How to Find Cheap Auto Insurance in Utah

Auto insurance in Utah doesn’t have to drain your budget. We at Direct Insurance Services know that finding cheap auto insurance in Utah means understanding what actually drives your rates and where real savings hide.

Most drivers overpay because they don’t shop around or miss discounts they qualify for. This guide walks you through the exact steps to cut your premiums without sacrificing coverage.

What Actually Drives Your Utah Auto Insurance Rates

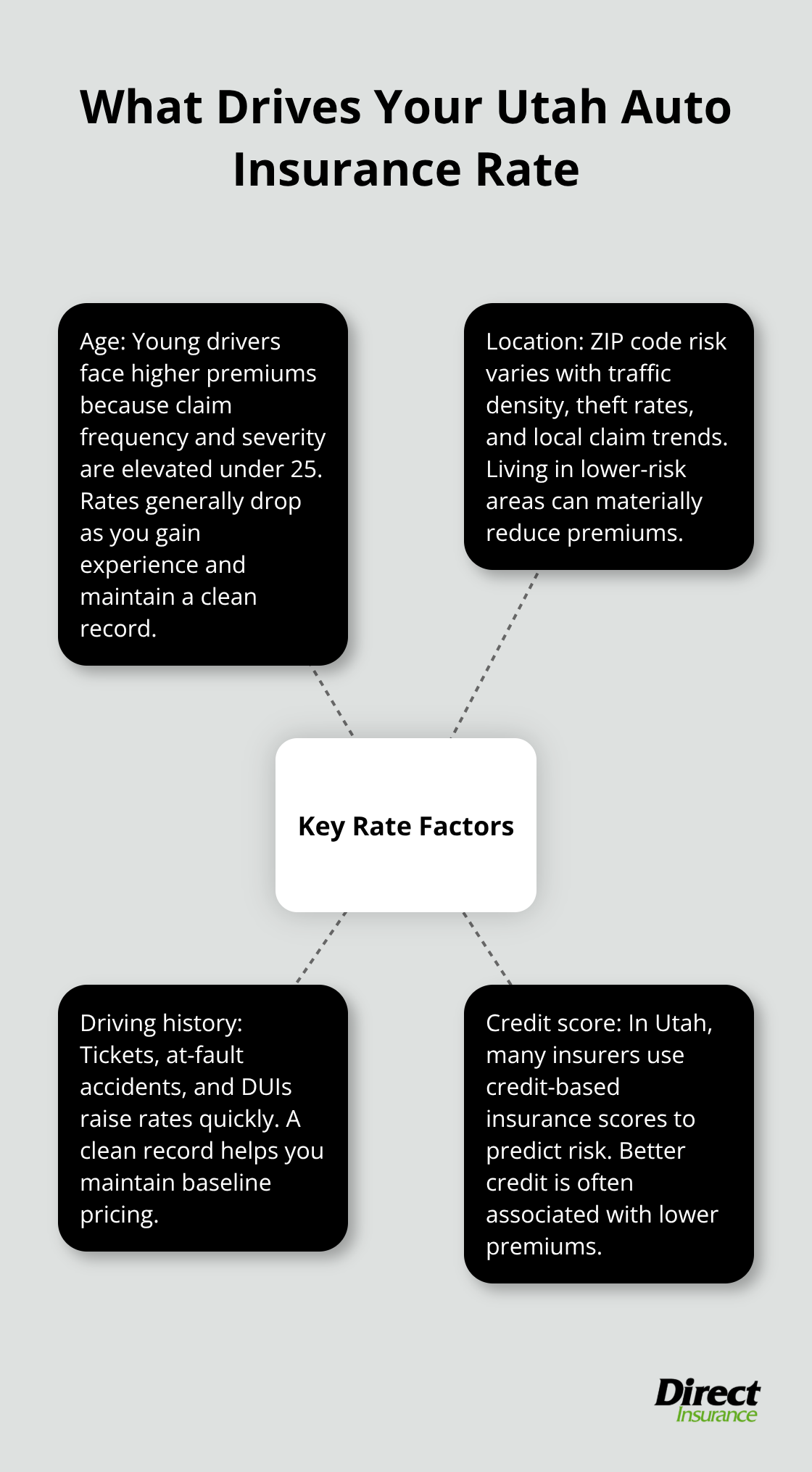

Age Creates the Biggest Price Gap

Your age determines more of your premium than almost any other factor. A 20-year-old in Utah pays roughly $3,824 annually for full coverage with Progressive, while a 50-year-old pays around $1,407 with Nationwide, according to NerdWallet’s March 2026 analysis. That’s a difference of nearly $2,400 per year for identical coverage. Insurers view younger drivers as statistically riskier because accident rates spike for drivers under 25. This isn’t opinion-it’s actuarial data that every carrier uses to price policies.

Location and Driving History Shape Your Rate

Where you live in Utah matters as much as your age. Drivers in Enoch pay significantly less than those in Kearns, with six-month premiums varying by hundreds of dollars depending on ZIP code. Your driving record carries enormous weight too. A clean record keeps you at baseline rates, but one speeding ticket can push your annual premium up by roughly $200 to $300 with most carriers. A DUI in Utah increases your average annual premium by about 104 percent, with some insurers charging well over $4,000 annually.

Credit score isn’t about fairness-it’s how insurers predict risk. Poor credit can add $1,000 or more to your annual premium compared to good credit, according to NerdWallet. These four factors (age, location, driving history, and credit) account for the vast majority of rate variation you’ll see when you shop.

Utah’s Market Offers Real Savings Compared to National Averages

Utah’s insurance market is actually cheaper than the national average. Full coverage in Utah costs about $2,188 per year versus the national average of $2,697, a difference of roughly $500 annually. Minimum coverage in Utah runs about $831 per year compared to the national average of $820, so you’re paying nearly the same for minimum but significantly less for full coverage. This advantage exists partly because Utah has fewer densely populated urban centers than many states, which reduces accident frequency.

Why Cheaper Doesn’t Always Mean Better Protection

Utah’s minimum liability limits are set by state law. These limits sound reasonable until you’re liable for a serious accident. A minor injury claim can easily exceed the minimum, leaving you personally responsible for the difference. Many Utah drivers mistakenly think minimum coverage is safe because it’s legal. It isn’t.

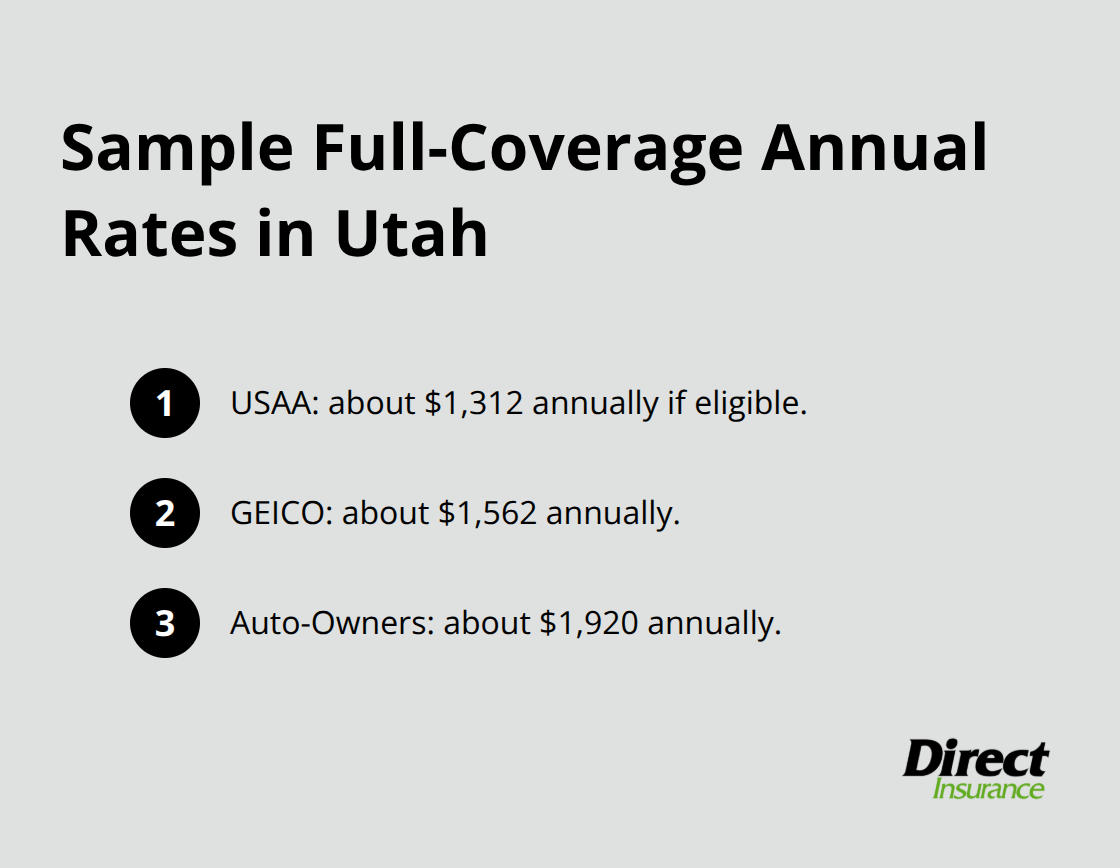

Full coverage costs about 2.5 times more than liability-only in Utah, roughly $1,097 versus $436 for six months according to The Zebra’s 2026 data, but that extra cost protects your vehicle and your assets. The real misconception is that you must choose between cheap and safe. You don’t. USAA offers full coverage in Utah for around $1,312 annually if you’re military-eligible, while GEICO averages about $1,562 for the same coverage. Auto-Owners Insurance stands out for claims satisfaction in Utah, meaning when you actually need your insurance, they deliver. Shopping around reveals the truth that cheap rates and good service often coexist at the same carrier.

