Finding the Best Business Insurance in Salt Lake City

Salt Lake City businesses face unique insurance challenges, from winter weather risks to Utah’s specific regulatory requirements. Many entrepreneurs struggle to navigate the complex world of commercial coverage options.

We at Direct Insurance Services understand that choosing the right business insurance Salt Lake City providers offer can make or break your company’s financial security. Smart coverage decisions protect your investment and keep operations running smoothly.

What Coverage Does Your Salt Lake City Business Actually Need

Salt Lake City businesses require three non-negotiable insurance types that directly address Utah’s regulatory landscape and climate challenges. General liability insurance stands as your first line of defense, with Utah businesses paying a median of $45 monthly according to industry data. This coverage protects against third-party injury claims and property damage lawsuits that can devastate small companies. Commercial leases in Salt Lake City typically mandate this coverage, making it a business requirement rather than an option.

Workers Compensation Remains Mandatory for Utah Employers

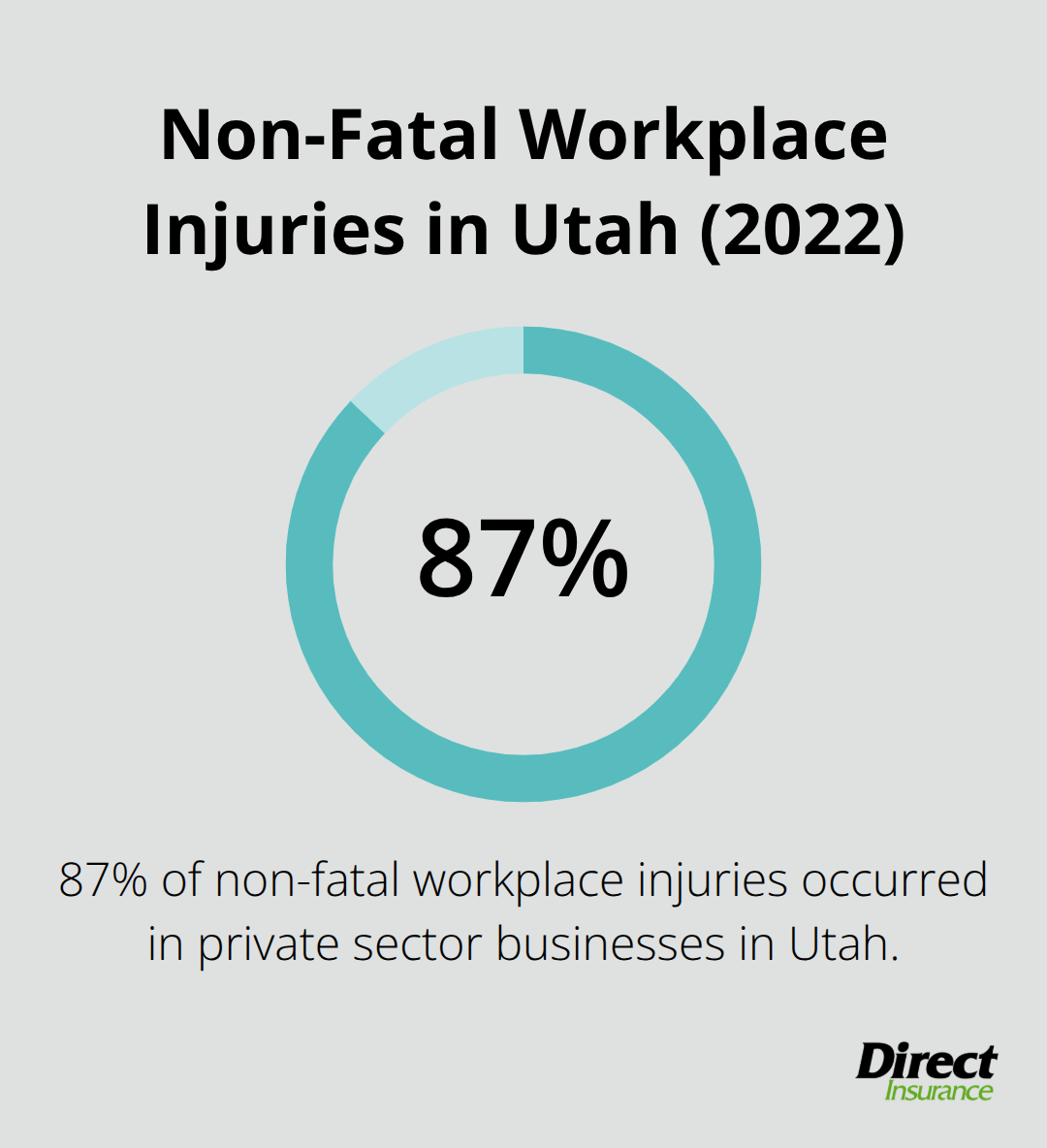

Utah law requires all businesses with employees to carry workers compensation insurance (with a few exceptions). The state reported 31,700 non-fatal workplace injuries in 2022, with 87% occurring in private sector businesses according to Bureau of Labor Statistics data. Construction companies face the highest risk, paying median premiums of $63 monthly, while fitness businesses enjoy lower rates at $15 monthly. Utah’s tiered system covers temporary and permanent disabilities from job-related injuries, protecting both employees and employers from devastating medical costs.

Commercial Property Insurance Addresses Utah’s Weather Extremes

