Tech Company Insurance Utah: Protecting Innovation

Utah’s tech sector is booming, but rapid growth brings real risks. Data breaches, lawsuits, and equipment failures can derail even the most innovative companies.

At Direct Insurance Services, we’ve seen firsthand how the wrong coverage-or no coverage at all-can devastate a tech business. Tech company insurance in Utah isn’t one-size-fits-all, which is why we’ve put together this guide to help you protect what you’ve built.

Why Tech Companies Face Different Insurance Challenges

The Wasatch Front Risk Environment

Utah tech companies operate in an environment where traditional business insurance falls short. The Wasatch Front tech corridor-spanning Salt Lake City, Provo, and Ogden-concentrates software firms, cloud service providers, and digital innovators that face threats far beyond what standard policies cover. Companies in this region handle sensitive client data, manage complex systems, and operate across multiple jurisdictions, creating exposures that generic business policies simply don’t address.

The True Cost of Data Breaches

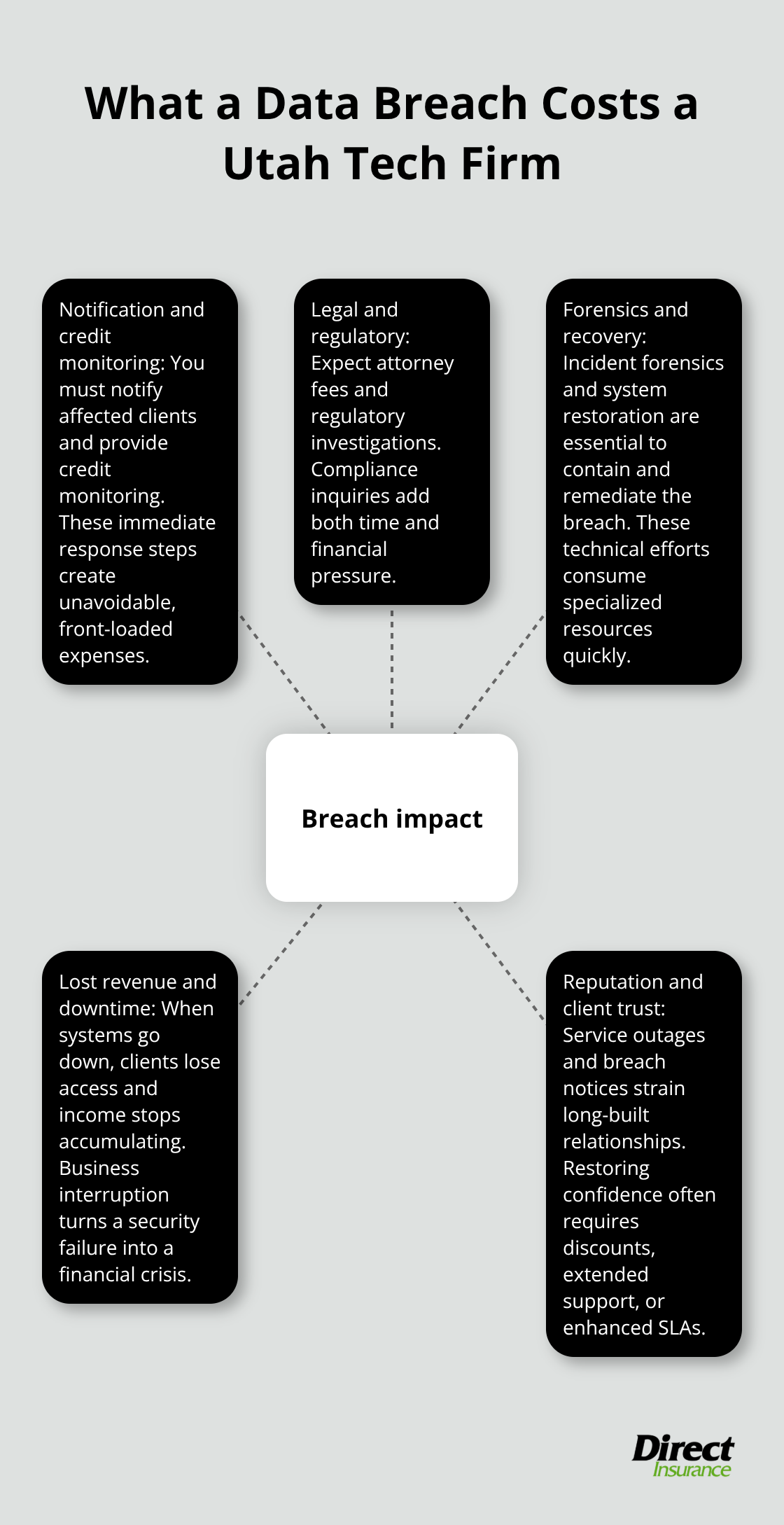

A data breach at a mid-sized Utah tech company triggers notification costs, credit monitoring, legal fees, and regulatory investigations. These aren’t theoretical numbers; they reflect the real financial exposure that tech businesses encounter when security fails. Cyber incidents also interrupt revenue streams instantly-when your systems go down, clients can’t access your service, and income stops accumulating.

Standard business insurance doesn’t compensate for this lost revenue, which means a single ransomware attack or network compromise can wipe out months of profit margins.

Professional Liability and Service Failures

Professional liability presents another distinct threat. If your software fails and damages a client’s operations, if your IT consulting creates compliance violations, or if your custom application causes data loss, the client will sue. These errors and omissions claims often reach six figures because they involve downstream business losses, not just direct damages. Tech firms that work across state lines or internationally face additional exposure when their mistakes trigger regulatory investigations or compliance violations.

Coverage That Matches Your Actual Operations

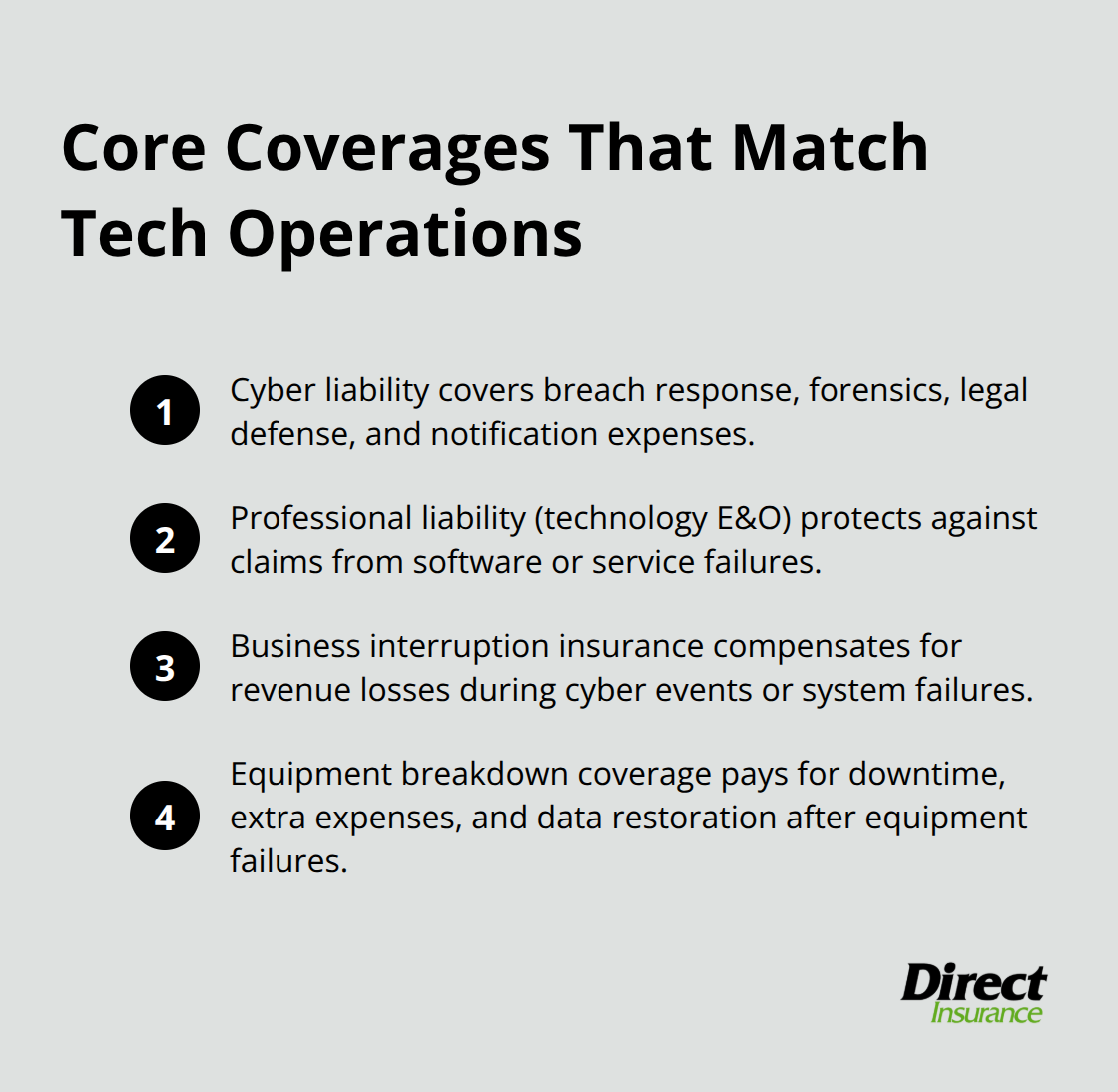

The insurance industry recognizes that tech firms need coverage tailored to their actual operations. Cyber liability policies now cover breach response, forensic investigation, legal defense, and notification expenses-costs that emerge immediately after an incident. Professional liability, sometimes called technology errors and omissions, protects against claims tied to mistakes or failures in your software or services.

Business interruption insurance compensates for revenue losses when cyber events or system failures interrupt normal operations. Equipment breakdown coverage extends protection beyond standard property policies, covering downtime and extra expenses from equipment failures.

Regulatory Compliance and Cost Realities

Utah tech companies that handle multi-state or international client data should prioritize policies addressing CCPA, GDPR, and HIPAA compliance, plus regulatory fines coverage. A small software startup with roughly $500,000 in revenue typically pays $2,000 to $4,000 annually for cyber and professional liability combined. A firm generating $5 million in revenue usually pays between $8,000 and $15,000. These costs reflect the genuine protection needed; skipping this coverage or under-insuring creates catastrophic exposure that no growth trajectory can absorb. Understanding your specific coverage needs and comparing options from multiple carriers helps you avoid both over-insurance and dangerous gaps in protection.

What Coverage Do Utah Tech Companies Actually Need

Cyber Insurance: Your First Line of Defense

Cyber insurance sits at the top of your protection stack, and it’s non-negotiable for Utah tech firms. First-party cyber coverage handles your costs when a breach happens: forensic investigation, legal defense, breach notification, credit monitoring, and regulatory investigation expenses. Third-party cyber liability protects you when clients or end-users suffer harm from your security failures and sue for damages. A mid-sized Utah tech company should target cyber insurance limits between $1 million and $5 million depending on client data volume and revenue. The cost varies significantly by your security posture, but firms with $5 million in revenue typically pay $8,000 to $15,000 annually for cyber coverage combined with professional liability. Carriers now scrutinize your actual security controls before quoting, so companies using multi-factor authentication, encryption, and regular security audits pay substantially less than those with basic protections.

Professional Liability Claims and Real Exposure

Professional liability, also called technology errors and omissions, covers claims when your software fails, your IT consulting creates compliance violations, or your custom application causes a client’s data loss. These claims routinely exceed six figures because they involve the client’s downstream business losses, not just direct damages. A SaaS platform outage that causes a client to lose customer data can trigger claims in the $500,000 to $2 million range. Technology E&O policies typically offer limits up to $5 million for firms handling mission-critical systems. This coverage also includes defense costs, which means the insurer pays your legal fees even if the claim proves baseless. Firms working across multiple states or internationally absolutely need this protection because a single mistake affecting clients in California, Colorado, and Utah multiplies exposure across different regulatory frameworks and damage calculations.

General Liability and Property Protection

General liability covers bodily injury and property damage claims from your operations, while commercial property insurance protects your on-site equipment, servers, and office fixtures from fire, theft, and other perils. Utah tech companies often overlook business interruption insurance, which compensates for revenue losses when cyber events or equipment failures stop operations. If ransomware locks your systems for two weeks, business interruption coverage pays for lost income during that downtime, not just the cost to recover systems. Equipment breakdown coverage extends beyond standard property policies to cover downtime and extra expenses from equipment failures, including costs to restore data and rent temporary equipment.

Building a Complete Protection Strategy

A complete protection strategy combines these coverages because a single incident often triggers multiple losses simultaneously. Investors and lenders increasingly mandate cyber and professional liability coverage, sometimes requiring $2 million to $5 million in limits, particularly for firms handling regulated data or serving multi-state clients. These requirements reflect the genuine financial exposure that tech companies face when incidents occur. Understanding which coverages apply to your specific operations and revenue level helps you avoid both over-insurance and dangerous gaps in protection. The next section walks through how to find an insurance partner in Utah who understands these tech-specific needs and can compare options from multiple carriers to match your actual risk profile.

How to Find the Right Insurance Partner for Your Tech Business

What Your Insurance Agent Must Understand

Your insurance agent needs to understand both the tech industry and Utah’s specific business environment. Generic insurance brokers who treat tech firms like retail shops will miss critical exposures and recommend coverage that doesn’t match your actual operations. The agent you choose should ask detailed questions about your software architecture, client data types, geographic reach, and revenue model before quoting anything. They should also recognize that coverage needs will shift as you scale. A startup with five employees and $500,000 in revenue has vastly different exposures than a $5 million firm with thirty employees and clients across multiple states. An agent who doesn’t revisit your coverage during quarterly or semi-annual reviews as you grow will leave you either over-insured or dangerously under-protected. Quarterly policy reviews during high-growth phases matter because your headcount, services, and revenue change faster than most traditional businesses, and your insurance should change too.

Access to Multiple Carriers Matters

The second critical factor is access to multiple carriers and the willingness to compare them side-by-side. Avoid agents who represent a single insurance company or who push their house policies without showing alternatives. Independent agencies can access 15 or more A-rated carriers and pull real quotes from each one, letting you see the actual cost differences and coverage variations across providers. Some carriers specialize in technology risks and offer better rates for firms with strong security controls like multi-factor authentication and encryption. Others focus on specific tech sectors like SaaS, digital media, or IT consulting.

When you request quotes, provide the same detailed information to each carrier so comparisons are meaningful. Ask your agent to explain exactly which coverages differ between quotes and why the pricing varies. A $2,000 annual premium difference between two cyber policies might reflect different breach response limits, different regulatory investigation coverage, or different deductibles. Understanding those differences prevents you from selecting cheap coverage that leaves you exposed when incidents occur.

Demand Plain-Language Policy Reviews

Request plain-language policy reviews before you commit to any coverage. Your agent should walk through what’s actually covered, what’s excluded, and what gaps remain unfilled. Ask about retroactive date options and tail coverage if you’ve had past client work, because claims from old projects can surface years later and destroy your business if you lack proper protection. Request that your agent explain the deductible structure, what triggers coverage, and what documentation you’ll need to file a claim. Tech founders often skip this step because they’re eager to move forward, but investing two hours in a thorough policy review prevents catastrophic surprises when you actually need the coverage to work.

Conclusion

Tech company insurance in Utah protects what you’ve built and enables the innovation that drives your business forward. The coverage gaps we’ve outlined throughout this guide aren’t theoretical risks-they’re exposures that destroy companies every year. A data breach, a professional liability claim, or an equipment failure eliminates months of revenue and damages client relationships that took years to establish.

Building long-term business resilience means treating insurance as a strategic business decision, not an administrative checkbox. Your coverage should evolve as your company scales, with quarterly reviews during growth phases to keep cyber liability, professional liability, and business interruption protection aligned with your actual operations. Investors and lenders increasingly mandate these protections anyway, so securing proper coverage now positions you for future funding rounds and partnership opportunities.

Contact an independent agency that understands Utah’s tech environment and can compare quotes from multiple carriers. At Direct Insurance Services, we’ve been serving Utah businesses since 1973, and we specialize in shopping multiple top-rated insurance companies to find the coverage that matches your specific needs and budget. Reach out to Direct Insurance Services today for a tech company insurance Utah quote, and we’ll help you build the protection your business needs to keep innovating without exposure.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation