High-Risk Home Insurance: Protection When You Need It Most

Getting rejected for standard home insurance is frustrating. If your property sits in a high-crime neighborhood, has structural issues, or you’ve filed claims before, insurers often turn you away.

At Direct Insurance Services, we know that high-risk home insurance exists for exactly this situation. You have options-and this guide walks you through them.

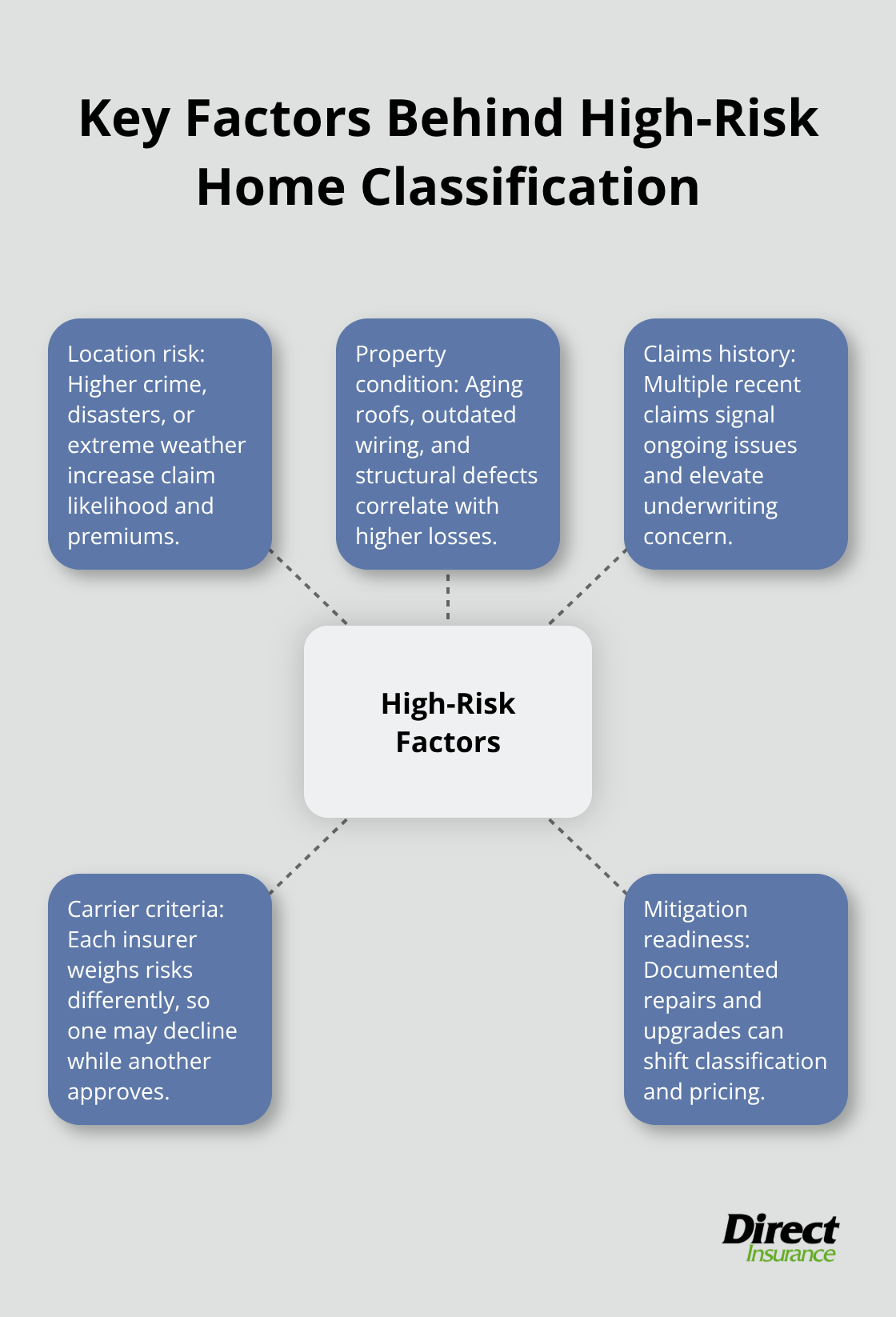

What Triggers High-Risk Classification

Insurers classify homes as high-risk based on concrete factors that increase claim likelihood. Location matters enormously-homes in areas with higher crime rates, frequent natural disasters, or extreme weather patterns face steeper premiums and nonrenewal rates. According to the U.S. Treasury Federal Insurance Office, policy nonrenewal rates are about 80% higher in the highest-risk ZIP Codes than in the lowest-risk areas. In high-risk wildfire zones across California, nonrenewals have accelerated significantly as carriers reassess exposure. Your home’s physical condition also determines risk classification. Structural issues like a cracked foundation, a roof older than 20 years, or knob-and-tube wiring push insurers toward high-risk pricing because these defects directly correlate with claims. Dated HVAC systems, failing septic tanks, and unsafe plumbing create similar concerns. One critical point: insurers don’t apply universal standards. A home labeled high-risk by one carrier may be insurable by another at standard rates. This means shopping multiple insurers isn’t optional-it’s essential for finding coverage that fits your situation.

How Location Affects Your Insurability

Properties in high-crime neighborhoods or disaster-prone regions face immediate classification challenges. Carriers pull loss data for specific ZIP Codes and neighborhoods to calculate expected claims. Wildfire-risk areas in California see particularly aggressive nonrenewals. If you receive a nonrenewal notice, contact your insurer immediately to ask about risk-mitigation steps that might preserve coverage. Starting your search early matters significantly because delays reduce available options in tight markets. The California Department of Insurance provides a Residential Insurance Company Contact List of 50+ carriers willing to write in high-risk areas, and their Premium Comparison Tool helps you avoid overpaying across different quotes.

Claims History and Property Condition

Previous claims signal higher future risk to underwriters. Filing multiple claims within five years (especially for water damage or theft) makes standard coverage difficult. Insurers view frequent claims as predictive of ongoing problems. Your property’s maintenance history also appears in underwriting reports. Missing repairs, neglected maintenance, or unresolved damage from prior incidents elevate risk classification. Vandalism and malicious mischief coverage becomes essential when properties face elevated risk from crime or neglect. If you’ve been denied coverage or faced nonrenewals, document what triggered the rejection. This information helps when shopping non-standard markets or working with agents familiar with your specific situation.

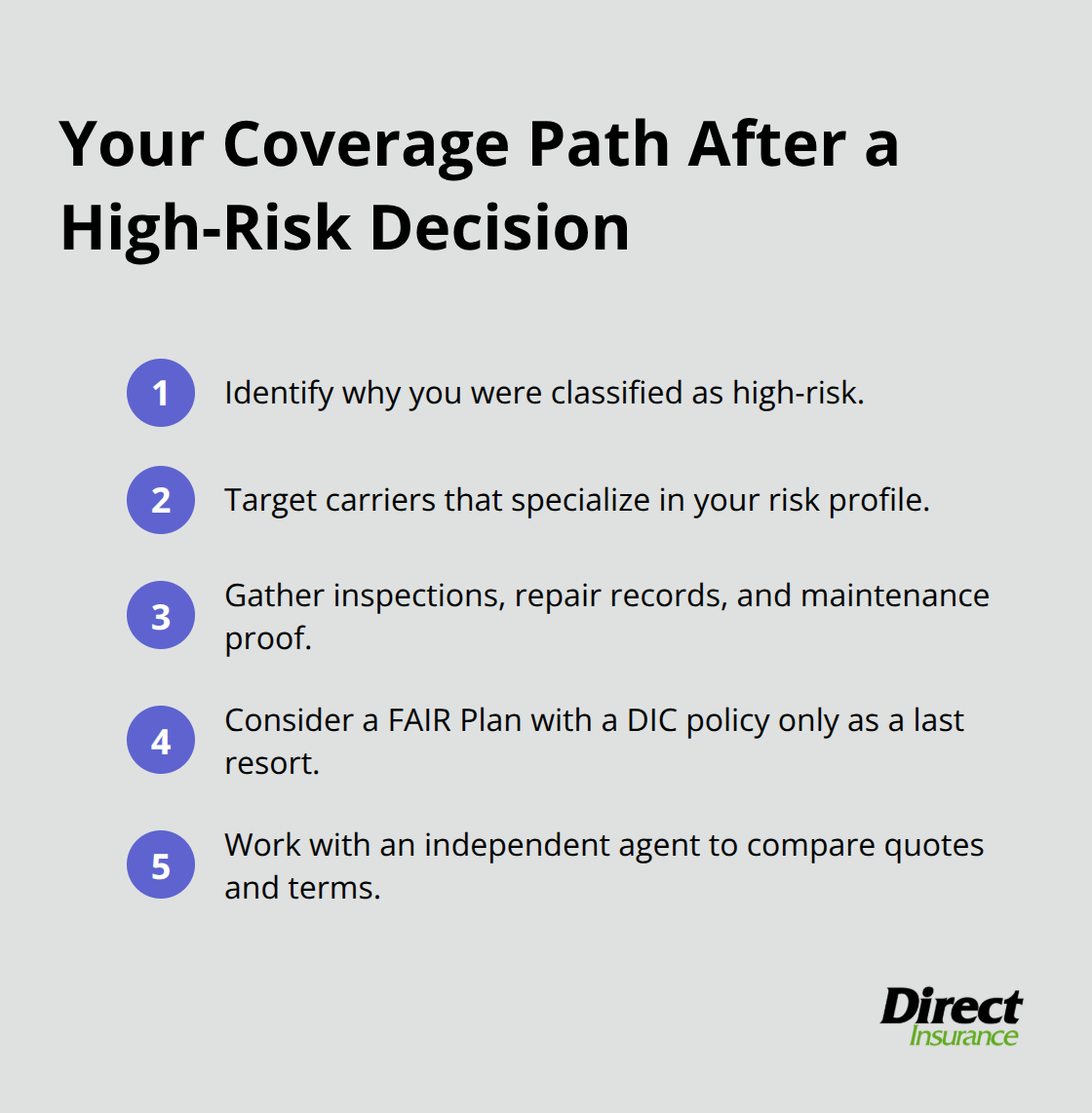

What Happens Next in Your Search

Once you understand why insurers classified your home as high-risk, you can take targeted action. The factors that triggered rejection-whether location, condition, or claims history-point you toward the right coverage solutions. Some carriers specialize in high-risk properties and actively write in markets others have abandoned. Others offer specialized plans with adjusted terms and higher premiums that reflect the elevated risk. Knowing your specific risk profile accelerates the process of finding an insurer willing to work with you, rather than applying blindly to carriers that won’t consider your situation.

Finding Coverage When Standard Insurance Won’t

Specialized Carriers Fill the Gap

When standard insurers reject your application, specialized carriers actively underwrite high-risk properties that mainstream insurers have abandoned. These carriers understand the specific factors that triggered your rejection and don’t treat high-risk homes as charity cases-they price policies to reflect genuine claim risk and operate profitably within that segment. Start by contacting non-standard insurers directly or through an independent agent who maintains relationships with carriers specializing in your risk profile.

The California Department of Insurance maintains a Residential Insurance Company Contact List of carriers willing to write high-risk coverage, which accelerates your search considerably. Many of these carriers offer HO-3 policies with standard coverage structures but apply stricter underwriting, higher premiums, or specific exclusions. The key difference: they’ll actually issue the policy.

How Coverage Varies Across Carriers

Some carriers offer specialized endorsements that address your specific risk. If your home has aged wiring, one carrier might exclude electrical damage while another might require an inspection and charge a premium adjustment. This variation means quotes from three carriers can differ dramatically in both price and coverage scope.

Start gathering documentation immediately: recent home inspections, renovation records, proof of maintenance, and details about any claims. This paperwork accelerates underwriting and demonstrates you’re a serious applicant. Many high-risk carriers complete underwriting faster when you present complete information upfront.

FAIR Plans: Protection of Last Resort

State FAIR Plans exist precisely for situations where no private insurer will write coverage. California’s FAIR Plan provides up to three million dollars in combined coverage across all policy sections, but covers only fire, lightning, internal explosion, and smoke-not wind, theft, or liability. This means a FAIR Plan policy alone leaves significant gaps.

If you obtain FAIR Plan coverage, you must layer additional protection through a Difference in Conditions policy to cover perils the FAIR Plan excludes. The FAIR Plan should be your last resort, not your first choice, because premiums run substantially higher than standard or even specialized high-risk policies. However, it guarantees you’re not uninsured while you continue shopping for better options.

Why Independent Agents Matter

An independent agent or broker becomes invaluable because they access both standard and non-standard markets simultaneously. They know which carriers are actively writing in your area, understand each carrier’s specific risk appetite, and can negotiate terms on your behalf. Rather than applying to ten carriers individually and facing ten rejections, an experienced agent submits applications to carriers likely to approve your risk profile.

This approach saves time and protects your credit from multiple inquiries. The difference between working alone and working with an agent often amounts to finding coverage versus remaining uninsured. With the right agent guiding your search, you move from rejection to approval faster and with less frustration. Your next step involves understanding what coverage you actually need once you secure coverage.

How to Lower Your Premiums and Improve Insurability

Fix Structural Problems First

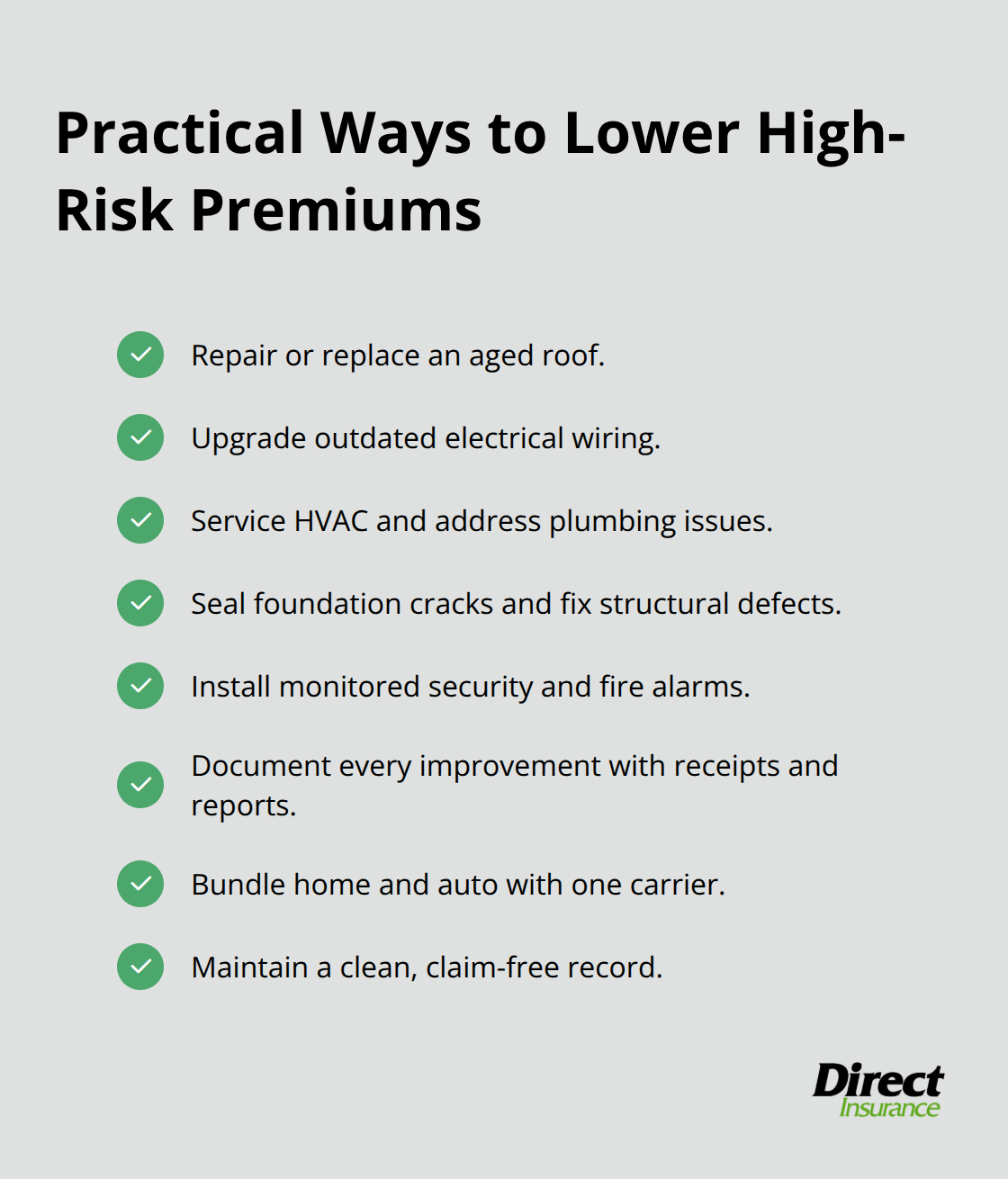

The most direct way to lower your premiums is fixing the problems that triggered high-risk classification in the first place. Roof repairs rank first because insurers scrutinize roof condition heavily-a roof older than 20 years signals imminent claims, and carriers either decline you or charge steep premiums. Replacing or repairing your roof can drop your premium by 10-15% immediately with some carriers. Upgrading outdated electrical systems matters equally; knob-and-tube wiring disqualifies you from most standard carriers, but installing modern wiring opens access to better rates and broader coverage options.

HVAC system repairs, plumbing upgrades, and foundation crack sealing follow similar logic-each repair removes a specific risk factor that underwriters flag during inspection.

The U.S. Treasury Federal Insurance Office data shows that high-risk ZIP Codes experience average claims around $24,000 compared to $19,000 in low-risk areas, meaning carriers price policies to account for severity. When you eliminate the physical defects driving that higher severity, insurers adjust your premium downward. Installing security systems and fire alarms delivers smaller but meaningful reductions, typically 5-10%, because these systems directly reduce theft and fire loss frequency.

Document Your Improvements

You must document every repair with receipts and inspection reports-this paperwork accelerates underwriting when you apply to new carriers and demonstrates you’re actively managing risk rather than ignoring problems. Carriers view documented improvements as proof that you take property maintenance seriously, which shifts their perception of your risk profile. This documentation becomes your strongest negotiating tool when shopping for better rates.

Bundle Policies for Immediate Savings

Bundling your home and auto policies with the same carrier typically yields 10-20% savings on your home premium, making this the fastest path to rate reduction if you haven’t already combined policies. This approach works regardless of your risk classification because carriers reward loyalty and multi-policy customers across all segments. If you currently split your coverage between different insurers, consolidating with one carrier produces immediate financial benefits.

Build a Clean Claims Record

Maintaining a clean claims history going forward matters enormously because even one claim within five years signals ongoing risk to underwriters; if you handle small repairs out-of-pocket instead of filing claims for minor damage, your renewal rates stay stable or decline. However, this doesn’t mean skipping legitimate claims-catastrophic damage should be reported immediately. The strategy is selective claims management: handle $500 roof leaks yourself, but report $15,000 water damage through insurance.

Once you hold a policy claim-free for three years, many carriers begin offering loyalty discounts and may reconsider your risk classification entirely, potentially moving you from high-risk to standard rates. An independent agent during this improvement period keeps you informed about which carriers are most receptive to your profile as conditions improve, so you can switch to better rates the moment you qualify rather than staying with an overpriced policy.

Final Thoughts

High-risk home insurance opens doors when standard carriers won’t write your policy, and your next step depends on your specific situation. If you’ve received a nonrenewal notice, contact your current insurer first to ask about risk-mitigation steps that might preserve coverage. If that fails, start shopping early because delays shrink your available options in tight markets, and specialized carriers actively underwrite properties that mainstream insurers have abandoned.

An independent agent becomes your strongest asset because they access both standard and non-standard markets simultaneously, submitting applications to carriers likely to approve your risk profile rather than facing rejection from ten carriers individually. While you search for coverage, start fixing the problems that triggered high-risk classification-roof repairs, electrical upgrades, and HVAC system improvements remove specific risk factors that underwriters flag, often dropping your premium by 10-15% once completed. Bundle your home and auto policies for immediate 10-20% savings, and build a clean claims record by handling minor repairs out-of-pocket while reporting catastrophic damage through insurance.

Contact Direct Insurance Services to discuss your high-risk home insurance options and start your path toward better coverage and lower premiums.