Commercial Liability Insurance Utah: Coverage For Your Business

One accident on your business premises can trigger a lawsuit that threatens everything you’ve built. Commercial liability insurance in Utah protects you from the financial fallout of injuries, property damage, and legal claims.

At Direct Insurance Services, we’ve helped countless Utah business owners understand what coverage they actually need. This guide walks you through the essentials so you can make an informed decision.

What Commercial Liability Insurance Actually Protects

Bodily Injury and Property Damage Form Your Coverage Foundation

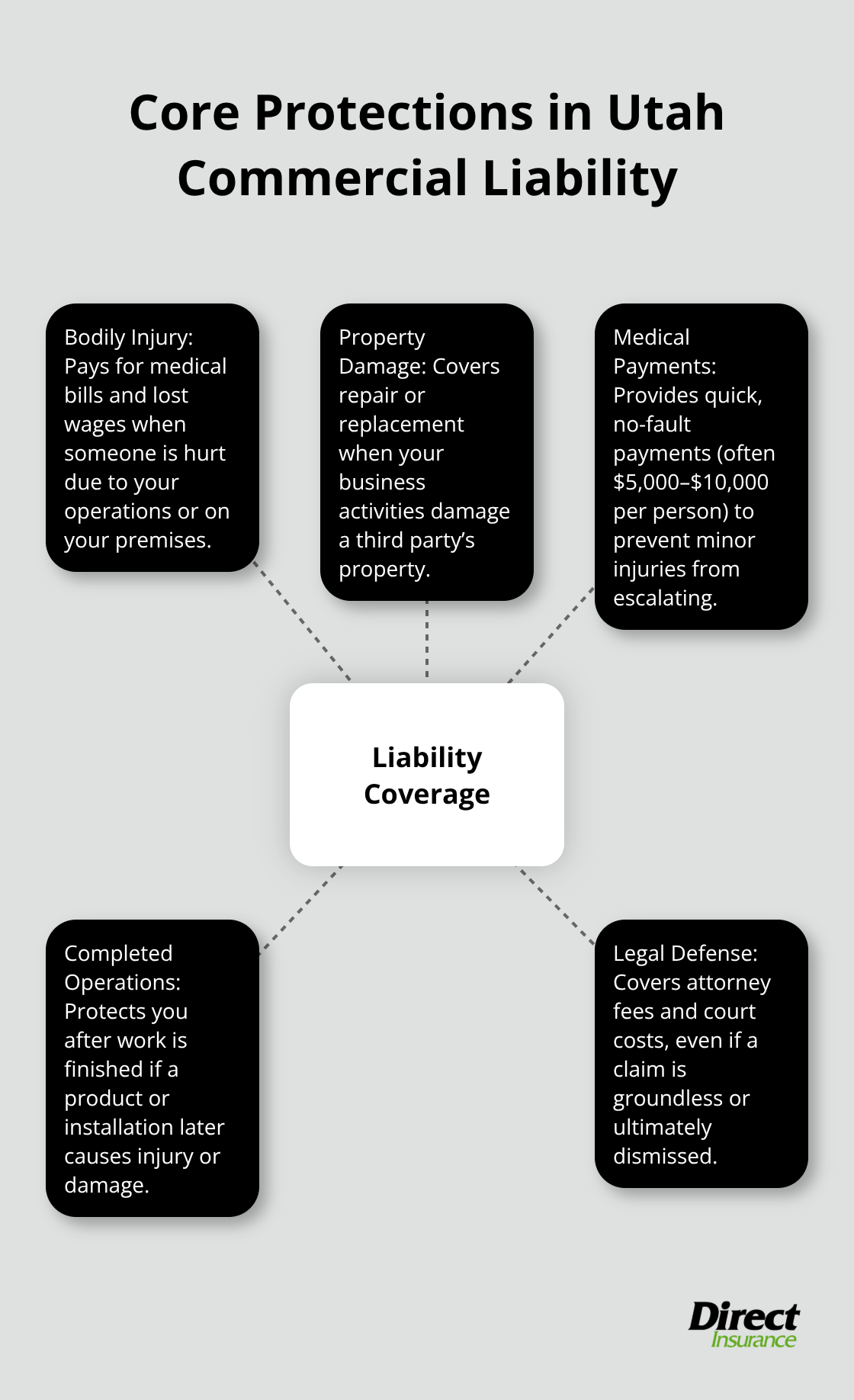

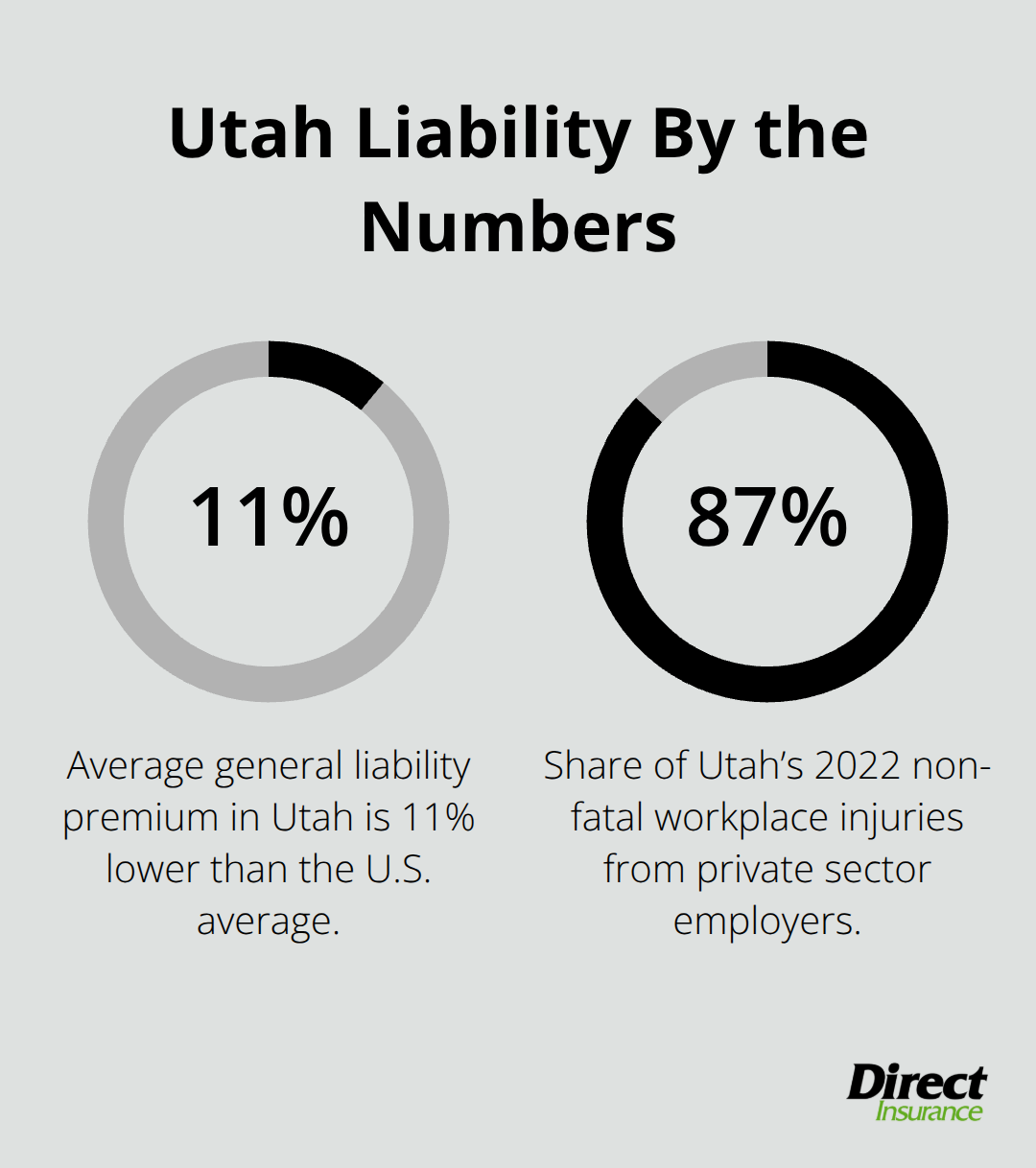

Commercial liability insurance covers three core areas that matter most when something goes wrong on your property or through your business operations. Bodily injury and property damage claims form the backbone of any liability policy. If a customer trips on your premises and breaks their leg, or your equipment damages a client’s property, this coverage pays for their medical bills, lost wages, and repair costs. In Utah, general liability policies typically start at $1,000,000 per occurrence and $2,000,000 aggregate, though higher-risk businesses often need $2,000,000 per occurrence and $4,000,000 aggregate. According to MoneyGeek data, Utah small businesses pay an average of $110 per month for general liability coverage, which is about 11% below the national average of $123 per month.

Industry Risk Determines Your Premium and Coverage Needs

Construction and contracting businesses in Utah pay significantly more at around $291 per month because jobsite risk is substantially higher, while tech and IT services cost roughly $26 per month. The key is matching your coverage limits to your actual exposure, not just picking a standard number and hoping it works. Your industry classification directly affects what you’ll pay and what limits you’ll need to carry.

Medical Payments Coverage Stops Small Claims From Becoming Lawsuits

Medical payments coverage is separate from bodily injury claims and typically covers $5,000 per person for minor on-site injuries. Many Utah business owners ignore this because it seems minor, but raising it to $10,000 per person actually prevents small incidents from escalating into lawsuits. When you pay for a customer’s immediate medical care yourself, you reduce their motivation to hire an attorney and pursue a larger claim. Legal defense costs are also built into your liability policy, meaning the insurer covers your attorney fees and court costs even if the claim is frivolous.

Completed Operations Coverage Protects You Long After the Work Ends

This matters enormously in Utah because the state allows a four-year window for civil actions, which means claims can surface years after an incident. If you run a product-based business, completed operations coverage protects you after you’ve delivered the product or finished the job. A faulty installation or defective product that causes damage months later remains your responsibility under this coverage. Contractors and manufacturers in Utah need to verify their completed operations coverage extends long enough to match their typical project timelines and customer relationships.

Understanding what your policy actually covers is only half the battle-knowing whether you have enough coverage for your specific business risks is what separates protected operations from exposed ones.

Why Your Utah Business Needs This Coverage Now

Utah’s Legal Framework Creates Unique Liability Exposure

Utah’s Modified Comparative Fault Rule holds you liable for a percentage of damages even when you’re not the primary cause of an incident. This shifts your financial risk in ways that many business owners don’t anticipate. The state’s four-year civil action window means claims can surface years after an incident occurs, extending your exposure period far beyond what most business owners expect. Unlike states with shorter claim windows, Utah gives injured parties substantial time to pursue legal action, which means your liability exposure persists long after a project ends or a transaction closes.

Real Injury Data Shows Why Coverage Matters in Utah

According to the Bureau of Labor Statistics, Utah experienced 31,700 non-fatal workplace injuries in 2022, with about 87% coming from private sector employers. That statistic matters because it shows how real these risks are in your market.

Without commercial liability coverage, a single incident can wipe out years of profit. One customer injured on your premises could trigger a lawsuit that costs tens of thousands in legal defense alone, regardless of whether the claim succeeds.

The True Cost of Operating Without Coverage

Many Utah business owners assume their personal assets stay separate from business liability, but that protection only holds if you maintain proper insurance. Contracts with landlords, vendors, and clients increasingly require proof of liability coverage before they’ll work with you, making insurance a practical necessity for winning business deals. If a lawsuit hits and you lack coverage, you’re personally responsible for settlements, court costs, and attorney fees that could easily exceed $50,000 even for a straightforward claim.

Coverage Costs Far Less Than You Might Think

General liability in Utah costs an average of $110 per month for most small businesses, roughly 11% cheaper than the national average. That’s $1,320 annually for baseline protection that prevents a single lawsuit from destroying your business. Construction contractors in Utah pay around $291 per month because their risk exposure is higher, while tech services might pay $26 per month. Your industry determines your actual cost, not some theoretical benchmark. Medical payments coverage at $5,000 per person typically costs almost nothing to add but prevents minor incidents from becoming major lawsuits.

Choosing the Right Coverage Protects Your Business Future

The decision to carry adequate liability coverage isn’t about compliance alone-it’s about protecting the revenue, assets, and reputation you’ve built. Your specific business operations demand coverage limits tailored to your actual exposure, not generic limits that leave gaps. Understanding what you need to carry is the first step, but selecting the right limits for your industry and operation size requires careful analysis of your real risks.

How to Choose the Right Commercial Liability Coverage

Assess Your Business Risks and Industry Exposure

Start by tallying your real exposure, not industry averages. If you operate a construction company, your jobsite liability differs vastly from a consulting firm working from an office. Walk through your premises and identify where injuries could happen: customer areas, loading zones, equipment storage, parking lots. Talk to your employees about near-misses they’ve experienced. These conversations reveal exposure gaps that generic benchmarks miss. Your coverage limits should reflect your specific operations.

Compare Coverage Limits and Policy Options

A $1,000,000 per occurrence limit works for many Utah small businesses, but if you handle high-value client property or operate in high-traffic areas, you may need $2,000,000 per occurrence. The additional cost to jump from $1,000,000 to $2,000,000 in coverage runs roughly $600 annually through an umbrella policy, which is minimal protection compared to the exposure you’d carry without it. If a single carrier can’t offer your target limits, an umbrella policy bridges the gap efficiently.

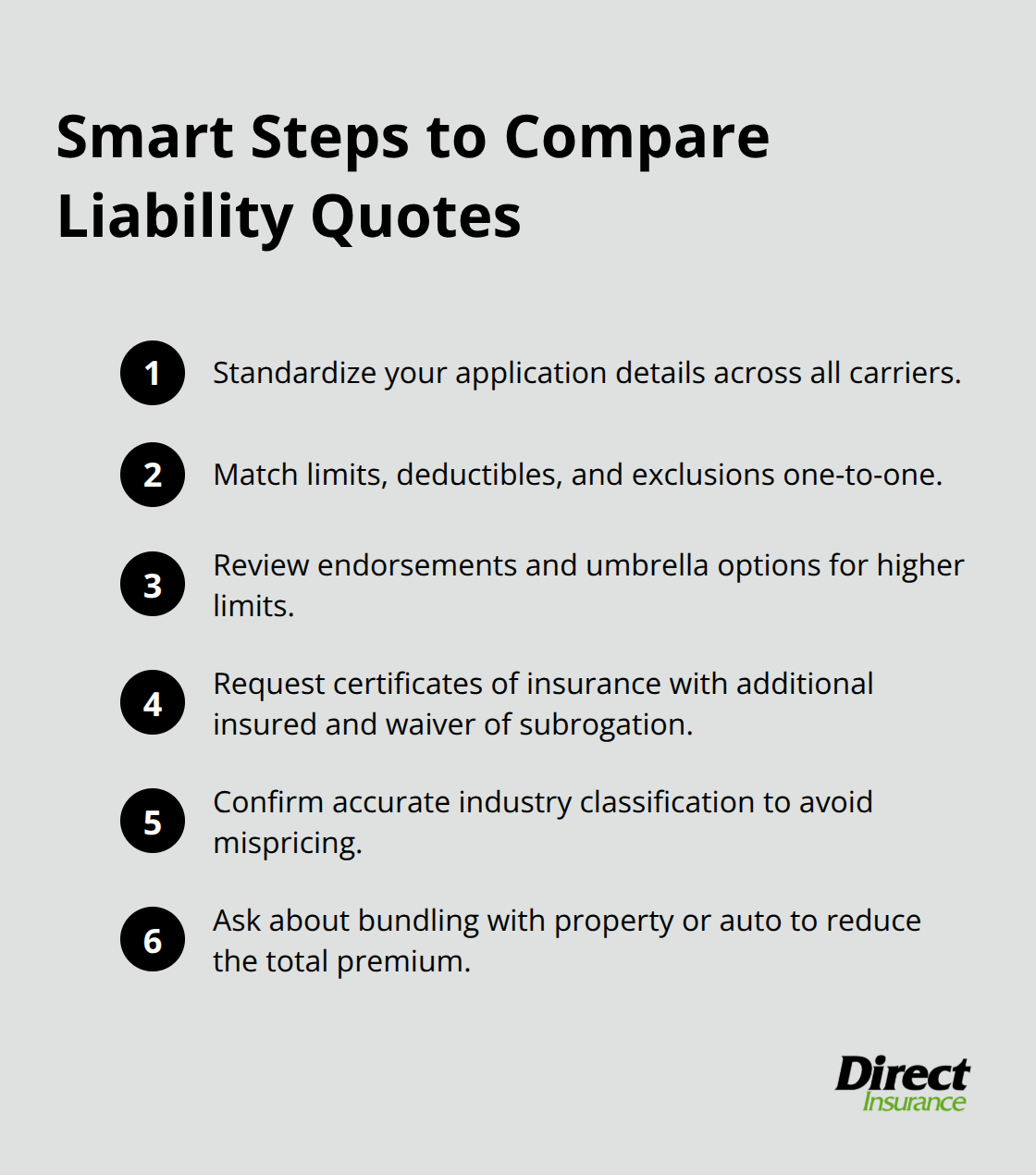

Don’t accept the first quote you receive. When you request quotes, provide identical information to multiple insurers so you can actually compare apples to apples. Verify that each quote includes the same coverage limits, deductible, and exclusions. A $500 deductible versus a $1,000 deductible creates meaningful price differences, as does the scope of coverage.

Some carriers exclude certain business operations you actually perform, leaving gaps you didn’t anticipate.

Request certificates of insurance from each carrier that name you as an additional insured and include waiver of subrogation language, because that’s what your clients and landlords will demand anyway. Your industry classification directly controls your price, so accurate classification matters more than shopping for discounts alone.

Work With a Local Insurance Agent Who Understands Utah

A local Utah insurance agent understands regional hazards like wildfire and earthquake risk that affect your premiums, plus they know how local courts interpret liability claims under modified comparative fault rule in Utah. Prepare a simple inventory of your operations before any agent conversation. Write down what you do, how many employees you have, your annual revenue or payroll, and any prior claims or incidents. Include details about client interactions, property you handle, and whether you use vehicles for business. If you hire contractors or subcontractors, note that too. Agents can’t accurately quote you without this context.

When you meet with a local Utah agent, bring lease agreements or vendor contracts that specify insurance requirements, because those often mandate minimum limits higher than your baseline needs. Many landlords in Utah require tenants to carry $2,000,000 aggregate coverage, which means your standard $1,000,000 per occurrence won’t satisfy their lease terms. Knowing these requirements upfront prevents delays and policy cancellations later. Ask your agent about bundling options, since combining general liability with property or auto coverage often reduces your total premium. That savings compounds across multiple policies.

Final Thoughts

Commercial liability insurance in Utah protects your business from financial devastation that a single incident can trigger. The coverage costs far less than most business owners expect-roughly $110 monthly for small businesses-yet one uninsured claim can exceed $50,000 in legal fees alone. Your industry determines your actual premium, so a tech consultant pays around $26 monthly while a construction contractor pays $291 monthly, reflecting real exposure differences that your coverage limits must match.

Start by walking through your premises to identify where injuries could occur and talk to your employees about near-misses they’ve experienced. Document your operations, employee count, and annual revenue before contacting an agent, and gather any lease agreements or vendor contracts since they often specify minimum coverage limits you must carry. Request quotes from multiple carriers using identical information so you can compare prices and coverage accurately, then ask about bundling options that combine general liability with property or auto coverage to reduce your total premium.

We at Direct Insurance Services understand Utah’s unique liability landscape and shop multiple top-rated insurance companies to find you the best commercial liability insurance Utah coverage at competitive rates. Contact us to discuss your specific needs and receive a quote tailored to your actual operations.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation