Liability Insurance Auto Coverage Explained

Most states require you to carry liability insurance auto coverage by law. Without it, you risk paying thousands out of pocket if you cause an accident.

At Direct Insurance Services, we help drivers understand exactly what liability coverage protects and how much they actually need. This guide breaks down the types of coverage, limits, and how to pick the right policy for your situation.

What Liability Coverage Actually Protects

Liability auto coverage pays for injuries and property damage you cause to other people when you’re at fault in an accident. It covers their medical bills, lost wages, pain and suffering, and legal fees if they sue you. It also covers damage to their vehicle, home, fence, or any other property. Your own injuries or vehicle damage fall outside this coverage-collision and comprehensive coverage handle those losses instead. The stakes matter because a serious accident can easily produce medical bills and repair costs exceeding $100,000. Without adequate liability coverage, you’d pay the difference from your own pocket, which could mean wage garnishment, asset seizure, or bankruptcy.

State Requirements Vary, But Coverage Is Nearly Universal

Almost every state requires you to carry liability coverage to drive legally. The minimum amounts differ by state, but most states require at least $15,000 to $25,000 per person for bodily injury and $10,000 to $25,000 for property damage. Louisiana, for example, requires $15,000/$30,000/$25,000, while California requires $15,000/$30,000/$5,000. These minimums, however, are dangerously low. Bodily injury claim severity rose 9.2 percent year over year in 2024, and the average bodily injury claim paid out $28,278. A single serious accident can blow past state minimums instantly. Most drivers who shop their policies-over 45 percent did so in 2024-choose limits of $100,000/$300,000 or higher because they understand that state minimums leave them exposed. If you cause an accident where damages exceed your policy limits, you’re personally liable for the rest. That’s why you should review your specific state’s requirements and then choose limits well above the minimum.

Why Your Assets Matter More Than You Think

The real question isn’t what your state requires-it’s what your net worth demands. Insurance protects your assets. If you own a home, vehicles, savings, or retirement accounts, your liability limits should match or exceed your total net worth. A $28,278 average bodily injury claim is just an average; catastrophic injuries can result in claims exceeding $500,000 or even $1,000,000. If your policy only covers $50,000 and the judgment is $500,000, the plaintiff can go after your paycheck, your house, and your bank accounts. An umbrella policy provides additional liability coverage beyond your auto insurance limits, typically starting at $1,000,000, and costs surprisingly little-often $150 to $300 annually for a million dollars of extra protection. Calculate your net worth today, look at your current liability limits, and if there’s a gap, you need either higher auto liability limits or an umbrella policy.

How Rising Claim Severity Changes the Math

Bodily injury and property damage claims have grown substantially. Property damage claim severity increased 2.5 percent year over year in 2024, while bodily injury severity jumped 9.2 percent. These increases mean that accidents you cause today will cost more to settle than accidents from previous years.

Distracted driving violations increased 50 percent from 2023 to 2024, and major speeding violations rose 16 percent year over year, both of which drive up claim frequency and severity. Higher claim costs make state minimum limits even more inadequate than they were five years ago. You should try limits of at least $100,000/$300,000 if you have meaningful assets to protect.

Shopping for the Right Limits Matters Now

Over 45 percent of drivers shopped their auto policies in 2024, and many discovered that higher liability limits cost far less than they expected. The difference between a $25,000 limit and a $100,000 limit on your premium is often just $10 to $20 per month. That small increase in cost provides massive protection against catastrophic loss. When you compare quotes from multiple insurers, you’ll see how dramatically premiums can vary for the same coverage-which is why shopping remains one of the most effective ways to control costs while protecting yourself. The next step involves understanding the specific types of liability coverage and how coverage limits work together to create a complete protection strategy.

Types of Liability Coverage and Coverage Limits

Liability coverage splits into two distinct parts, and understanding how each works prevents costly mistakes when selecting limits. Bodily injury liability covers medical expenses, lost wages, pain and suffering, and legal fees for people you injure in an accident you cause. Property damage liability covers repair or replacement costs for vehicles, homes, fences, mailboxes, and other property you damage. These aren’t interchangeable protections-they’re separate buckets of money your insurer will pay on your behalf. The average bodily injury claim paid $28,278 in 2024, according to ISO data, while the average property damage claim was $6,770. However, these averages mask the real risk: serious injuries routinely exceed $100,000, and catastrophic cases can reach $500,000 or more.

Understanding the Numbers Behind Your Limits

When you see a liability limit written as 25/50/10, that means $25,000 bodily injury per person, $50,000 bodily injury per accident, and $10,000 property damage per accident. If two people are injured in an accident you cause and medical bills total $60,000, the 25/50/10 limit pays only $50,000 total for both people combined-you cover the remaining $10,000 from your own pocket. This is why the difference between state minimums and actual adequate coverage matters so dramatically. Most drivers with meaningful assets choose limits of $100,000/$300,000 or higher because they understand that state minimums leave them exposed to personal liability.

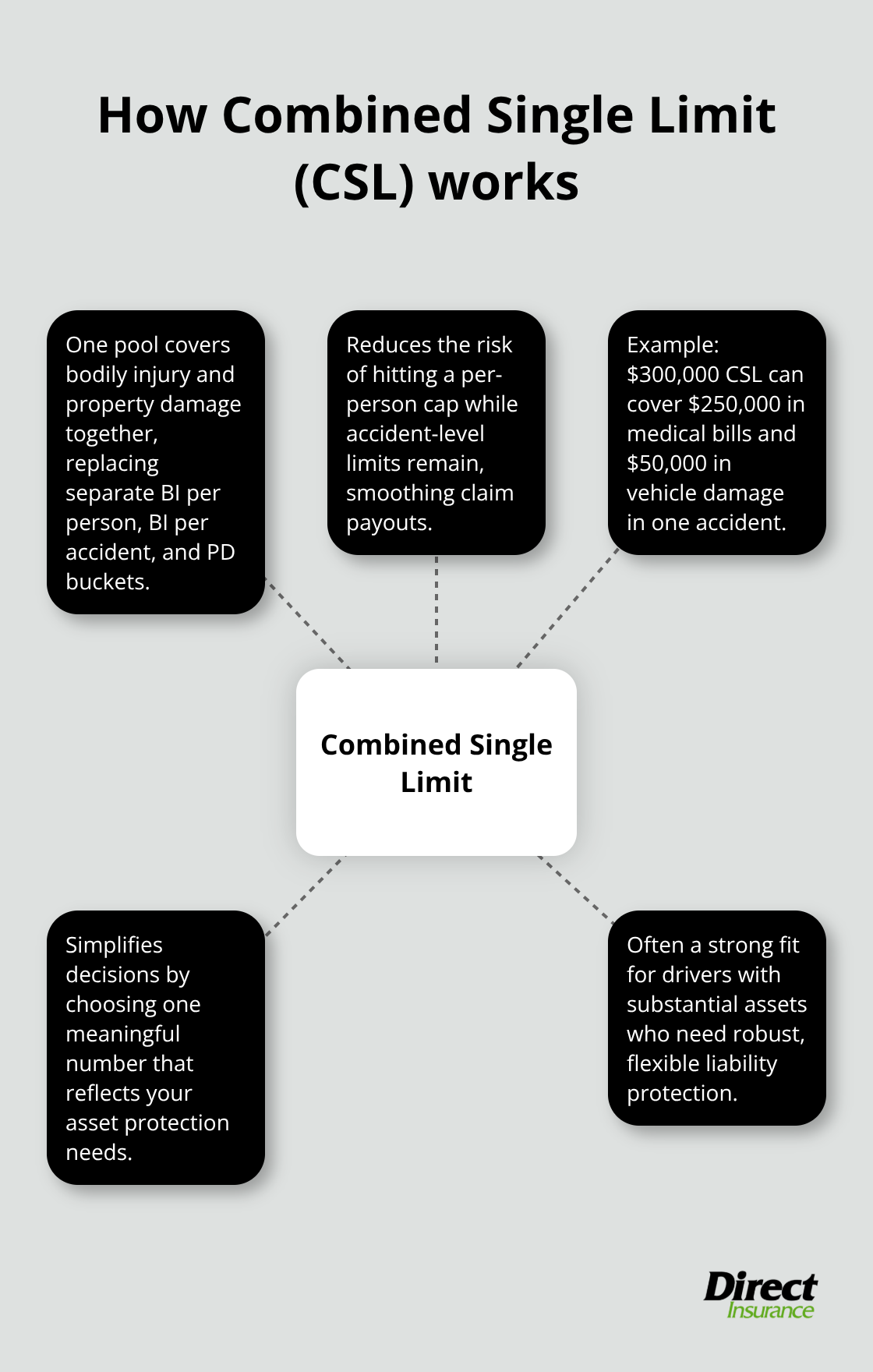

Combined Single Limits Simplify Your Decision

Some insurers now offer Combined Single Limit (CSL) policies that pool bodily injury and property damage under one total limit, such as $300,000 or $500,000. Rather than tracking separate buckets for BI per person, BI per accident, and PD, you have one pool that covers everything. CSL policies eliminate the math problem of hitting your per-person limit while still having accident-level limits remaining. If you cause a serious accident with $300,000 in total damages-say $250,000 in medical bills and $50,000 in vehicle damage-a $300,000 CSL covers it all.

With traditional limits like 100/300/50, you’d have $300,000 for all bodily injury claims but only $50,000 for property damage, creating an awkward gap. CSL structures force you to choose one meaningful number that reflects your asset protection needs, which is simpler than balancing three separate limits. Most drivers with substantial assets benefit from at least $300,000 CSL or traditional limits of 100/300/100 or higher.

Why Bodily Injury Severity Trends Matter to Your Limits

Bodily injury claims grew 9.2 percent in severity year over year in 2024. This means accident injuries today cost substantially more to resolve than they did three years ago. Medical inflation, longer recovery periods, and higher pain-and-suffering awards all drive this trend upward. Distracted driving violations jumped 50 percent from 2023 to 2024, increasing both the frequency and severity of accidents. Major speeding violations rose 16 percent year over year and now sit 38 percent higher than 2019 levels. These behavioral trends make the accidents that do happen more severe, pushing bodily injury settlements higher.

State minimum liability limits haven’t changed in most states, yet the actual cost of claims has climbed substantially. A $25,000 bodily injury limit in 2024 provides far less protection than the same limit provided five years ago. If you own a home or have retirement savings, you need limits that reflect today’s claim environment, not yesterday’s. Shopping for quotes across multiple insurers reveals that premium differences between $100,000 and $300,000 limits are modest-often $15 to $30 monthly-making the upgrade financially rational for anyone with meaningful assets.

Property Damage Liability Deserves Attention Too

Property damage claim severity increased 2.5 percent year over year in 2024, meaning the cost to repair or replace damaged property has risen. A single accident can damage multiple vehicles, a home, or expensive property, and your PD limit determines how much your insurer covers. Many drivers underestimate their property damage exposure and choose limits like $10,000 or $25,000, which can be exhausted quickly in accidents involving newer vehicles or multiple properties. Try limits of at least $50,000 to $100,000 for property damage if you have assets to protect. The next step involves assessing your specific situation and comparing how different insurers price these coverage options.

Choosing Liability Limits That Protect Your Actual Wealth

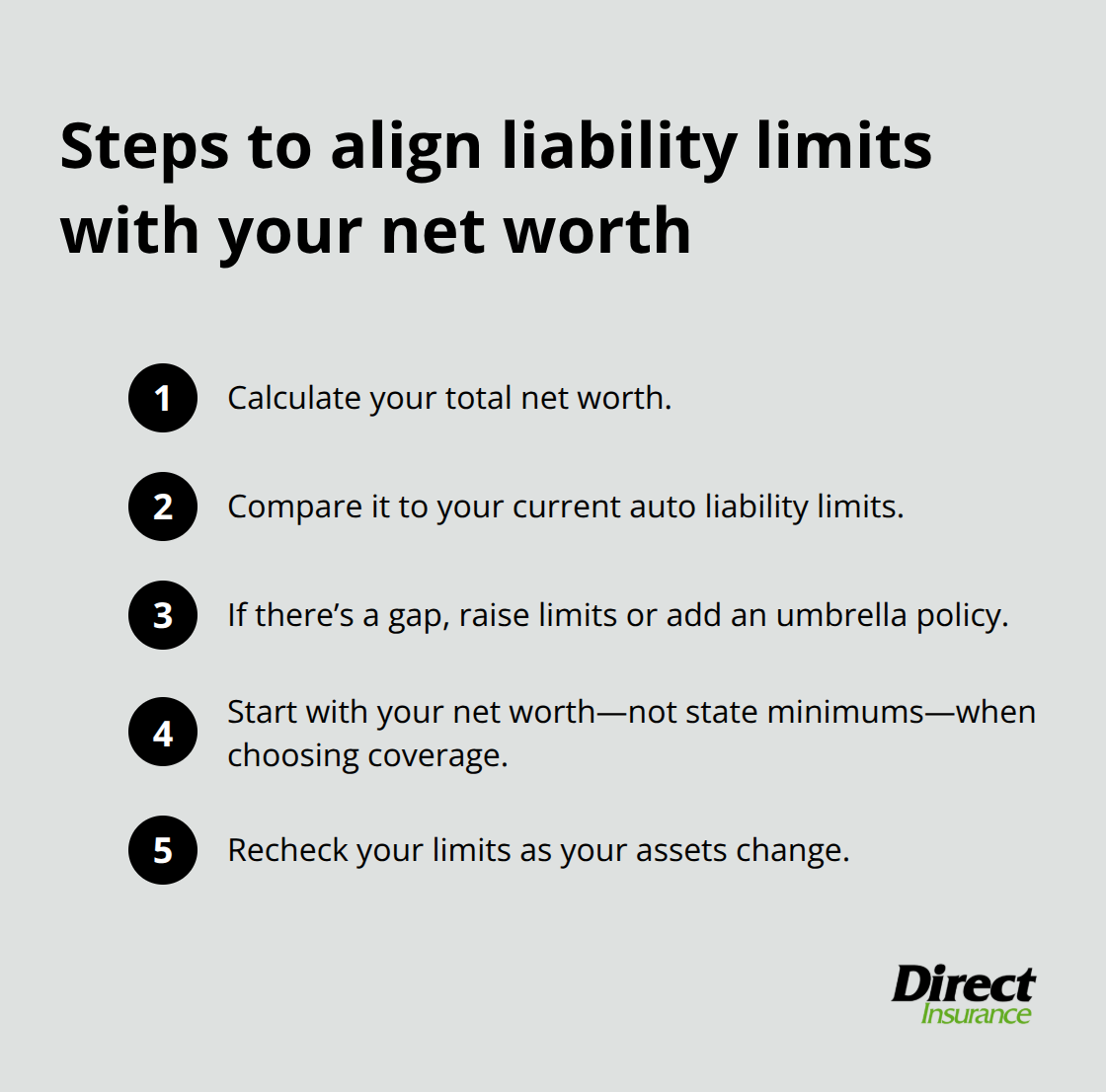

Calculate Your Net Worth First

Start with your net worth, not your state’s minimum requirements. Your net worth includes your home value, vehicles, savings accounts, retirement funds, and any other assets a lawsuit judgment could target. If you own a home worth $400,000 and have $150,000 in retirement savings, your net worth is $550,000. Your liability limits should match or exceed this number because that’s what you stand to lose in a serious accident. Most drivers discover they’re dramatically underinsured when they actually do the math.

A liability limit of $50,000 leaves a $500,000 gap between your coverage and your assets if you cause a catastrophic accident.

Understand What Claims Actually Cost

Severe spinal injuries, permanent brain damage, or death produce settlements and judgments exceeding $500,000 or $1,000,000. If your policy limit is $100,000 and the judgment is $750,000, you’re personally responsible for the remaining $650,000. That means wage garnishment for years, forced sale of your home, or bankruptcy. These aren’t theoretical scenarios-they happen to real drivers who underestimated their exposure.

Add an Umbrella Policy for Real Protection

An umbrella policy costs remarkably little to solve this problem. A $1,000,000 umbrella policy typically costs $150 to $300 annually, making it the most cost-effective protection available. If your auto liability limits are $100,000/$300,000 and your net worth exceeds $300,000, you should add an umbrella policy immediately. The calculation is simple: annual umbrella cost versus the risk of losing everything you’ve built.

Shop Multiple Insurers for Better Rates

When you shop for quotes, request the same limits from multiple insurers to see how dramatically premiums vary. Comparing a $100,000/$300,000 limit across five different companies might show a $40 monthly difference between the cheapest and most expensive option. Over a year, that’s a $480 difference for identical coverage. Over five years, it’s $2,400. Don’t accept your current insurer’s quote without checking competitors.

Maximize Discounts to Lower Your Premium

When comparing quotes, ask about available discounts like bundling home and auto policies, maintaining a clean driving record, completing a defensive driving course, or installing safety devices. These discounts can reduce your premium by 10 to 25 percent, which often exceeds the difference between liability limits. A driver with a $100,000/$300,000 limit at one company might pay $1,200 annually, while another company offers the same coverage at $950 with a bundling discount. That’s $250 saved without sacrificing protection.

The key is requesting quotes with identical coverage details so you’re comparing apples to apples. Don’t let insurers quote you different limits or deductibles when you’re trying to compare prices. Specify your desired limits, your current deductibles, and any discounts you qualify for before requesting the final quote. As an independent insurance agency, we shop multiple top-rated insurance companies to help you find the best coverage at competitive rates, ensuring you’re not overpaying for the protection you need.

Final Thoughts

Liability insurance auto coverage protects your financial future in ways most drivers don’t fully appreciate until they need it. State minimum limits prove inadequate for anyone with meaningful assets, since bodily injury claims averaged $28,278 in 2024, yet serious accidents routinely exceed $100,000 or $500,000. Distracted driving violations jumped 50 percent from 2023 to 2024, making accidents more frequent and costly when they occur.

Your liability limits should match or exceed your net worth because that’s what you stand to lose in a catastrophic accident. Most drivers benefit from at least $100,000/$300,000 limits or a Combined Single Limit of $300,000 or higher, and if your net worth exceeds your auto liability limits, an umbrella policy ($1,000,000 coverage costs just $150 to $300 annually) fills the gap. Shop multiple insurers for the same coverage to find the best rate, and ask about bundling discounts, defensive driving credits, and safety device discounts that can reduce your premium by 10 to 25 percent.

At Direct Insurance Services, we shop multiple top-rated insurance companies on your behalf to find the best coverage at competitive rates. Contact Direct Insurance Services today to review your liability insurance auto coverage and ensure your assets are properly protected.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation