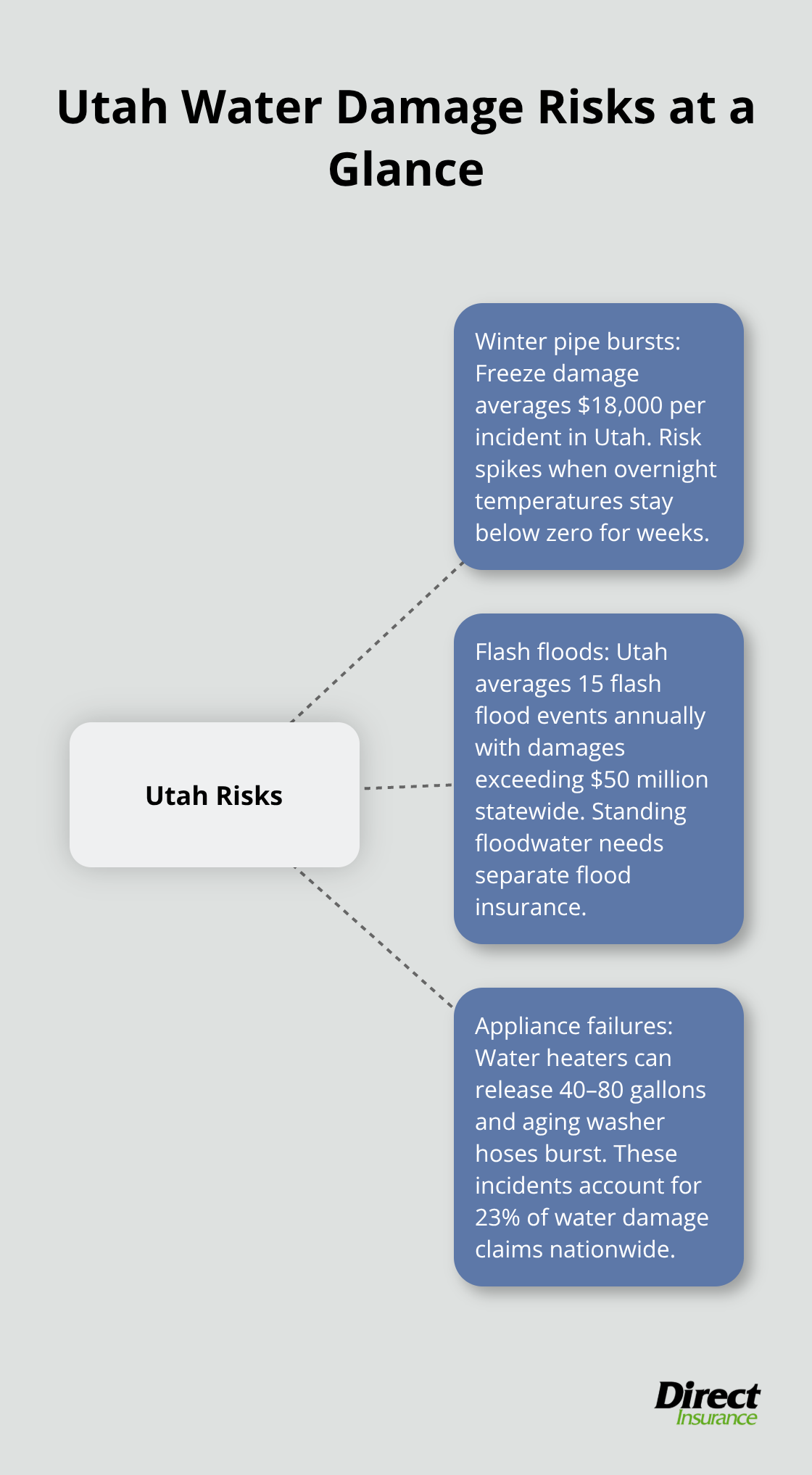

Utah homeowners confront three primary water damage threats that cost thousands in repairs annually. Winter freeze damage accounts for the highest claim frequency, with temperatures that drop below freezing and cause pipes to burst in unheated areas like crawl spaces and exterior walls. The Insurance Information Institute reports that freeze damage claims average $18,000 per incident, which makes winter preparation essential for Utah residents.

Winter Pipe Bursts Hit Utah Hardest

Pipes freeze when temperatures drop below freezing for extended periods, which happens frequently across Utah’s mountainous regions. Copper pipes in exterior walls fail first, followed by supply lines in unheated garages and basements. Most claims occur during January and February when overnight temperatures stay below zero for weeks. Homeowners who maintain interior temperatures below 65°F during vacations face the highest risk of pipe failures. The damage extends beyond initial water release, as burst pipes continue to flow until someone discovers the problem and shuts off the main water supply.

Flash Floods and Sudden Storm Damage

Utah’s mountainous terrain creates flash flood conditions that catch homeowners unprepared, especially in areas like Salt Lake County and Utah County where development sits near canyon mouths. The National Weather Service reports that Utah averages 15 flash flood events annually, with damages that exceed $50 million statewide. Spring snowmelt combined with sudden rainstorms overwhelms drainage systems and sends water through neighborhoods. Storm-driven rain through damaged roofs activates coverage immediately, but standing floodwater requires separate flood insurance that most Utah homeowners lack.

Appliance Failures Create Unexpected Claims

Water heaters fail without warning after 8-12 years of service and release 40-80 gallons of water into areas around them. Washing machine supply hoses burst under normal water pressure, especially in homes with older rubber hoses that homeowners should replace every five years. Dishwasher door seals deteriorate and leak gradually before they fail completely, which causes extensive floor damage that homeowners often miss until wood warps and becomes visible. These appliance-related incidents account for 23% of all water damage claims nationwide (according to the Insurance Information Institute).

Now that you understand the specific risks Utah homes face, let’s explore proven strategies to prevent these costly water damage scenarios from affecting your property.

How Can You Prevent Water Damage Before It Happens

Prevention beats expensive repairs every time, and smart homeowners take action before water damage strikes their homes. The American Society of Home Inspectors recommends annual roof inspections to catch missing shingles and damaged flashing before they create interior damage. Check your roof after every major storm and replace worn shingles immediately. Inspect plumbing connections under sinks, behind toilets, and around water heaters monthly for signs of moisture or corrosion. Household leaks can waste more than 1 trillion gallons annually nationwide, which shows how common undetected water problems become.

Smart Technology That Saves Thousands

Water detection systems pay for themselves after they prevent just one major leak incident. Install leak detectors near water heaters, washing machines, and under kitchen sinks where failures cause the most damage. Smart systems like Flo by Moen automatically shut off your main water supply when they detect unusual flow patterns. These devices cost $400-800 but prevent thousands in damage from burst pipes or appliance failures. Replace washing machine hoses every five years regardless of their appearance, as rubber deteriorates internally before visible cracks appear.

Winter Protection That Actually Works

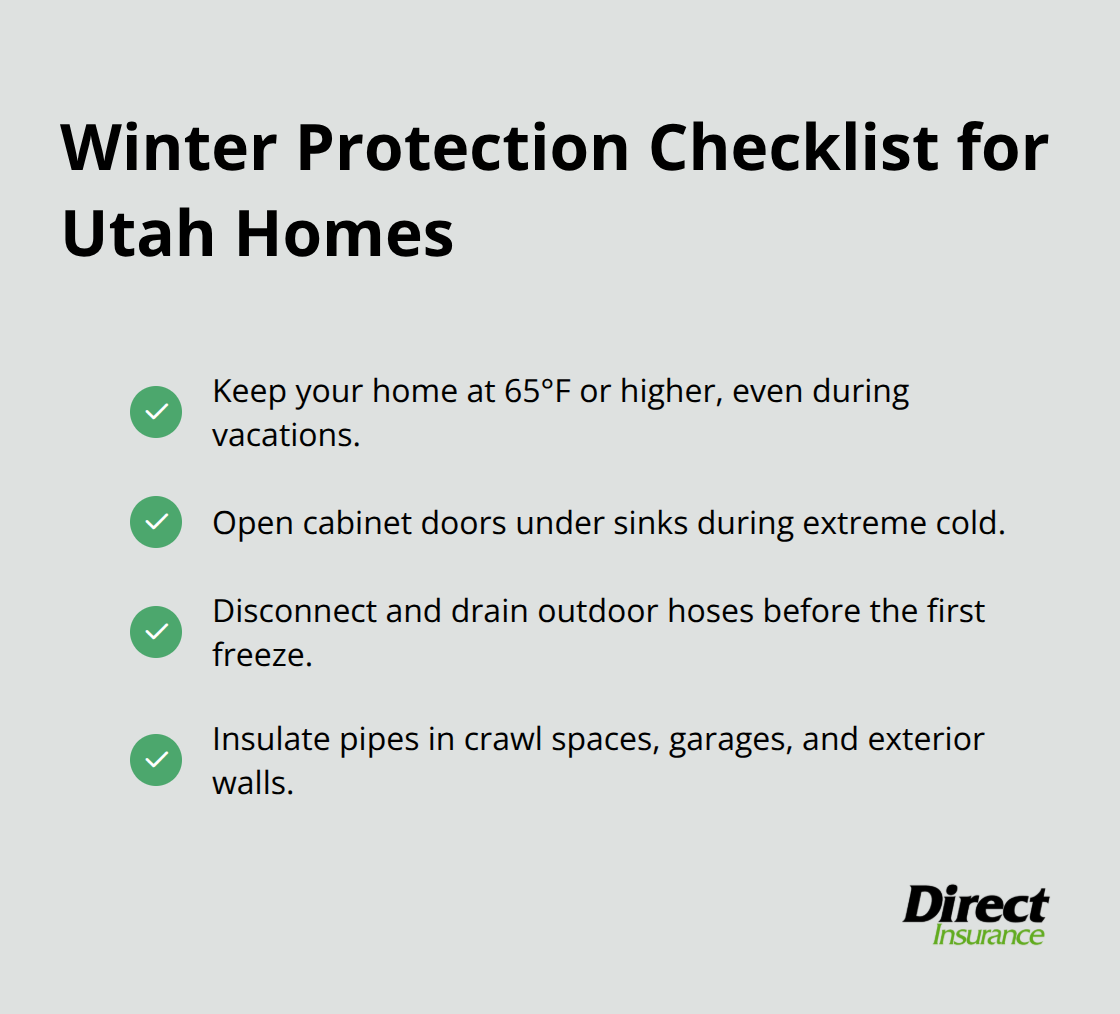

Maintain interior temperatures above 65°F even during vacations, as pipes freeze rapidly when homes drop below this threshold. Open cabinet doors under sinks during extreme cold snaps to allow warm air circulation around pipes. Disconnect and drain outdoor hoses before first freeze, as trapped water expands and cracks faucet connections. Insulate pipes in crawl spaces, garages, and exterior walls with foam pipe insulation that costs under $20 per 100 feet.

Essential Maintenance Tasks

Test your sump pump twice yearly by pouring water into the pit until the float activates the motor. Know your main water shutoff location and teach family members how to operate it quickly during emergencies. Clean gutters twice annually to prevent water overflow that damages foundations and exterior walls. Check caulking around bathtubs, showers, and windows annually (replacing deteriorated seals prevents gradual water penetration that standard insurance excludes).

Final Thoughts

Water damage protection demands proactive steps and proper coverage knowledge. Utah homeowners face specific risks from winter freezes, flash floods, and appliance failures that standard policies may not fully address. The average water damage claim costs $13,954, which makes prevention and adequate coverage essential for financial protection.

Review your current policy annually to identify coverage gaps, especially for sewer backups and flood protection. Most Utah homes need additional endorsements beyond standard coverage to protect against regional water damage risks. Document your home’s condition with photos and maintain detailed inventories of personal property to streamline future claims (this preparation saves time during stressful claim periods).

We at Direct Insurance Services understand Utah’s unique water damage challenges and help homeowners navigate complex home insurance and water damage coverage options. Our team shops multiple top-rated insurance companies to find comprehensive protection that fits your specific needs and budget. Take action now by scheduling a coverage review with Direct Insurance Services to identify potential gaps in your water damage protection before costly incidents occur.