Salt Lake City’s harsh winters, summer storms, and seismic activity create unique property risks that standard coverage often overlooks. Utah’s climate demands specialized protection for equipment damage from temperature fluctuations and weather-related business interruptions. Smart business owners bundle commercial property insurance with general liability through Business Owner’s Policies (achieving up to 25% savings) while addressing Utah-specific environmental challenges that can shut down operations for weeks.

Professional Liability Protects Service-Based Businesses

Professional liability insurance, also known as errors and omissions coverage, protects Utah businesses that provide professional services against claims of work-related negligence. Utah businesses pay approximately $75 monthly for this coverage according to industry data. This protection becomes essential when clients suffer financial losses and blame your professional advice or services. Many professional licenses in Utah require this coverage, particularly in real estate and legal services sectors.

The next step involves evaluating which Salt Lake City insurance providers can deliver these essential coverages at competitive rates.

Which Salt Lake City Insurance Provider Should You Choose

Salt Lake City business owners must decide between local independent agencies and national insurance chains, with local agencies consistently delivering superior outcomes for Utah-specific risks. Independent agencies shop multiple carriers simultaneously and secure coverage from top-rated companies at competitive rates rather than push single-company products. Local agents understand Utah’s regulatory landscape, winter weather challenges, and seismic risks that national call centers miss entirely. The Yelp ratings for top Salt Lake City insurance agencies show several local firms achieve perfect scores, while national chains struggle with standardized approaches that ignore regional business needs.

Response Times Separate Strong Providers from Weak Ones

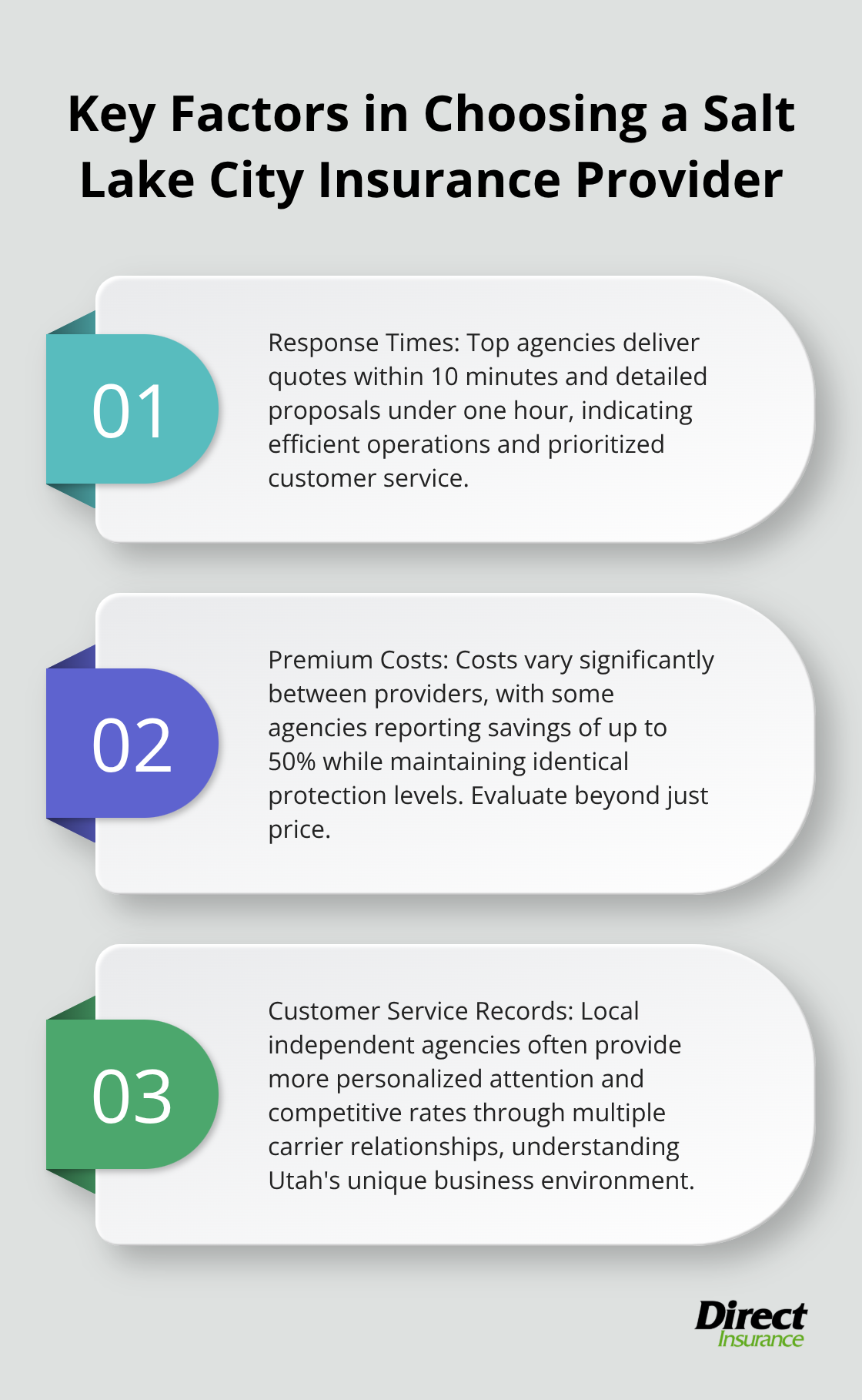

Salt Lake City insurance agencies deliver quotes within 10 minutes on average, with detailed proposals that arrive under one hour according to local market data. Fast response times indicate efficient operations and prioritized customer service, while slow providers often lack adequate staff or systems. We recommend that you request quotes from three local agencies and measure their response speed, thoroughness, and follow-up communication. Agencies that offer virtual consultations provide additional convenience for busy business owners, though face-to-face meetings remain valuable for complex coverage discussions.

Premium Costs Vary Dramatically Between Providers

Premium costs vary significantly between providers, with some agencies that report savings of 50% compared to previous coverage while they maintain identical protection levels. Utah business insurance costs reflect comprehensive health coverage premiums that average per member monthly rates across commercial markets, but premium prices alone mislead business owners about true value. Construction companies pay higher median premiums due to increased injury risks, while fitness businesses enjoy lower rates that reflect reduced liability exposure. Smart business owners evaluate claims speed, agent accessibility, and policy adjustment flexibility before they compare prices.

Customer Service Records Reveal Long-Term Provider Quality

State Farm and Farmers Insurance maintain strong customer satisfaction ratings in Salt Lake City, though independent agencies often provide more personalized attention and competitive rates through multiple carrier relationships. Direct Insurance Services stands out among local independent agencies, with a history that dates back to 1973 and deep Utah market knowledge. Local agents build long-term relationships and understand how Utah’s unique business environment affects coverage needs, while national chains rely on standardized scripts that miss regional nuances.

Most Salt Lake City entrepreneurs make critical mistakes when they select business insurance, which leads to coverage gaps and unnecessary expenses.

What Critical Insurance Mistakes Are Utah Entrepreneurs Making

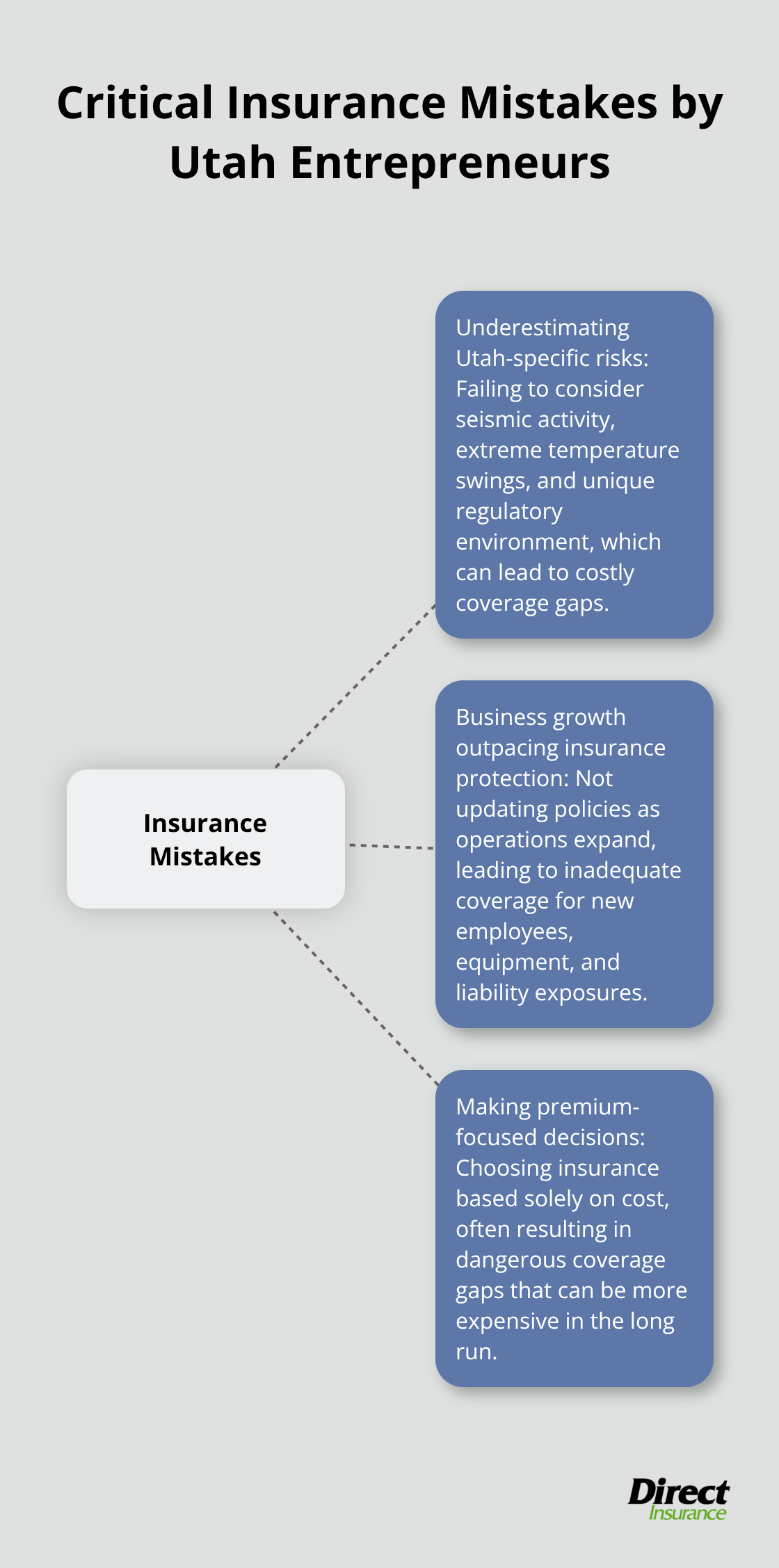

Salt Lake City business owners consistently make three expensive mistakes that expose them to devastating financial losses and regulatory violations. The most damaging error involves underestimation of Utah-specific risks that standard policies ignore completely. Utah’s seismic activity, extreme temperature swings, and unique regulatory environment create coverage gaps that cost businesses thousands when disasters strike. Construction companies that operate near the Wasatch Fault line need specialized earthquake coverage, while businesses in Salt Lake Valley must protect against inversions that can halt operations for days. The state’s rapid growth rate means businesses face increased liability exposure from higher foot traffic and congested commercial areas that amplify accident risks. Most policies include a 30-day waiting period before coverage becomes active, which means businesses can’t get insured the moment tremors start.

Business Growth Outpaces Insurance Protection

Utah ranks as the nation’s fastest-growing state with nearly 573,000 small businesses that employ close to half the workforce (according to Salt Lake Tribune data), yet most entrepreneurs never update their policies as operations expand. Addition of employees triggers mandatory workers compensation requirements, while new equipment demands higher property coverage limits that original policies cannot handle. Businesses that start in home offices and move to commercial spaces face entirely different liability exposures that basic policies miss. Revenue growth often pushes companies into higher risk categories that require professional liability coverage, especially service-based businesses that provide advice or consultation.

Premium-Focused Decisions Create Dangerous Gaps

Selection of insurance based solely on premium costs creates dangerous coverage gaps that cost more than comprehensive protection when claims occur. Cheap policies typically exclude Utah-specific risks like earthquake damage, winter weather interruptions, and cyber liability protection that businesses desperately need. The median business insurance cost in Utah is $46 monthly, but construction companies pay $63 while fitness businesses pay just $15 based on actual risk exposure levels. Low-cost providers often delay claims processing and provide minimal customer service when businesses need support most. Professional liability claims average thousands in defense costs alone, which makes the $75 monthly premium for errors and omissions coverage look insignificant compared to potential lawsuit expenses.

Policy Review Neglect Compounds Risk Exposure

Most Utah business owners purchase insurance once and forget about annual policy reviews that could save money and improve coverage. Market conditions change rapidly, with new insurance products that address emerging risks like cyber attacks and supply chain disruptions. Businesses that skip annual reviews miss opportunities to bundle policies for savings up to 25% or adjust deductibles based on improved cash flow. Claims history affects future premium rates, yet many entrepreneurs fail to implement safety measures that could reduce their risk profile and lower costs over time.

Final Thoughts

Salt Lake City business owners must take three strategic steps to protect their companies from Utah’s unique risks and regulatory requirements. You need general liability, workers compensation, and commercial property insurance that meet state mandates and address local climate challenges. Multiple quotes from local providers help you compare coverage options, premium costs, and response times within minutes.

Local Utah insurance experts deliver better results than national chains that overlook regional challenges. Independent agencies shop multiple carriers and understand earthquake risks, winter weather threats, and Utah’s regulatory landscape that affect your coverage needs. Direct Insurance Services has served the Salt Lake City market with personalized service and competitive rates through relationships with top-rated insurance companies.

Schedule consultations with three local agencies to evaluate their response speed, coverage recommendations, and premium quotes for your business insurance Salt Lake City needs. Review your policies annually to capture savings opportunities and adjust coverage as your company expands. Smart entrepreneurs choose comprehensive protection over cheap premiums to avoid devastating coverage gaps when claims happen (and they will happen eventually).