How to Find the Best Car and Home Insurance Bundle

Bundling your car and home insurance can save you hundreds of dollars annually, but only if you pick the right combination. Most people overpay because they don’t compare enough options or understand what coverage they actually need.

At Direct Insurance Services, we’ve helped thousands of customers find the best car and home insurance bundles tailored to their situations. This guide walks you through the exact steps to compare quotes, optimize your coverage, and lock in real savings.

What Coverage Do You Actually Need?

Your vehicle and home represent your largest financial assets, so selecting the right coverage amounts matters far more than finding the cheapest premium. Start by honestly assessing what you own and what would financially devastate you if lost. For your vehicle, document its actual cash value using resources like Kelley Blue Book rather than guessing. If you financed or leased the car, your lender requires collision and comprehensive coverage at specific limits. If you own it outright, you have more flexibility, but dropping collision coverage on a vehicle worth $15,000 to save $50 monthly is false economy. For your home, most lenders require coverage equal to the replacement cost of the structure itself, not the land value. This matters because construction costs in Utah have risen significantly, and your original home purchase price often underestimates what it would cost to rebuild today. Your homeowners policy should cover the full rebuilding expense, not just the current market value.

How Much Liability Protection Do You Need?

Liability coverage protects you if someone is injured on your property or in your vehicle, and this is where many people underestimate their risk. Standard homeowners policies include $100,000 to $300,000 in liability coverage, but medical costs and legal judgments regularly exceed these amounts. If a guest falls down your stairs and requires surgery costing $50,000 in medical bills plus ongoing care, your basic liability limit disappears fast. For auto insurance, most states require minimum liability coverage, but minimums rarely protect your actual assets. If you cause an accident injuring multiple people, the damages can easily reach $500,000 or more. Financial experts recommend $250,000 per person and $500,000 per incident for auto, and $300,000 minimum for home. If you have significant assets or higher income, consider umbrella coverage, which provides an additional $1 million or more in liability protection across both auto and home policies at relatively low cost.

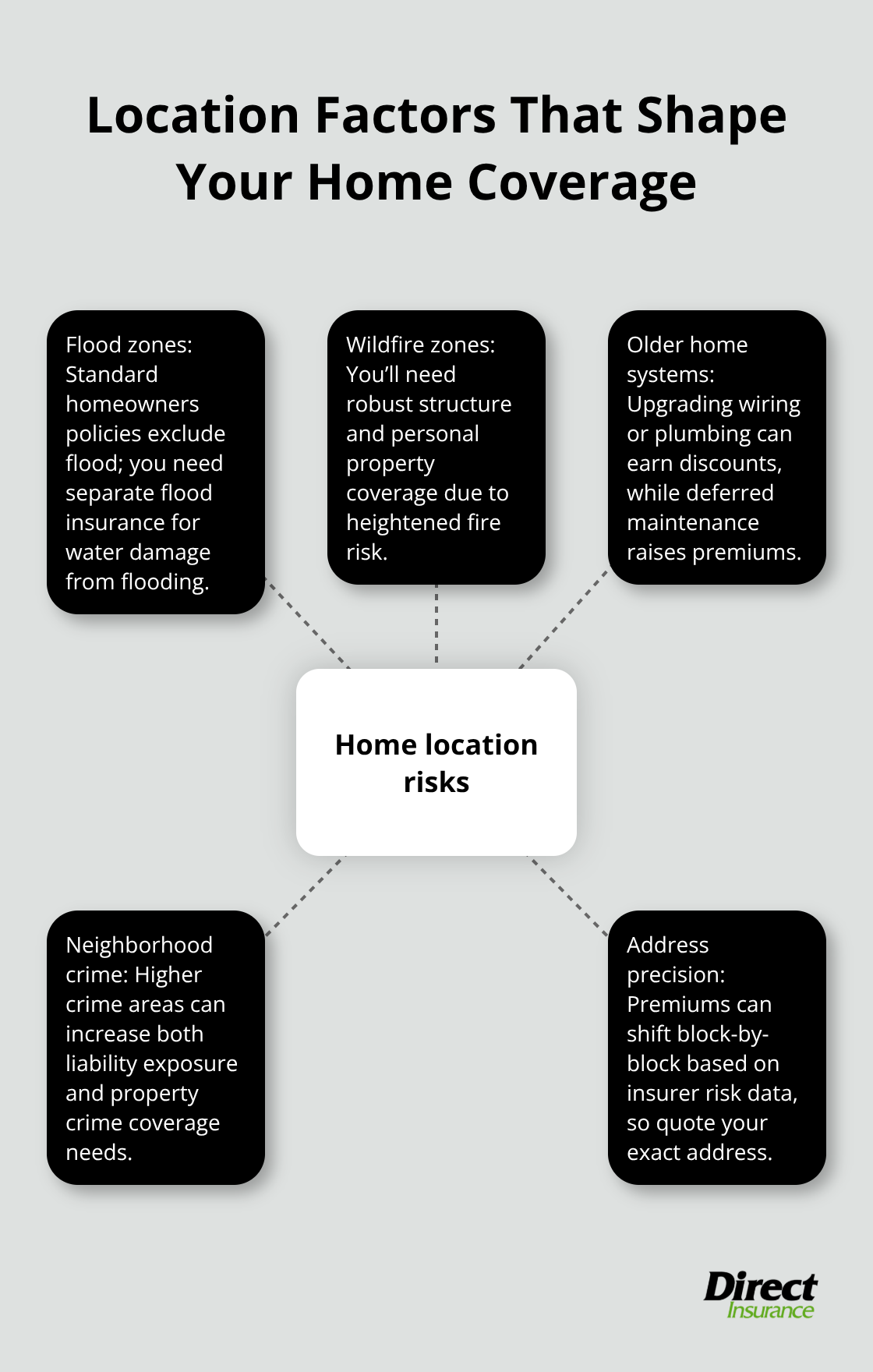

How Your Home’s Location Shapes Your Coverage Needs

Where your home sits determines what specific risks you face and what coverage costs. Homes in flood zones require separate flood insurance since standard homeowners policies exclude water damage from flooding. Homes near wildfire zones need robust coverage for structure and personal property. Older homes with original wiring or plumbing may qualify for discounts if you upgrade systems, but insurers also charge more for homes with deferred maintenance.

Crime rates in your neighborhood affect both your liability risk and your property crime coverage needs. Get specific quotes for your exact address rather than generalizing from neighborhood averages. The difference between one side of a street and the other can shift your premium significantly based on local risk data that insurance companies track closely.

Moving Forward With Your Coverage Assessment

Once you understand what coverage you actually need, you’re ready to shop for quotes that match those requirements. This is where most people make their second mistake-they compare prices without comparing the actual protection each policy provides.

Compare Quotes from Multiple Insurance Companies

Getting quotes from at least three different providers is non-negotiable if you want real savings. Most people call one or two insurers, receive a number, and assume that’s the market rate. It’s not. Insurance pricing varies wildly based on how each company weighs your specific risk factors. USAA quotes $1,499 annually for auto while another carrier quotes $2,607 for identical coverage. State Farm bundles your home and auto for $2,090 in auto plus $2,185 in home, while American Family could quote $2,607 and $2,745 respectively. These aren’t small differences. Over five years, choosing the wrong carrier costs you thousands.

When you request quotes, provide identical information to each company: same vehicle details, same home specifications, same coverage limits, same deductibles. Apples-to-apples comparisons matter because insurers structure their base premiums differently. Some start with a lower foundation premium and apply smaller discounts. Others quote higher base rates but offer aggressive bundling discounts that actually bring your total cost down. You won’t know which strategy benefits you until you compare the final numbers side by side.

How Bundling Discounts Actually Work

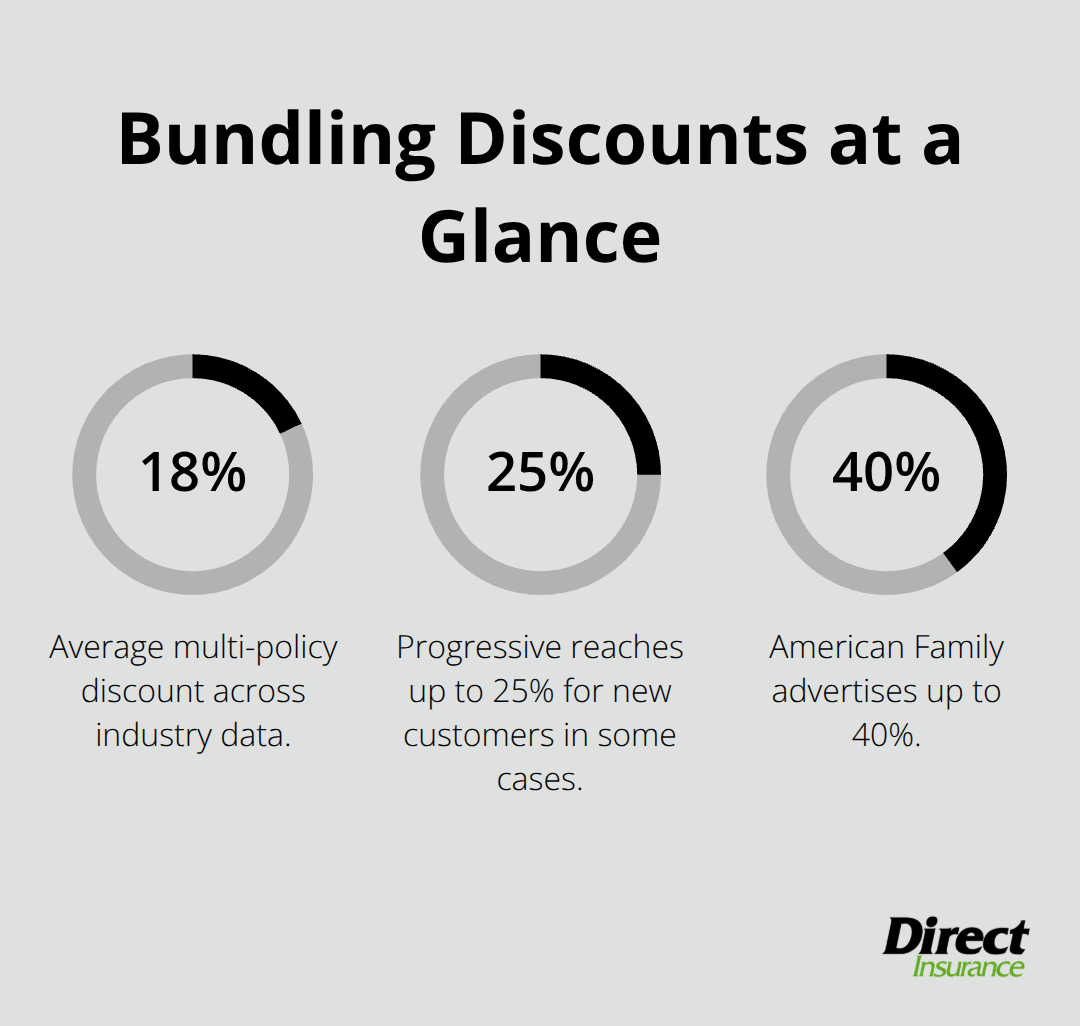

Multi-policy discounts average around 18 percent according to industry data, which translates to roughly $900 annually on a $5,000 insurance bill. But this number masks critical variation. USAA offers up to 10 percent bundling discount. Progressive reaches up to 25 percent for new customers in some cases.

American Family advertises up to 40 percent. State Farm customers save up to $1,429 per year on average through bundling.

The actual savings you receive depends on your location, credit history, driving record, home age, and dozens of other variables. Don’t assume the advertised discount applies to you. When comparing quotes, verify that the discount applies to both your auto and homeowners policies within the bundle. Some carriers apply the discount only to auto or only to home. Others layer multiple discounts so your final savings exceed the headline bundling percentage.

Ask each insurer directly: What is my bundling discount percentage? What discounts stack on top of it? What happens to my rate at renewal? This last question matters because premiums often increase after year one. Bundle discounts can be significant, so you might want to shop around for a new insurance company that offers both policy types. Shopping annually protects you from paying inflated renewal rates that erode your bundling advantage.

Deductible Strategy Within Your Bundle

Your deductible choice directly controls your monthly premium. Raising your deductible from $500 to $1,000 on both auto and homeowners typically reduces your bundled premium by 15 to 25 percent. But this works only if you can actually afford to pay that deductible out of pocket when you need to file a claim. Setting a $2,500 deductible to save $40 monthly creates a trap: one accident or roof claim forces you into financial stress.

Try the $1,000 deductible sweet spot, which offers meaningful savings without creating hardship if claims occur. Many customers successfully use this level. Additionally, ask whether bundled policies allow different deductible levels across your auto and home coverage. Some carriers require matching deductibles within a bundle. Others let you set higher deductibles on policies you rarely claim against and lower deductibles on your higher-risk coverage (this flexibility saves money without increasing your actual risk exposure). Clarify these options before committing to a quote because your deductible structure directly impacts both your premium and your financial security.

What to Verify Before You Commit

Before you accept any bundled quote, confirm that the discount applies to both policies and that you understand what happens at renewal. Verify the exact coverage limits match your needs from the earlier assessment. Check whether the insurer allows you to customize coverage within the bundle or whether bundling locks you into specific options. Some carriers bundle aggressively but limit your ability to adjust liability limits or add optional coverages. Others provide full flexibility.

The cheapest quote means nothing if it forces you into inadequate coverage or inflexible options that don’t match your actual situation. Once you’ve compared quotes and verified the details, you’re ready to optimize your bundle for both cost and protection.

Optimize Your Bundle for Cost and Protection

Unlock Hidden Discounts Beyond the Base Bundle

The gap between a good bundled quote and a great one often comes down to features you haven’t asked about yet. After you’ve compared prices from multiple carriers, your next step is identifying which discounts actually apply to your specific situation. Usage-based insurance programs track your driving habits through a mobile app or device installed in your vehicle. Insurers like Progressive and Liberty Mutual offer these programs, and they work best if you’re a low-mileage driver or someone with genuinely safe driving patterns.

Before you commit to a bundle, ask whether the carrier offers usage-based discounts and whether bundling qualifies you for additional savings on top of the multi-policy discount. Some carriers layer discounts aggressively, while others cap total savings at a specific percentage. Safety features matter too-installing anti-theft devices, security systems, or upgrading to newer vehicles with advanced safety technology can unlock additional discounts on your homeowners and auto policies. Ask your insurer for a complete list of discounts you qualify for right now, not just the bundling discount. Many people miss 5 to 15 percent in additional savings simply because they don’t ask.

Watch Your Renewal Rate Carefully

Renewal rates reveal the true cost of bundling, and this is where you need to be skeptical. Insurance companies often quote aggressively in year one to win your business, then increase rates significantly at renewal. If your bundled rate jumps 20 percent after year one, you’ve lost most of your bundling advantage and you’re overpaying compared to what competitors would quote you.

Track your renewal rate increase annually and compare it against current quotes from at least two other carriers. If your increase exceeds 8 to 10 percent, shopping around almost always saves money. This annual comparison protects you from paying inflated renewal rates that erode your bundling advantage over time.

Evaluate Claims Processing Speed and Service Quality

Claims processing speed and customer service quality matter because bundling only works if you actually receive payment quickly when something goes wrong. Call your prospective insurer’s claims line before you sign up and ask how long it takes to process a homeowners claim or an auto claim. Ask whether you can file claims through a mobile app or whether you must call an agent. Request their average claims processing time in writing if possible.

Some carriers process simple claims in 48 hours. Others take two weeks. That difference matters when you’re without your vehicle or dealing with roof damage. Liberty Mutual and State Farm both rank highly for claims handling speed, but regional carriers sometimes outperform national companies in specific states. We at Direct Insurance Services work with multiple top-rated insurers and understand their actual performance in Utah, so we can help you evaluate which carriers deliver the fastest claims service in your area.

Final Thoughts

Finding the best car and home insurance bundle requires three concrete steps: assess your actual coverage needs based on your assets and location, compare quotes from at least three carriers with identical specifications, and verify that bundling discounts apply to both policies before you commit. Your coverage limits matter more than your premium because underinsuring creates financial exposure that no discount justifies. When you compare quotes, look beyond the headline bundling percentage and examine your total annual cost across both policies, since an insurer advertising 40 percent bundling might still cost more than a competitor offering 15 percent if their base rates are higher.

Track what you actually pay at renewal because bundling advantages disappear quickly if your rate jumps 20 percent after year one. Shopping annually protects you from this trap and ensures you don’t overpay for coverage that competitors would quote at lower rates. The best car and home insurance bundle matches your coverage needs, delivers genuine savings, and processes claims quickly when you need it.

We at Direct Insurance Services have helped thousands of Utah customers navigate this process since 1973. As an independent agency, we shop multiple top-rated insurers to find coverage that fits your specific situation and budget. Contact Direct Insurance Services and let our local team handle the comparison work instead of spending hours calling carriers individually.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation