How to Save Money on Your Auto Insurance Premiums

Auto insurance premiums continue rising across the United States, with the average driver paying $1,895 annually in 2024. Learning how to save on auto insurance has become a financial priority for millions of families.

We at Direct Insurance Services see drivers overpaying by hundreds of dollars each year simply because they haven’t explored available options. The right strategies can reduce your premiums by 20-40% without sacrificing coverage quality.

What Really Drives Your Insurance Costs

Your driving record stands as the single most powerful factor that affects your premium rates. Insurance companies track every violation, accident, and claim for three to five years, with major incidents like DUI convictions that keep rates elevated for up to seven years. Drivers with clean records pay 34% less than those with violations (according to Progressive data). A single speeding ticket can increase your premium by $480 annually, while an at-fault accident typically adds $800-1,200 to your yearly costs. Many drivers remain unaware that even minor infractions create financial impacts that last for years.

Vehicle Selection Impacts Premium Costs

The car you drive directly determines your insurance expenses through repair costs, theft rates, and safety ratings. Luxury vehicles and sports cars cost significantly more to insure due to expensive parts and higher theft rates. A Honda Civic costs roughly $1,400 annually to insure, while a BMW 3 Series averages $2,100 for identical coverage. Vehicle age creates a sweet spot around 5-8 years old where depreciation reduces comprehensive costs while safety features remain current. Cars older than 10 years may warrant the decision to drop collision coverage entirely, which potentially saves $1,165 annually when coverage exceeds 10% of vehicle value.

Geographic Location Creates Major Rate Differences

Your ZIP code influences premiums more than most drivers realize, with urban areas that consistently cost 15-25% more than rural locations. Florida drivers pay average premiums that exceed $3,500 annually while Maine residents average just $1,200 for similar coverage. A move from suburban areas to city centers can increase costs by 8% or more due to higher theft rates, vandalism, and accident frequency. Weather patterns also affect rates, with hail-prone regions like Colorado and Texas that see elevated comprehensive premiums during storm seasons.

These factors work together to create your base premium, but smart drivers know how to work within these constraints to find significant savings through strategic choices and comparison tactics.

How Can You Cut Your Insurance Costs in Half

Most drivers waste hundreds of dollars annually because they accept the first quote they receive or stick with the same insurer for years without comparison shopping. Consumer Reports found that 30% of policyholders who switched companies saved $461 annually. The key lies in obtaining quotes from at least five different insurers, as rates can vary by $1,000 or more for identical coverage.

Independent agents provide access to multiple carriers simultaneously, which eliminates the time-consuming process of contacting each company individually.

Maximize Every Available Discount

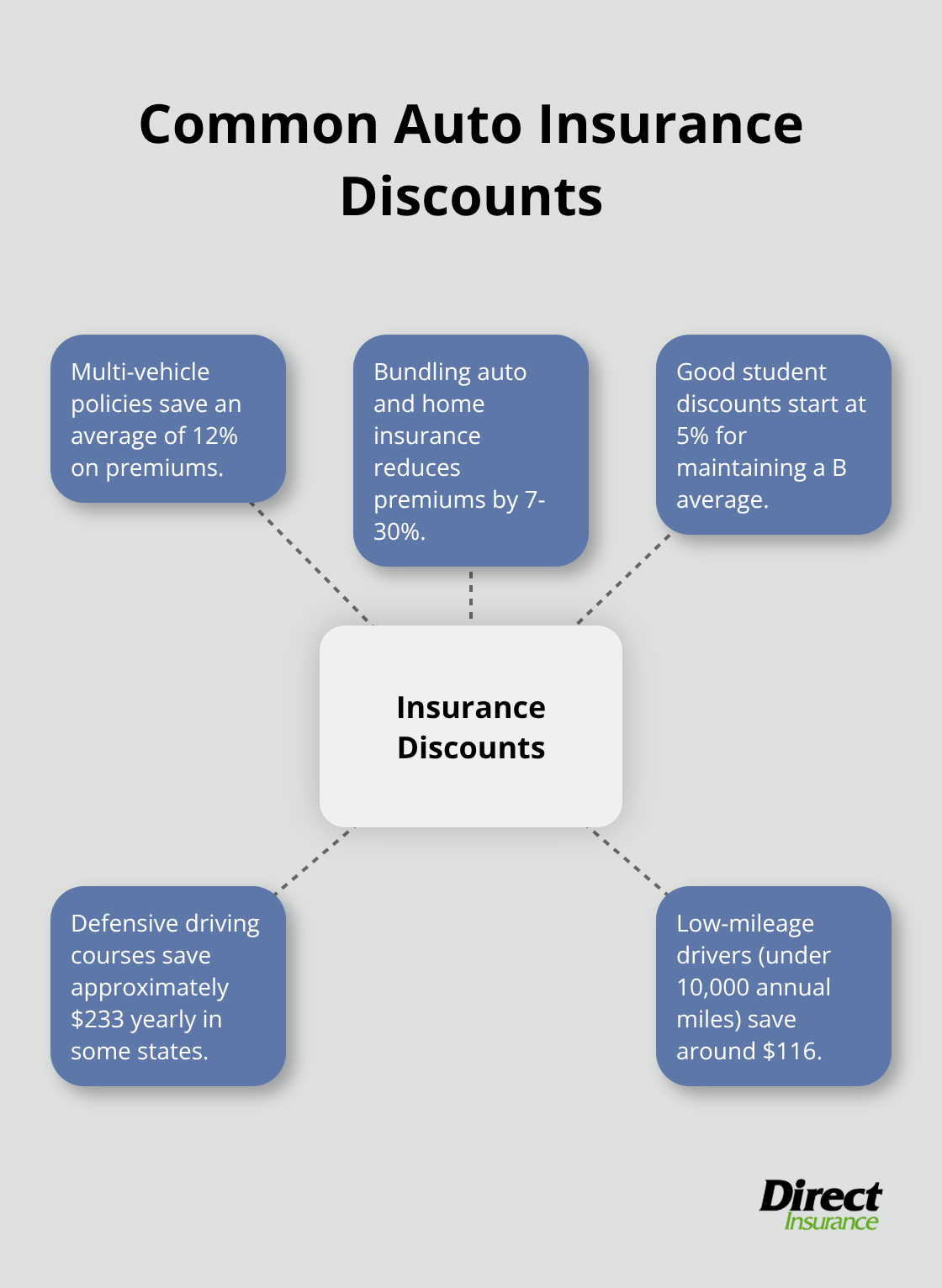

Insurance companies offer dozens of discounts that most drivers never claim. Multi-vehicle policies save an average of 12%, while bundling auto and home insurance reduces premiums by 7-30% (according to the Consumer Federation of America).

Good student discounts start at 5% for maintaining a B average, defensive driving courses save approximately $233 yearly in states like New York and Virginia, and low-mileage drivers who report under 10,000 annual miles save around $116. Automated monitoring programs like Snapshot provide personalized rates based on actual driving behavior, with safe drivers who save an average of $322 annually.

Strategic Coverage Adjustments Generate Real Savings

Raising your deductible from $500 to $1,000 reduces premiums by 20-25%, which saves $464 to $525 annually according to the Insurance Information Institute. This strategy works best for drivers with emergency funds who can handle higher out-of-pocket costs. Older vehicles warrant careful coverage evaluation, as dropping collision and comprehensive on cars worth less than $3,000 can save $1,165 yearly when coverage costs exceed 10% of vehicle value.

However, minimum liability limits of $30,000 per person prove inadequate for serious accidents, with experts who recommend $100,000/$300,000/$100,000 coverage despite slightly higher premiums that provide substantially better protection.

These proven strategies work together to create substantial savings, but Utah drivers face unique opportunities and challenges that require specific approaches tailored to local conditions and state requirements.

What Utah-Specific Strategies Cut Insurance Costs Most

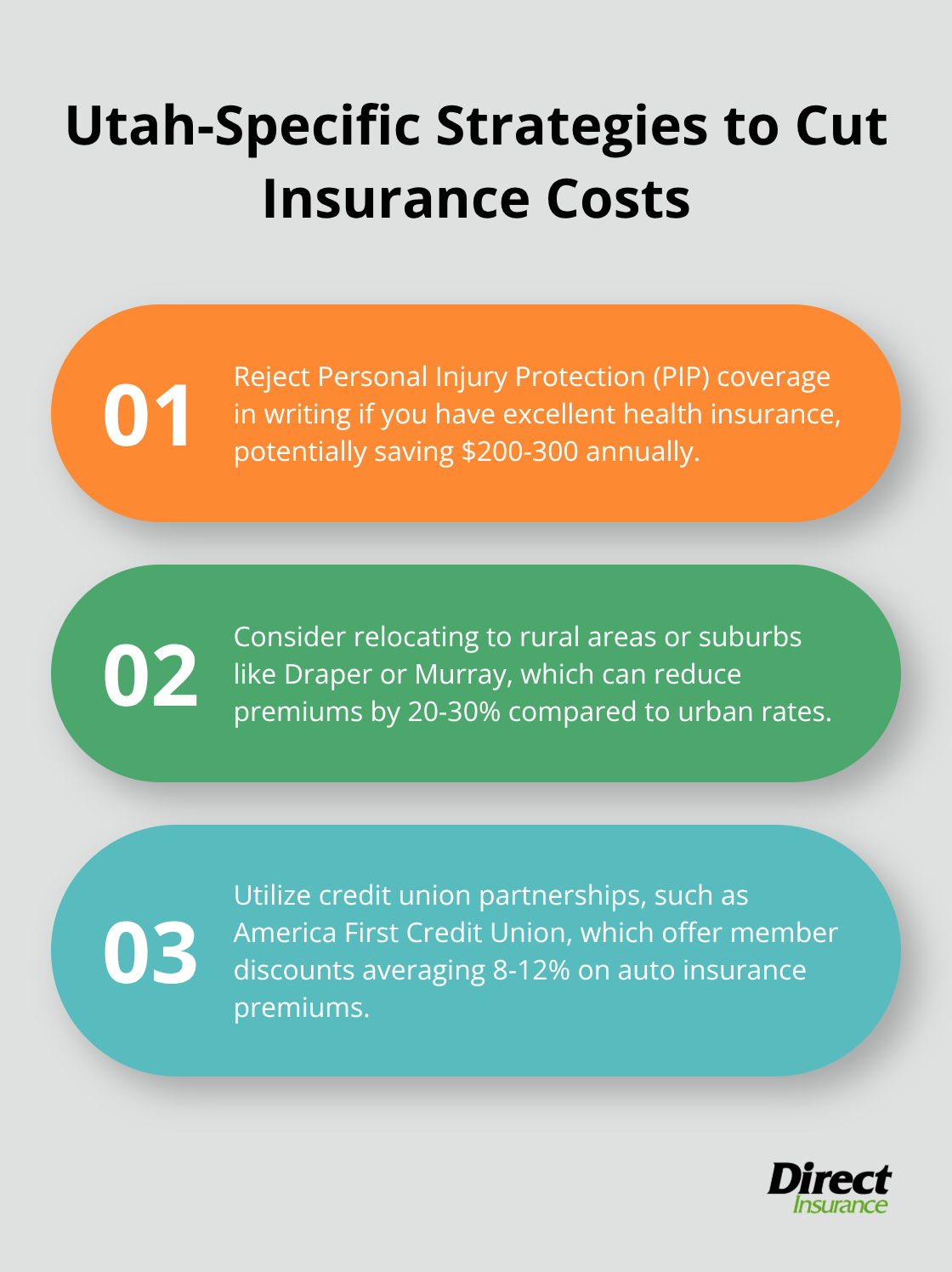

Utah drivers face unique insurance challenges that create specific money-saving opportunities most residents never explore. The state’s no-fault insurance system requires Personal Injury Protection coverage, but Utah allows drivers to reject this coverage in writing, which saves approximately $200-300 annually for those with excellent health insurance. Utah’s relatively low population density outside Salt Lake City and Provo creates significant rate variations, with rural drivers who pay 20-30% less than urban residents. A move just 15 miles from downtown Salt Lake City to suburbs like Draper or Murray can reduce premiums by $400-600 yearly while you maintain reasonable commute times.

Winter Weather Creates Hidden Savings Opportunities

Utah’s severe winter conditions actually provide insurance advantages that most drivers overlook. Comprehensive coverage becomes more valuable due to hail damage risks along the Wasatch Front, but drivers can increase deductibles to $1,000 during summer months then reduce them before winter storm season. Many Utah insurers offer seasonal storage discounts for vehicles that owners garage during heavy snow months, with savings that reach $150-200 annually. Anti-theft devices become particularly valuable in Utah due to higher theft rates in ski resort areas, with GPS systems that provide discounts of 5-10% while they offer practical benefits during winter emergencies.

Local Insurer Programs Target Utah Conditions

Regional insurers like Mountain West Farm Bureau offer Utah-specific programs that national companies cannot match. These local carriers understand Utah’s unique risks that include flash floods in southern counties and frequent deer collisions along mountain highways. Farm Bureau provides agricultural equipment discounts for rural properties and offers specialized coverage for recreational vehicles popular among Utah outdoor enthusiasts. Credit union partnerships through institutions like America First Credit Union provide member discounts that average 8-12% on auto insurance premiums (with some reaching 15% for long-term members). Utah drivers who maintain continuous coverage while they attend college out-of-state can preserve their local rates and discounts, which creates substantial savings when they return to Utah after graduation.

Final Thoughts

Auto insurance savings require multiple strategies that work together to create substantial reductions in your premiums. Smart drivers who shop around save $461 annually on average, while those who maximize discounts and adjust coverage levels reduce premiums by 20-40% without sacrificing protection. Utah drivers have additional advantages through state-specific programs, seasonal adjustments, and local insurer partnerships that national companies cannot match.

The combination of strategic deductible increases, discount maximization, and geographic considerations creates savings opportunities that reach $1,000 or more annually. Insurance rates change constantly, and your personal situation evolves over time. Annual policy reviews help you capture new discounts, adjust coverage levels, and identify better rates from competing insurers (making this the most overlooked money-saving strategy).

We at Direct Insurance Services help Utah families save hundreds of dollars when they shop multiple top-rated insurance companies. Our local expertise helps identify Utah-specific savings opportunities that out-of-state agents miss. Contact our Salt Lake City team to learn how to save on auto insurance with personalized coverage recommendations that fit your budget and protect your family.