General Liability Insurance Utah: A Practical Guide for Businesses

Running a business in Utah means facing real liability risks every day. One accident or injury claim can drain your finances fast, which is why general liability insurance Utah is non-negotiable for most business owners.

At Direct Insurance Services, we’ve helped hundreds of Utah businesses find the right coverage to protect their operations. This guide walks you through what you need to know to make the right decision.

What General Liability Insurance Actually Covers

The Three Core Areas of Protection

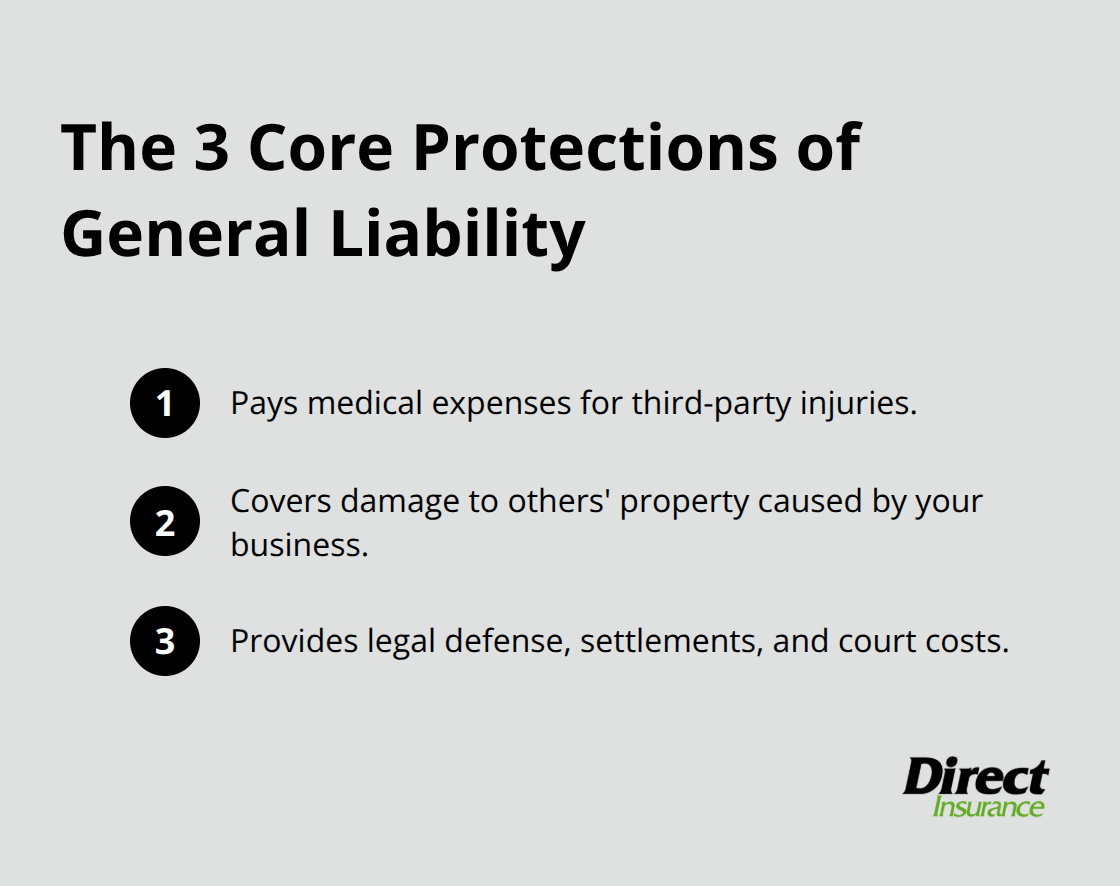

General liability insurance in Utah protects your business across three core areas that directly shield your finances. First, it pays medical expenses and related costs when a customer or third party suffers an injury during your business operations. Slip-and-fall injuries in retail spaces, tourist injuries on guided outdoor activities, and contractor mishaps on job sites represent common claims we see regularly. Second, it covers repair or replacement costs for damage to someone else’s property caused by your business activities.

A landscaping company that damages a client’s fence or a retail operation where a display fixture falls and breaks merchandise both rely on this protection. Third, it covers attorney fees, settlements, and court costs if your business faces a lawsuit. Legal defense alone can exceed $50,000 before any judgment or settlement is reached, making this component essential.

How Defense Costs Work in Your Policy

A standard Utah GL policy includes defense costs built into the coverage, which means your insurer pays your legal team separately from your policy limits. This structure provides a major advantage because it doesn’t reduce the money available for actual damages. Your policy also covers personal and advertising injury claims-mistakes in your marketing materials or false statements that damage someone’s reputation. This protection matters more than many business owners realize, particularly for businesses with active marketing campaigns or online presence.

Coverage Extensions Beyond Basic Protection

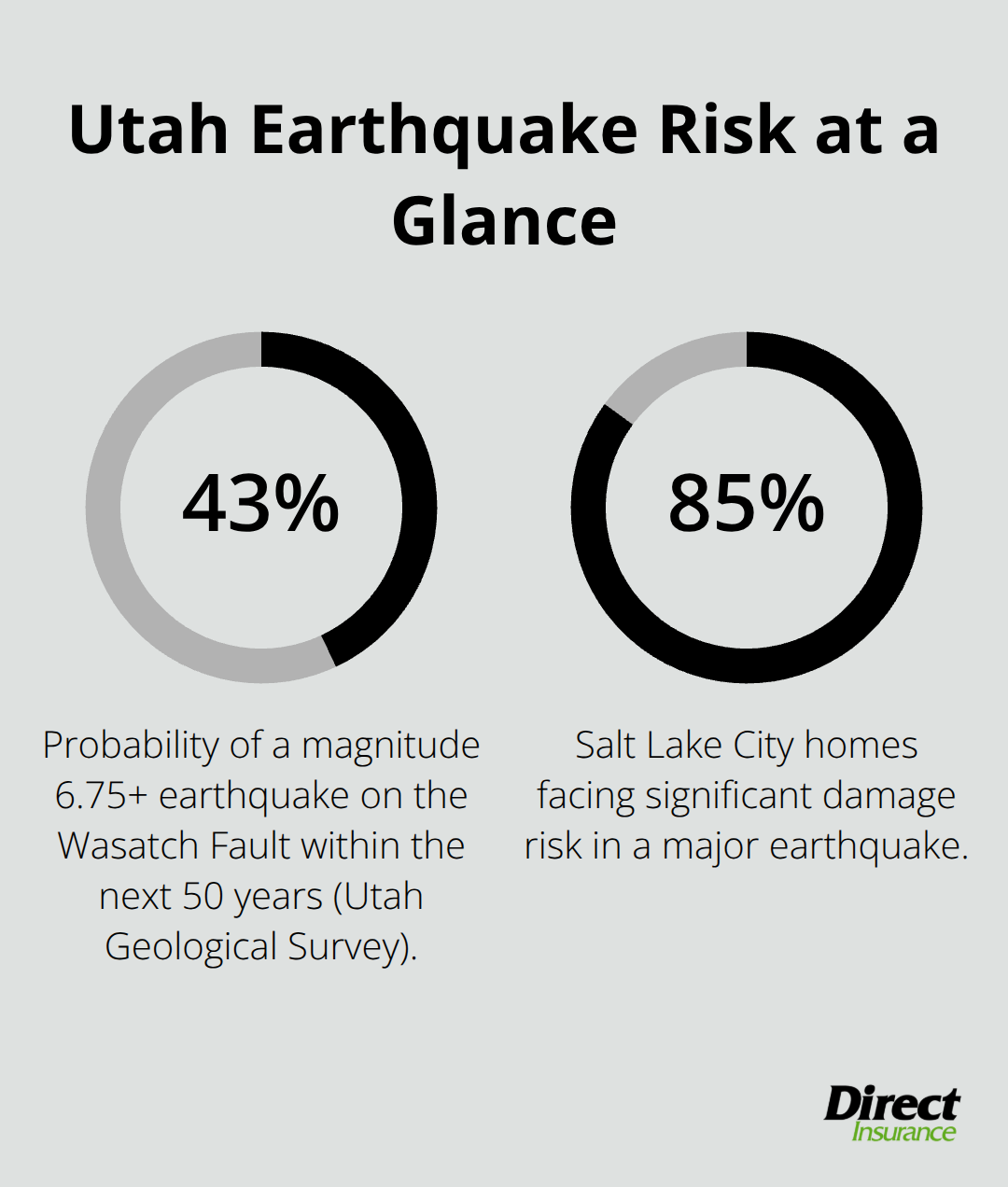

Some policies include premises and operations coverage, protecting you when customers are on your property. Products and completed operations coverage protects you after you finish a job or sell a product. However, standard GL policies exclude earthquake damage in Utah, which demands your attention. The Utah Geological Survey estimates a 43% probability of a magnitude 6.75 or greater earthquake on the Wasatch Fault in the next 50 years, and about 85% of Salt Lake City homes face significant damage risk in a major quake. You need separate earthquake coverage or an earthquake endorsement to protect against this risk. That coverage typically carries a deductible of 10-15% of your limits rather than a standard dollar amount.

Selecting the Right Coverage Limits

The coverage limits you choose directly impact your protection level. Most Utah businesses start with $1 million per occurrence and $2 million aggregate limits. Contractors and service providers often need higher limits like $2 million per occurrence because Utah law requires minimums of $100,000 per incident. This makes it sensible to exceed those minimums significantly. Your specific industry, location, and customer base all influence whether you should push limits higher than the standard starting point.

Understanding what your policy covers sets the foundation for choosing the right protection level. The next step involves assessing your specific industry risks and determining which additional endorsements your business actually needs.

Why Utah Businesses Need General Liability Insurance

Legal Requirements That Protect Your License

The Utah Division of Occupational and Professional Licensing (DOPL) mandates general liability insurance for licensed trades with minimum limits of $1 million per occurrence. Electrical contractors, landscaping companies, and registered handypersons all must carry this coverage. Operating without required protection puts your license at immediate risk and exposes your personal assets to liability claims. DOPL enforces these requirements strictly, and violations result in license suspension or revocation. Beyond contractors, many Utah businesses face practical insurance demands even without legal mandates. Landlords in busy areas like downtown Salt Lake City require proof of coverage before leasing space, and winning contracts often hinges on showing insurance documentation. Sole proprietors may escape legal requirements, but most on-site client work demands coverage proof in the contract itself. The consequences of ignoring these obligations extend beyond license suspension-you face breach-of-contract lawsuits and personal asset exposure if sued without coverage.

How GL Insurance Protects Your Financial Stability

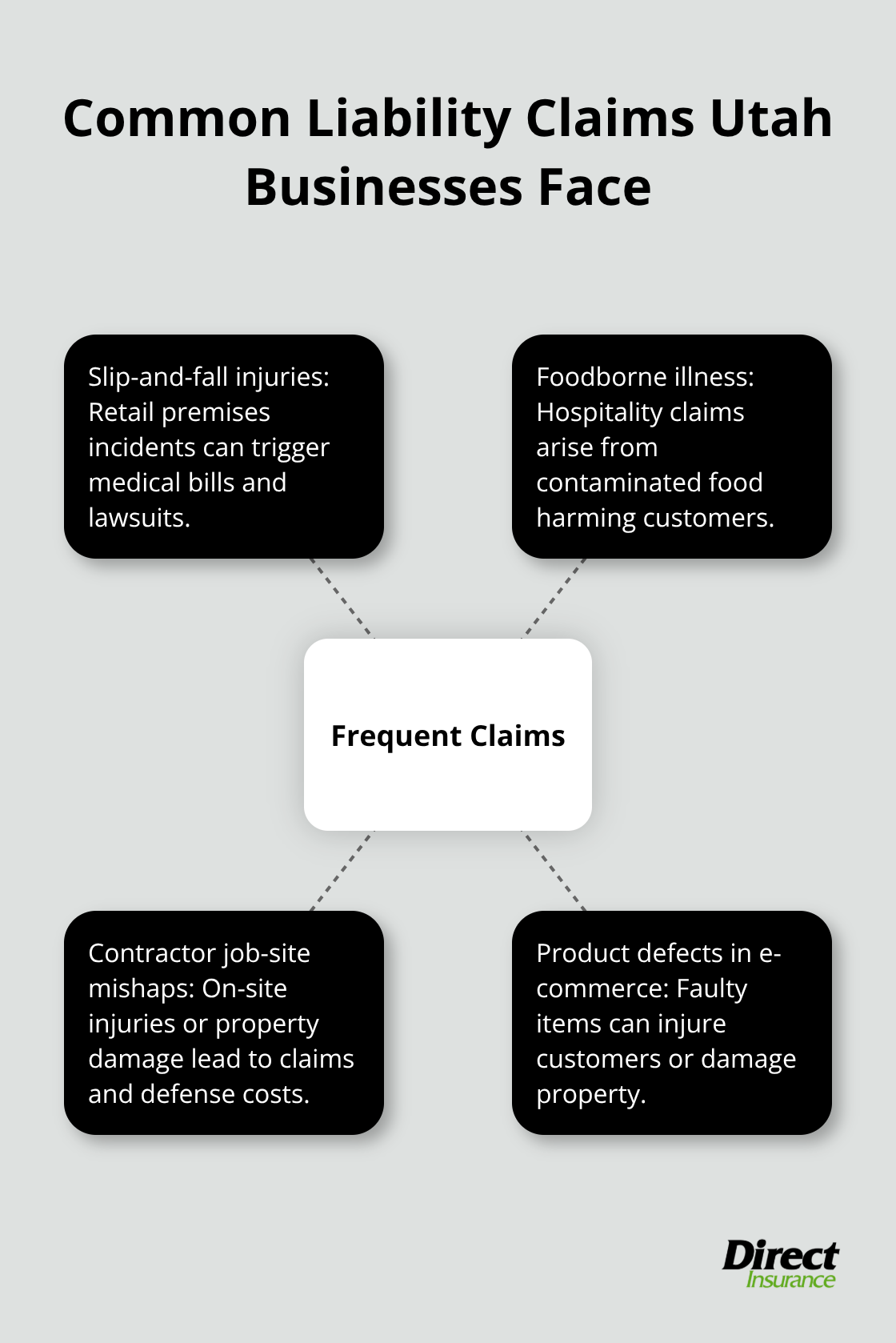

A single lawsuit drains finances faster than most business owners anticipate. Legal defense costs alone can exceed $50,000 before any settlement or judgment, and that money comes directly from your operating capital if you lack coverage. Slip-and-fall injuries in retail, foodborne illness claims in hospitality, contractor mishaps on job sites, and product defects in e-commerce represent the types of claims we see regularly across Utah industries.

Small and medium-sized businesses particularly struggle with unexpected litigation costs-they lack the financial reserves of larger corporations. General liability insurance separates these costs from your business operations, meaning your legal team gets paid without draining cash reserves needed for payroll, inventory, or growth.

Utah’s Growing Construction Market and Liability Exposure

Utah construction employment peaked at approximately 145,300 in May 2025, signaling strong market activity and corresponding liability exposure across the state. Whether you operate in construction, retail, hospitality, or professional services, the financial protection GL insurance provides isn’t optional-it’s the difference between surviving a claim and closing your doors. The liability risks you face depend heavily on your specific industry and daily operations. Understanding these risks helps you select appropriate coverage limits and endorsements that actually match your exposure.

How to Choose the Right General Liability Policy for Your Utah Business

Map Your Daily Operations to Actual Risk Exposure

Start by documenting what happens in your business each day, not industry generalizations. A landscaping contractor faces different risks than a tech consultant, and a retail store in downtown Salt Lake City encounters different hazards than one in a rural county. Your first step involves identifying the types of injuries or property damage that could realistically occur in your operations. Retail businesses should focus on slip-and-fall exposure and customer injuries on premises. Contractors need to assess on-site injury risks and property damage potential. Service providers should evaluate client property damage exposure during service delivery.

This assessment directly determines whether standard $1 million per occurrence limits suffice or whether you need $2 million coverage. Liability exposure analysis should include reviewing contract obligations, industry-specific rules, and past claim patterns to ensure adequate protection.

Understand Utah’s Minimum Requirements and Coverage Limits

The Utah Division of Occupational and Professional Licensing requires $100,000 per incident and $300,000 aggregate minimums for licensed trades, but this floor doesn’t represent your actual need. Most Utah businesses start with $1 million per occurrence and $2 million aggregate, then adjust upward based on contract requirements and exposure analysis. Higher limits add minimal premium costs at this range-often just 5-10% more-yet provide substantially better protection.

Your location within Utah influences premium costs dramatically. Salt Lake Valley experiences very high earthquake risk with premium multipliers around 140-180% of state average, while Northern Utah runs 95-120%. Obtain quotes from carriers experienced with Utah’s regional risk factors, particularly if you operate in high-risk Wasatch Front areas or near ski resort regions with mountain-specific exposures.

Address Earthquake Coverage and Policy Exclusions

Standard general liability policies exclude earthquake damage entirely, yet the Utah Geological Survey estimates a 43% probability of a magnitude 6.75 or greater earthquake on the Wasatch Fault within the next 50 years. Separate earthquake endorsements typically carry 10-15% deductibles rather than fixed dollar amounts, making them affordable additions to your base policy.

This protection matters far more in Utah than in most states.

Beyond earthquake coverage, review whether your policy includes additional insured status for clients who require it, hired and non-owned auto liability if you use contractor vehicles, and completed operations coverage if you deliver products or finish projects. Your policy exclusions matter more than most business owners realize, and earthquake coverage demands immediate attention in Utah.

Compare Carriers Based on Your Specific Needs

Businesses needing multiple endorsements should compare carriers carefully. ERGO NEXT excels for sole proprietors wanting fast digital quotes and same-day certificates of insurance, while The Hartford offers broader professional service endorsements like employment practices liability and cyber coverage. Simply Business connects you with multiple carriers for instant comparison quotes. Thimble works best for flexible short-term coverage on hourly or monthly terms.

Your industry type and growth plans should drive your carrier selection. A contractor needing comprehensive coverage with multiple endorsements faces different priorities than a service provider seeking basic protection with flexible payment terms. Request quotes from at least five carriers to confirm which option aligns with your actual exposure and budget constraints.

Final Thoughts

General liability insurance in Utah protects your business from the financial devastation that follows a single lawsuit or injury claim. The coverage you’ve learned about-bodily injury protection, property damage liability, and legal defense costs-forms the foundation of responsible business operations across Utah, whether you operate a contractor business subject to DOPL requirements or run a service company where clients demand proof of coverage. Your next step involves requesting quotes from at least five carriers to understand what coverage costs for your specific situation, and you should ask specifically about earthquake endorsements, additional insured status for client requirements, and any industry-specific endorsements your contracts demand.

Regional factors matter significantly when you compare proposals, since Salt Lake Valley premiums run substantially higher than Northern Utah due to earthquake risk and population density. Same-day certificate of insurance availability matters if you bid on projects regularly, so confirm turnaround times during your comparison process. An independent insurance agent who understands Utah’s unique risks gives you a significant advantage over shopping alone, since they know which carriers excel for contractors in the Wasatch Front and which providers work best for retail operations.

Direct Insurance Services helps Utah businesses find the right general liability insurance coverage that actually matches your exposure and budget. Contact us today to discuss your specific needs and receive a customized quote that protects your Utah business properly.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation