Protect Your Practice: Utah Professional Liability Insurance

One mistake can cost your practice thousands of dollars-or worse, your reputation. Utah professional liability insurance protects you when clients claim you failed to deliver the standard of care they expected.

At Direct Insurance Services, we’ve helped countless Utah professionals understand that this coverage isn’t optional for most practices. It’s a business necessity that separates thriving practices from those struggling to recover from a single claim.

What Professional Liability Insurance Actually Covers

Professional liability insurance protects you against claims that your work caused financial loss to a client. Unlike general liability, which covers bodily injury or property damage, professional liability insurance specifically addresses mistakes, errors, or failures in the services you deliver. The coverage pays for defense costs, settlements, and judgments when a client sues you for negligence, misrepresentation, inaccurate advice, missed deadlines, incomplete work, or breach of contract. According to MoneyGeek’s analysis of Utah small businesses, professional liability insurance costs an average of $74 per month, making this protection affordable for most practices. What makes this coverage essential is that you can face lawsuits even when you didn’t actually make a mistake-the claim alone triggers your insurer’s obligation to defend you, which costs thousands in legal fees before any settlement occurs.

When You Actually Need This Coverage

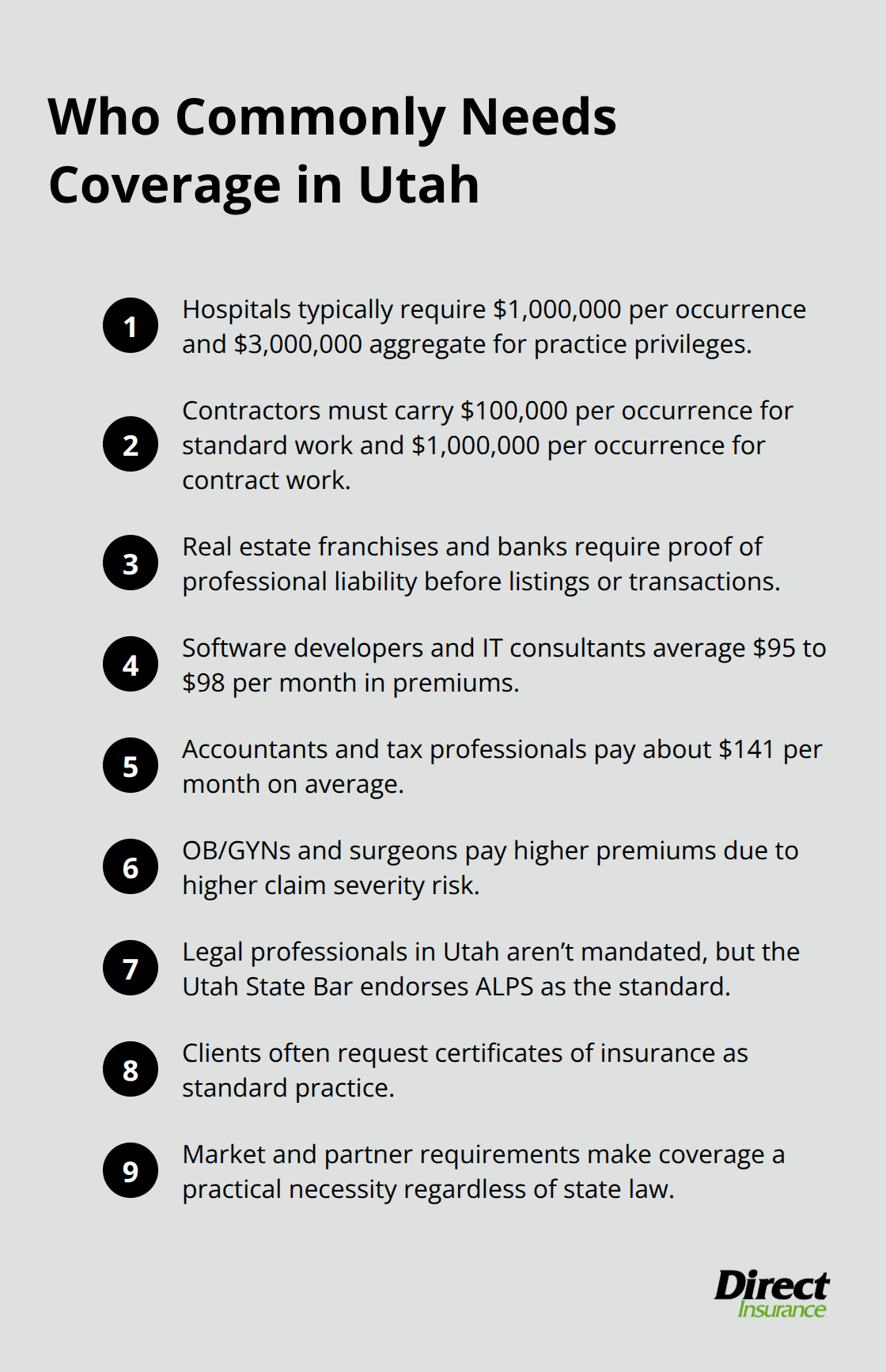

Utah doesn’t mandate professional liability insurance by statute for most professions, but that absence of legal requirement creates a false sense of security. Contractors must meet Department of Professional Licensing minimums: $100,000 per occurrence and $300,000 aggregate for standard work, or $1,000,000 per occurrence and $2,000,000 aggregate for contract work. Real estate agents face consistent requests for proof of coverage from franchise partners, banks, and clients, even though the state doesn’t require it. Healthcare providers aren’t state-mandated to carry coverage either, but hospitals routinely demand $1,000,000 per occurrence and $3,000,000 aggregate before granting practice privileges. The pattern is clear: your clients and business partners will demand this coverage regardless of state law, making it a practical requirement that affects your ability to work. Software developers, IT consultants, accountants, and management consultants in Utah’s Silicon Slopes tech sector should carry coverage to protect against data breaches, project-delivery failures, and intellectual property disputes-areas where claims have become increasingly common.

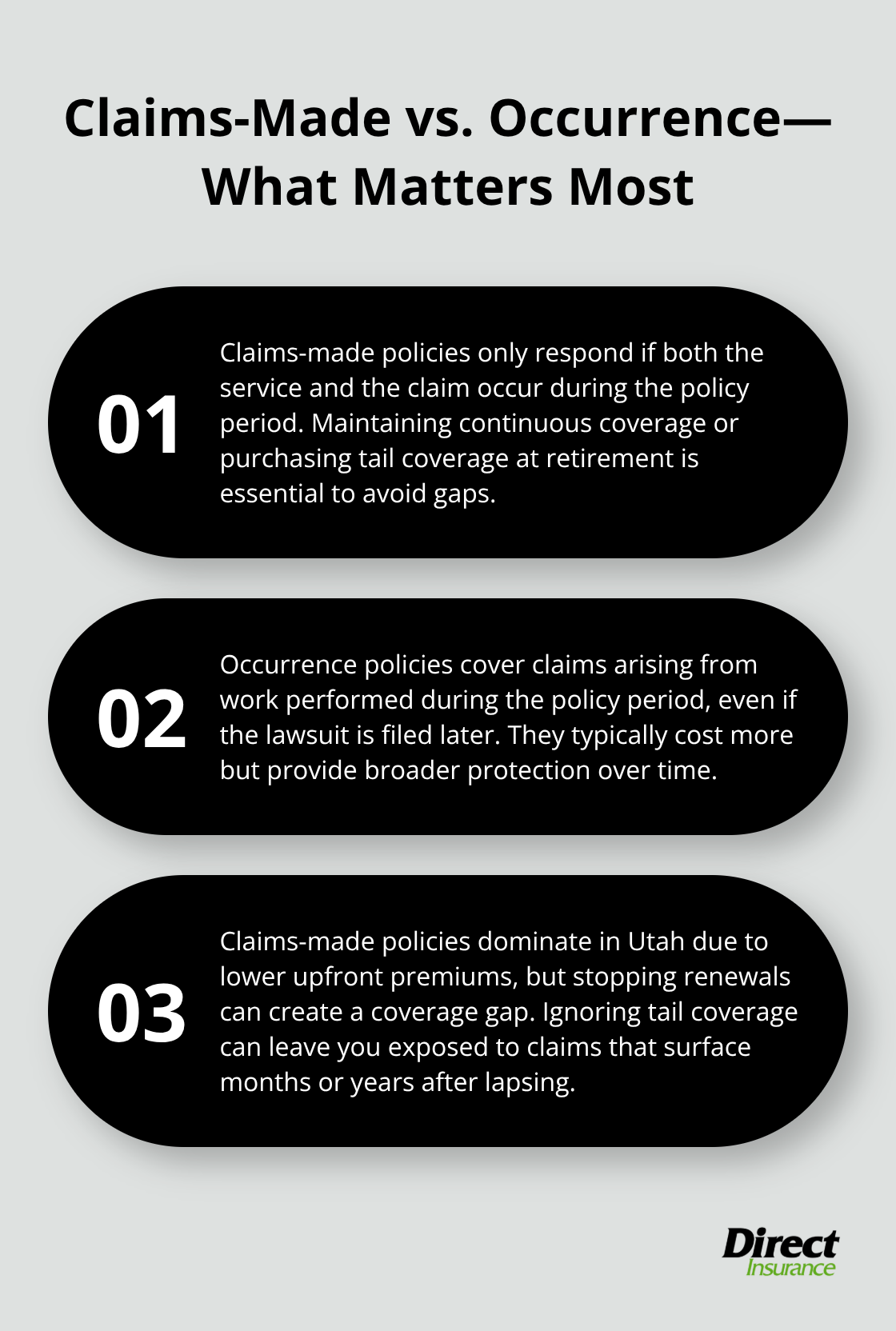

Claims-Made vs. Occurrence Policies

Claims-made policies cover claims only if both the service and the lawsuit occur during the policy period, which means you must maintain continuous coverage or purchase tail coverage when you retire. Occurrence policies cover any claim arising from work performed during the policy period, regardless of when the lawsuit is filed, and they offer broader protection but typically cost more. For Utah professionals, claims-made policies dominate the market and cost less upfront, but they create a coverage gap if you stop renewing. Many practices ignore tail coverage until it’s too late, only to discover a client claim arrives months or years after they’ve let their policy lapse.

Your choice between these structures depends on your industry, client contracts, and how long you plan to maintain your practice-factors that shape both your immediate costs and your long-term exposure.

Who Needs Professional Liability Insurance in Utah

Healthcare Providers Face Market Demands

Healthcare providers in Utah confront a hard reality: hospitals will not grant practice privileges without proof of coverage, typically $1,000,000 per occurrence and $3,000,000 aggregate. State law does not mandate this protection, but the market does. Physicians, surgeons, dentists, and mental health professionals operate in a landscape where a single misdiagnosis or treatment error triggers six-figure defense costs before any settlement occurs. OB/GYNs and surgeons pay higher premiums because their work carries greater financial risk to patients, yet they cannot practice at major facilities without this coverage. Medical malpractice insurance is essential for healthcare professionals seeking to maintain practice privileges and protect against liability claims.

Real Estate and Financial Professionals

Real estate agents encounter consistent pressure: franchise networks like RE/MAX and Coldwell Banker require proof of professional liability insurance before agents can list properties or represent clients. Banks involved in real estate transactions increasingly demand this coverage from agents, and sophisticated clients now request certificates of insurance as standard practice. Accountants, CPAs, and tax professionals working with small businesses face claims averaging $141 per month in premiums, a modest investment compared to the cost of defending a single audit error or missed deduction claim.

Contractors and Licensed Professionals

Utah’s contractor market operates under Department of Professional Licensing minimums that vary sharply by work type-$100,000 per occurrence for standard projects versus $1,000,000 per occurrence for contract work. Failure to maintain these limits puts your license at risk, not just your wallet. Software developers and IT consultants in Utah’s Silicon Slopes region should treat professional liability as non-negotiable. These professionals average $95 to $98 per month in premiums but face claims tied to data breaches, incomplete project delivery, and intellectual property disputes that grow more common each year.

Legal and Consulting Professionals

Legal professionals operate under unique pressure: Idaho and Oregon mandate professional liability insurance for attorneys, and while Utah does not, the Utah State Bar endorses ALPS as the official provider, signaling that coverage represents the professional standard. Management consultants advising small businesses on strategy or operations decisions face negligence claims when their recommendations fail, yet many carry no coverage.

The Real Requirement: Your Business Relationships

The pattern across all these professions remains identical: Utah law rarely requires coverage, but your clients, partners, and licensing bodies will demand it anyway. Your contracts and business relationships have already answered whether you need this protection. The real question becomes how to select the right policy limits and coverage structure for your specific practice.

Choosing the Right Coverage Limits for Your Utah Practice

Start with Your Contracts

Pull every client agreement, vendor contract, and employment document your practice uses before you compare any policies. Many contracts explicitly state required insurance limits-hospitals demand $1,000,000 per occurrence and $3,000,000 aggregate, real estate franchises specify minimums, and government contractors have their own thresholds. If your contracts don’t specify limits, call three practices in your field and ask what they carry.

MoneyGeek data shows contractors need $100,000 per occurrence for standard work but $1,000,000 for contract work in Utah, a tenfold difference that reflects actual market risk. Your contracts have already answered whether you need this protection; you simply need to read them.

Match Your Deductible to Your Cash Flow

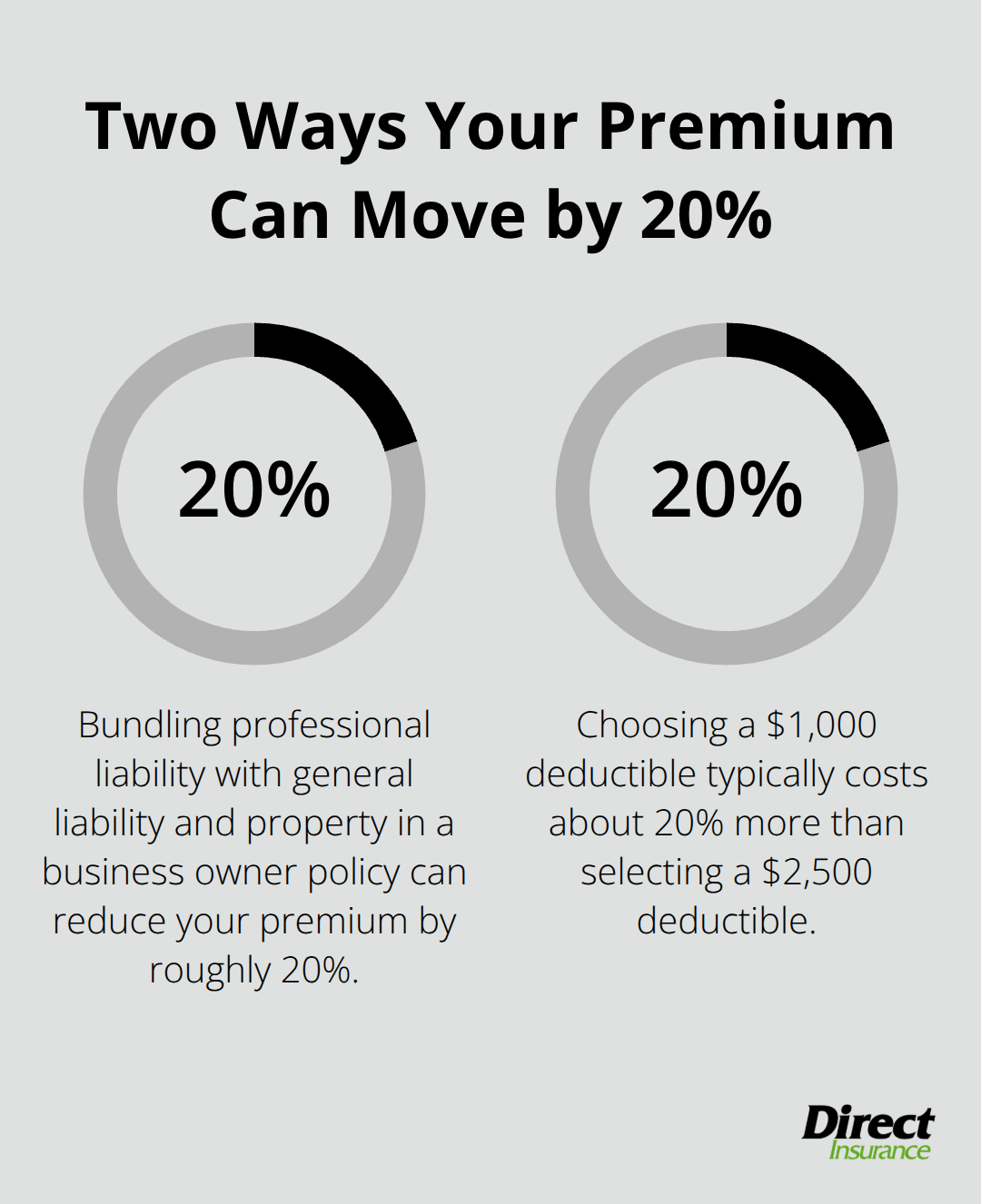

Your deductible shapes both your premium and your financial exposure. A $1,000 deductible costs roughly 20% more than a $2,500 deductible, but it also means you absorb less of the defense costs when a claim arrives. Software developers and IT consultants in Utah’s Silicon Slopes region pay $95 to $98 monthly on average; accountants pay $141 monthly. These numbers reflect industry risk, not just business size.

Surgeons and OB/GYNs pay substantially more because their work carries higher financial exposure per claim. Your cash reserves should cover your deductible without forcing you to liquidate business assets or delay operations when a claim lands.

Decide Between Claims-Made and Occurrence Coverage

Claims-made policies cover claims only if both the service and the lawsuit occur during the policy period, which means you must maintain continuous coverage or purchase tail coverage when you retire. Occurrence policies cover any claim arising from work performed during the policy period, regardless of when the lawsuit is filed, and they offer broader protection but typically cost more.

Most Utah practices choose claims-made because premiums run lower, but ignoring tail coverage costs thousands more when you eventually retire or sell your practice. Your choice determines whether you face a coverage gap years after you stop working.

Review Exclusions Before You Bind Coverage

Professional liability policies exclude intentional harm, illegal acts, services performed under another entity’s license, defamation, and discrimination claims. But professional liability insurance exclusions vary by carrier-some exclude cyber liability entirely, others bundle it in. Tech professionals should refuse any policy that excludes data breaches or project-delivery failures; these are your most common claims.

Real estate agents need coverage that explicitly includes misrepresentation claims and injuries during showings, not just negligence. Healthcare providers should verify that your policy covers the specific procedures and patient populations you serve; a policy that excludes high-risk specialties protects the insurer, not your practice. Request sample policy language from at least three carriers and compare exclusion sections directly.

Compare Carriers and Bundle for Savings

ERGO NEXT leads Utah pricing at $67 per month, The Hartford offers strong claims handling at about $68 monthly, and Simply Business provides access to 18 carriers for hard-to-insure businesses. Bundling professional liability with general liability and property coverage through a business owner policy yields roughly 20% in savings according to MoneyGeek research. Your final choice depends on whether you prioritize cost, claims support, or coverage breadth for your specific practice risk.

Final Thoughts

Your contracts and client agreements already tell you what coverage limits you need-review them before you compare any policies. Utah professional liability insurance costs between $67 and $141 per month depending on your industry, making this protection affordable for practices of any size. Match your deductible to your cash reserves, choose between claims-made and occurrence policies based on your career timeline, and read the exclusions carefully to verify your policy actually protects you against your most common claims.

Bundling professional liability with general liability and property coverage saves roughly 20% on your total premium. Compare quotes from multiple carriers, prioritize claims support and exclusion language over price alone, and verify that your final policy matches your actual business exposure. Utah’s professional landscape demands this protection regardless of what state law requires.

We at Direct Insurance Services understand the specific risks Utah professionals face because we’ve served this community since 1973. Contact us today to discuss your professional liability needs and secure the protection your practice deserves.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation