Best Rated Auto and Home Insurance Providers

Finding the best rated auto and home insurance providers takes time and research. At Direct Insurance Services, we’ve analyzed the top carriers to help you understand what sets them apart-from premium costs to customer service ratings to claims speed.

This guide breaks down the leading providers across different needs, whether you’re looking for the lowest rates, specialized coverage, or bundled discounts. You’ll learn what metrics matter most and how to avoid common mistakes when comparing quotes.

Top-Rated Auto Insurance Providers in 2025

National Carriers with the Best Price and Service Balance

Travelers ranks as the top-rated auto insurer according to the J.D. Power 2025 U.S. Auto Insurance Study, which surveyed 48,121 customers over a full year. The study shows that overall auto insurance satisfaction averages 644 on a 1,000-point scale, indicating most customers feel dissatisfied with their current provider. Travelers delivers consistent satisfaction across the board, making it a reliable choice if you want to avoid frustration.

USAA ranks second nationally and serves military members, veterans, and their families with specialized coverage and bundling discounts. However, USAA restricts eligibility to those with military connections, making it unavailable to most consumers. For affordable premiums without military ties, Geico and Progressive consistently undercut competitors on base rates, though Progressive charged around 11% more in 2025 than in 2024 as auto insurance prices climbed across the industry.

State Farm rounds out the national tier with a massive agent network and bundling discounts when you combine auto and home policies. This discount makes State Farm attractive if you need both coverages from one carrier.

Regional Insurers That Outperform National Competitors

Regional carriers often beat national companies on customer satisfaction in their territories. Amica dominates New England with a 735 satisfaction score (the highest in the J.D. Power study) and offers bundling discounts across multiple policy types. Erie Insurance leads both the Southeast and North Central regions with 718 and 684 scores respectively, making it worth requesting quotes if you live in those areas.

The Mid-Atlantic region’s top performer is NJM Insurance Co. with a 721 score, while Shelter Insurance commands the Central region for the fifth consecutive year with a 673 score. These regional players succeed because they understand local risks and pricing patterns better than national carriers. The catch is availability: Erie operates in limited states, and NJM primarily serves the Mid-Atlantic, so you need to verify coverage in your location before requesting quotes.

Specialized Coverage for High-Risk Drivers

High-risk drivers face substantially higher premiums, but certain insurers specialize in this segment. Progressive explicitly targets senior drivers and those with recent violations or accidents, offering tailored discounts that can offset higher base rates. Nationwide leads the usage-based insurance segment with a 698 satisfaction score for the second consecutive year-if you share driving data through their mobile app, you can reduce premiums by proving safe habits.

Auto-Owners attracts drivers with recent claims or speeding tickets by focusing on comprehensive endorsements like inland flooding and cybersecurity coverage. For your situation, shopping at least three quotes reveals whether a specialist’s discounts beat your current premium, since high-risk rates vary significantly across carriers based on their underwriting appetite. This comparison process sets the stage for understanding how home insurance providers approach similar risk assessment and pricing strategies.

Top-Rated Home Insurance Providers in 2025

Amica, USAA, and State Farm Lead the Market

Amica leads the homeowners insurance rankings with the lowest sample premium at approximately $96.98 per month, according to U.S. News’ 2025 analysis based on Quadrant Information Services data and a survey of 1,125 homeowners. Amica’s strength lies in its consistent claims handling and service scores, making it the safest choice if you prioritize reliability over specialized coverage options. However, Amica isn’t available in Alaska or Hawaii, so verify eligibility before requesting a quote.

USAA ranks second for homeowners and offers military-specific benefits like uniform coverage for active duty and reserve members, averaging around $129.67 per month. State Farm sits third with competitive rates near $129.02 per month and remains accessible to those with lower credit scores in most states, though it stopped accepting new homeowners policies in California, Massachusetts, and Rhode Island.

Specialized Coverage and Higher-End Options

Chubb delivers the most comprehensive coverage through its Masterpiece policy, which includes replacement cost, water backup, and ordinance and law coverage at approximately $154.05 per month, but requires agent quotes and typically costs more than competitors. Auto-Owners attracts homeowners with recent claims or problematic histories by offering inland flooding and cybersecurity endorsements at around $141.17 per month, available in 26 states through agent-based quotes.

Bundle Discounts That Actually Save Money

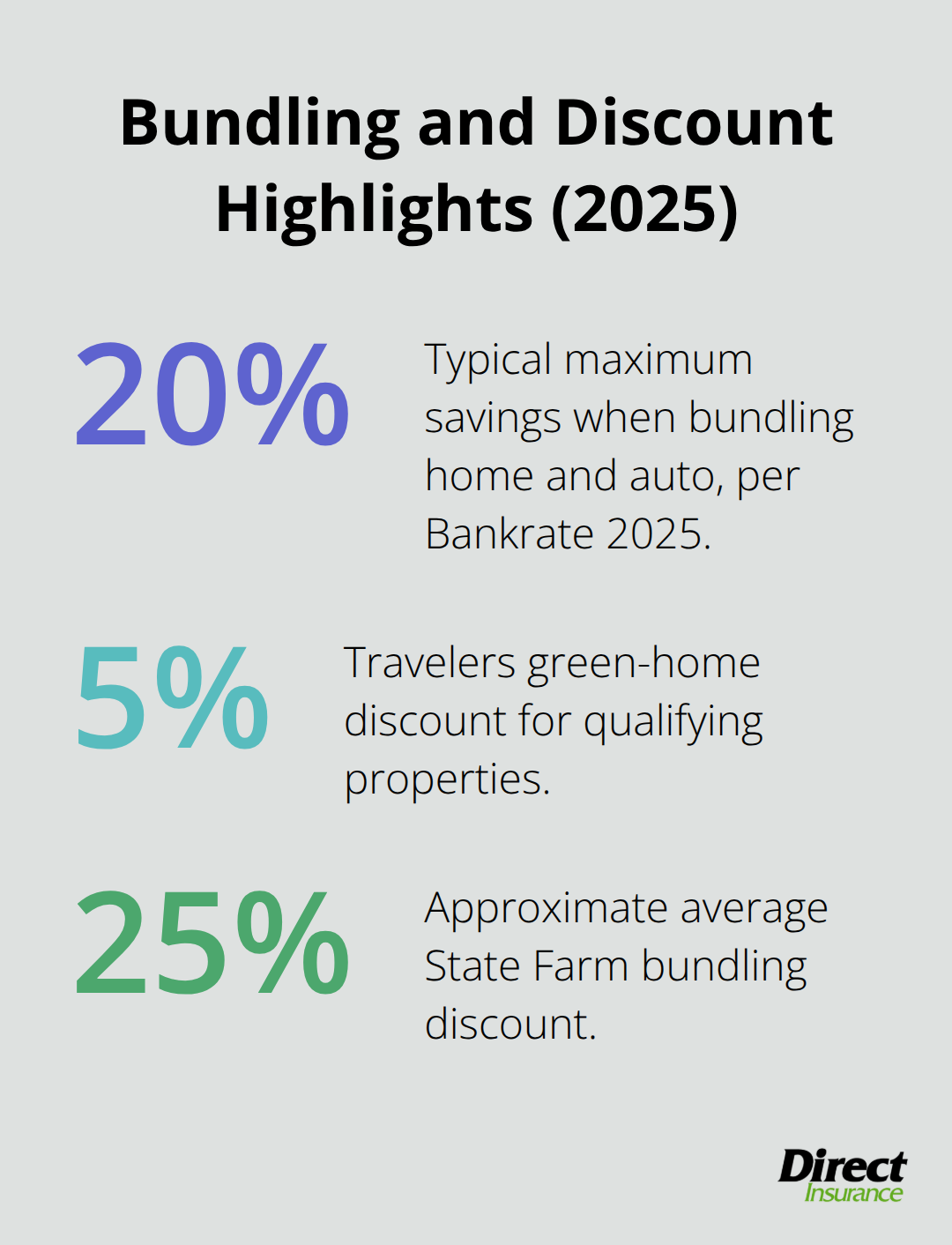

Bundling home and auto insurance typically saves up to 20 percent on combined premiums according to Bankrate’s 2025 analysis. State Farm offers competitive bundling discounts when combining auto and home, while Travelers provides home and auto discounts alongside a 5 percent green-home discount for eco-friendly properties.

Nationwide was named Best for Bundling Home and Auto in the 2025 Bankrate Awards and features its On Your Side annual policy review to optimize coverage. When comparing bundles, obtain quotes from at least three providers using identical coverage limits and deductibles to accurately assess discounts, since one insurer rarely offers the cheapest rates across both lines.

How to Switch Without Coverage Gaps

Pro-rated refunds typically apply if you cancel existing policies early, so align start dates carefully to avoid coverage gaps and notify your mortgage lender about any homeowners insurance switch. The comparison process matters more than brand loyalty: bundling can reduce premiums significantly, but separate policies from different carriers sometimes cost less than bundled options, particularly if your auto insurer’s home rates run higher than regional competitors in your area.

This foundation of understanding top home insurance providers and bundling mechanics prepares you to evaluate which carriers truly fit your situation. The next section walks you through the specific metrics that separate quality providers from mediocre ones.

Comparing Quotes and Spotting the Best Deals

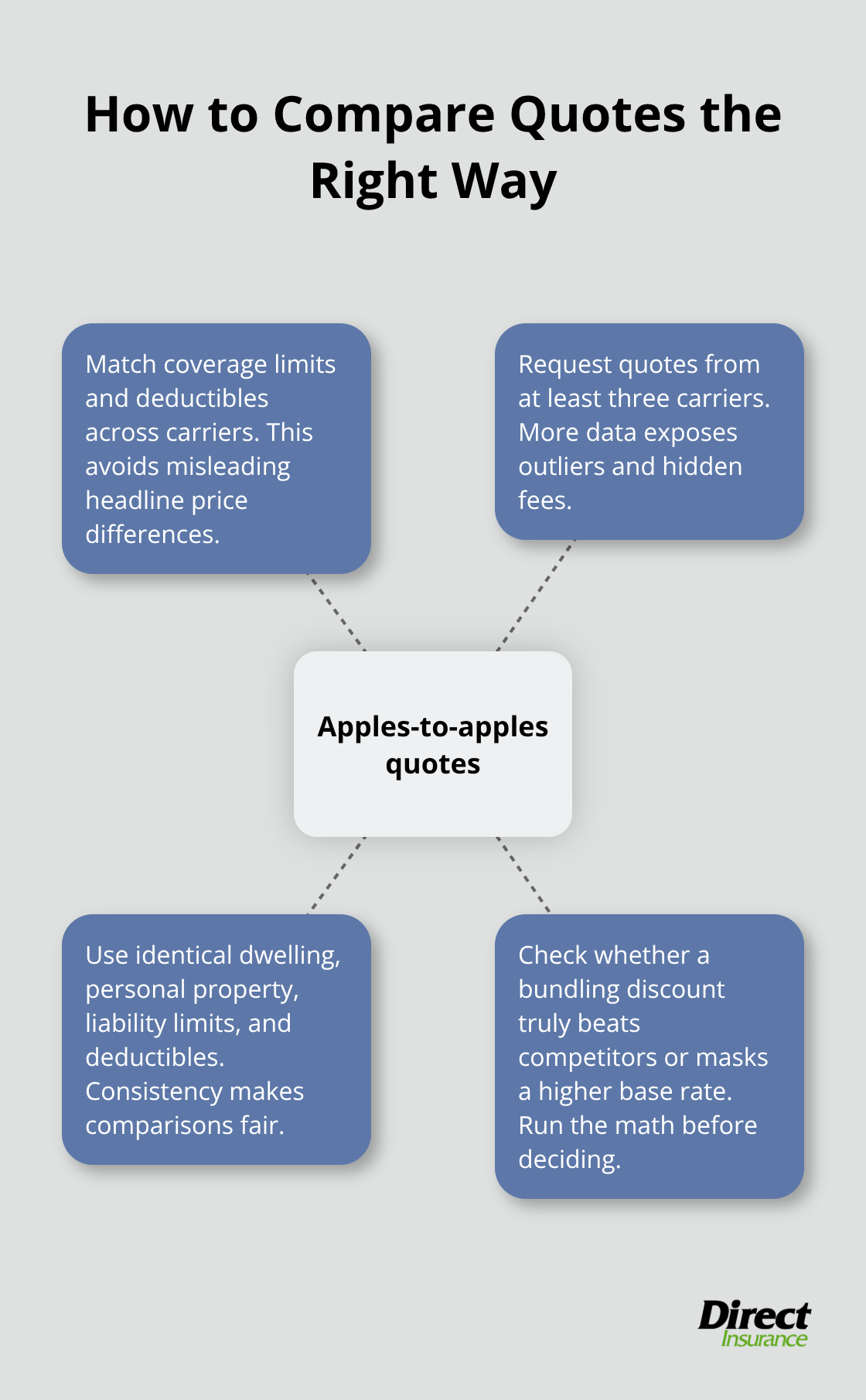

Match Coverage Limits Across Carriers

Accurate quotes require matching coverage limits and deductibles across carriers, not just comparing headline numbers. Most people request quotes from two insurers and stop, but the J.D. Power 2025 U.S. Auto Insurance Study reveals that 38 percent of auto insurance customers feel dissatisfied with their current provider, often because they never shopped properly in the first place. Request quotes from at least three carriers using the exact same dwelling replacement cost, personal property limits, liability limits, and deductibles.

This apples-to-apples comparison shows whether a carrier’s bundling discount actually beats competitors or simply masks a higher base rate.

Bankrate’s 2025 bundling analysis found that bundling discounts range from about 10 percent to 25 percent depending on the insurer, but bundling from the cheapest base-rate carrier sometimes costs less than bundling from an expensive one offering a larger percentage discount. For example, Allstate offers up to 25 percent bundling discounts, while Amica’s bundling reaches 30 percent, yet Amica’s sample home premium sits around $96.98 monthly versus Allstate’s $143.95. The math matters more than the discount percentage.

Identify Red Flags Before You Commit

Avoid carriers that won’t provide online quotes or require agent contact before showing pricing, since opacity often signals higher costs or limited availability in your area. State Farm stopped accepting new homeowners policies in California, Massachusetts, and Rhode Island, so verify your state’s eligibility before investing time in quotes. Check J.D. Power’s regional satisfaction data before selecting a provider, particularly if you live in a region where a specialist outperforms nationals.

Amica scores 735 in New England, Erie Insurance hits 718 in the Southeast, and Shelter Insurance dominates the Central region with a 673 score after five consecutive years leading that territory. If your region’s leader isn’t available to you, pick the national carrier ranking highest in your area rather than defaulting to brand recognition. Watch for carriers that bundle aggressively but lack strong claims satisfaction scores. Travelers ranks number two nationally for auto insurance and offers bundling discounts alongside a five percent green-home discount, making it a legitimate choice if your quotes land competitively. Progressive and Geico undercut on base rates but sometimes handle claims through networks of independent adjusters rather than direct employees, which can slow processing. Review NAIC complaint data for any carrier you’re seriously considering, since complaint ratios reveal whether price comes at the expense of claims service.

Calculate Total Costs to Find the Real Winner

Bundling saves approximately 20 percent on combined premiums according to Bankrate’s analysis, but only if you compare the bundle against your current separate policies. If you already pay $80 monthly for auto and $120 monthly for home, a 20 percent bundle discount saves roughly $40 per month. However, if that same bundled package costs $175 monthly while separate quotes from other carriers run $85 and $105, the bundle loses.

Request quotes for bundled policies and for each line separately from different carriers, then calculate total costs to identify the real winner. State Farm offers around a 25 percent bundling discount on average, making it worth requesting quotes if you need both auto and home. Nationwide features its On Your Side annual policy review, which means an agent reviews your coverage yearly to catch gaps or over-insurance without charging extra fees. This service appeals to people who set policies once and forget them, though it only matters if you actually use it.

Reassess After Major Life Changes

Life events like marriage, moving, or a new vehicle can change which bundle offers the best value, so re-shop after major changes rather than assuming your current bundle remains optimal. Bankrate found that bundling discounts and availability vary significantly by state, so a carrier ranked highly nationally might offer weak discounts in your location due to local competition or regulatory factors.

Final Thoughts

The best rated auto and home insurance providers match coverage to your actual needs rather than push unnecessary add-ons. Amica leads homeowners insurance with the lowest premiums and strongest claims satisfaction, while Travelers ranks first for auto insurance nationally. Your coverage needs depend on your home’s replacement cost, your driving habits, and your financial ability to absorb losses through higher deductibles-a driver with a clean record and a paid-off home can afford higher deductibles and skip optional coverages, while someone with recent claims or a mortgage needs comprehensive protection.

Bundling typically saves around 20 percent on combined premiums, but only if you compare the bundle against separate quotes from different carriers. State Farm’s 25 percent bundling discount sounds attractive until you discover that Amica’s base home rate costs $47 less monthly, making separate policies cheaper overall. Request quotes from at least three carriers using identical coverage limits and deductibles to identify which approach saves you the most money.

We at Direct Insurance Services shop multiple top-rated insurance companies on your behalf to find the coverage and rates that fit your budget and protect what matters most. As locals in Utah since 1973, we understand the unique risks of living here and can explain why certain endorsements make sense for your situation while others waste money. Contact us to get personalized quotes without the hassle of calling multiple carriers yourself.