Home Insurance Water Damage Coverage Explained

Water damage ranks as the second most common homeowner’s insurance claim, affecting 1 in 50 homes annually according to the Insurance Information Institute.

Home insurance water damage coverage protects against specific types of water incidents, but understanding what’s included and excluded can save you thousands in unexpected costs.

We at Direct Insurance Services help Utah homeowners navigate these complex coverage details to avoid claim denials when water damage strikes.

What Does Your Water Damage Policy Actually Cover?

Standard homeowners insurance covers sudden and accidental water damage from internal sources like burst pipes, appliance overflows, and plumbing failures. The Insurance Information Institute reports the average water damage claim costs exceed $12,500, which makes coverage limits critical for Utah homeowners. Most policies cover discharge from washing machines, dishwashers, and water heaters when the damage happens quickly and unexpectedly. However, gradual leaks that develop over time face automatic denial, even if they cause identical damage to sudden incidents.

Coverage Exclusions That Catch Homeowners Off Guard

Flood damage from external sources requires separate flood insurance through FEMA’s National Flood Insurance Program, with a mandatory 30-day wait period before coverage begins. Sewer backup and sump pump failures need specific endorsements (typically $50-100 annually for $10,000 in coverage). Groundwater seepage, common in Utah’s older neighborhoods with basements, receives no coverage under standard policies. Mold damage only qualifies for coverage when it results from a covered water incident, not from humidity or poor ventilation.

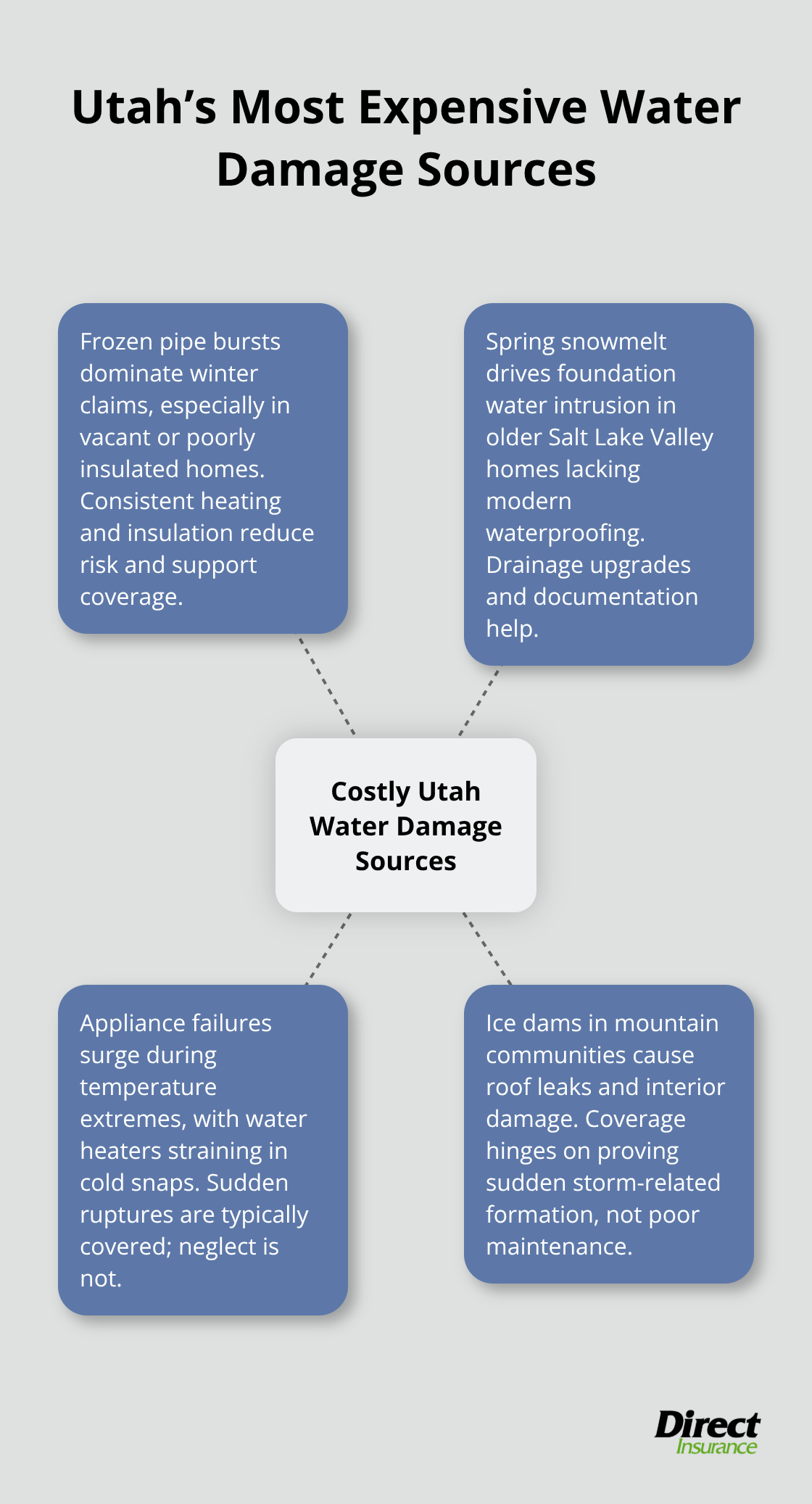

Utah’s Most Expensive Water Damage Claims

Frozen pipe bursts dominate Utah winter claims, particularly in vacant properties and homes with poor insulation.

Spring snowmelt creates foundation water intrusion issues, especially in Salt Lake Valley homes built before modern waterproofing standards. Appliance failures peak during Utah’s temperature extremes, with water heater failures that spike during cold snaps when units work harder. Roof leaks from ice dams cause significant damage in Park City and mountain communities, where coverage depends on proof that the leak resulted from sudden storm damage rather than poor maintenance.

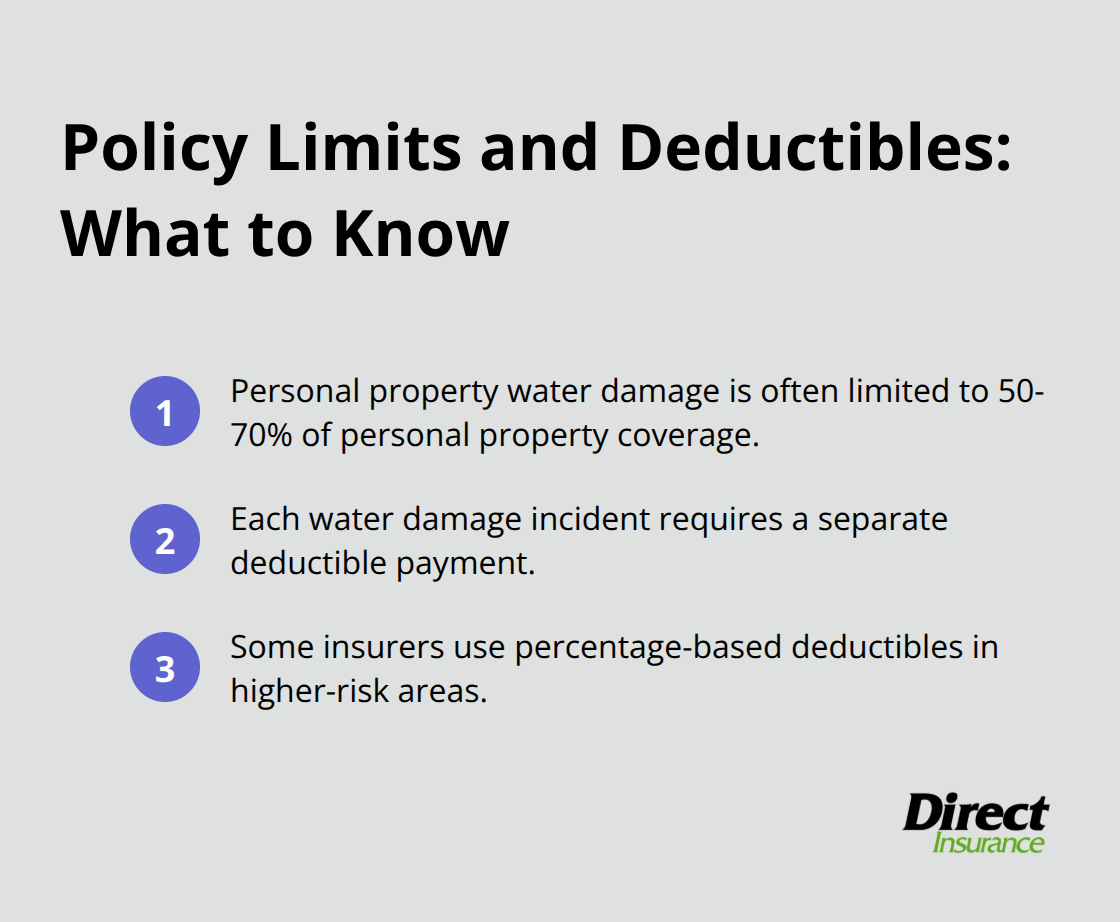

Policy Limits and Deductibles

Most homeowners policies include sub-limits for personal property damaged by water (often 50-70% of total personal property coverage). Your deductible applies to each water damage claim, which means multiple incidents in one year require separate deductible payments. Some insurers offer percentage-based deductibles for water damage claims, particularly in high-risk areas.

These coverage details become critical when you face specific water damage scenarios that Utah homeowners encounter most frequently.

Which Water Damage Scenarios Get Covered

Burst pipes from freezing temperatures create Utah’s highest-value water damage claims, with average costs of $18,000 per incident. Homes left unheated during winter face automatic coverage denial if pipes freeze due to negligence, but sudden bursts from extreme cold snaps with adequate heating typically receive full coverage. Denial rates drop to less than 5% when homeowners maintain minimum 55-degree temperatures and document heating system operation. Copper pipes in Utah homes built before 1990 show three times higher failure rates than newer PEX systems during temperature swings below 20 degrees.

Storm Damage Coverage Depends on Entry Point

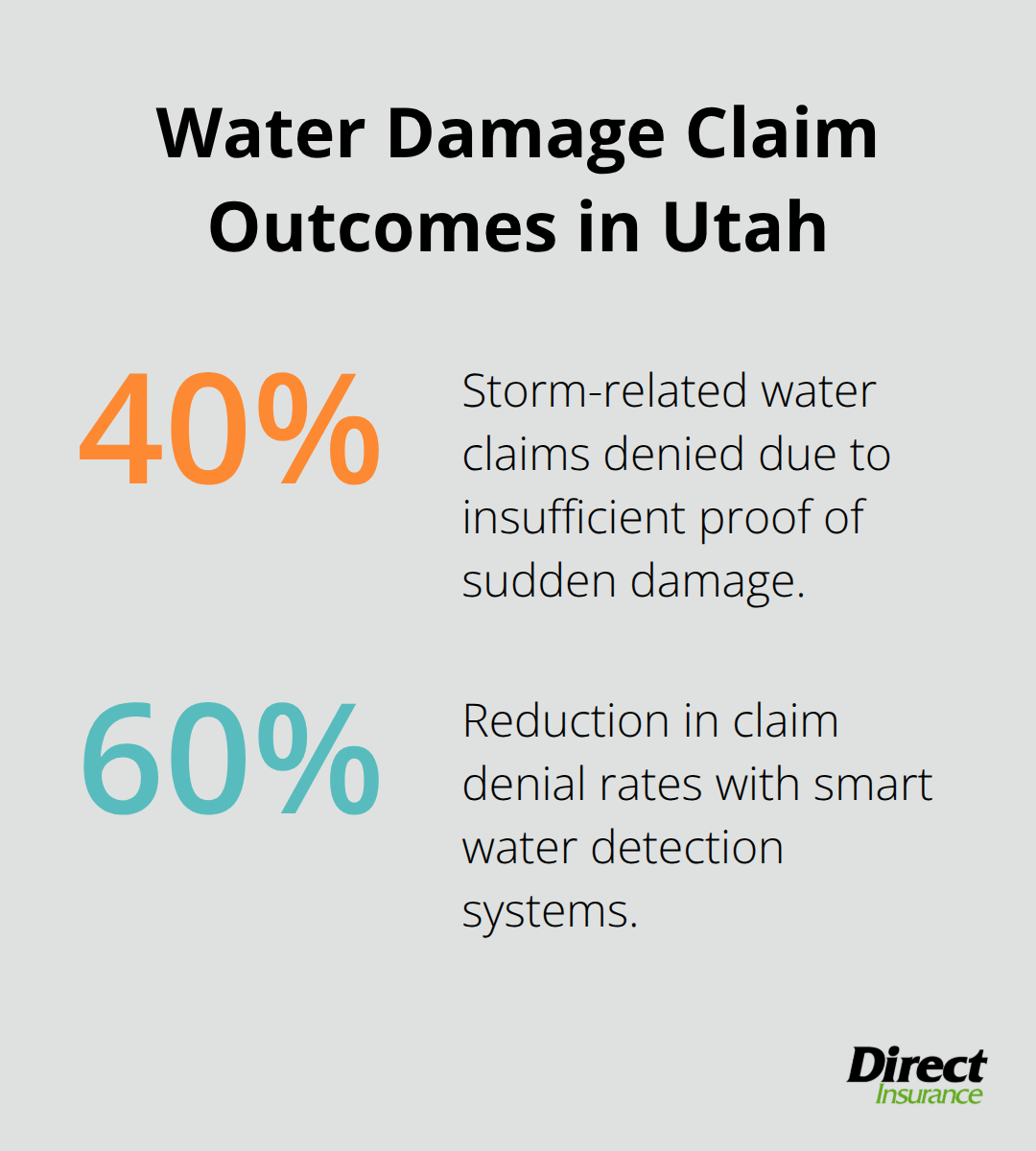

Wind-driven rain through damaged roofs, broken windows, or torn siding qualifies for coverage, but water that enters through intact openings faces automatic denial. Utah’s monsoon season creates unique challenges where coverage hinges on proof that storm damage caused the entry point rather than pre-existing maintenance issues. Ice dam formations in northern Utah counties receive coverage only when sudden temperature changes create the dams, not gradual winter accumulation. Documentation becomes critical since adjusters deny 40% of storm-related water claims due to insufficient proof of sudden damage versus gradual deterioration.

Appliance Failures Show Clear Coverage Patterns

Water heater ruptures receive coverage for damage but not appliance replacement costs, with claims that average $8,500 according to the National Association of Insurance Commissioners. Washing machine supply line failures get covered when hoses burst suddenly, but gradual leaks from worn connections face denial. Dishwasher overflows qualify only when mechanical failure causes the overflow, not user error or maintenance neglect. Smart water detection systems reduce claim denial rates by 60% since they provide timestamped evidence of sudden failures versus gradual leaks.

Foundation and Basement Water Issues

Sudden foundation cracks from seismic activity or extreme weather receive coverage, but gradual settlement damage faces exclusion. Basement flooding from broken interior pipes qualifies for coverage, while groundwater seepage through foundation walls does not. Sump pump failures require specific endorsements (typically costing $75-150 annually) to receive any coverage protection.

These coverage scenarios directly impact how you should document and report water damage incidents to maximize your claim approval chances.

How Do You File a Water Damage Claim Successfully

Contact your insurance company within 24 hours of water damage discovery, as most Utah insurers require immediate notification to prevent coverage denial. Many policies require that damage be reported within a certain time frame, and late reporting is a common reason for denied homeowners insurance claims. Stop the water source immediately, then photograph everything before you move damaged items or start cleanup.

Document Everything Before Cleanup Begins

Take photos from multiple angles that show the water source, affected areas, and damaged items with timestamps enabled on your camera. Document serial numbers on damaged appliances and electronics since replacement value depends on specific model information. Create a detailed inventory list with purchase dates and estimated values for all affected items. Insurance adjusters approve significantly more claims when homeowners provide comprehensive photo documentation compared to verbal descriptions alone.

Schedule Your Adjuster Visit Strategically

Schedule your insurance adjuster visit within 48-72 hours while water damage remains visible, as dried areas lose evidence that supports your claim. Accompany the adjuster during their inspection and point out all affected areas, including hidden damage behind walls or under floors. The adjuster needs to see wet materials and standing water to validate your claim fully.

Get Independent Contractor Estimates

Obtain written estimates from licensed contractors before your adjuster completes their assessment, since independent contractor estimates often exceed adjuster valuations significantly. Request a copy of the adjuster’s report and challenge any discrepancies immediately, as Utah law allows 30 days for claim disputes (after this period, appeals become much more difficult).

Choose the Right Restoration Team

Select contractors who work directly with insurance companies and understand claim documentation requirements. These professionals know how to document damage in ways that support your claim and can communicate effectively with adjusters. They also understand which repairs qualify for coverage and which fall under policy exclusions. Independent agents can provide valuable claims advocacy when disputes arise, improving your claim outcomes significantly.

Final Thoughts

Home insurance water damage coverage protects against sudden incidents like burst pipes and appliance failures, but excludes flooding, gradual leaks, and groundwater seepage. Utah homeowners face unique risks from frozen pipes, spring snowmelt, and ice dams that require specific documentation and immediate notification for successful claims. Policy reviews become essential as coverage limits, deductibles, and exclusions change annually.

Many homeowners discover gaps in their protection only after water damage occurs. Proactive coverage assessment provides vital financial protection against unexpected incidents. Utah’s specific water damage risks demand policies that address the most common scenarios that affect Salt Lake Valley properties (particularly winter freeze damage and spring snowmelt issues).

We at Direct Insurance Services shop multiple top-rated insurance companies to find comprehensive coverage at competitive rates. Our local team understands Utah’s water damage risks and works directly with homeowners to build appropriate policies. Direct Insurance Services provides personalized guidance through the claims process and helps you understand policy language when water damage strikes your home.