Now that you understand what drives your rates, the next step is learning which specific strategies actually cut your premiums without forcing you to sacrifice the protection you need.

How to Cut Your Premiums Without Sacrificing Coverage

Shop Multiple Insurers to Expose Real Price Differences

Comparing quotes across multiple insurers is the single most effective way to lower your premium, and it’s non-negotiable if you want the best rate. A J.D. Power study found that nearly half of American auto insurance customers shopped for a new policy in the past year, yet most Utah drivers still stick with their current insurer out of inertia. When you shopping multiple insurers to compare quotes with identical coverage limits and deductibles, you expose the real price differences that exist in Utah’s market.

The process takes roughly 20 minutes per company, and most carriers now provide instant online quotes. Request quotes from carriers like Progressive, Allstate, and Liberty Mutual to capture the full range of options available in Utah. Each carrier uses different risk models, so your rate will vary based on how each company assesses your risk profile. Shopping once per year keeps you honest with your current insurer and reveals whether competitors offer better rates as your circumstances change.

Raise Your Deductible and Bundle Your Policies

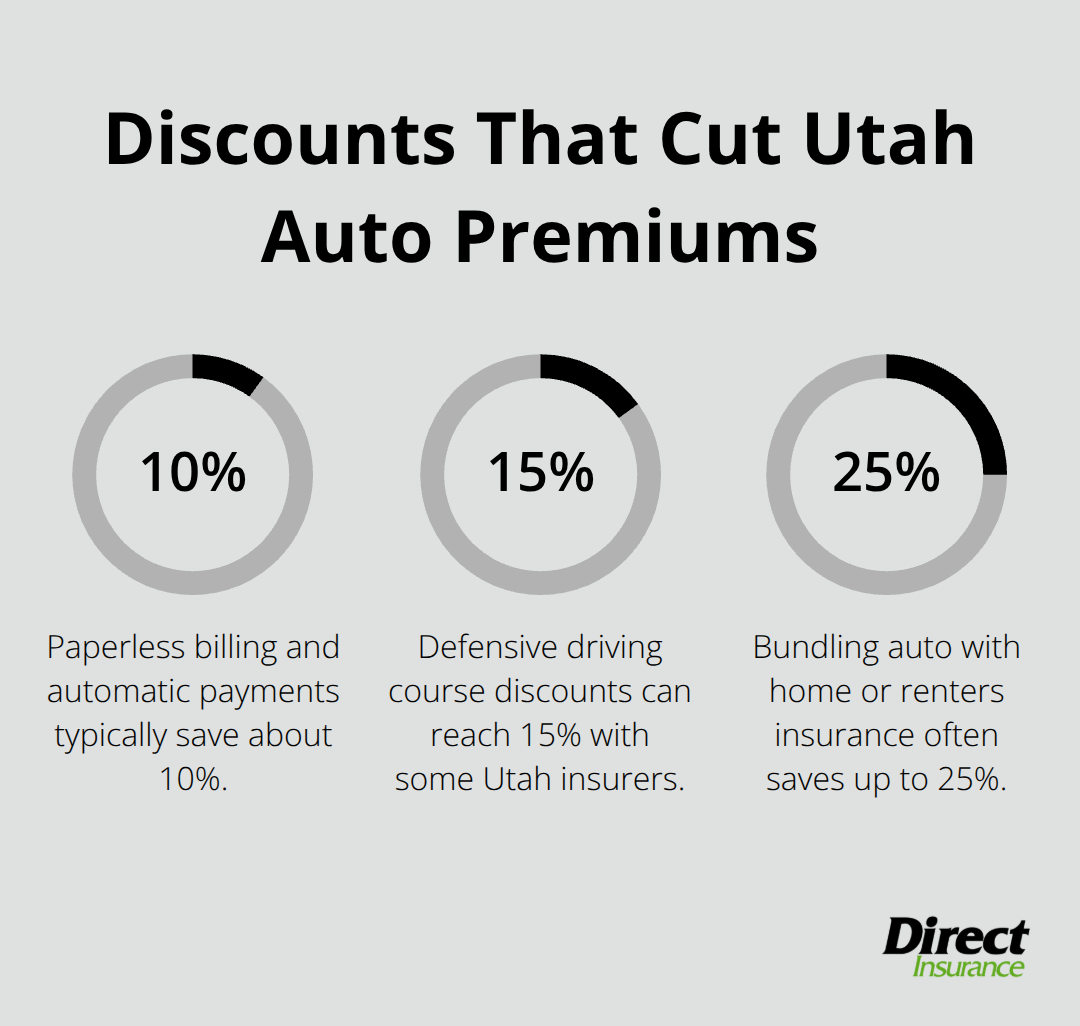

Increasing your deductible directly lowers your premium, but only if you have cash reserves to cover the higher out-of-pocket cost if you file a claim. Moving from a $500 deductible to a $1,000 deductible typically reduces your annual premium by 10 to 15 percent depending on the insurer and your profile. The math works only if you can actually pay that deductible without financial stress.

Bundling auto insurance with home or renters insurance at the same carrier yields substantial savings through multi-policy discounts, often ranging from 10 to 25 percent off your combined premiums. This approach simplifies your billing and strengthens your relationship with one insurer who understands your full coverage picture.

Claim Discounts You Actually Qualify For

Specific discounts you likely qualify for include paperless billing and automatic payments (typically 5 to 10 percent savings), good student discounts if you maintain a 3.0 GPA or higher, and defensive driving course completion (which some Utah insurers discount by 5 to 15 percent). Vehicle safety features like anti-theft devices, airbags, and blind-spot monitoring reduce premiums at most carriers.

If you drive fewer than 7,000 miles annually, usage-based or pay-per-mile programs from Progressive and other carriers can reduce your rate significantly since lower mileage means lower accident risk. Homeowner discounts apply if you own your residence. Ask your insurer directly which discounts apply to your situation rather than assuming you don’t qualify, because eligibility requirements vary and some discounts require explicit enrollment.

The discounts you uncover through direct conversation with your insurer often surprise you. Many drivers leave hundreds of dollars on the table each year simply because they never asked. Once you’ve locked in the right coverage level and discount strategy, the next step involves evaluating which insurers actually deliver when you need them most.

Which Insurers Actually Pay Claims in Utah

Claims Satisfaction Matters More Than Price Alone

Coverage limits on paper mean nothing if your insurer refuses to pay when you file a claim. Auto-Owners Insurance consistently ranks highest for claims satisfaction in Utah according to J.D. Power’s 2024 Regional Customer Satisfaction Study, alongside AAA and State Farm. When you deal with accident damage or injury liability, you trust an insurer with thousands of dollars and your financial security. GEICO offers full coverage in Utah at roughly $1,562 annually and maintains solid claims satisfaction ratings, making it competitive on both price and reliability. Auto-Owners full coverage runs around $1,920 annually in Utah, higher than GEICO but justified by consistently strong claims handling that protects you when accidents happen. The difference between a $400 annual savings and losing a $5,000 claim due to poor service becomes obvious fast.

Payment Flexibility Determines Whether You Keep Coverage

Utah drivers often overlook payment flexibility when comparing plans, yet this directly impacts whether you maintain coverage or lapse. Some carriers require full annual payment upfront, while others offer monthly installments with no penalty. Progressive and Nationwide both provide flexible payment options in Utah without forcing you into expensive payment plans. Utah families have different financial situations, so identifying carriers offering monthly billing, automatic payment setup, and paperless billing discounts reduces costs without forcing inflexible payment structures.

Accident Forgiveness Protects You From Rate Spikes

Carriers offering accident forgiveness programs deserve serious consideration if you have a teen driver or worry about rate increases after a first claim. These programs vary significantly in how they work and which violations qualify, so comparing specific policy language matters more than comparing marketing claims. A single accident can double your rate at renewal, making accident forgiveness valuable protection for your budget.

Final Thoughts

Finding cheap auto insurance in Utah requires three concrete actions: comparing quotes across multiple carriers, claiming every discount you qualify for, and prioritizing claims satisfaction alongside price. USAA offers around $1,312 annually, GEICO runs roughly $1,562, and Auto-Owners costs approximately $1,920 for full coverage-all three deliver strong claims service, proving that affordability and reliability coexist.

Your age, location, driving history, and credit score determine most of your premium, but these factors don’t lock you into high rates when you shop annually and expose the price differences available in Utah’s market.

Utah’s insurance market delivers real value compared to national averages, with full coverage costing about $500 less per year than the national average. Bundling policies, raising your deductible to match your financial capacity, and enrolling in usage-based programs cut premiums significantly. Accident forgiveness programs protect your budget from rate spikes after a first claim, making them worth evaluating if you have teen drivers or worry about unexpected accidents.

Your next step is straightforward: gather quotes from at least three carriers with identical coverage limits, ask about every discount you might qualify for, and evaluate claims satisfaction ratings alongside price. If shopping independently feels overwhelming, contact Direct Insurance Services, which has served Utah families and businesses since 1973 by shopping multiple top-rated carriers to match you with the best coverage at competitive rates. Our team knows which discounts apply to your situation, how claims actually get handled by each carrier in Utah, and which payment options fit your budget.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation