Affordable Home Insurance for Every Budget

Home insurance doesn’t have to drain your budget. Many homeowners overpay simply because they haven’t compared rates or explored the discounts available to them.

At Direct Insurance Services, we’ve helped thousands of people find affordable home insurance that actually matches their needs. This guide walks you through the real strategies that lower your costs without cutting corners on protection.

What Coverage Do You Actually Need

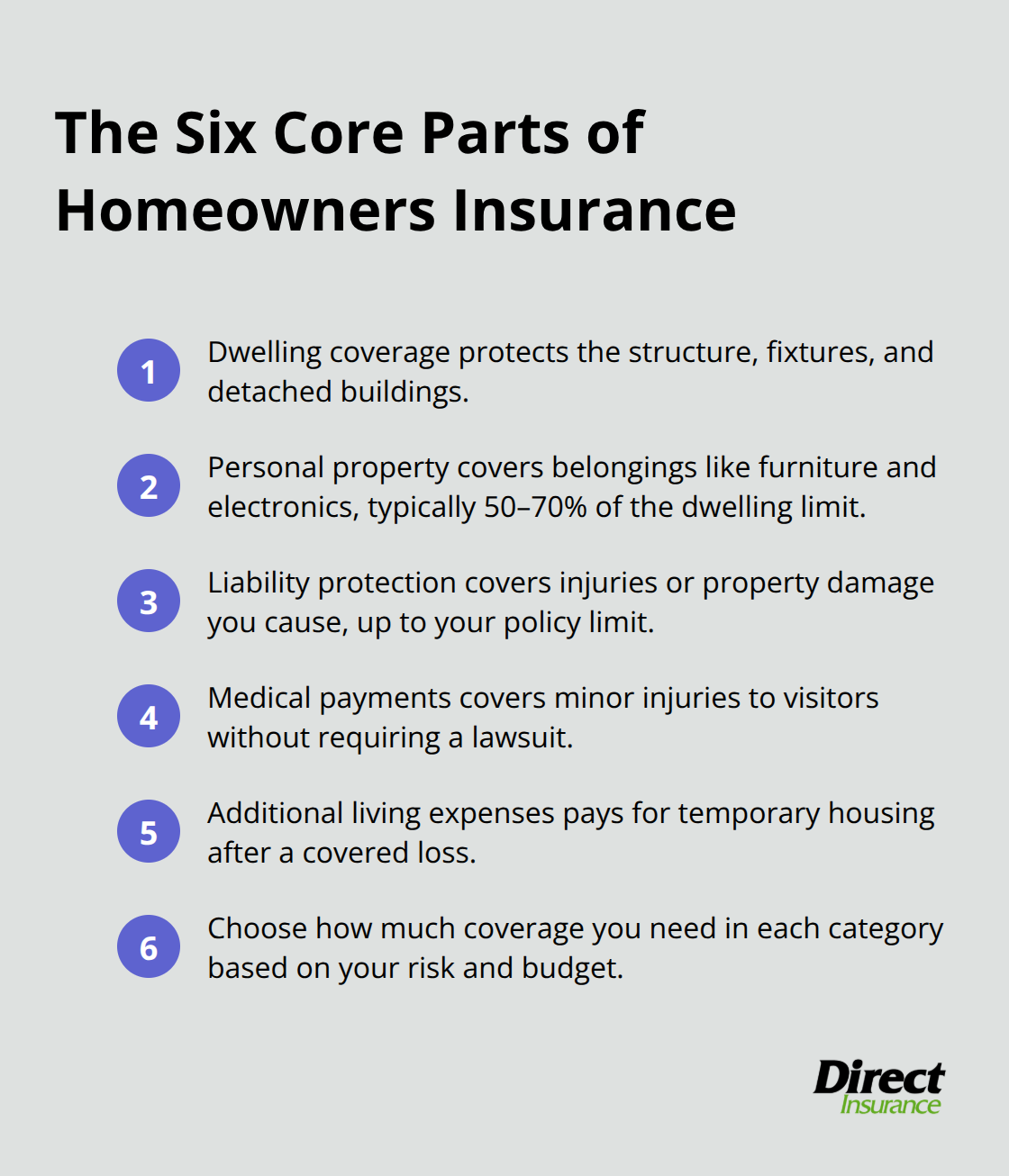

The Six Core Components of Homeowners Insurance

Standard homeowners policies contain six core components, and understanding each one matters because you pay for what you choose. Property damage coverage protects your dwelling structure, permanent fixtures, and detached buildings from fire, wind, hail, and theft. Personal property coverage reimburses you for damaged or stolen belongings like furniture, electronics, and clothing, though this typically maxes out at 50–70% of your dwelling coverage. Liability protection shields you if someone gets injured on your property or you accidentally damage their belongings, covering medical bills and legal costs up to your policy limit. Medical payments coverage handles minor injuries to visitors without requiring them to sue. Additional living expenses pay for temporary housing if your home becomes uninhabitable after a covered loss. Most homeowners need all six components, but the real question is how much coverage in each category.

The 80% Rule: Why Underinsurance Costs You

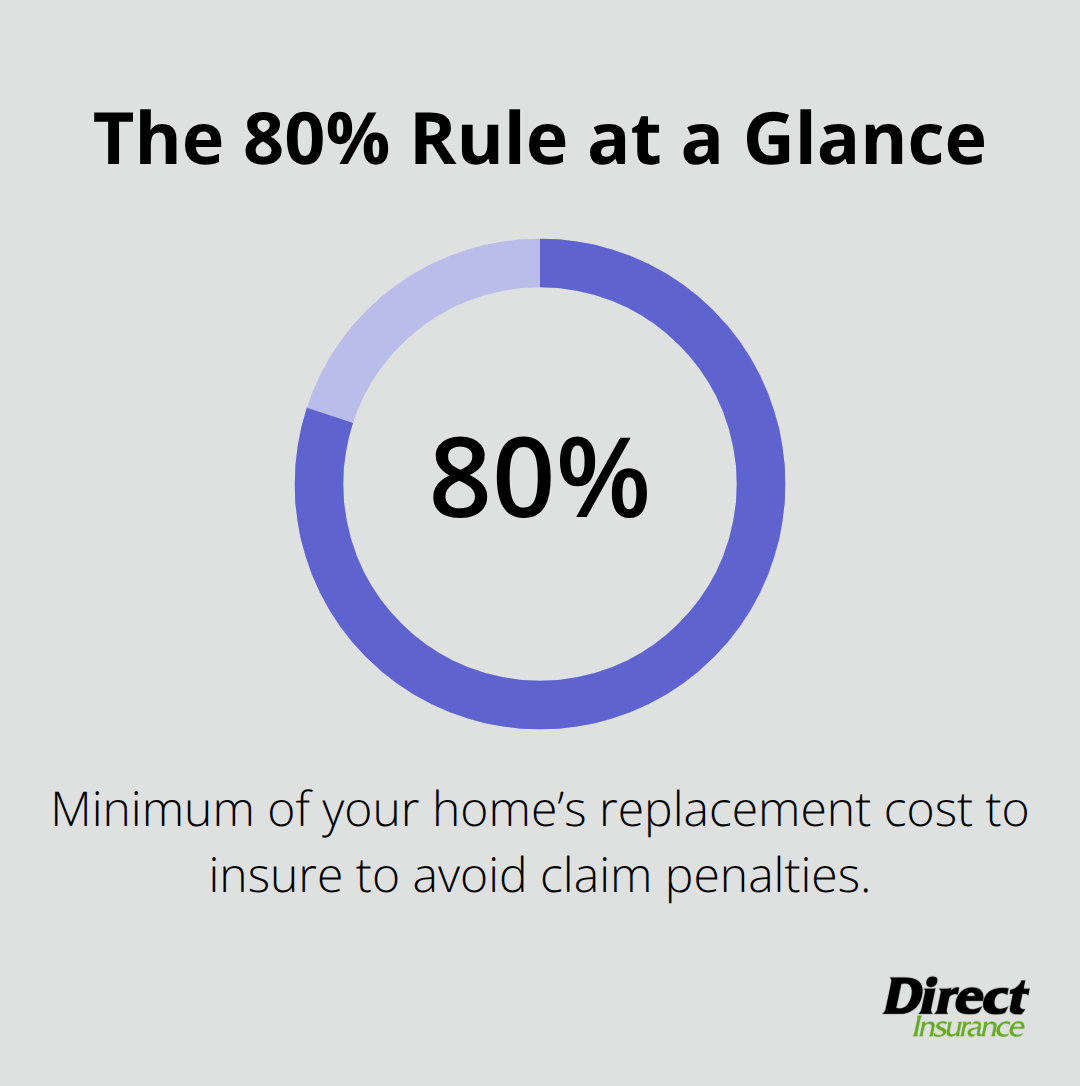

The 80% rule is non-negotiable: you must insure at least 80% of your home’s replacement cost, not its market value. Underinsuring below this threshold triggers a penalty where your claim payout gets reduced proportionally.

A home worth $400,000 on the market might cost $500,000 to rebuild with current construction costs, labor, and materials. That’s the number that matters for your dwelling limit, not the property tax assessment.

Choosing the Right Deductible for Your Budget

Your deductible choice directly controls your premium. The Zebra reports that homeowners with a $500 deductible pay roughly $2,999 annually on average, while those with a $2,000 deductible pay about $2,542. That $457 difference annually adds up over time, but only if you can actually afford the higher out-of-pocket cost when you file a claim. Your deductible should match your emergency fund, not your wishful thinking.

Prioritizing Coverage Where It Matters Most

Personal property coverage matters less than most people think because standard policies already cover the basics adequately for typical households. Unless you own jewelry, art, firearms, or other high-value items, you should increase your dwelling and liability limits instead-they deliver more protection per dollar spent. Liability coverage of $300,000 to $500,000 is a solid starting point for many households. Your homeowners policy excludes flood, earthquake, and certain water damage unless you purchase separate endorsements, and these exclusions are absolute. If you live in a flood zone or earthquake-prone area, you should add coverage before you need it-the cost is minimal compared to the catastrophic gap in protection.

The coverage decisions you make now directly shape what happens when disaster strikes. Next, we’ll show you how to lower what you pay for that protection without sacrificing the limits that actually matter.

How to Lower Your Home Insurance Costs

Bundle Your Home and Auto Policies

Bundling your home and auto policies is the fastest way to cut your overall insurance bill. Most insurers offer multi-policy discounts ranging from 10% to 25%, according to data from Bankrate. If you pay for home and auto separately, you leave money on the table. Erie advertises bundle discounts up to 25%, while Nationwide offers up to 20%. Beyond the discount itself, bundling simplifies your life-one renewal date, one agent to contact, and one login to manage both policies.

Claim the Discounts You Qualify For

Most homeowners miss discounts simply because they don’t ask about them. A monitored security system can reduce your premium by 5% to 15%, according to industry data. Water leak detectors with automatic shut-off systems save about 5% to 10% annually and address one of the leading causes of home insurance claims. Newer homes built within the last five years often qualify for new-construction discounts around 15%. If you maintain a claims-free history for three to five years, you qualify for a 5% to 15% discount, with savings reaching 10% to 25% after five or more years. Paperless billing and automatic payments typically add another small discount.

Improving your credit score can reduce premiums by roughly 10% to 20% in most states, though California, Maryland, and Massachusetts prohibit insurers from using credit scores for home insurance pricing. Smoke detectors, fire extinguishers, and other safety equipment also qualify for discounts at many carriers.

Compare Quotes From Multiple Insurers

The average American home insurance premium sits around $2,802 per year according to The Zebra, but your actual rate depends entirely on which carriers you compare. Getting quotes from just two or three insurers isn’t enough-you need to compare at least four to five major carriers to spot the real savings. A homeowner in one ZIP code might save $600 annually by switching to a different insurer, while another homeowner a few blocks away might save only $150 with the same switch. Location matters enormously because local weather patterns, building codes, and market dynamics affect pricing differently for each carrier. When you compare quotes, standardize the coverage levels across all quotes so you compare apples to apples. Verify that each insurer holds a strong financial strength rating of at least A- from AM Best, because the cheapest quote means nothing if the company cannot pay claims when disaster strikes.

The real savings emerge when you move beyond the basics and examine how your specific home, location, and risk profile affect your rates across different carriers. Your next step involves assessing your home’s actual value and contents to match your coverage to what you truly need to protect.

Finding the Right Home Insurance Plan for Your Situation

Calculate Your Home’s True Replacement Cost

Your home’s replacement cost differs dramatically from its market value, and this distinction determines whether you have adequate coverage. Construction costs have risen significantly due to inflation, supply chain disruptions, and tariffs on imported materials, according to The Zebra. To estimate your home’s replacement cost, multiply your home’s square footage by average building costs per square foot in your area. Once you know your replacement cost, apply the 80% rule strictly: insure at least 80% of that figure to avoid claim penalties. Insuring only 70% triggers proportional claim reductions, leaving you to cover the gap yourself.

Protect High-Value Items With Scheduled Endorsements

Your homeowners policy covers personal property at 50% to 70% of your dwelling limit by default, which works fine for most households. If you own jewelry, firearms, art, or collectibles worth more than a few thousand dollars, you need scheduled personal property endorsements that list items individually with specific coverage amounts. These endorsements cost roughly $100 to $300 annually but prevent devastating gaps when valuable items are stolen or damaged.

Assess Your Location’s Risk Profile

Your actual risk level depends on location far more than most homeowners realize. The Zebra data shows that premiums in Wrightsville Beach, North Carolina average $13,760 annually due to hurricane and flood exposure, while Hawaii homeowners pay roughly $721 on average. Within a single state, a home in Oklahoma City averages $8,544 annually while a home in Oklahoma’s rural areas might cost half that. Check whether your home sits in a flood zone, wildfire risk area, or earthquake zone using FEMA’s flood maps and your state’s geological survey data. If you live in a high-risk area, add flood and earthquake coverage before you need it-new policies typically have a 30-day waiting period, meaning coverage purchased after a storm or earthquake won’t protect you.

Factor In Home-Specific Risk Elements

Your roof age significantly affects your premium: homes with roofs over 20 years old pay substantially more because roof failure causes major water damage claims. Roofs under 5 years old qualify for age-related discounts at many carriers. Construction type also matters-brick and stone homes typically cost less to insure than wood-frame homes because they resist fire and wind damage better. Distance from a fire station affects your rate too; homes within 5 miles of a professional fire department pay less than those farther away.

Choose Payment Options That Maximize Savings

When you review payment options, select automatic monthly payments over annual or semi-annual payments because most insurers offer small discounts for autopay enrollment, typically 1% to 3%. This discount compounds over time and eliminates the risk of missing a payment deadline that could lapse your coverage.

Final Thoughts

Affordable home insurance comes down to three core actions: understanding what coverage you actually need, comparing rates across multiple carriers, and claiming every discount available to you. Homeowners who bundle policies save 10% to 25% on their total insurance costs, while those who raise their deductible from $500 to $2,000 cut their annual premium by roughly $450. Installing a monitored security system or water leak detector reduces premiums by 5% to 15%, and these concrete reductions add up to hundreds of dollars annually.

Your next step involves getting personalized quotes that reflect your specific home, location, and risk profile. Generic online quotes give you a starting point, but they miss the nuances that affect your actual rate-a home built in 2020 qualifies for different discounts than one built in 1985, and a brick home in a flood zone faces different pricing than a wood-frame home on higher ground. Only quotes tailored to your situation reveal where you can actually save money on affordable home insurance.

We at Direct Insurance Services shop multiple top-rated insurance companies to find you the best coverage at competitive rates. Contact us today to get a personalized quote and see how much you can save. Visit Direct Insurance Services to speak with an agent who understands your home and your budget.