How to Get Commercial Auto Liability Insurance Coverage

Commercial auto liability insurance protects your business when a vehicle causes injury or property damage to someone else. Without proper coverage, a single accident could drain your company’s finances and expose you to serious legal consequences.

At Direct Insurance Services, we help business owners navigate the coverage options that actually fit their operations. This guide walks you through everything you need to know to get the right protection in place.

What Commercial Auto Liability Insurance Actually Protects

Commercial auto liability insurance covers two critical areas when your vehicle causes harm to someone else. First, bodily injury liability pays for medical expenses, lost wages, and legal costs if your vehicle injures or kills another person. Second, property damage liability covers damage to someone else’s vehicle, building, or other property. These aren’t optional protections-they’re mandatory in every state, including Utah. The National Association of Insurance Commissioners identifies these as essential coverages that distinguish commercial auto policies from personal auto insurance, which explicitly excludes business use.

Why Utah Businesses Can’t Skip This Coverage

Utah law requires minimum liability limits for commercial vehicles, though the specifics depend on your vehicle type and how you use it. More importantly, a single accident can cost far more than Utah’s minimum requirements allow. If a delivery truck hits a passenger vehicle and injures three people, medical bills alone could reach $300,000 to $500,000 depending on injury severity.

If your policy only carries Utah’s minimum liability limits of $25,000 per person and $65,000 per accident, your business becomes personally liable for the difference. This is why business owners should carry limits significantly higher than the state minimum-typically $100,000 per person and $300,000 per accident at an absolute minimum, though many successful operations carry $500,000 to $1,000,000 in limits. The difference in premium between minimal coverage and adequate coverage is often just 15 to 25 percent annually, making it a straightforward business decision. If you operate multiple vehicles or transport high-value goods, the risk exposure grows exponentially, and your coverage should reflect that reality. Utah’s winter driving conditions increase accident frequency, which means your liability exposure is higher than in states with milder climates year-round.

How Utah’s Rules Shape Your Coverage Decision

Utah requires proof of financial responsibility for any business vehicle you own, lease, or rent. If employees drive company vehicles, your policy must cover them as authorized drivers. If employees occasionally use personal vehicles for business purposes (dropping off supplies or meeting clients), you need employee hired auto coverage or a separate endorsement to protect yourself. Many Utah business owners assume their general liability policy covers vehicle-related incidents, but it doesn’t. Commercial auto liability is a separate requirement. Additionally, if your business involves transporting goods or operating in construction, your exposure differs from a service business where employees simply drive to appointments. Utah’s minimum liability limits are lower than what most insurers actually recommend, so relying on state minimums leaves your business dangerously underprotected. Work with an agent who understands Utah’s specific requirements and your actual risk exposure rather than defaulting to whatever meets the legal minimum.

What Happens When You Underestimate Your Exposure

Your actual liability risk extends beyond what state law requires. If your business operates vehicles in high-traffic areas or transports valuable cargo, your exposure multiplies. A single serious accident involving multiple vehicles or injuries can generate claims that far exceed Utah’s minimum limits. Courts award damages based on actual harm, not on what your policy covers. If a judgment exceeds your policy limits, creditors can pursue your business assets and personal finances to satisfy the difference. This is precisely why comparing quotes from multiple insurers matters-different carriers price risk differently, and some offer higher limits at rates that won’t shock your budget. The next step in protecting your business is assessing exactly what vehicles you operate and how your team uses them, which directly determines the coverage limits you actually need.

Getting Your Coverage in Place

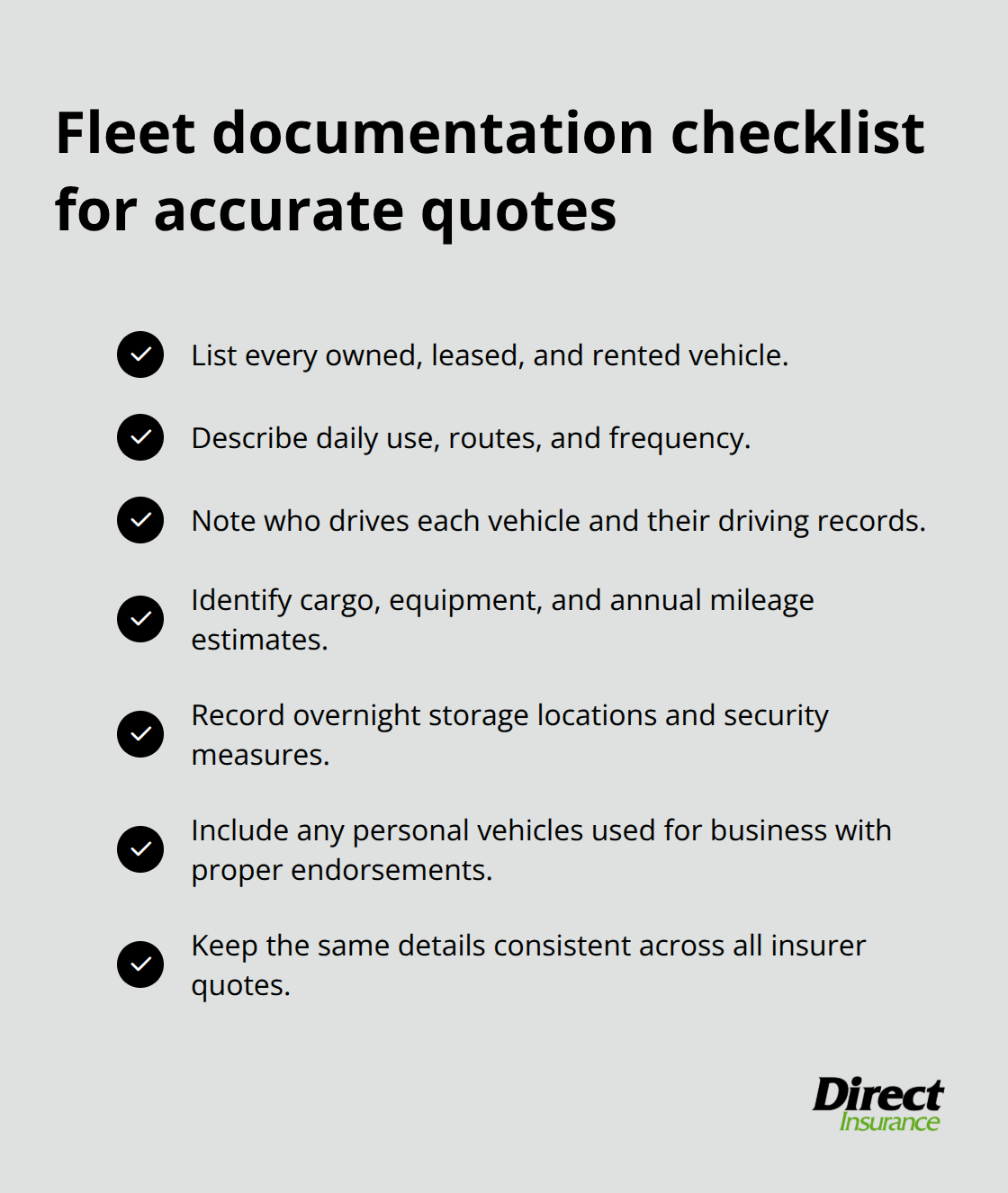

Document Your Fleet Operations

List every vehicle your business owns, leases, or rents, then document how each one gets used. A delivery van that operates daily in Salt Lake City carries different risk than a construction truck that sits idle most weeks. Note whether employees drive company vehicles, whether personal vehicles are ever used for business, and what cargo or equipment travels in each vehicle. This inventory becomes your baseline for comparing quotes because insurers need exact details to price your coverage accurately.

Utah’s winter conditions mean you should also document where vehicles are stored overnight-a secure garage versus an open lot affects your premium and available discounts. Many business owners provide vague descriptions to insurers, which either leads to coverage gaps later or inflated quotes based on worst-case assumptions. Thirty minutes of documentation prevents both problems.

Contact Multiple Insurers Directly

Call three to five insurers directly rather than relying on online quote tools that oversimplify your business structure. When you call each carrier, provide your vehicle details, your drivers’ ages and driving records, and your actual annual mileage. Carriers price risk differently-one might charge $1,200 annually for $500,000 in limits while another quotes $1,450 for identical coverage, depending on their appetite for your specific risk profile. The difference matters over time.

Ask About Discounts and Optimize Your Limits

Don’t accept the first quote or assume the lowest price equals the best value. Ask each insurer what discounts apply to your operation: safe driver programs, fleet telematics, secure parking, or prior insurance history can reduce your premium by 10 to 20 percent. These reductions add up significantly across your annual costs.

Set your coverage limits based on your actual exposure, not Utah’s minimums. If your business operates multiple vehicles or transports goods, carry at least $500,000 in liability limits; if you have significant assets to protect, $1,000,000 makes sense despite the modest premium increase. This decision requires honest assessment of what a serious accident could cost your business, not just compliance with state law. Once you’ve narrowed your choices and selected appropriate limits, the next step involves reviewing the specific policy details and exclusions that separate adequate protection from gaps that could expose your business to unexpected liability.

Common Mistakes That Drain Your Business Finances

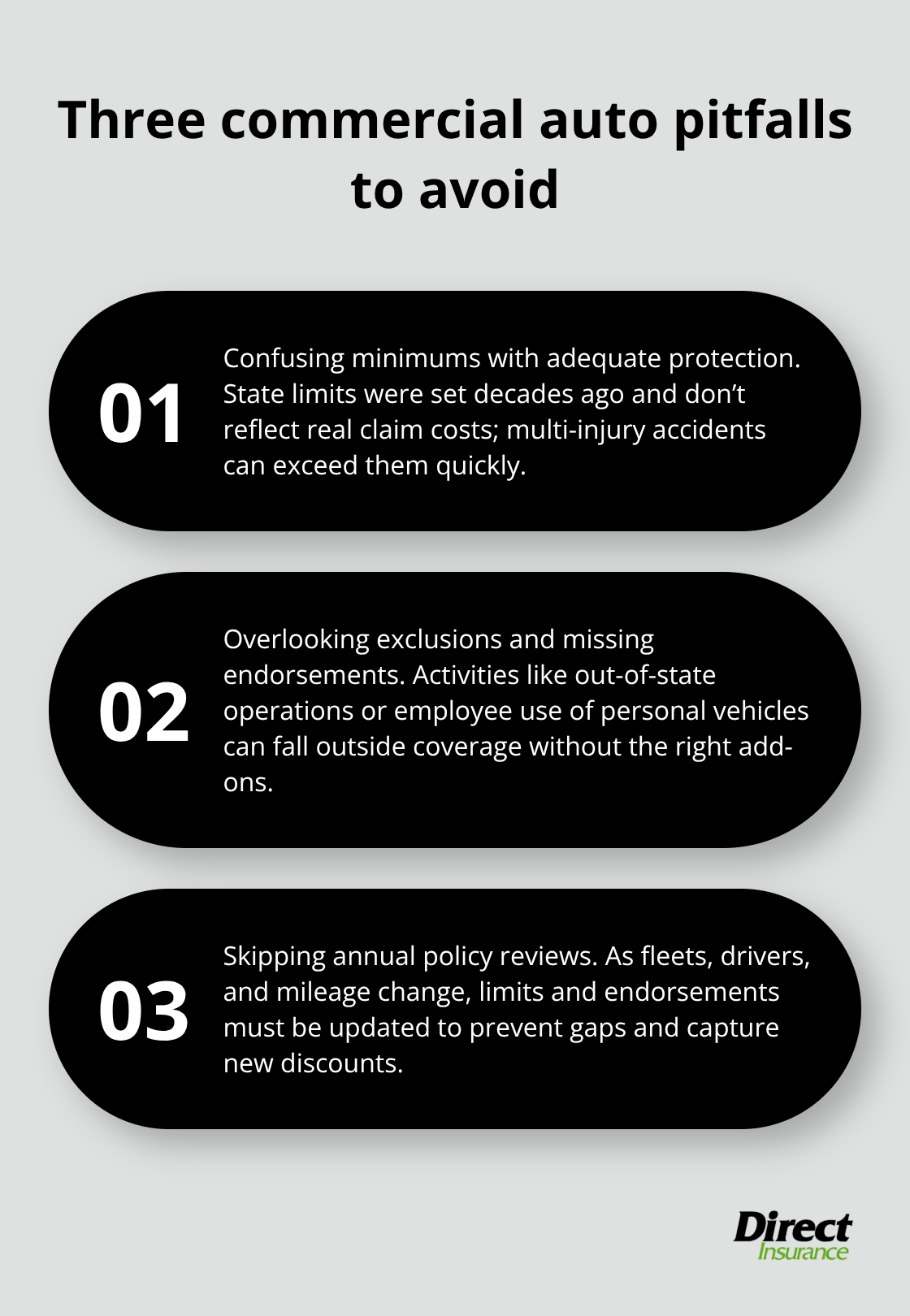

Utah’s Minimum Coverage Falls Short of Real Accident Costs

Most Utah business owners confuse minimum legal coverage with adequate protection. Utah’s minimum liability limits of $25,000 per person and $65,000 per accident exist because legislators set them decades ago, not because they reflect actual accident costs. The National Association of Insurance Commissioners found that bodily injury claims in commercial auto accidents average $50,000 to $150,000 per injured party when multiple injuries occur. A delivery vehicle hitting a sedan carrying three passengers in Salt Lake City’s high-traffic corridors could generate medical expenses reaching $200,000 before considering lost wages, pain and suffering, or legal fees. Your $25,000 per-person limit covers maybe one injured person’s immediate medical bills. Your business becomes responsible for the remaining $175,000 or more.

Utah’s winter conditions and congested urban areas mean collision frequency is measurably higher than national averages. Insurers recommend $100,000 per person and $300,000 per accident as an absolute minimum for any business vehicle. Many successful operations in Utah carry $500,000 to $1,000,000 in limits, and the premium difference between $100,000 and $500,000 in coverage typically runs only 12 to 18 percent annually. Choosing minimum coverage to save a few hundred dollars annually exposes your business to six-figure liability.

Policy Exclusions Create Hidden Gaps

The second mistake involves ignoring what your policy actually excludes. Many business owners assume their commercial auto policy covers all business-related vehicle use, then discover mid-claim that certain activities fall outside coverage. If you transport hazardous materials, operate a vehicle commercially outside Utah, or have employees drive personal vehicles for business purposes without the proper hired auto endorsement, gaps emerge instantly.

Your policy documents spell out these exclusions, but most owners never read them until a claim denial arrives. Spend two hours reviewing your actual policy language-not the summary, but the exclusions and coverage conditions. If your employees occasionally use personal vehicles for business, confirm you have employee hired auto coverage explicitly listed. If you operate across state lines, verify your coverage applies in those jurisdictions.

Annual Policy Reviews Prevent Coverage Mismatches

Failing to review your policy annually means you operate blind as your business changes. If you add a new vehicle, hire younger drivers, expand into a new service area, or increase annual mileage, your coverage may no longer match your actual risk. Insurers typically allow annual policy reviews at no cost. Schedule one every January and provide updated information about your fleet, drivers, and operations. This simple habit catches coverage gaps before accidents expose them and often reveals new discounts you’ve become eligible for as your business evolves or improves its safety record.

Final Thoughts

Getting commercial auto liability insurance coverage requires three concrete actions. First, document your actual fleet operations and vehicle usage patterns rather than guessing at your exposure. Second, contact multiple insurers directly and compare quotes based on identical coverage limits and vehicle details, not just price. Third, set your liability limits based on what a serious accident could actually cost your business, not what Utah’s minimum legal requirements allow.

Your next step involves scheduling conversations with insurers who understand Utah’s specific environment. Winter driving conditions, congested urban corridors, and the state’s unique business landscape all affect your actual liability exposure. Ask each carrier about discounts for safe driver programs, fleet telematics, or secure vehicle storage, since these reductions compound across your annual costs and often reveal that higher coverage limits cost less than you’d expect.

At Direct Insurance Services, we shop multiple top-rated insurance companies on your behalf to find commercial auto liability insurance that matches your actual risk exposure at rates that fit your budget. Our team understands the specific challenges Utah businesses face, from winter weather impacts to the state’s regulatory environment, and we work with you to assess your fleet operations and build a protection strategy that keeps your business assets safe. Contact us at saltlakeinsurance.com to discuss your coverage needs and get quotes from the carriers that offer the best combination of protection and price for your operation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation