How to Find the Cheapest Commercial Auto Insurance

Commercial auto insurance is one of the biggest expenses for any business that relies on vehicles. At Direct Insurance Services, we know that finding the cheapest commercial auto insurance without sacrificing coverage is challenging.

The good news is that your rates aren’t fixed. Vehicle type, driver history, and how you shop for quotes all directly impact what you pay each month.

What Determines Your Commercial Auto Insurance Cost

Vehicle Type and Repair Costs

The price you pay for commercial auto insurance hinges on factors that insurers measure and quantify every single day. Vehicle type sits at the top of this list because replacement cost and repair expenses vary dramatically. A light service van typically costs $120–$350 per month to insure with standard liability coverage, while a heavy truck or tractor hauling freight runs $900–$2,500 or more monthly. The difference isn’t arbitrary-newer vehicles with sophisticated safety technology and expensive parts drive up repair costs significantly. Supply chain disruptions and skilled-labor shortages have made vehicle repairs 10–15% more expensive over recent years, and insurers pass this reality directly to your premiums.

Location and Garaging ZIP Code

Your garaging location matters more than most business owners realize. Rural ZIP codes can cost 15–20% less than nearby urban areas in the same state, even within the same city. If your vehicles sit in a high-claim frequency zone, you’ll pay more regardless of how safely your drivers operate. This factor often outweighs other considerations, so verify that your insurer has your correct garaging address on file.

Driver History and Motor Vehicle Records

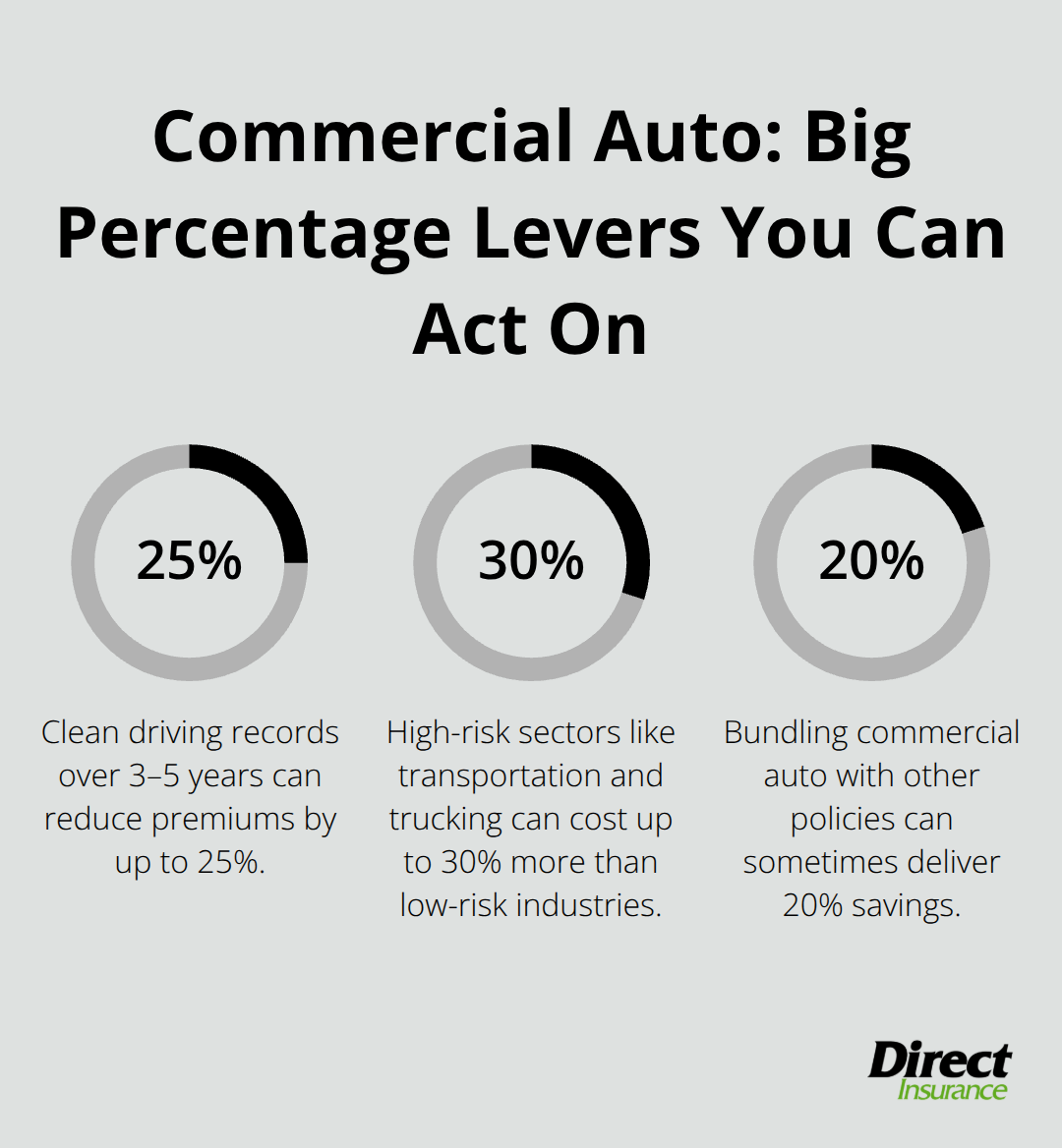

Driver history is the second major lever, and it’s one you can actually control. Insurers pull motor vehicle records for every driver with access to your vehicles. A single at-fault accident can raise your renewal premium for 3–5 years afterward. Conversely, clean records over 3–5 years can reduce premiums by up to 25% compared to drivers with violations or claims.

This means your team’s driving behavior directly impacts what you pay month after month.

Industry Classification and Operating Radius

Industry classification and annual mileage round out the core pricing factors. High-risk sectors like transportation and trucking see premiums up to 30% higher than low-risk industries such as financial services or professional consulting. A construction fleet carrying tools and equipment costs more to insure than a consulting business with a single service vehicle. Operating radius matters too-vehicles traveling under 100 miles locally cost 10–15% less than those running multi-state routes. If your business operates nationally or crosses state lines, expect to pay significantly more because long-haul exposure carries higher frequency and severity risk.

Taking Control of Your Risk Profile

Your premium reflects real, measurable risk. Lower your risk profile through clean driving records and precise classification of your actual operations, and your cost drops accordingly. The factors that determine your rate aren’t mysteries-they’re concrete metrics that you can influence. Once you understand what moves your premium, you’re ready to shop strategically and compare quotes that actually match your business needs.

How to Shop and Save on Commercial Auto Insurance

Compare Quotes Across Multiple Carriers

The biggest mistake we see business owners make is accepting the first quote they receive. Insurers price risk differently, and the same coverage can swing by 30% or more between carriers. When you shop five to ten markets including both direct insurers and independent agencies, you uncover what your actual risk profile is worth. Start your search 45 to 60 days before your renewal date. This timing gives you leverage to switch carriers smoothly and forces insurers to compete for your business rather than simply renewing you at a higher rate.

Get quotes with identical liability limits, deductibles, and vehicle schedules so you compare apples to apples. A $500k liability limit quote from one carrier should match exactly against another. Don’t let online quote tools confuse you with different coverage assumptions. Verify garaging ZIP codes and annual mileage on every quote because these details shift premiums dramatically.

Leverage Bundle Discounts for Immediate Savings

Bundling policies ranks among the fastest ways to cut costs without cutting coverage. Combining commercial auto with general liability or property insurance typically saves 10 to 15% on your total premium, sometimes reaching 20%. This discount exists because insurers reward customer loyalty and reduce their administrative costs when they manage multiple policies for one business. Independent agents have access to carriers offering strong bundle discounts across their product lines.

When you ask about discounts, go beyond the obvious multi-policy bundle. Request prior auto insurance discounts if you’re switching from personal to commercial coverage, paid-in-full discounts for annual payments, and safety program credits if your fleet has dash cams or telematics installed. Many insurers offer 5 to 15% fleet discounts for fleets of three or more vehicles, and some provide up to 25% reductions for clean driving records spanning three to five years.

Unlock Additional Credits Through Safety and Maintenance

Driver training programs and vehicle maintenance records unlock credits that most business owners overlook. Clean up your driver file by removing anyone who no longer needs vehicle access, and implement written safety standards that you can document. These actions signal lower risk to insurers and translate directly into premium reductions.

Higher deductibles move the needle too. Increasing your physical damage deductible from $500 to $1,000 or $2,500 typically cuts premiums by 10 to 20%, but only raise your deductible if your cash reserves can actually cover that out-of-pocket cost after a claim. This strategy works best when you’ve already optimized your coverage limits and driver qualifications.

Timing and Precision Drive Real Savings

The mechanics of shopping matter as much as the effort itself. Carriers compete hardest when you initiate quotes before your renewal, not after. Request multiple options from each carrier to see how different deductible and limit combinations affect your price. This approach reveals which levers move your premium most dramatically for your specific business profile.

Your next step involves understanding which coverage gaps expose your business to real financial risk-and which optional coverages you can safely skip.

Common Mistakes Business Owners Make When Buying Commercial Auto Insurance

State Minimum Liability Limits Leave You Exposed

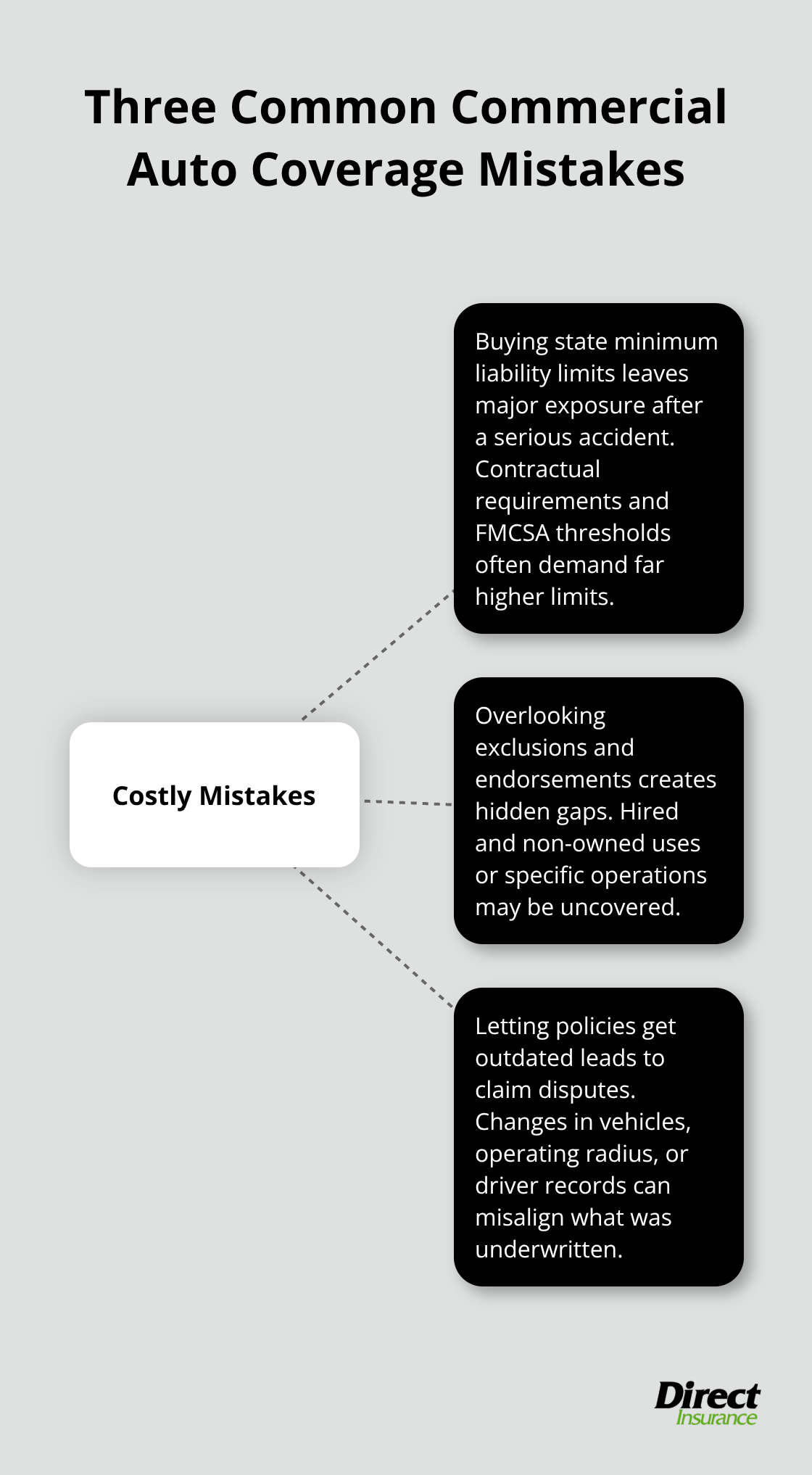

Business owners consistently purchase coverage that protects them far too little or costs far more than necessary because they skip critical steps before purchase. The first mistake is buying state minimum liability limits and calling it done. Most states require $25,000 to $50,000 in bodily injury liability, but that amount is genuinely insufficient for commercial operations. A single serious accident involving multiple vehicles or pedestrians can generate $500,000 to $1,000,000 in damages in seconds. If your business contracts require higher limits-and many do-state minimums leave you personally liable for the gap.

Under FMCSA regulations, non-hazardous freight operations typically demand at least $750,000 in liability coverage, and hazardous materials require substantially more. The cost difference between $100,000 and $1,000,000 in liability is modest, often $50 to $150 monthly, yet the protection gap is catastrophic. Most business owners purchase inadequate limits simply because they never ask what their actual exposure should be.

Policy Exclusions and Endorsements Hide Coverage Gaps

The second critical error occurs when you purchase a policy without reviewing exclusions and endorsements before the first claim happens. Many business owners discover mid-claim that their hired and non-owned auto coverage has gaps, that certain vehicle uses aren’t covered, or that their policy excludes specific operations they actually perform. Reading the policy details matters far more than the premium amount.

When you obtain quotes, request the full policy language or at least a detailed coverage summary showing what’s excluded, what’s endorsed, and what specific uses are covered. Don’t rely on the summary page alone. This step takes 15 minutes but prevents thousands of dollars in unexpected out-of-pocket costs after an accident.

Outdated Policies Create Coverage Disputes at Claim Time

Failing to update your policy annually as your business evolves creates dangerous gaps. If you added two new vehicles, changed your operating radius from local to multi-state, or hired drivers with different records, your existing policy may no longer match your actual risk. Claims filed under outdated policies sometimes face coverage disputes because your operations no longer align with what the insurer underwrote.

Schedule a formal policy review each year before your renewal date-ideally 60 to 90 days out-so you can address changes and shop competitively with accurate information about your current fleet and operations. This timing also gives you leverage to switch carriers if a competitor offers better rates for your updated risk profile.

Final Thoughts

Finding the cheapest commercial auto insurance requires more than hunting for the lowest price-you need accurate information about your fleet, clear understanding of your actual coverage needs, and quotes from multiple carriers that truly match your business profile. The three mistakes we outlined (buying inadequate limits, ignoring policy exclusions, and failing to update annually) cost business owners thousands in unexpected expenses after claims occur. Avoiding these pitfalls protects your bottom line far more effectively than chasing a slightly lower monthly premium.

Independent agents change how you shop for coverage because they access dozens of carriers and compare rates across multiple markets simultaneously. This access matters because the cheapest option for your specific industry, location, and fleet composition varies dramatically. An agent who understands your operations identifies which discounts apply to your situation, flags coverage gaps before they become problems, and handles policy updates as your business evolves.

Gather your current policy documents, vehicle schedules, and driver information, then request quotes from at least three carriers with identical coverage specifications. Schedule this search 45 to 60 days before your renewal date to maximize your negotiating position. Direct Insurance Services can help you compare options and secure the right coverage at the best price.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation