How to Find Low Cost Home Insurance That Works

Home insurance doesn’t have to drain your budget. At Direct Insurance Services, we know that finding low cost home insurance requires understanding what drives your rates and where you can cut corners without sacrificing protection.

The difference between paying too much and getting a fair deal often comes down to a few smart decisions. This guide walks you through the factors that impact your premiums, proven strategies to lower them, and the mistakes that quietly push costs up.

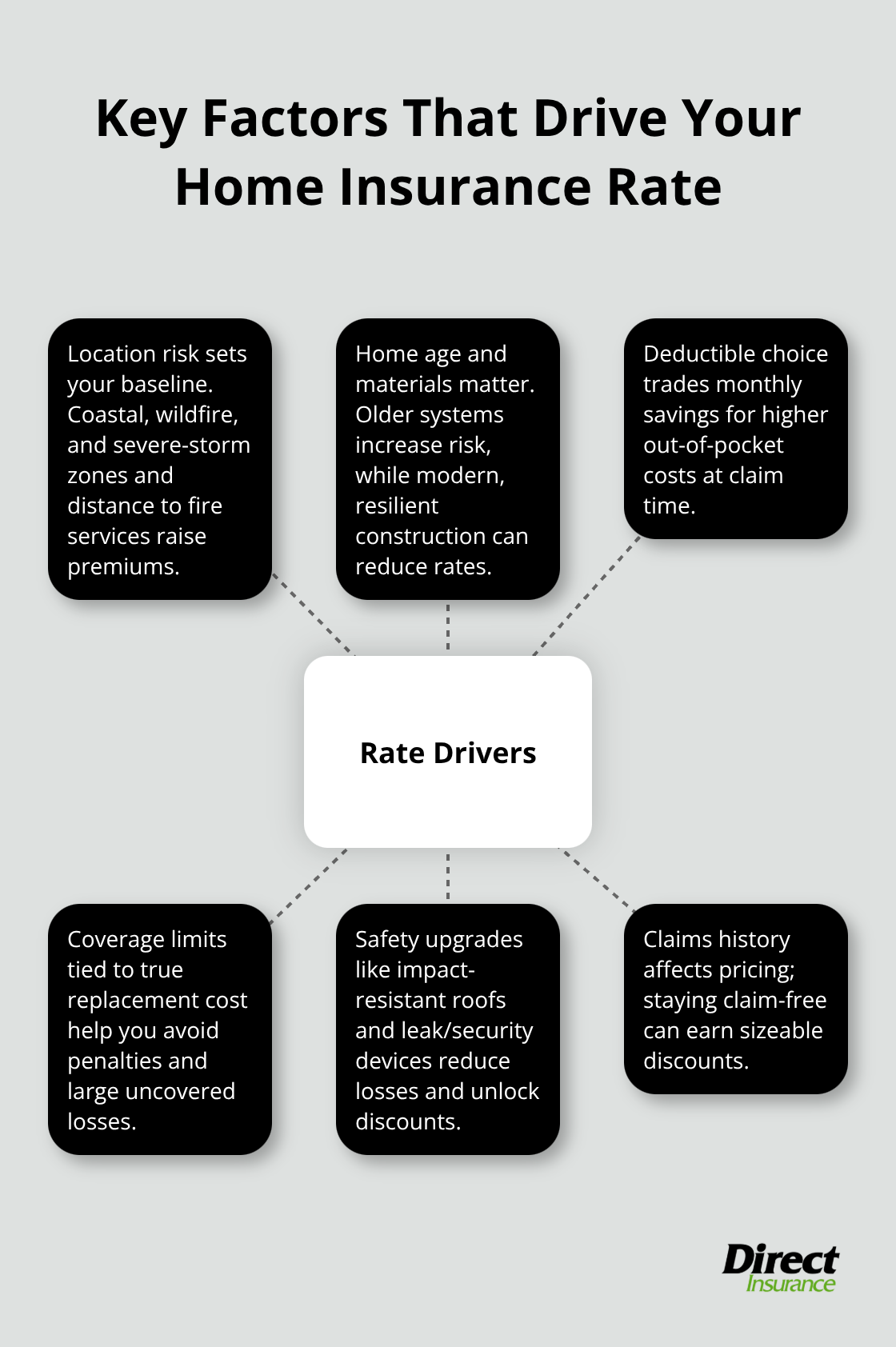

What Actually Drives Your Home Insurance Rates

Your location is the single biggest factor determining what you pay for home insurance, and it’s not something you can change. If you live in Oklahoma, you’re paying roughly nine times more than someone in Hawaii according to 2025 data from Quadrant Information Services. States like Florida and Louisiana carry premiums that reflect hurricane wind risk, while coastal areas and wildfire zones push rates even higher. Within your state, ZIP code matters enormously. A home in a rural area with volunteer fire services costs more than an identical home near a professional fire department. Crime rates in your neighborhood, distance from the coast, and local disaster frequency all factor into your quote.

Home Age and Construction Materials

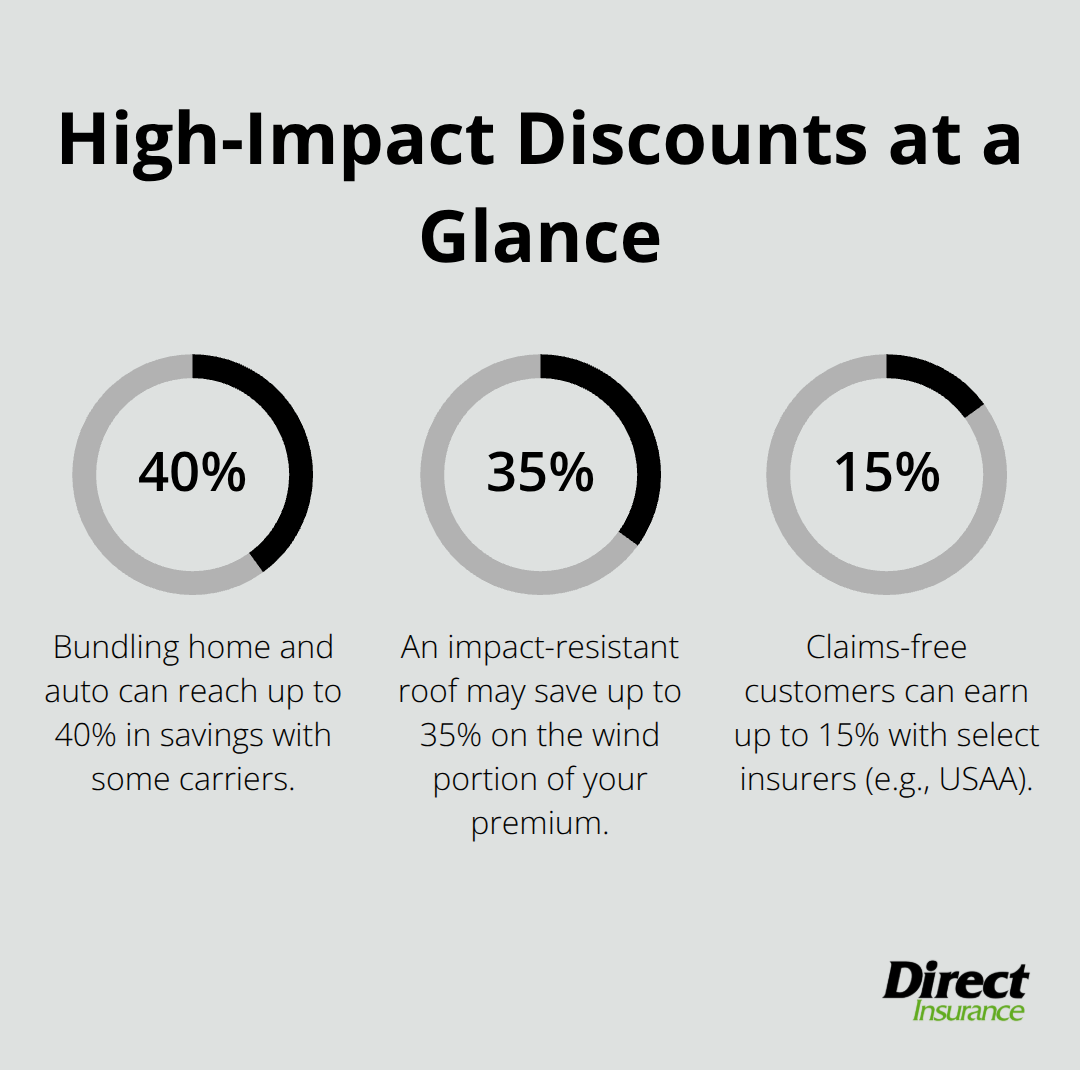

Older homes cost significantly more to insure because rebuilding them requires more expense and carries greater unpredictability. A 1970s home with outdated wiring, plumbing, or roofing presents higher risk to insurers. However, this is where you gain real leverage. An impact-resistant roof can qualify you for discounts of 20% to 35% off the wind portion of your insurance. Updating your HVAC system, electrical wiring, or plumbing makes your home safer and directly reduces what you pay. Homes built with modern materials like reinforced concrete or impact-resistant glass qualify for bigger discounts than older wood-frame construction. If you’ve recently completed upgrades, contact your insurer immediately. Many carriers don’t automatically apply these discounts unless you request them and provide proof of the work. The material your home is made from also matters; brick and stone homes typically cost less to insure than wood-frame homes because they’re more fire-resistant.

How Your Deductible and Coverage Choices Impact Price

The deductible you choose directly controls your monthly payment. Moving from a $500 deductible to $1,000 reduces your premium by a double-digit percentage, according to the Insurance Information Institute. Higher deductibles like $5,000 can produce substantial savings, though you must realistically be able to cover that amount if you file a claim. The coverage limits you select matter equally. Many homeowners make the mistake of underinsuring by assuming their home’s market value equals replacement cost. Building costs including labor and materials rose roughly 40% from 2019 to 2024 according to the Bureau of Labor Statistics. Your home might be worth $400,000 but cost $550,000 to rebuild. The 80% rule states you should insure your home for at least 80% of its replacement cost to avoid sharing uncovered costs in a claim.

Getting Your Replacement Cost Right

Accurate replacement cost assessment prevents you from paying too much for coverage you don’t need and too little for protection that leaves you exposed. Many lenders require 80% of replacement value as a minimum, so verify this with your mortgage company. You should also consider “loss of use” coverage, which pays for living costs during rebuilding if your home becomes uninhabitable. This protection matters more than most homeowners realize, especially in states with high construction costs. The difference between underinsuring and proper coverage can mean thousands of dollars out of your pocket after a disaster. Your next step involves understanding which strategies actually lower your rates without cutting corners on the protection you need.

How to Cut Your Premiums Without Sacrificing Protection

Bundle Your Home and Auto Policies Together

Bundling your home and auto policies together produces the fastest rate reduction available. Most carriers offer discounts when you combine policies, with some reaching up to 40%. Frankenmuth Insurance customers in the 2025 data showed approximately $70 per month in bundle savings alone. State Farm and USAA both reward bundling heavily, and the savings stack on top of other discounts you qualify for.

Most homeowners shop for home insurance in isolation, which costs them money. You should always request quotes for both home and auto together, then compare the bundled total across at least three carriers. A $20 monthly difference on home insurance alone becomes meaningless if your bundled rate elsewhere costs $100 less overall.

Install Security Systems and Safety Devices

Security systems and water leak detection devices lower your risk profile in an insurer’s eyes. The Insurance Information Institute reports that security systems and cameras save 2% to 6% on premiums, while water and gas leak detectors provide similar reductions. These aren’t theoretical savings-insurers price them in because claims data shows homes with these devices file fewer losses.

An impact-resistant roof or new HVAC system qualifies for even steeper discounts. Contact your insurer after any home upgrade and provide documentation of the work. Many carriers don’t automatically apply these discounts, and you lose money every month you don’t request them.

Maintain a Clean Claims Record

A clean claims record holds real monetary value. USAA offers up to 15% savings for customers with no claims in the past five years according to 2025 data. This means staying claim-free for five years on a $2,400 annual premium saves roughly $360 per year-$1,800 over five years.

This doesn’t mean you should never file a claim when you need one. Filing a claim for a $2,000 water damage loss might trigger a rate increase that costs you $500 to $1,000 over the next three to five years. The math only works in your favor for major losses. Small repairs often cost less out of pocket than the premium increases that follow a claim.

Shop Around Before Your Policy Renews

Armed Forces Insurance and State Farm lead the 2025 market at approximately $2,184 and $2,362 per year respectively, but pricing varies dramatically by ZIP code, credit score, and home characteristics. Getting quotes from at least three providers takes 20 minutes online and can reveal $500+ annual differences.

The Insurance Information Institute confirms that shopping early before your policy start date (typically 7 to 10 days ahead) qualifies you for early-bird discounts when switching carriers. Most homeowners renew with their current insurer out of inertia. This costs thousands over a decade. Your next step involves identifying which common mistakes quietly push your costs higher and how to avoid them.

Common Mistakes That Drive Up Home Insurance Costs

Underinsuring Your Home Creates Hidden Financial Risk

Most homeowners sabotage their own insurance costs through three preventable errors that compound over years. The first mistake is underinsuring your home, which creates a false sense of savings until disaster strikes. You select a $300,000 dwelling limit when your home actually requires $450,000 to rebuild. Building costs including labor and materials rose roughly 40% from 2019 to 2024, making replacement cost calculations harder than ever.

When you underinsure, insurers apply the 80% rule during claims, meaning you share the cost of damages above your coverage limit. A $100,000 gap between your limit and actual replacement cost becomes your financial responsibility after a total loss. This mistake costs some homeowners tens of thousands of dollars. Get a professional replacement cost assessment from your insurer or a local contractor before selecting coverage limits. Contact your mortgage lender to confirm their minimum requirement, then add 10% to 15% above that threshold to account for inflation between now and when you might file a claim.

Ignoring Annual Rate Reviews Costs Hundreds Every Year

The second mistake is ignoring your annual rate review, which lets your premiums climb without resistance. Homeowners typically renew with their current carrier out of habit, losing hundreds annually to rate creep. Armed Forces Insurance and State Farm averaged $2,184 and $2,362 per year in 2025 data, yet premiums vary enormously by ZIP code and individual risk factors.

Getting quotes from three carriers before your renewal date takes roughly 20 minutes and frequently reveals $500 to $1,000 annual differences. Most homeowners never perform this simple task, which costs them thousands over a decade. The savings compound when you switch carriers every few years to lock in competitive rates.

Failing to Request Available Discounts Leaves Money on the Table

The third mistake is failing to ask about available discounts after home improvements or life changes. You install a new roof qualifying you for a 20% to 35% discount on wind coverage, but your insurer doesn’t automatically apply it. You improve your credit score or complete five years without claims, yet your premium stays unchanged.

Contact your agent annually and specifically ask about discounts for security systems, updated electrical wiring, new HVAC systems, no-claim history, bundling, early-bird policy switches, and any other programs your carrier offers. These three mistakes cost homeowners thousands over a decade. The solution requires 30 minutes annually to review rates, confirm your coverage matches replacement cost, and request available discounts.

Final Thoughts

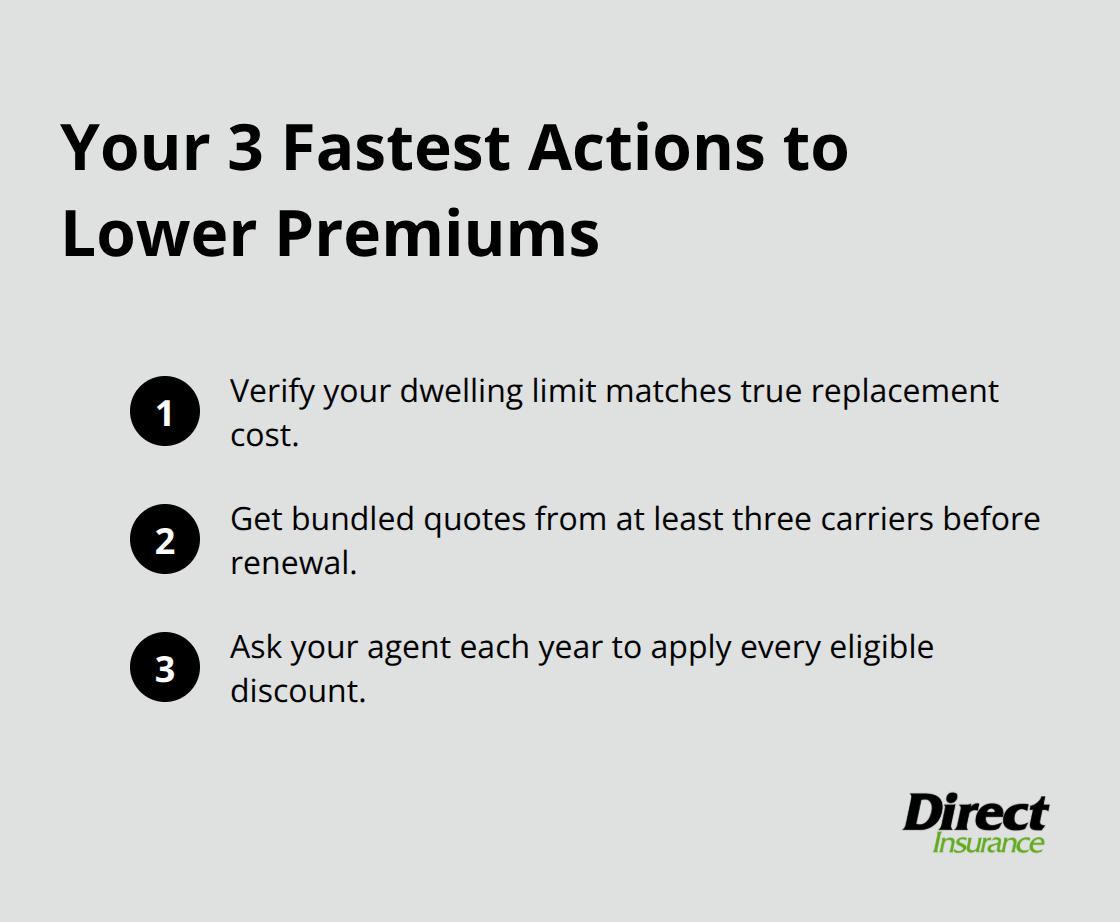

Finding low cost home insurance requires three concrete actions you can take immediately. First, verify your replacement cost matches what your home actually costs to rebuild, not its market value. Second, obtain quotes from at least three carriers before your renewal date and compare bundled rates for home and auto together. Third, contact your agent annually to request discounts for security systems, roof upgrades, claims-free history, and any other improvements you’ve made.

The difference between overpaying and getting fair coverage often amounts to hundreds of dollars per year. Armed Forces Insurance and State Farm averaged $2,184 and $2,362 annually in 2025, yet your actual rate depends entirely on your location, home age, and the choices you make about deductibles and coverage limits. Shopping around reveals these differences, bundling saves 10% to 30% on premiums, and maintaining a clean claims record qualifies you for discounts worth thousands over five years.

We at Direct Insurance Services understand that finding the right coverage at the right price matters. Our team can help you navigate the choices that actually lower your premiums and get quotes for low cost home insurance that protects what matters most. Contact us today to discover how we can help you save.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation