How to Calculate Home Insurance Costs

Home insurance premiums vary wildly from one house to the next. Your location, home value, and deductible choice all play a role in what you’ll pay each month.

At Direct Insurance Services, we break down exactly how insurers calculate your rate and what you can do to lower it. This guide shows you the real factors that matter when you calculate home insurance costs.

What Drives Your Home Insurance Premium

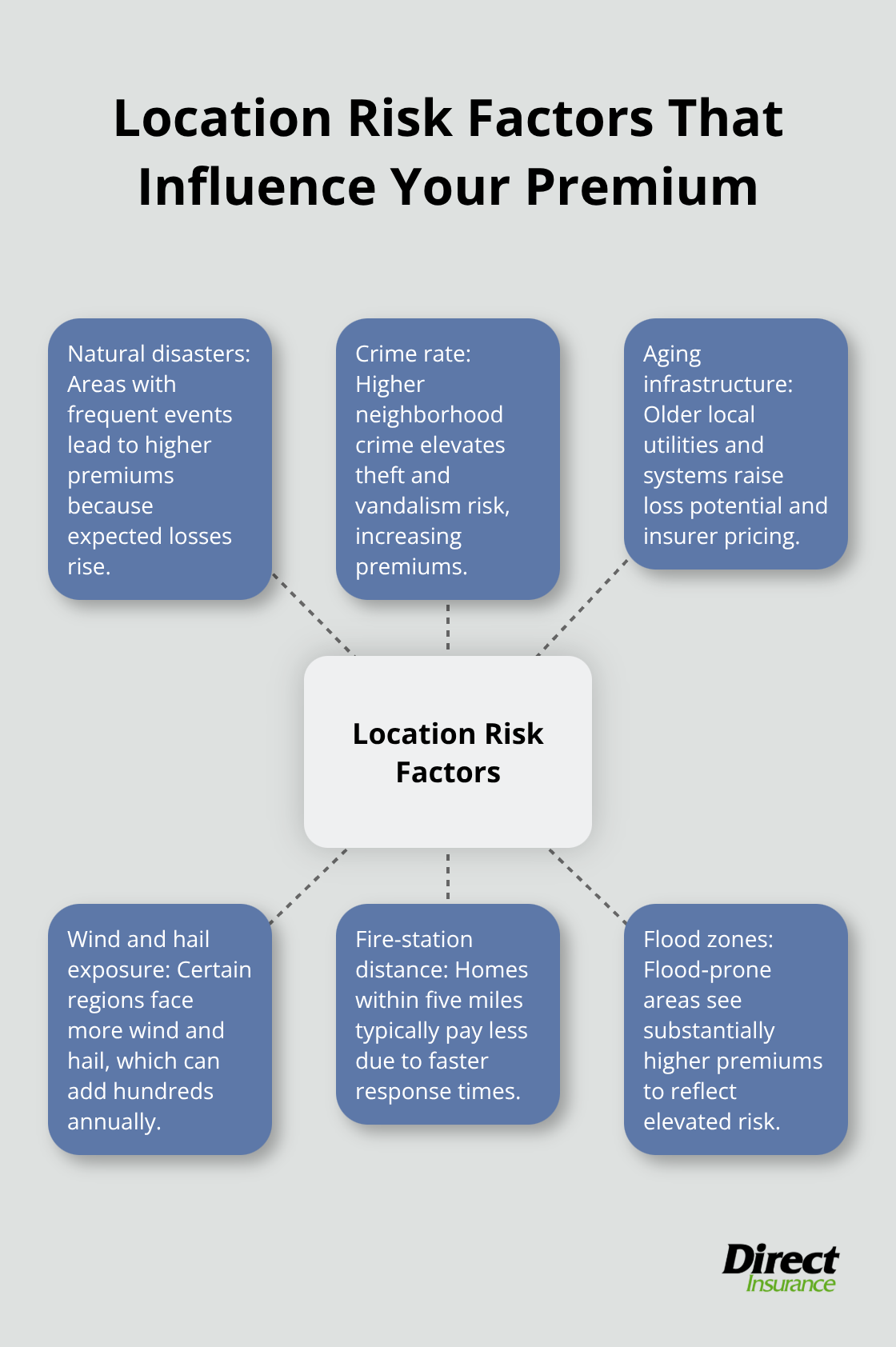

Your location matters more than most people realize. Insurers charge significantly higher premiums in areas with frequent natural disasters, high crime rates, or aging infrastructure. If you live in a flood-prone zone, your premium jumps substantially compared to someone in a low-risk area. Wind and hail exposure in certain regions can add hundreds to your annual cost.

Location and Local Risk Factors

Crime statistics for your specific neighborhood directly influence your rate, which is why two houses on the same street can have different premiums. Even the distance from a fire station affects pricing-homes within five miles of a station typically pay less because firefighters can respond faster. Your zip code tells insurers a lot about what risks you face, and they price accordingly.

How Your Home’s Characteristics Shape Cost

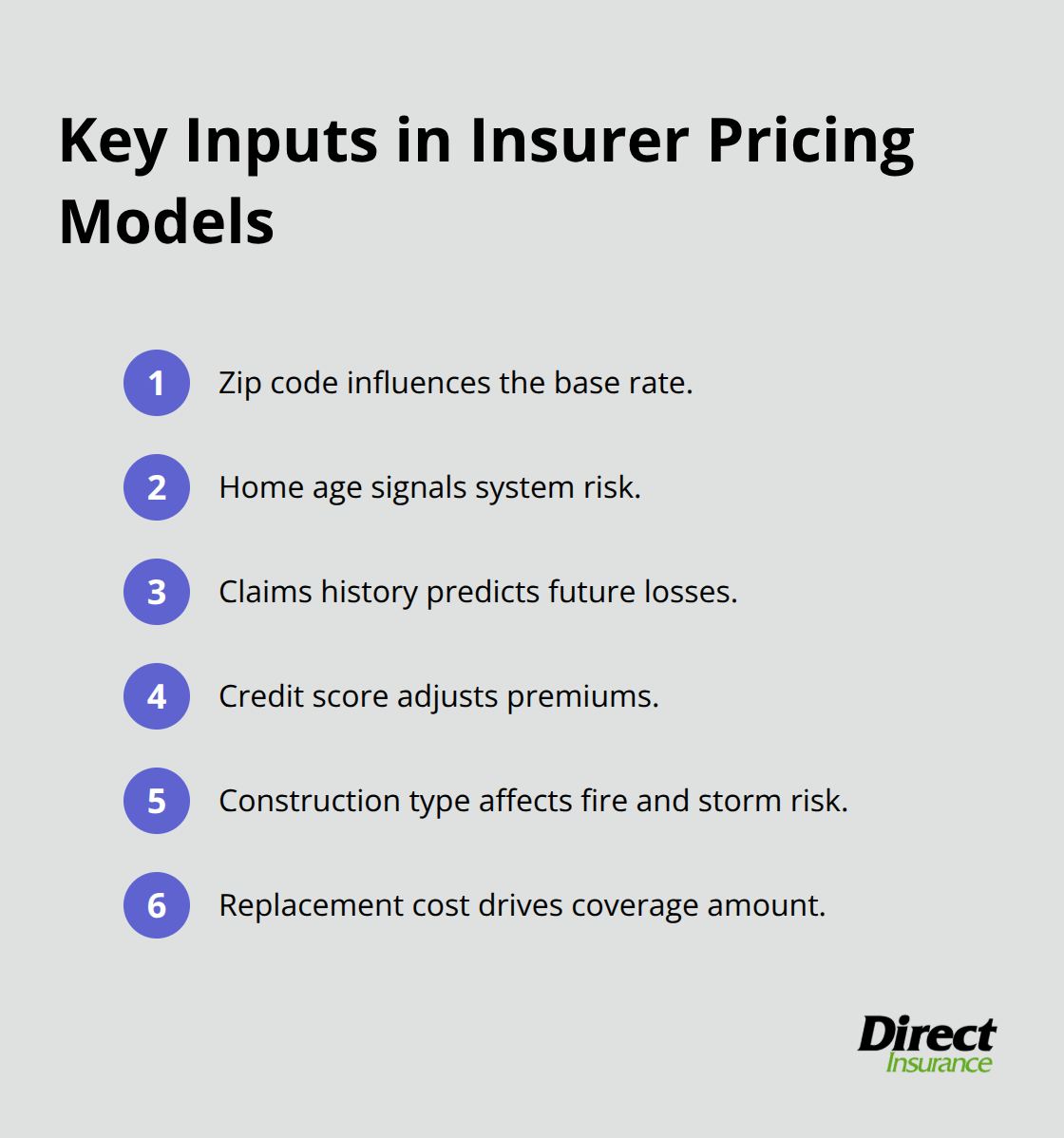

Your home’s replacement cost is the primary driver of your premium. A 2,000-square-foot house costs more to insure than a 1,200-square-foot home because rebuilding it would cost more. The age of your home significantly impacts your rate. Homes built before 1980 often face higher premiums due to outdated systems that increase risk. Newer homes with updated systems qualify for better rates.

The construction type matters too-wood-frame houses cost more to insure than brick or concrete structures because wood is more flammable. If your roof is over 20 years old, expect a rate increase or potential coverage denial until you replace it.

The Deductible Decision

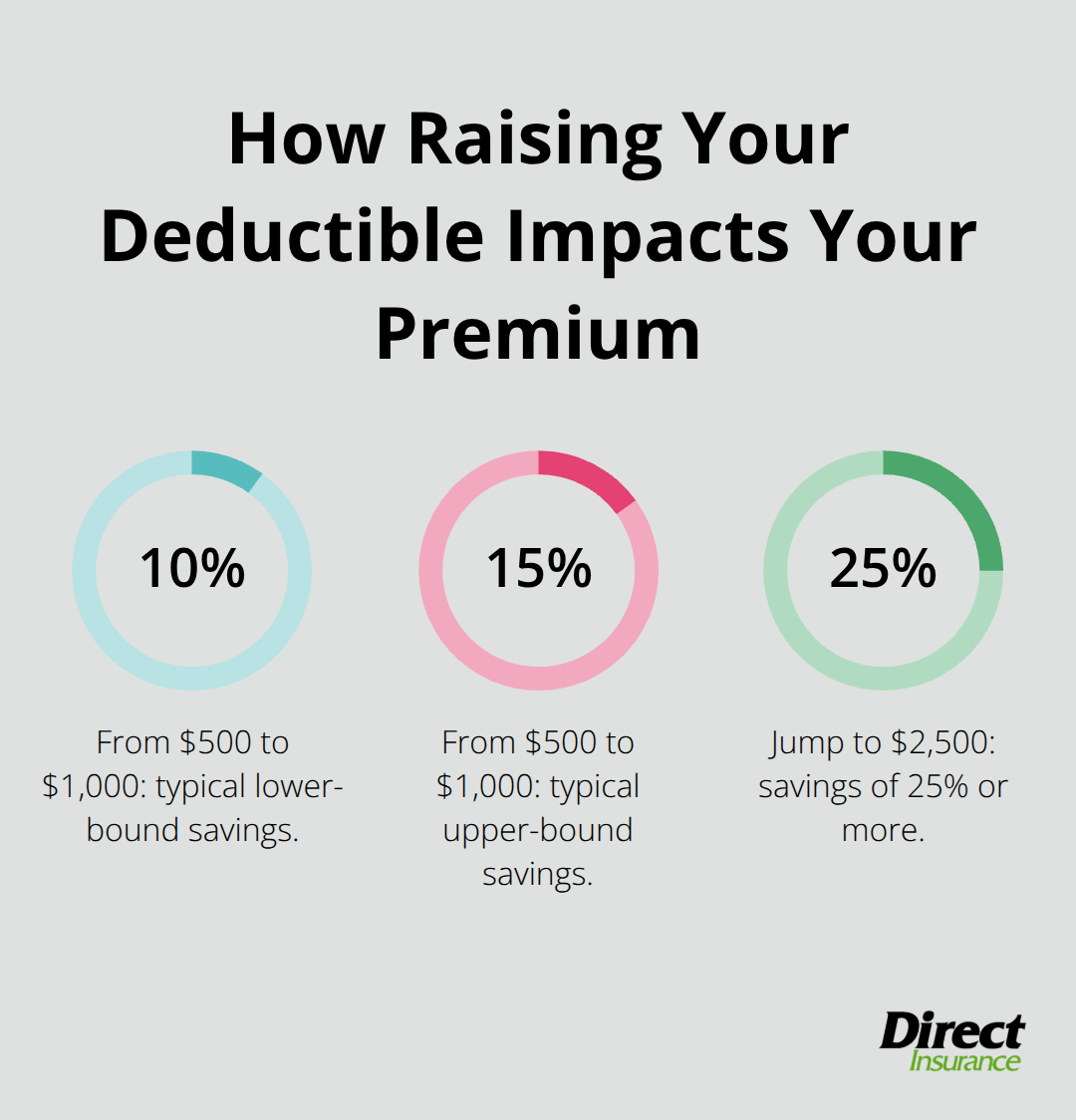

Your deductible choice directly controls what you pay monthly. Increasing your deductible from $500 to $1,000 typically reduces your premium by 10 to 15 percent. A $2,500 deductible can cut your premium by 25 percent or more. The tradeoff is clear: you save money upfront but pay more when you file a claim.

Try a deductible you can actually afford to pay out of pocket if disaster strikes. Your coverage limits also affect pricing. Higher liability limits cost more but protect your assets if someone gets injured on your property and sues you. Most insurers recommend liability coverage of at least $300,000, though wealthier homeowners often choose $500,000 or more.

Understanding these factors puts you in control of your premium. However, insurers don’t stop at these basics-they also examine your personal history and use sophisticated models to calculate your final rate.

How Insurers Price Your Coverage

Claims History Reveals Your Risk Profile

Insurance companies examine your claims history as one of the strongest predictors of future risk. Insurers assess risk based on claims history to determine your premiums. This pattern holds across the industry because insurers have decades of data showing that past claim behavior predicts future losses.

Credit Scores and Financial Responsibility

Your credit score plays a major role in your premium calculation. The National Association of Insurance Commissioners published studies showing that people with lower credit scores file more claims, so insurers use credit-based insurance scores to adjust premiums. Someone with a credit score above 750 typically pays 20 to 30 percent less than someone scoring below 600, even if they live in identical homes. This correlation isn’t about fairness-it reflects statistical reality. The way you manage debt and payment obligations tells insurers something about how you maintain your property and handle risk.

Actuarial Models and Risk Segmentation

Insurers employ actuarial analysis to calculate group risk patterns across their entire customer base. They segment customers into thousands of micro-categories based on combinations of zip code, home age, claims history, credit score, construction type, and replacement cost. A computer model then assigns a base rate for your category and applies individual adjustments. Insurance companies spend millions annually updating these models with new claims data to identify which combinations of factors predict the highest losses. Your premium reflects where you land in this statistical universe.

If you fall into a segment with consistently high claim frequency, you pay more regardless of your personal circumstances.

How You Can Shift Your Risk Category

You control several inputs that move you toward lower-risk categories. Raising your deductible, improving your credit score over time, avoiding claims when possible, and updating your home’s systems all work in your favor. Different insurers weight these factors differently, which is why comparing quotes from multiple providers matters significantly. One company might heavily penalize older roofs while another focuses more on crime statistics, meaning your rate varies substantially between carriers even though they evaluate the same property. This variation creates real opportunities to find better pricing.

Practical Ways to Cut Your Home Insurance Costs

Raise Your Deductible for Immediate Savings

The most effective way to lower your premium is raising your deductible, and the math is straightforward. Moving from a $500 deductible to $1,000 typically cuts your annual premium by 10 to 15 percent, while jumping to $2,500 can reduce it by 25 percent or more. The key is choosing a deductible amount you can actually pay without financial strain if you need to file a claim.

If you have $5,000 in emergency savings, a $2,500 deductible makes sense. If your emergency fund is smaller, stick with $1,000 to avoid creating a new problem when disaster strikes.

Bundle Home and Auto Insurance

Bundling your home and auto insurance with the same carrier can typically qualify for savings of 5% to 30% off your combined premiums, depending on your insurer. This bundling discount is real money-a household paying $1,500 annually for homeowners insurance and $1,200 for auto could save $400 to $675 per year simply by consolidating with one carrier. The savings vary by insurer, so comparing bundle quotes from multiple companies matters more than staying loyal to your current provider.

Install Security Systems and Safety Features

Home security improvements deliver measurable premium reductions. Installing a monitored burglar alarm system typically earns a 5 to 15 percent discount because it reduces theft risk and property damage claims. Deadbolts on all exterior doors, motion-sensor lighting, and security cameras also qualify for discounts with many insurers. These upgrades signal lower risk to insurers and protect your property simultaneously.

Update Your Home’s Major Systems

Upgrading your roof before it reaches 20 years old prevents rate increases and potential non-renewal. Replacing outdated electrical wiring, plumbing, or HVAC systems signals lower risk to insurers and can result in 5 to 10 percent savings. These improvements reduce the likelihood of claims and demonstrate responsible property maintenance to your carrier.

Improve Your Credit Score Over Time

Improving your credit score over time is slower but equally powerful-someone who raises their credit score from 600 to 750 can expect to pay 20 to 30 percent less for the same coverage within a few years. The way you manage debt and payment obligations tells insurers something about how you maintain your property and handle risk. This path forward requires action on multiple fronts rather than hoping for one magic fix.

Final Thoughts

Your home insurance premium reflects choices you control. Location, home value, deductible selection, claims history, credit score, and risk modeling all combine to determine what you pay each month. The most effective approach pairs immediate savings with long-term improvements-raising your deductible cuts costs quickly, bundling policies saves hundreds annually, and installing security systems qualifies for measurable discounts.

Shopping around for quotes matters more than most people realize. Different insurers weight risk factors differently, so your rate varies substantially between carriers even for identical coverage (one company might penalize older roofs heavily while another focuses on crime statistics). This variation creates real opportunities to find better pricing without sacrificing protection.

We at Direct Insurance Services help Utah residents calculate home insurance costs by shopping multiple top-rated carriers to find the best rates and coverage for your situation. Contact Direct Insurance Services to compare quotes and see how much you could save through optimizing your deductible, bundling policies, or making strategic home improvements.