How to Find Affordable Auto Insurance for Teens

Teen drivers face insurance premiums that are often two to three times higher than adult drivers. This reality puts pressure on families already managing tight budgets.

At Direct Insurance Services, we know that affordability doesn’t mean sacrificing protection. This guide walks you through concrete strategies to lower auto insurance for teens while keeping coverage strong.

Why Teen Auto Insurance Costs More

Teen drivers represent a significantly higher risk for insurance companies, and the numbers prove it. According to data from The Zebra, teen drivers aged 16–19 crash at rates roughly four times higher than drivers aged 20 and older. This isn’t a minor statistical difference-it directly translates to real claims and real payouts that insurers must cover.

How Accident Risk Drives Premium Costs

Insurance companies price premiums based on risk, and teens simply generate more accidents. A 16-year-old pays approximately $5,744 per year on average, while that same driver at age 20 pays around $2,780-a drop of nearly 52 percent. The decline continues into the mid-20s as driving history accumulates and accident risk diminishes.

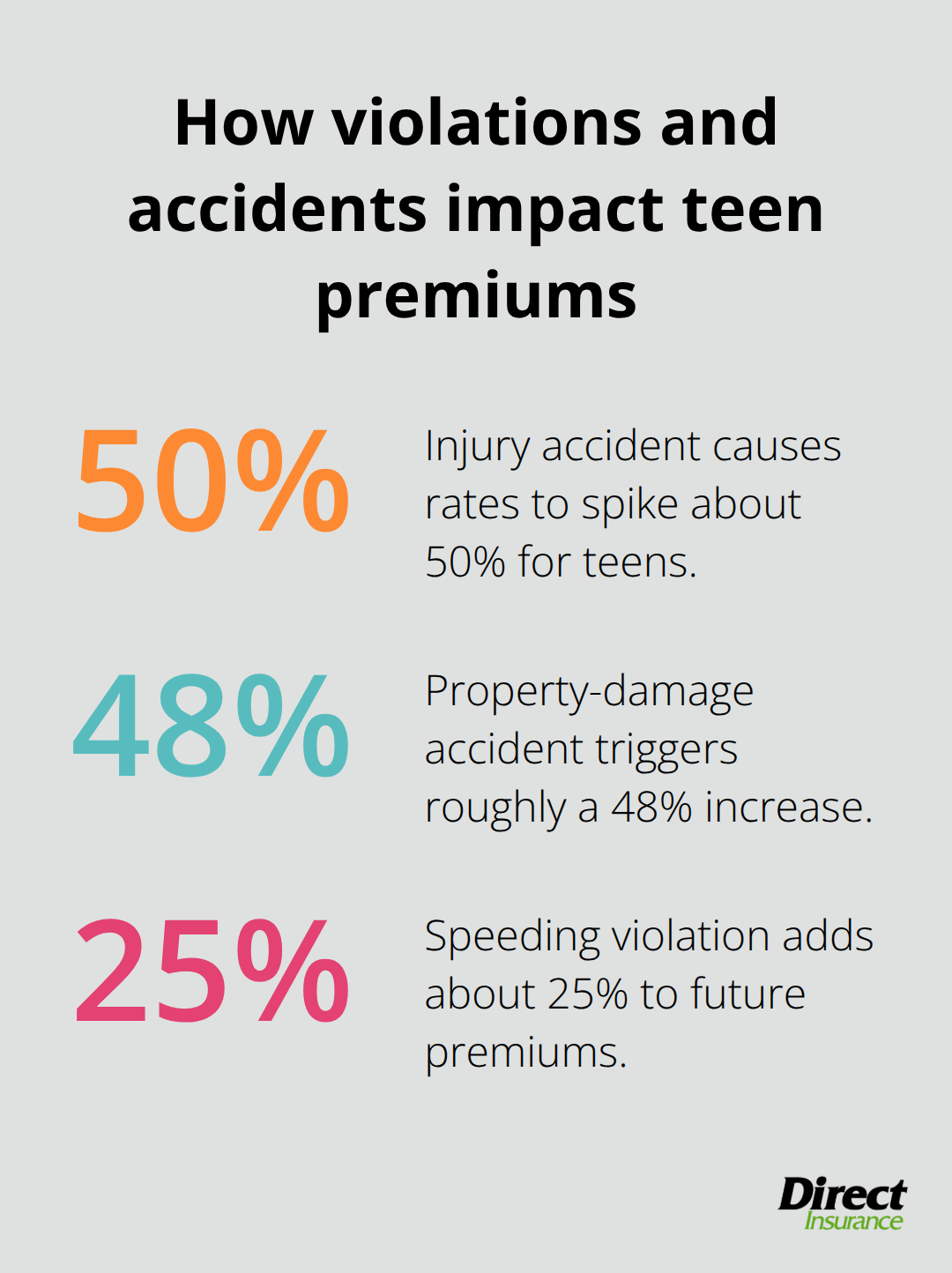

Beyond raw accident frequency, insurers factor in accident severity. When a teen causes an accident with injuries, rates typically spike about 50 percent according to Forbes Advisor data. Property-damage accidents alone trigger roughly a 48 percent increase. Speeding violations add about 25 percent to future premiums.

These penalties reflect the actual cost of claims that insurers pay out.

The Impact of Limited Driving History

Insurance companies scrutinize driving history length carefully. A teen with a license for three months has virtually no track record to evaluate, forcing insurers to apply broad risk assumptions rather than individual performance data. This absence of history proves expensive because insurers cannot differentiate between safe and reckless teen drivers.

How Insurers Calculate Teen Premiums

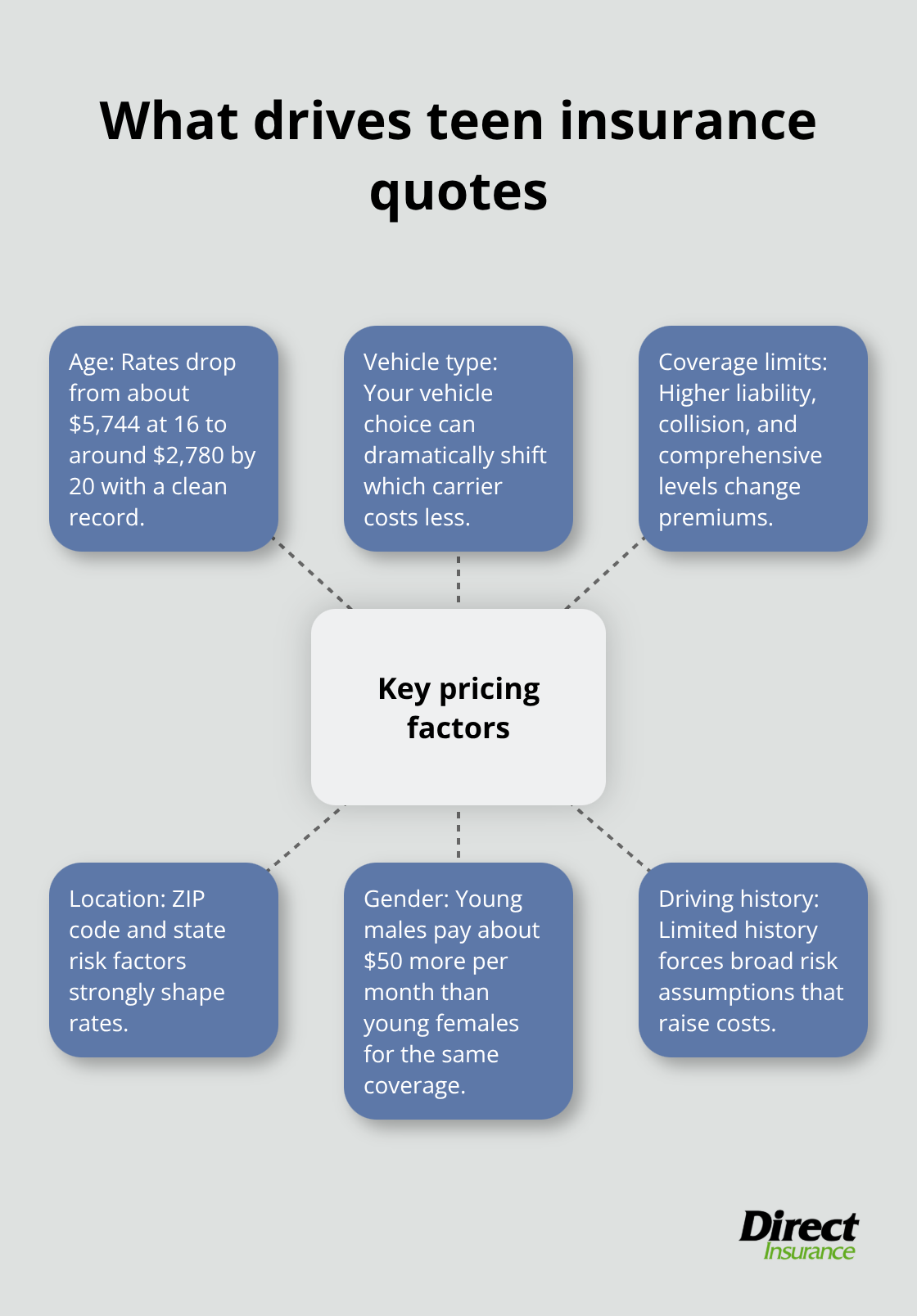

Insurers use sophisticated models that combine age, vehicle type, coverage limits, and location to calculate premiums. A 16-year-old on their own policy averages around $8,608 annually, compared to roughly $2,408 more per year when added to a parent’s policy, according to Forbes Advisor. The difference reflects how insurers view shared household policies-adding a teen to an existing adult policy distributes risk differently than insuring a teen independently.

Geographic and Demographic Factors

Geography amplifies these costs significantly. States like Louisiana, Texas, and Arizona consistently show higher teen insurance rates due to accident frequency, road infrastructure, and local driving patterns. Conversely, North Dakota ranks as the cheapest state for teen drivers, with costs around $1,421 per year to add a teen to a parent’s policy.

Gender also matters. Young male drivers pay approximately $50 more per month than young female drivers for the same coverage, reflecting historical claim data showing higher accident and violation rates among teenage males. These aren’t arbitrary numbers-they’re built on decades of claims data that reveal which drivers cost insurers the most money.

Understanding why teen insurance costs so much helps you identify which factors you can actually control. The next section explores concrete strategies that reduce premiums without leaving your teen underprotected.

Practical Discounts That Actually Cut Your Teen’s Premium

The gap between what families pay and what they could pay for teen auto insurance often comes down to discounts most people overlook. Families miss thousands in savings simply because they don’t know which discounts apply to their situation or how to stack them effectively.

Good Student Discounts and Safety Course Savings

A good student discount can lead to savings of $186 per year on car insurance when coupled with a good driver discount. To qualify, your teen needs to maintain at least a 3.0 GPA and provide transcripts twice yearly. Some insurers accept Dean’s List placement or top 20% class ranking as alternatives. Ask your insurer exactly which documentation they need before your teen’s grades arrive.

Driver safety courses offer another concrete reduction, typically worth 5 to 10 percent depending on your insurer. These programs work because completion data shows course-takers have fewer accidents. Your teen completes an approved defensive driving program, you submit proof, and the discount applies to the next renewal cycle.

Bundling Policies Generates Immediate Savings

Combining your teen’s auto policy with your home or renters insurance generates immediate savings around $460 annually for teens according to The Zebra’s research. Homeowners bundles typically yield about 10 percent off, while renters bundles save around 5.3 percent. Many families insure teens separately without checking what bundling could accomplish.

Deductible Adjustments Reduce Monthly Costs

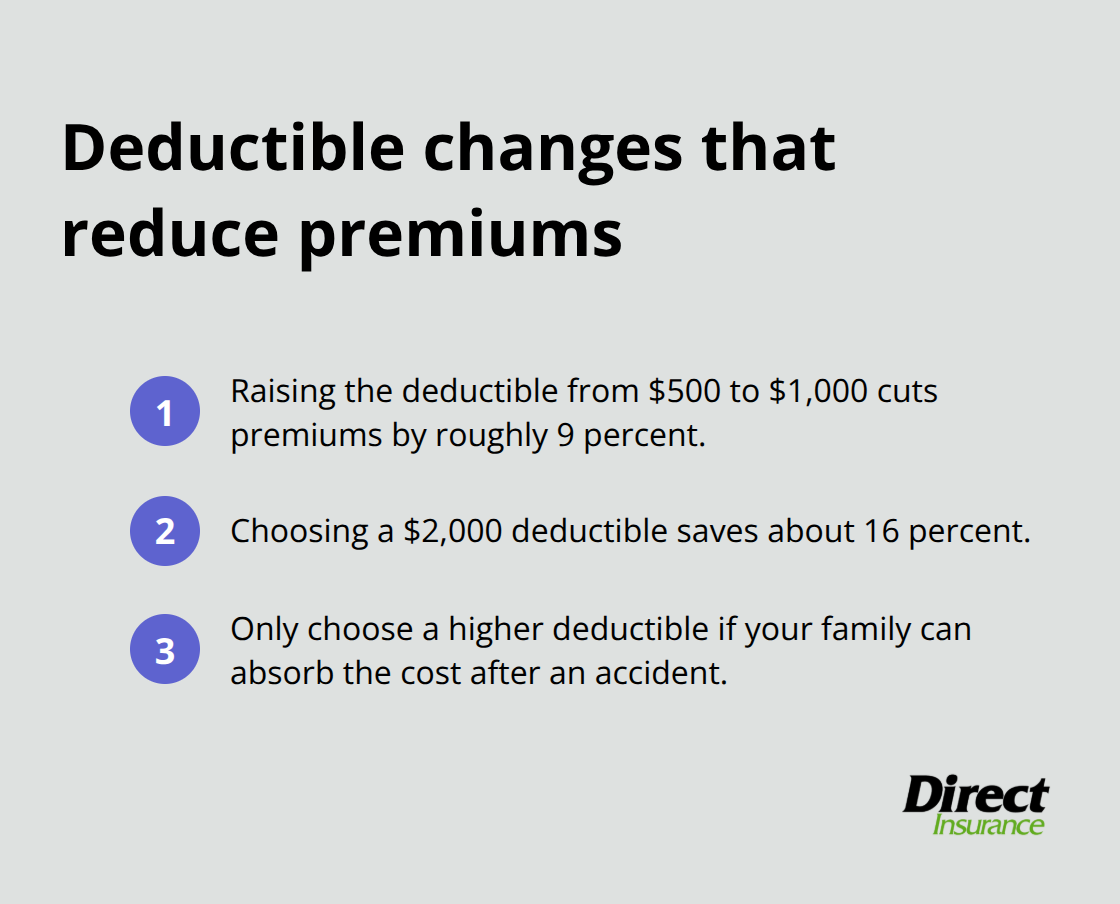

Adjusting deductibles represents a leverage point that actually works. Increasing your deductible from $500 to $1,000 cuts premiums by roughly 9 percent, while jumping to $2,000 saves about 16 percent-potentially $517 to $919 annually depending on your state. This strategy only makes sense if your family can absorb a higher deductible after an accident, but for families with emergency savings, it’s one of the fastest ways to reduce monthly costs.

Usage-Based Insurance Programs Build Better Rates Over Time

Usage-based insurance programs operate differently from traditional discounts. Programs like Steer Clear or Drive Safe and Save install a small device that monitors your teen’s actual driving behavior-speed, braking, time of day behind the wheel. Insurers then adjust rates based on performance data rather than age assumptions. The average savings hovers around $172 yearly according to The Zebra, but some states like Connecticut see higher reductions.

Safe teen drivers can lock in lower rates as their driving record builds, whereas traditional policies automatically increase rates after any accident regardless of circumstances. This performance-based approach rewards actual safe driving rather than penalizing all teens equally. Once you’ve identified which discounts apply to your teen’s situation, the next step involves comparing how different insurers actually price these discounts-because the same discount can vary significantly from one company to another.

Where to Find the Lowest Teen Auto Insurance Rates

Shopping for teen auto insurance without comparing multiple quotes leaves money on the table. Families often accept the first quote they receive, assuming prices stay consistent across carriers. The reality differs sharply: the same 16-year-old driver costs $5,744 with one company and $4,200 with another, depending on how that insurer weights age, location, and available discounts. Start by gathering quotes from at least three carriers before making any decision. GEICO, Travelers, and American Family consistently rank among the cheapest options for teens according to The Zebra’s rate data, but your specific ZIP code and vehicle choice dramatically shift which carrier actually costs less. Use online quote tools to compare full-coverage policies with identical deductibles across carriers so you’re truly comparing apples to apples. Most families stop after one quote because they assume prices are similar everywhere.

That assumption costs thousands.

Coverage Levels Create Significant Financial Differences

The difference between minimum coverage and adequate coverage for a teen driver often amounts to just $100 to $150 monthly, yet the financial risk swings dramatically. Minimum liability coverage of 25/50/25 leaves your teen severely underinsured if they cause an accident. Forbes Advisor data shows that property-damage accidents alone increase future premiums by roughly 48 percent, and injury accidents spike rates about 50 percent. If your teen causes a serious accident with medical costs exceeding their liability limits, your family becomes personally liable. Try 100/300/100 liability coverage paired with collision and comprehensive protection instead. If your teen’s car is financed or leased, lenders require collision and comprehensive anyway, so this decision is already made for you. The real choice centers on deductible amounts. A $1,000 deductible saves roughly 9 percent compared to $500, while $2,000 saves about 16 percent according to The Zebra. Only choose a higher deductible if your family has emergency savings to cover it after an accident.

Renewal Dates Trigger Rate Recalculations

Insurance companies recalculate rates annually, and teen premiums drop noticeably each year if your teen maintains a clean driving record. A 16-year-old paying $5,744 yearly drops to roughly $4,876 at age 17, then $4,271 at age 18, with steeper declines continuing through age 25 according to The Zebra’s data. However, this decline only happens if you don’t lock into a bad rate early. When your teen’s policy renews, request fresh quotes from competitors before automatically accepting the renewal rate. Insurers often offer lower rates to new customers than they charge existing policyholders, so shopping around at renewal actually works in your favor. Additionally, if your teen’s situation changes during the year-they move away to college, complete a driver safety course, or improve their grades-contact your insurer immediately to update the policy. Discounts for away-at-school situations apply if your teen attends college far from home and only drives during breaks. These discounts don’t apply automatically; you must inform your insurer of qualifying changes.

Final Thoughts

Reducing auto insurance for teens requires layering multiple strategies that work together. Good student discounts, driver safety courses, bundling policies, and usage-based insurance programs each contribute meaningful savings when you stack them strategically. Shopping multiple carriers amplifies these reductions further, since the same 16-year-old driver costs thousands more with one insurer than another depending on how that company weights age, location, and available discounts.

The temptation to choose minimum coverage feels strong when monthly payments strain your budget. This approach backfires when your teen causes an accident, exposing your family to personal liability that can last years. The difference between minimum coverage and adequate protection for auto insurance for teens often costs just $100 to $150 monthly, yet the financial protection gap spans hundreds of thousands of dollars. Try liability limits of at least 100/300/100 paired with collision and comprehensive protection if your teen’s vehicle is financed or leased.

Your teen’s premiums decline naturally as they age and build a clean driving record, dropping from roughly $5,744 at age 16 to around $2,780 by age 20 if they avoid accidents and violations. Shopping around at each renewal captures rate reductions that insurers offer new customers, and updating your policy when your teen’s situation changes unlocks discounts that don’t apply automatically. Contact us to get started with a personalized quote for your teen driver.