How to Save with Home and Car Insurance Bundles

Most people don’t realize that bundling your home and car insurance can cut your premiums by hundreds of dollars each year. We at Direct Insurance Services have helped thousands of Utah residents find these savings without sacrificing coverage.

The right bundle simplifies your life in ways that go beyond just lower rates. In this guide, we’ll show you exactly how much you can save and how to find the bundle that works best for your situation.

How Bundling Actually Works

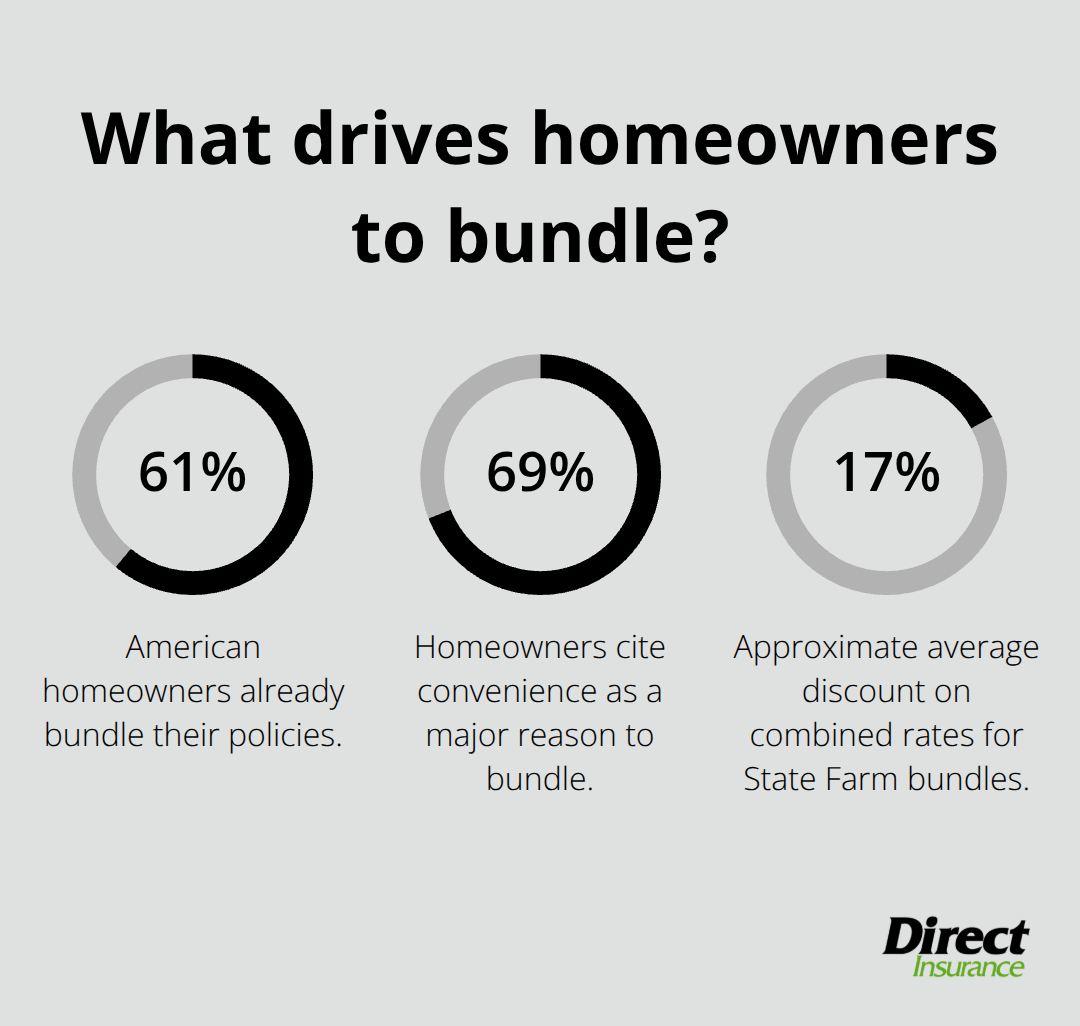

When you bundle home and auto insurance, insurers apply a multi-policy discount to your combined premiums. This isn’t just a marketing gimmick-it’s a real financial incentive that reflects lower risk for the insurance company. According to data from a nationally representative survey of 1,000 U.S. homeowners conducted in December 2025, 61% of American homeowners already bundle their policies, and the primary reason is straightforward: it’s cheaper. The average multi-policy discount ranges from 5% to 30% depending on your insurer and location, though some companies advertise discounts as high as 25%. For example, State Farm bundling can save around $1,356 annually on average-roughly 17% off combined rates. Allstate offers up to 25% off bundled policies, while Progressive typically saves customers around 7% with potential discounts exceeding 25%.

The second major reason people bundle, cited by 69% of surveyed homeowners, is convenience. One agent, one renewal date, one bill, and one login portal eliminates the administrative friction of managing separate policies with different companies.

What Happens When You Add a Second Policy

The discount activates the moment your second eligible policy takes effect. You don’t need to wait for renewal or jump through complicated hoops. If you already have auto insurance with a carrier, adding homeowners coverage immediately qualifies you for the multi-policy discount on both premiums. Liberty Mutual reports new customers who switch and bundle save approximately $950 per year on average. The key is comparing your bundled total against your current separate premiums with identical coverage limits and deductibles-apples to apples. Too many people assume bundling saves money without running the actual math. A cheaper bundled quote that reduces your liability limits or removes important endorsements like water backup coverage could cost far more in claims later. Your mortgage lender also needs notification of any homeowners coverage changes, so inform them immediately when you bundle or switch policies to avoid complications.

Managing Your Bundled Policies

One consolidated bill simplifies your household finances and reduces the risk of missed payments. Digital policy management through mobile apps-offered by most major insurers-lets you access ID cards, file claims, and track coverage from your phone. This matters because 49% of homeowners surveyed said they would bundle for a 10% discount, and 39% would do so for a 20% discount, meaning savings drive the decision for most people. However, if you cancel one bundled policy, you typically lose the multi-policy discount on the remaining policy, so verify your options before making changes. The bundling strategy works best when you evaluate at least three providers in your area, request both bundled and separate quotes, and compare total annual premiums across all options. Once you’ve identified your top candidates, the next step involves assessing whether each bundle actually meets your coverage needs.

What Savings Can You Actually Expect

Real Numbers from Real Customers

Bundling discounts in Utah range from 5% to 30% depending on your insurer, but the actual number that matters is what you personally save on your annual premiums. State Farm bundling customers can save up to $1,429 annually when bundling auto and home insurance. Allstate offers up to 25% off bundled policies, while Progressive typically delivers around 7% savings with some customers seeing discounts exceed 25%. Liberty Mutual reports new customers who switch and bundle save approximately $950 per year on average. These aren’t theoretical numbers-they come from actual customers bundling their policies.

Your specific savings depend entirely on your current premiums, coverage limits, deductibles, and location within Utah. A homeowner paying $1,200 annually for auto insurance and $900 for homeowners coverage has a completely different savings opportunity than someone paying $2,000 for auto and $1,500 for homeowners. This is why running the actual math matters more than chasing advertised discount percentages.

Calculate Your Personal Savings

Start by requesting bundled quotes from at least three insurers and comparing the total annual cost against what you currently pay for separate policies with identical coverage. If your current auto policy costs $1,200 and home policy costs $900 for a $2,100 annual total, and a bundled quote comes in at $1,750, you’ve identified a real $350 annual savings. That’s concrete money you can calculate and verify before committing to any switch.

Uncover Hidden Savings Beyond the Discount

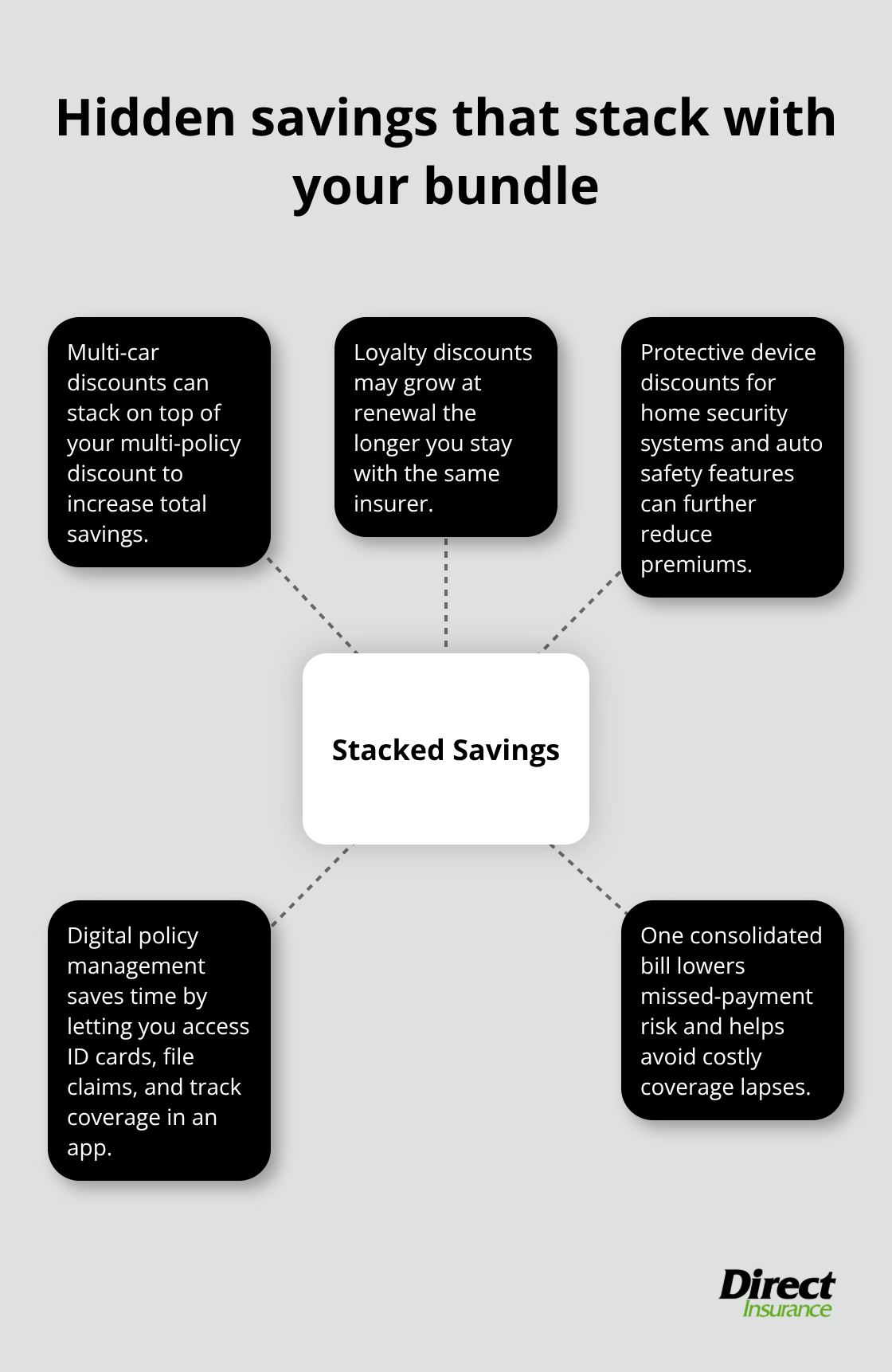

Beyond the price discount itself, bundling delivers secondary savings that often get overlooked. One consolidated bill eliminates the administrative burden of tracking multiple renewal dates and payment deadlines, reducing the risk of accidentally lapsed coverage that could cost thousands in uninsured claims. Digital policy management through mobile apps from most major insurers lets you access ID cards, file claims, and track coverage without calling an agent, saving time on routine tasks.

If you have multiple vehicles, many insurers layer additional discounts-Liberty Mutual applies a multi-car discount on top of the multi-policy discount, compounding your total savings. Loyalty discounts often apply to bundled customers, meaning the longer you stay with an insurer, the more your bundled rate decreases at renewal. Some insurers also offer protective device discounts for home security systems or auto safety features, which stack on top of your bundle discount.

Your true savings isn’t just the headline multi-policy percentage-it’s the combination of that discount plus any additional discounts your specific situation qualifies for, plus the operational efficiency of managing one policy instead of two. This layering effect means your bundled rate can improve significantly over time as you accumulate loyalty discounts and qualify for additional savings opportunities. Once you understand what you can save, the next step involves selecting the right bundle that actually covers your home and vehicle the way you need it to.

Choosing the Right Bundle for Your Needs

Know Your Current Coverage Before You Compare

Most people request bundled quotes without first understanding what they currently have, which leads to accidentally reducing coverage while chasing a lower rate. Pull your existing auto and homeowners policies and note your liability limits, deductibles, comprehensive and collision coverage amounts, and any endorsements like water backup or roof replacement coverage on your home policy. This baseline becomes your comparison standard. When you request bundled quotes from at least three insurers, ask each one to match your existing coverage exactly in both the bundled quote and a separate-policy quote. This apples-to-apples comparison reveals whether the bundle actually saves money or just appears cheaper because it strips coverage. Many bundled quotes come back lower because they reduce liability limits from 300/100/25 to 250/50/25 or remove water backup endorsements that cost $15 monthly but protect against thousands in damage. Your mortgage lender requires specific homeowners coverage limits, so reducing those limits to chase a lower rate creates a compliance problem you’ll discover when you try to close on a refinance or when your lender audits your policy during renewal.

Compare Rates from Multiple Utah Insurers

Progressive, State Farm, Allstate, Farmers, and Nationwide all operate statewide and offer bundled discounts, but their rates vary dramatically based on your driving record, home age, and location within Utah. A driver with one speeding ticket might find Progressive 15% cheaper than State Farm, while another driver with a clean record sees the opposite. Request quotes from at least three different carriers and compare the total bundled annual premium side by side with identical coverage limits. Don’t rely on national averages because those numbers reflect customers across all fifty states with completely different risk profiles than yours. Your actual savings in Utah depends entirely on your premiums in this market.

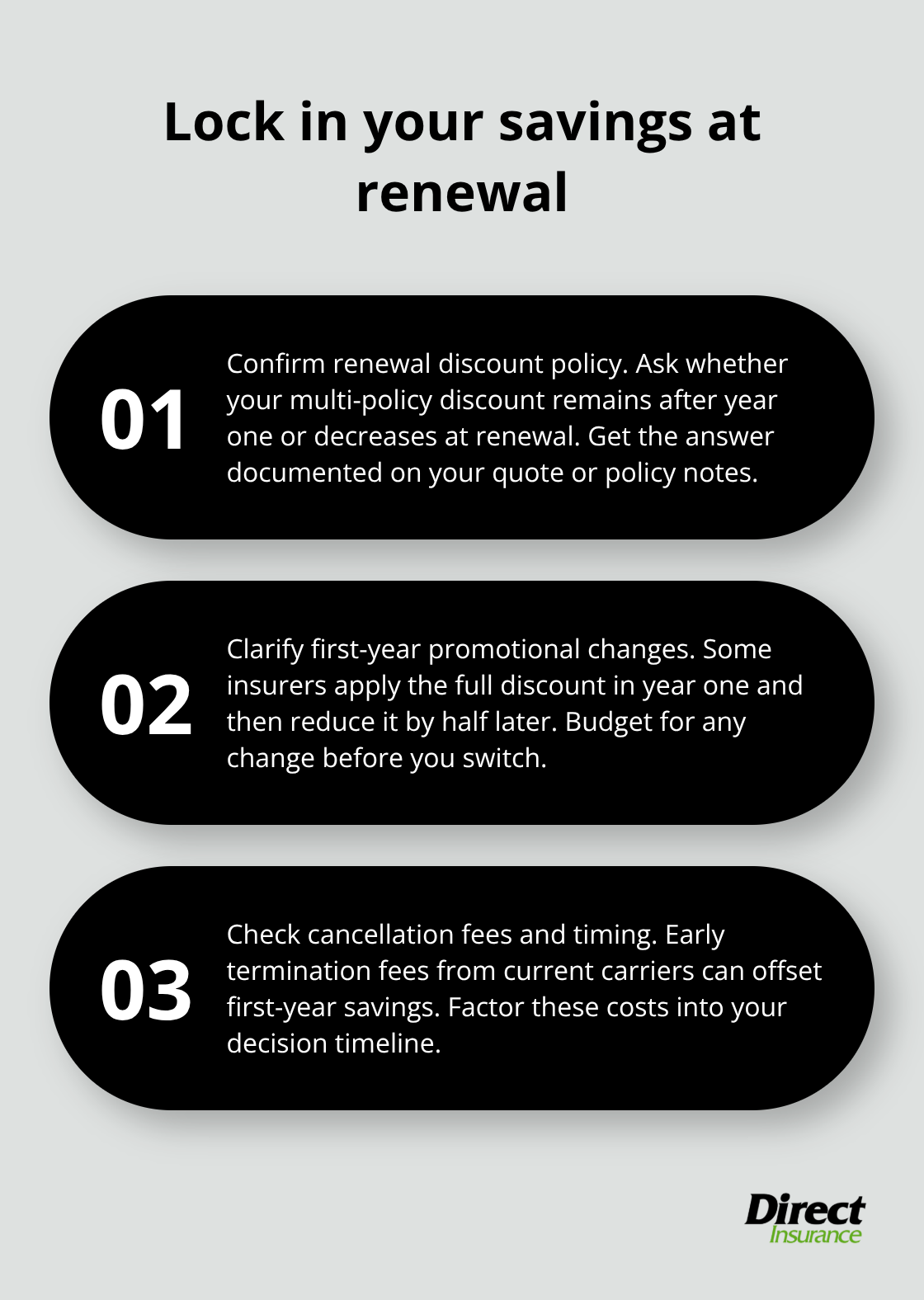

Verify Discount Stability and Hidden Fees

Once you’ve identified which insurer offers the lowest total bundled cost with matching coverage, verify that the discount doesn’t disappear at renewal. Ask the agent what happens to your multi-policy discount after year one, since some insurers apply the full discount only in the first year, then reduce it by half at renewal. Finally, confirm that canceling your current policies won’t trigger early termination fees that eat into your first-year savings. These hidden costs can eliminate your first-year savings entirely if you don’t ask about them upfront.

Final Thoughts

Bundling your home and car insurance delivers real savings that compound over time. Multi-policy discounts range from 5% to 30%, and customers who switch and bundle save hundreds annually-State Farm customers save around $1,356 per year, while Liberty Mutual reports new bundled customers save approximately $950 on average. Loyalty discounts accumulate at renewal, meaning your bundled rate improves the longer you stay with an insurer, and if you have multiple vehicles, additional discounts layer on top of your multi-policy savings.

Your next step requires requesting bundled quotes from at least three insurers and comparing total annual premiums with identical coverage limits. Run the actual math against your current separate policies rather than assuming the lowest quote saves money, and verify that the discount remains stable at renewal without early termination fees that eliminate your first-year savings. One consolidated bill eliminates missed payment risks that could trigger coverage lapses costing thousands in uninsured claims, while digital policy management through mobile apps saves time on routine tasks like accessing ID cards or filing claims.

Contact Direct Insurance Services to start your home and car insurance bundles quote today. Our local team understands Utah’s unique risks and shops multiple top-rated insurance companies to find you the best coverage at competitive rates. Discover how much you can save with a bundled policy tailored to your budget and needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation