Do You Have to Have Home Insurance?

Most homeowners assume home insurance is optional. The reality is more complicated-and the stakes are higher than you might think.

At Direct Insurance Services, we’ve seen firsthand what happens when people skip coverage. Whether you’re legally required to have it depends on your mortgage, your state, and your personal risk tolerance. This guide breaks down what you actually need to know.

When Your Lender Demands It

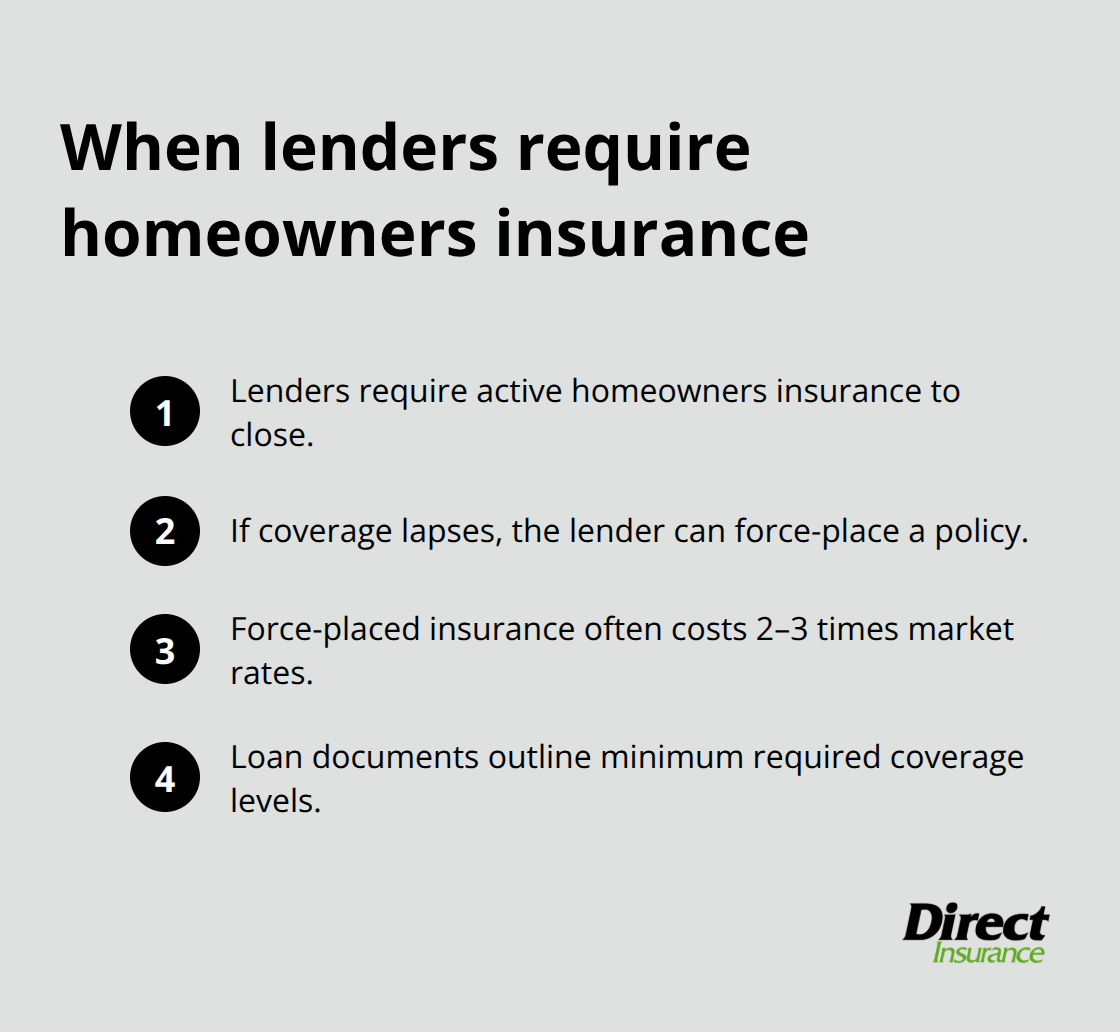

If you have a mortgage, your lender doesn’t care what you think about home insurance-they’re requiring it. Mortgage lenders protect their financial interest in your property, and homeowners insurance is non-negotiable before you close on the loan. The lender will specify minimum coverage amounts in your loan documents, typically covering the replacement cost of the structure itself. If you let that policy lapse after closing, your lender will force-place insurance on your behalf, which costs significantly more than buying your own policy. Force-placed premiums run 2 to 3 times higher than standard market rates, and you’ll pay for every penny of it.

Home equity loans and lines of credit operate the same way-the lender requires proof of active coverage before they’ll fund the loan. If your area faces flooding risk, your lender will demand flood insurance as a separate policy or rider, since standard homeowners policies exclude water damage from storms and rising water. Earthquake coverage follows the same pattern in seismically active regions. Your loan documents spell out exactly what coverage is required, so read them carefully before signing.

What Happens After You Pay Off Your Mortgage

Once your mortgage is paid off, the legal requirement vanishes-you’re free to drop coverage if you choose. However, that’s a mistake we strongly advise against. Your home is your largest financial asset, and one disaster wipes out decades of equity if you’re uninsured.

The data backs this up: Census Bureau research analyzed by NBC News found that 1 in 8 U.S. homeowners lack meaningful coverage. Among homeowners without mortgages, that rate climbs to 20.8%. In Florida, 18.3% of homeowners are uninsured or underinsured, and in Miami-Dade County alone, 24.6% lack adequate protection.

The Real Cost of Dropping Coverage

Rising premiums create genuine financial pressure. Nebraska’s average homeowners insurance hit $6,400 in 2024, the highest in the nation, while Florida averaged $5,800. An Oklahoma homeowner posting on Reddit reported annual premium increases of roughly $1,000-from $2,252 to $3,267 to $4,535 over consecutive years. When premiums jump that dramatically, the math gets brutal.

But dropping coverage to save money creates a different kind of financial disaster. After a major loss, uninsured homeowners face complete out-of-pocket rebuilding costs while dealing with trauma and displacement. Recovery becomes nearly impossible without insurance payouts to support contractors, repairs, and temporary housing. The question then shifts from “Can I afford insurance?” to “Can I afford to rebuild my entire home?”

What Happens When You Skip Home Insurance

Skipping home insurance to save money creates financial exposure far worse than any premium you’ll pay. Property damage from fire, storms, or theft doesn’t care whether you’re insured-it happens anyway. Without coverage, you absorb the entire cost of repairs or rebuilding from your own pocket. A house fire that destroys your roof, walls, and contents can cost homeowners between $3,000 and $40,000 for fire damage restoration, with the average cost around $11,900. Most homeowners don’t have that amount sitting in savings.

The Out-of-Pocket Catastrophe

You’d face the choice between taking on massive debt, selling assets at a loss, or living in a damaged home indefinitely. Insurance spreads that risk across thousands of policyholders so no single person bears the full weight of catastrophe. When disaster strikes, uninsured homeowners must pay contractors upfront while managing trauma and displacement simultaneously. That financial pressure forces impossible decisions at the worst possible time.

Personal Liability Can Bankrupt You

Home insurance includes liability protection that most people underestimate until they need it. If someone is injured on your property-a guest who falls down your stairs, a delivery driver who slips on your walkway, a child from the neighborhood who gets hurt in your yard-they can sue you for medical bills, lost wages, and pain and suffering. A serious injury claim routinely exceeds $100,000.

Without liability coverage, a judgment against you could lead to wage garnishment or forced sale of your home. Your homeowners policy typically covers $100,000 to $300,000 in liability protection depending on your plan. That protection makes the difference between a lawsuit that your insurance handles and one that destroys your financial life.

Rebuilding Without Insurance Costs Far More

After a major disaster, reconstruction costs spike immediately. Contractors, lumber suppliers, and laborers all face surging demand, which drives prices up. An uninsured homeowner competing for those resources while cash-strapped faces contractors who demand full payment upfront or simply won’t take the job. Insurance companies, by contrast, work directly with contractors and can authorize work to begin quickly.

The Insurance Information Institute notes that insured losses from hail and severe convective storms reached about $54 billion nationwide in 2024 alone. Those claims funded immediate repairs and recovery. Uninsured homeowners in the same storms faced months or years of delays, temporary housing costs they couldn’t recover, and the psychological toll of displacement. Rebuilding without insurance payouts means taking out loans at high interest rates, delaying repairs while your family lives elsewhere, and watching your home’s condition deteriorate further while waiting for funds you may never fully gather.

The financial math is clear: premiums protect your wealth far better than self-insuring ever could. Yet millions of homeowners still operate without adequate coverage, leaving themselves vulnerable to losses that insurance would have prevented entirely. Understanding what specific coverage types actually protect you-and which gaps leave you exposed-becomes the next critical step in making an informed decision about your home’s protection.

What Coverage Actually Protects Your Home

Structure and Personal Property Coverage

Standard homeowners insurance covers the structure of your home, personal belongings inside it, and liability protection if someone is injured on your property. Structure coverage pays to rebuild or repair walls, roofs, floors, and built-in fixtures after fire, wind, theft, or other covered perils. Personal property coverage reimburses you for furniture, electronics, clothing, and other items up to your policy limits, typically as a percentage of your home’s insured value.

Most standard policies come with deductibles ranging from $500 to $2,500, meaning you pay that amount out of pocket before insurance kicks in. Higher deductibles lower your premium, but only if you have savings to cover them when disaster strikes. Try matching your deductible to what you can actually afford to pay without financial strain.

Liability Protection Against Lawsuits

Liability protection covers medical bills and legal costs if someone sues you after an injury on your property. A serious injury claim routinely exceeds $100,000, and without this coverage, a judgment against you could lead to wage garnishment or forced sale of your home. Your homeowners policy typically covers $100,000 to $300,000 in liability protection depending on your plan.

The Critical Gap: Flood and Earthquake Coverage

Flood and earthquake coverage require separate policies or riders because standard homeowners insurance explicitly excludes water damage from storms and seismic activity. This gap catches many homeowners off guard. If you live in a flood-prone area, your mortgage lender will force you to purchase flood insurance through the National Flood Insurance Program or a private insurer, adding $400 to $2,000 annually to your housing costs depending on risk level.

In earthquake zones, private insurers offer riders that typically cost 5 to 15 percent of your base homeowners premium. The real problem emerges when homeowners assume their standard policy covers these events, then face denial of claims after water or seismic damage occurs. Read your policy documents carefully to identify these exclusions, then purchase the riders you actually need (especially if you live in a high-risk area). Skipping them to save money creates the exact financial exposure you bought insurance to prevent.

Final Thoughts

The answer to whether you have to have home insurance depends on your situation, but the financial case for carrying it is overwhelming regardless. If you have a mortgage, your lender makes the decision for you-coverage is mandatory before closing and required to stay in place for the life of the loan. Once you pay off that mortgage, the legal requirement disappears, but the financial risk remains exactly the same.

Rising insurance costs create real pressure on household budgets, and the temptation to drop coverage is understandable. Nebraska homeowners pay an average of $6,400 annually, while Florida averages $5,800, and an Oklahoma homeowner reported annual increases of roughly $1,000 per year, pushing premiums from $2,252 to over $4,500 in just three years. However, dropping coverage to save money trades a predictable expense for catastrophic financial exposure-a house fire costs an average of $11,900 in restoration alone, and major disasters easily exceed $100,000 in total losses.

Your home is your largest asset, and one disaster without insurance erases decades of equity and forces you into debt or displacement. Contact Direct Insurance Services to shop multiple insurers and find competitive rates that fit your budget. We’ve been helping homeowners since 1973, and we understand that protection doesn’t have to mean overpaying.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation