Commercial Auto Insurance in Utah for Your Business

Utah businesses operating commercial vehicles face specific insurance requirements that go beyond standard auto coverage. Commercial auto insurance Utah regulations include state minimums, federal DOT standards, and industry-specific mandates.

We at Direct Insurance Services understand these complex requirements can impact your bottom line significantly. The right coverage protects your business assets while meeting all legal obligations.

What Are Utah’s Commercial Auto Insurance Requirements?

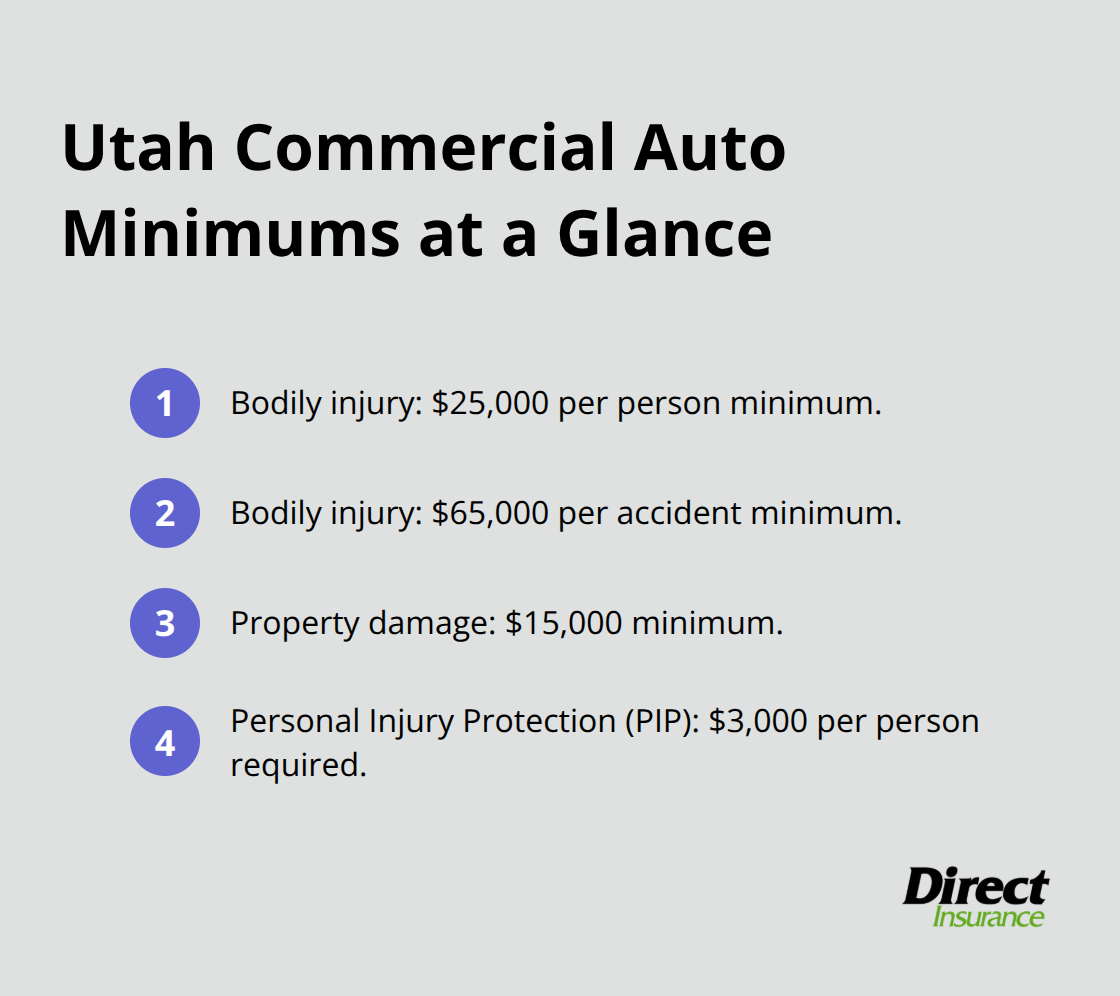

Utah law mandates specific minimum liability coverage for all commercial vehicles: $25,000 per person for bodily injury, $65,000 per accident for bodily injury, and $15,000 for property damage. Personal injury protection of $3,000 per person is also required and covers medical expenses regardless of fault. These state minimums represent the absolute floor, but smart businesses carry $1 million or more in liability coverage to protect against claims that could bankrupt a company.

Federal DOT Standards Add Complexity

Commercial vehicles that cross state lines or weigh over 10,001 pounds must meet Federal Motor Carrier Safety Administration requirements. Interstate truckers need minimum liability coverage of $750,000 for general freight, while hazardous materials transporters require $5 million. The USDOT also mandates specific procedures and continuous coverage verification. Companies that operate without proper federal compliance face penalties up to $16,000 per violation (making compliance non-negotiable for interstate operations).

Industry-Specific Mandates Vary Dramatically

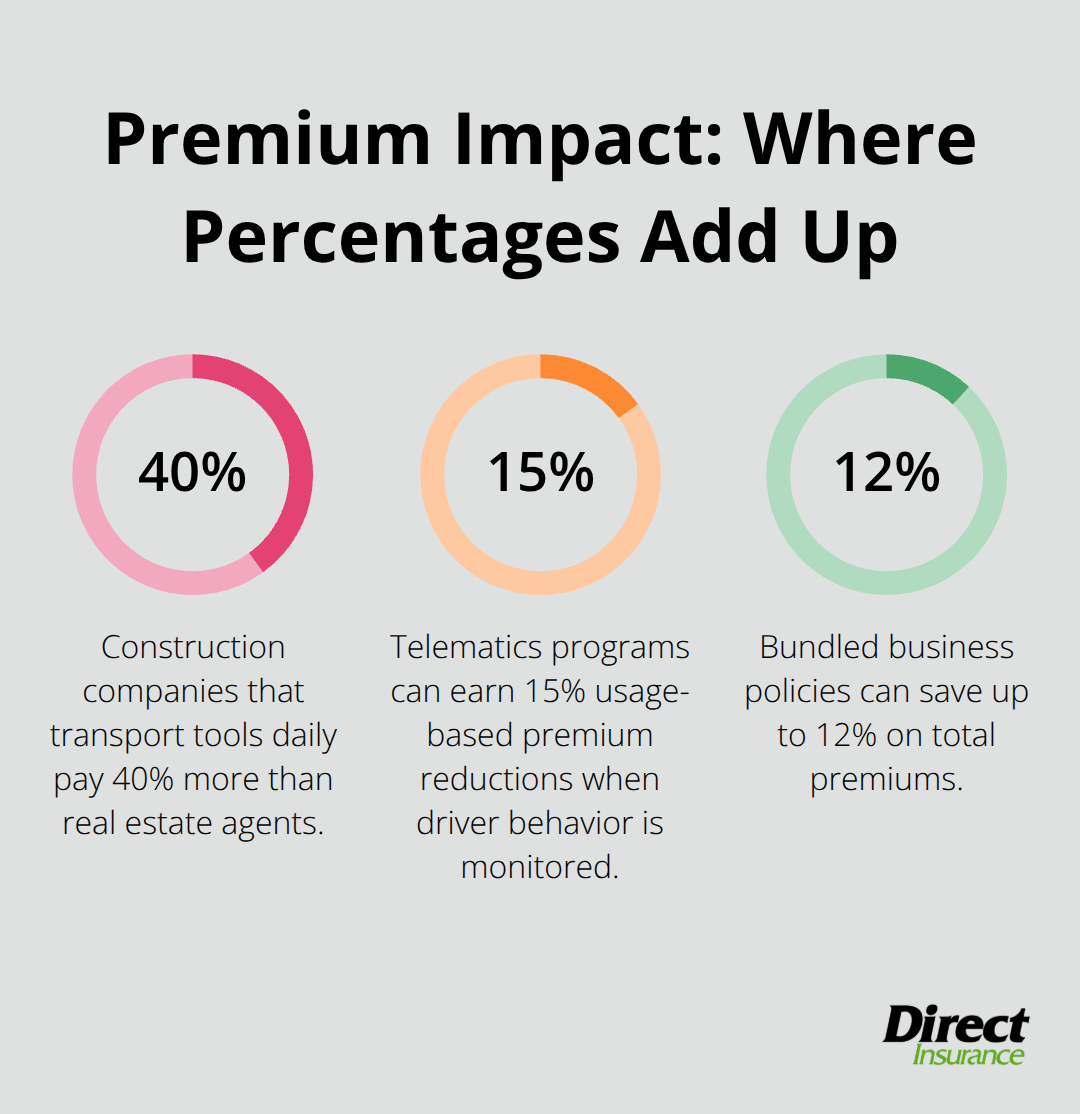

Food trucks in Utah face average premiums of $3,200 annually due to specialized equipment risks, while standard service vehicles average $1,800. Construction companies that transport tools daily pay 40% more than real estate agents who make occasional client visits. Taxi and limousine services require commercial policies with passenger liability endorsements, as personal policies exclude fare-paying passengers entirely.

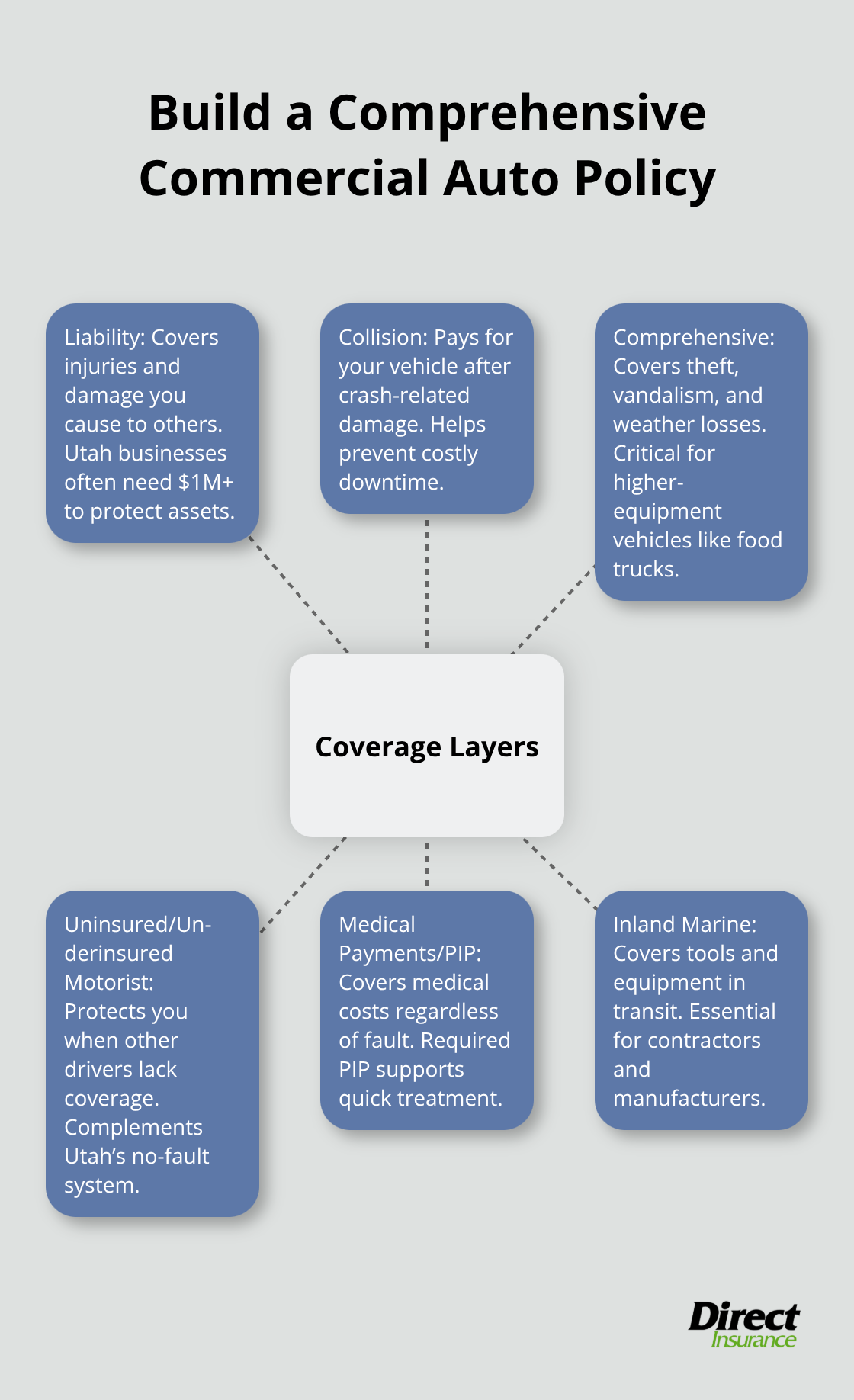

Equipment Transport Demands Additional Coverage

Manufacturing and landscaping businesses need inland marine coverage for transported equipment. This coverage adds $200-500 annually to base premiums but prevents massive equipment replacement costs. Contractors who transport valuable tools between job sites face similar requirements (with premiums that reflect the equipment’s value and theft risk).

These requirements form the foundation for commercial auto coverage, but businesses need to understand the specific types of protection available to build comprehensive policies that match their operations.

Which Coverage Types Protect Your Utah Business Vehicles

Liability coverage forms the backbone of commercial auto insurance, but Utah businesses need more than state minimums to survive major claims. Companies pay $130 per month on average for basic coverage, yet comprehensive protection requires strategic layers of multiple coverage types. Smart business owners build policies that address their specific operational risks rather than accept one-size-fits-all packages.

Liability Coverage Protects Against Lawsuits

Bodily injury liability covers medical expenses, lost wages, and legal fees when your business vehicle injures someone. Property damage liability handles repairs to other vehicles, buildings, or equipment your driver damages. Utah requires $90,000 minimum coverage in any one accident for bodily injury or property damage combined, but this won’t protect against serious accidents that generate six-figure claims. Businesses should carry at least $1 million in liability coverage, while high-risk operations like construction or delivery need $2 million or more to protect company assets from devastating lawsuits.

Physical Damage Coverage Prevents Business Interruption

Collision coverage averages $3,995 per claim according to industry data, while comprehensive coverage handles $1,621 in average damages from theft, vandalism, or weather events. Food trucks face particularly high comprehensive claims due to expensive equipment exposure (making this coverage non-negotiable for mobile food operations). Construction companies that transport tools daily need both collision and comprehensive protection, as equipment replacement costs can exceed vehicle values. Higher deductibles between $1,000-2,500 reduce premiums by 15-20% while they maintain protection against catastrophic losses.

Uninsured Motorist Protection Fills Critical Gaps

Utah’s no-fault system requires personal injury protection, but uninsured motorist coverage protects against drivers who lack adequate insurance. Medical payments coverage extends beyond PIP requirements and covers passengers and employees who suffer injuries in business vehicle accidents. Businesses that operate in Salt Lake City face 20-25% higher accident risks than rural areas (making these additional protections essential for companies with multiple drivers or frequent urban operations).

These coverage types work together to create comprehensive protection, but the actual costs depend on several key factors that vary significantly across Utah’s diverse business landscape.

What Drives Your Utah Commercial Auto Premium Costs

Your commercial auto insurance costs in Utah depend on three primary factors that insurance companies analyze to assess risk. Vehicle type creates the biggest premium variations, with different vehicle classes having varying insurance requirements and costs. An electrician who transports tools daily pays significantly higher premiums than a real estate agent who makes occasional client visits, as tool transport increases theft and equipment liability risks. Food trucks face average annual premiums of $3,200 compared to $1,800 for standard service vehicles because expensive cooking equipment creates higher comprehensive claims. Heavy-duty vehicles generally cost more to insure than light commercial vehicles, with pickup trucks used for landscaping averaging $2,400 annually while delivery vans average $1,900.

Driver History Determines Base Rates

Clean driving records can save companies 25-30% on premiums compared to policies that cover drivers with violations or accidents. Each driver’s past accidents, speeding tickets, and DUI convictions directly impact your policy costs, which makes driver screening absolutely essential for cost control. Companies with formal safety programs reduce premiums by 10-15% through documented training and monitoring systems. Telematics devices and GPS tracking help qualify for usage-based discounts, with some insurers offering 15% reductions for businesses that monitor driver behavior actively.

Geographic Territory Shapes Premium Structure

Salt Lake City businesses face 20-25% higher premiums than rural regions due to increased traffic density and accident frequency. Local routes in smaller cities like St. George present lower risk than regional routes (potentially reducing insurance costs by hundreds of dollars annually). Areas prone to natural disasters may incur higher premiums due to comprehensive coverage risks, while businesses that operate across state lines face additional compliance verification requirements that can increase administrative costs. Companies should document vehicle usage patterns comprehensively to secure accurate territorial ratings and avoid overpayment for coverage areas they don’t actually operate in.

Business Operations Impact Risk Assessment

Insurance companies evaluate how you use your vehicles to determine appropriate rates. Delivery services face higher premiums than consulting businesses because frequent stops and urban navigation increase accident exposure. Construction companies that haul equipment between job sites pay more than office-based businesses that use vehicles occasionally (reflecting the increased liability from heavy equipment transport). Manufacturing businesses need specialized coverage for transported goods, which adds $200-500 annually to base premiums but prevents massive replacement costs when equipment gets damaged or stolen.

Final Thoughts

Proper commercial auto insurance Utah coverage protects your business from financial devastation while it meets all legal requirements. Companies with adequate coverage avoid $400 fines, license suspensions, and potentially devastating lawsuits that could destroy years of hard work. Smart business owners document their vehicle usage patterns and driver records accurately to secure appropriate rates.

Multiple insurers offer different rates, so comparison shopping becomes essential for cost control. Bundled policies can save up to 12% on total premiums, while higher deductibles between $1,000-2,500 reduce costs by 15-20% and maintain protection against major losses. These strategies help businesses balance comprehensive coverage with budget constraints.

Local expertise makes the difference between adequate coverage and comprehensive protection that addresses Utah’s unique risks. We at Direct Insurance Services shop multiple top-rated insurance companies to find competitive rates for Utah businesses. Our team understands complex federal DOT requirements and industry-specific mandates that generic online quotes cannot address effectively (helping you navigate regulations while maintaining budget flexibility).