How to Find the Best Home Auto Insurance Bundle

Finding the best home auto insurance bundle requires more than just picking the first offer you see. The right combination of coverage can save you hundreds of dollars annually while protecting what matters most.

At Direct Insurance Services, we help Utah homeowners and drivers navigate the bundling process with clarity. This guide walks you through comparing quotes, selecting appropriate coverage levels, and making a decision that fits your specific situation.

What Makes a Home and Auto Bundle Actually Worth It

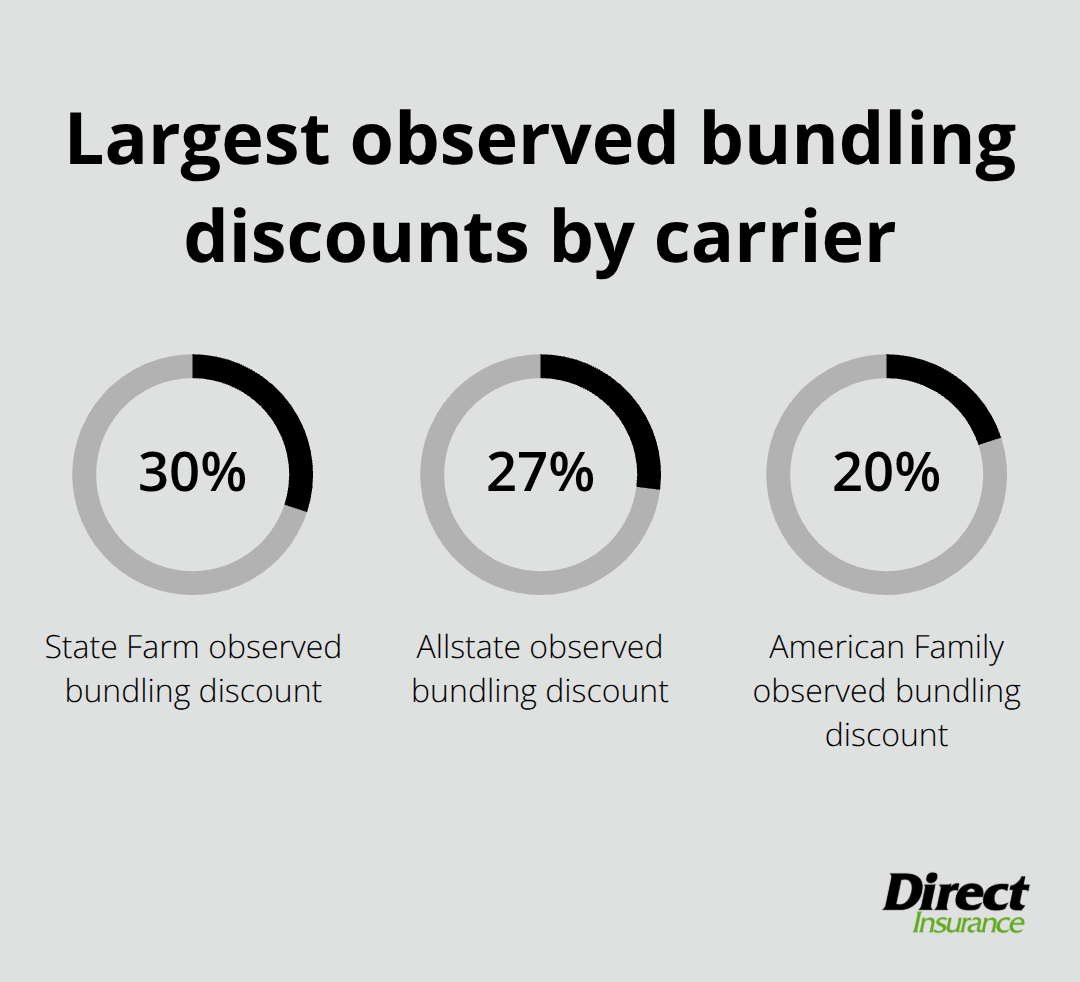

A bundle only makes financial sense when the combined discount exceeds what you’d pay for separate policies. According to The Zebra’s 2026 data, homeowners save an average of 10% when bundling home and auto insurance, while renters see about 5% savings. However, these are averages-your actual savings depend entirely on your location, profile, and the carriers you compare. The largest observed discounts come from State Farm at around 30%, Allstate at 27%, and American Family at 20%, according to The Zebra’s analysis.

This means a bundle from one carrier might save you significantly more than a bundle from another. Most people skip the critical step of comparing bundled quotes against unbundled quotes from multiple carriers. You might find that auto insurance from one company and home insurance from another costs less than a single-insurer bundle, even though bundling sounds simpler.

Real Savings Numbers to Expect

Bundling discounts typically range between 5% and 30% depending on the insurer and available discounts, according to industry data. State Farm’s multi-policy discount averages nearly 25% off car and home insurance. Progressive offers up to 25% bundle savings, while USAA provides up to 10% for military-connected members. American Family tops the list with up to 40% bundling discounts available in some states. These numbers matter because they show the potential range you should expect when shopping. If an insurer quotes you a 2% bundle discount, that’s below market average and worth questioning. Location dramatically affects your actual savings-a bundle discount in Utah might look different from the same carrier’s offer in another state due to local risk factors and regulatory differences.

What Actually Makes Bundling Valuable Beyond Discounts

The financial benefit extends beyond the advertised discount percentage. When you bundle, some carriers offer combined deductibles across home and auto claims, meaning you pay one deductible instead of two if both policies are affected by the same event. You also receive simplified billing with one payment instead of two, which reduces the chance of missed deadlines. The real value emerges when you factor in convenience-you manage policy documents, coverage updates, and claims through a single contact point, which saves time and reduces confusion. However, this convenience means nothing if the bundled rate isn’t competitive. The Zebra’s research shows that many customers benefit from working with independent agents who can quote both bundled and unbundled rates from multiple carriers, then recommend the actual cheapest option rather than the most convenient one.

How to Spot a Bundle That Actually Works for Your Situation

Not every bundle works for every household. A bundle that saves State Farm customers 30% might only save you 8% because your location, driving record, home age, and credit profile all affect the final price. You need to compare quotes from at least three providers and evaluate both bundled and unbundled options side by side. When you request quotes, ask each carrier for the bundled discount amount in dollars, not just percentages-this removes ambiguity. Some carriers partner with separate home insurers, which means your “bundle” isn’t truly unified; verify that you can manage both policies in one place and that the discount reflects genuine consolidated savings. The mix-and-match strategy often wins: sometimes auto from one carrier and home from another yields a lower total cost than any single-carrier bundle available to you.

Your next step involves gathering the right information to compare these quotes accurately.

Comparing Insurance Quotes From Multiple Carriers

Getting accurate quotes from at least three different insurers is non-negotiable if you want the best bundle price. Most people contact one or two carriers and accept the first bundled offer, which costs them money. These aren’t small differences. A 15% variance in your total premium means hundreds of dollars annually.

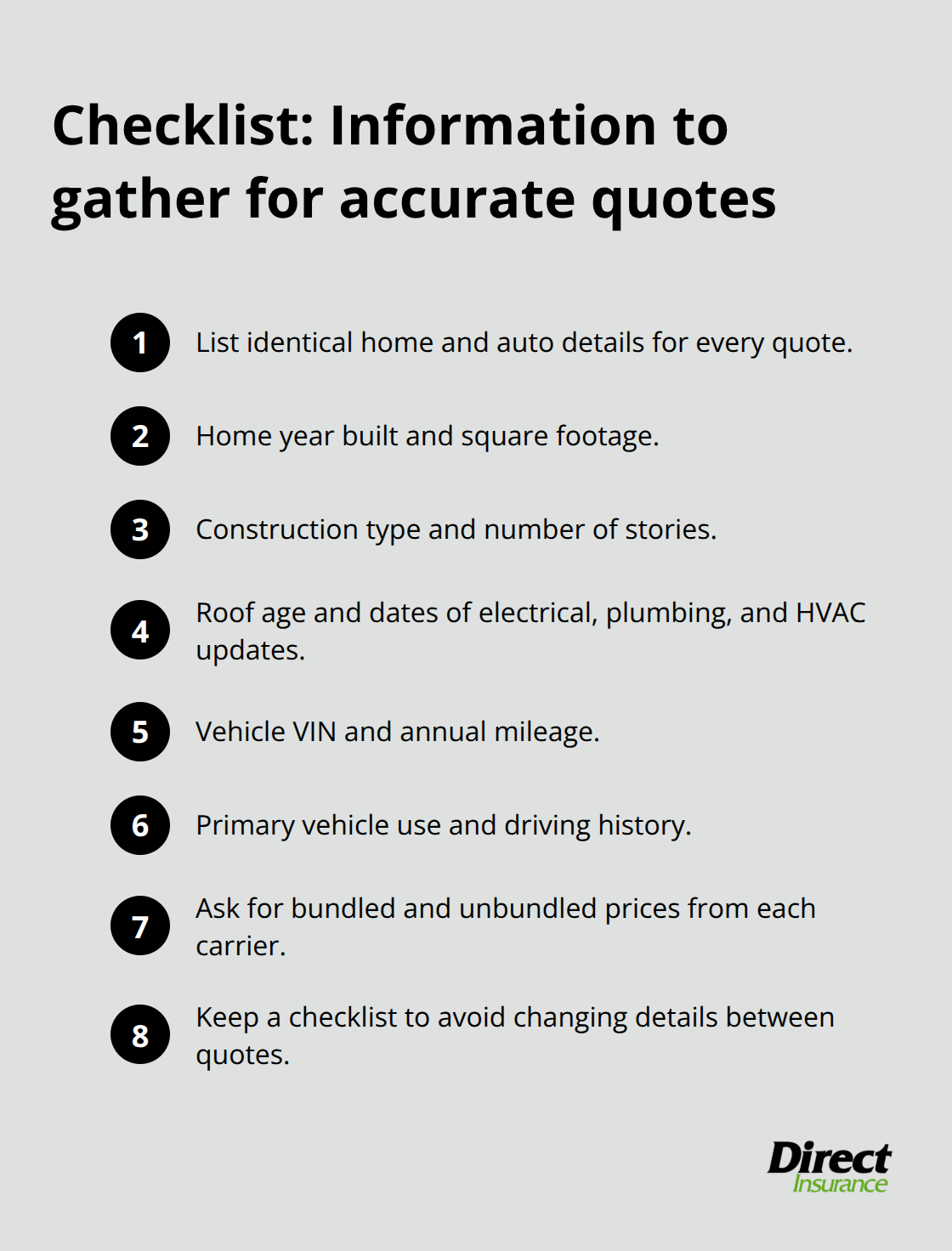

When you request quotes, you need identical information across all three carriers so the prices are actually comparable. Provide the same home value, the same vehicle details, the same coverage limits, and the same deductibles to each insurer. Many people accidentally change details between quotes, which makes comparison impossible. Ask each carrier explicitly for the bundled discount amount in dollars, not just the percentage-this prevents confusion and shows you the actual savings. Some carriers like Progressive and USAA advertise aggressive discounts, but your personal profile determines whether you qualify for the full amount.

Location matters tremendously. A bundle discount in Salt Lake City might differ from the same carrier’s offer in another Utah county due to local risk factors and claim history.

What Information You Need to Collect

Prepare a complete list of details before contacting any insurer. For your home, gather the year built, square footage, construction type, roof age, number of stories, and the last time you updated electrical, plumbing, or HVAC systems. Older systems and outdated wiring increase premiums significantly. For your vehicle, have the VIN, annual mileage, primary use, and your driving history ready.

Carriers also need your age, marital status, and credit score since these affect pricing. When you submit quotes online versus through an agent, you’ll receive different results-online quotes sometimes miss available discounts that agents can apply. Request both bundled and unbundled pricing from each carrier so you can verify that bundling actually saves you money compared to separate policies. Some people discover that auto from one carrier and home from another costs less than the cheapest bundle available.

Ask whether the carrier partners with a separate home insurer for bundled policies, because this affects claims coordination and policy management. When comparing final quotes, look beyond the premium amount. Check the deductible structure-some carriers offer combined deductibles for bundled policies, meaning you pay one deductible if both home and auto are affected by the same event. Verify that coverage limits meet your needs; a lower premium means nothing if you’re underinsured.

How to Evaluate Quotes Side by Side

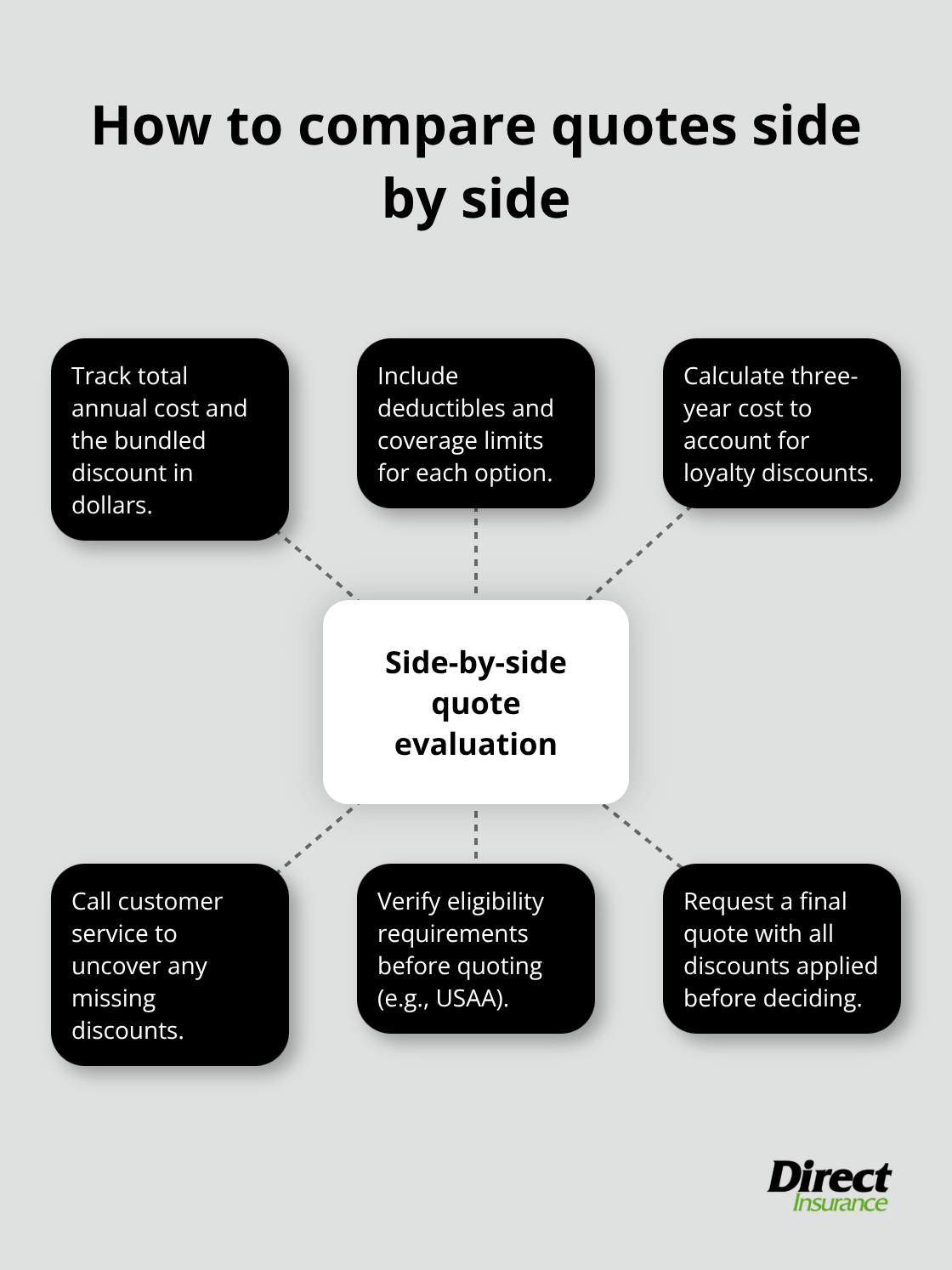

Spreadsheet the quotes so you can see total annual cost, bundled discount amount in dollars, deductibles, and coverage limits side by side. Calculate the three-year cost for each option since some carriers offer loyalty discounts that improve over time. This means your first-year bundle price might improve significantly in years two and three.

Contact the carriers’ customer service departments and ask about discounts you might have missed-discounts for paperless billing, automatic payments, safety features installed in your home, or professional affiliations can add up. Some carriers like USAA limit eligibility to military-connected members, so verify you qualify before spending time on their quotes. Once you’ve narrowed the field to two or three top options, request a final quote with all available discounts applied. Many people accept the first quote without asking about additional savings opportunities. The difference between a standard quote and one with all applicable discounts can exceed 10% on your total premium.

With your quotes in hand and discounts identified, the next step involves selecting the coverage levels that actually protect your situation rather than just minimizing your premium.

Selecting Coverage Amounts That Match Your Actual Risk

The most expensive mistake Utah homeowners and drivers make is choosing coverage levels based on price rather than what actually protects their situation. The right approach involves calculating what you can genuinely afford to lose, then setting your deductible to match that number while ensuring your coverage limits reflect your actual liability exposure and asset values.

Calculate Your Home’s True Replacement Cost

Start with your home’s replacement cost, not its market value. If your house burns down completely, you need enough coverage to rebuild it from the foundation up with current labor and material costs. Utah’s construction costs can be compared using the City Cost Index based on your project location, which means a 2,500-square-foot home requires minimum coverage of $375,000 to $500,000 just for the structure. Many people insure their homes at the purchase price from ten years ago, which leaves them massively underinsured. Get a professional replacement cost assessment from your insurer or a local contractor before selecting coverage limits; this number should guide your dwelling coverage limit, not your gut feeling.

Your personal property coverage should reflect the actual value of what’s inside your home. Conduct a detailed inventory of furniture, electronics, clothing, and other items. Most people dramatically underestimate this value until they actually list everything room by room. If you own valuable items like jewelry, art, or collectibles, those typically need separate riders because standard policies cap coverage per item at $1,500 to $2,500.

Set Liability Coverage That Protects Your Assets

For your vehicle, liability coverage is where most people make dangerous compromises. Utah’s minimum liability is 25/65/15, meaning $25,000 per person and $65,000 per accident for bodily injury, plus $15,000 for property damage. That’s dangerously low. If you cause an accident injuring multiple people or damaging expensive vehicles, you’ll personally owe the difference between your coverage and the actual damages.

Most financial advisors recommend 100/300/100 coverage as a baseline for Utah drivers. The difference in premium between 25/65/15 and 100/300/100 is usually $200 to $400 annually, which is negligible compared to the protection gap. If you have any significant assets to protect, consider even higher limits like 250/500/250.

Choose a Deductible You Can Actually Afford

Your deductible strategy should reflect your emergency fund, not minimize your premium. If you have $2,000 in savings, a $2,500 deductible is reckless because a claim would bankrupt you. Choose a deductible you could actually pay within 30 days without financial hardship. For most Utah households, that’s somewhere between $500 and $1,500.

The premium savings from jumping to a $5,000 deductible often feel attractive until you experience a claim and realize you can’t pay it. Some carriers offer combined deductibles when bundling, meaning a single $1,000 deductible applies if both home and auto claims occur from the same event (which provides modest additional protection).

Verify Coverage Limits in Your Bundle

When bundling, resist the temptation to accept lower limits just because the bundle price looks good. A $10,000 savings on your premium disappears instantly if you’re underinsured for a serious claim. Verify the exact coverage limits match your needs from your earlier assessment, and check whether the insurer allows you to customize coverage within the bundle. An independent agent can help you evaluate whether your bundled coverage actually meets your needs or whether a different combination of carriers would serve you better.

Final Thoughts

The best home auto insurance bundle requires you to compare actual prices from multiple carriers rather than accept the first offer you see. Utah’s specific risks-winter weather, local theft patterns, and construction costs-demand that you request quotes from at least three insurers using identical home and vehicle details. You’ll discover that bundling discounts range from 5% to 40%, but only if you verify that bundling actually saves you money compared to buying separate policies from different carriers.

An independent agent who understands Utah’s insurance landscape identifies discounts you won’t find on your own and spots coverage gaps that online quotes miss. We at Direct Insurance Services have helped Utah families navigate these decisions since 1973, shopping multiple top-rated insurance companies on your behalf to compare both bundled and unbundled options. Contact Direct Insurance Services to have our local agents review your quotes and recommend the option that provides the best coverage at the lowest cost.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation