Does Home Insurance Cover Mold?

Mold in your home is a serious problem, but the answer to whether home insurance covers mold isn’t straightforward. Most standard policies exclude mold damage entirely, leaving homeowners vulnerable to expensive repairs.

At Direct Insurance Services, we’ve seen countless claims denied because policyholders didn’t understand their coverage limits. The good news is that you can take steps to protect your home and fill gaps in your protection.

When Home Insurance Actually Covers Mold

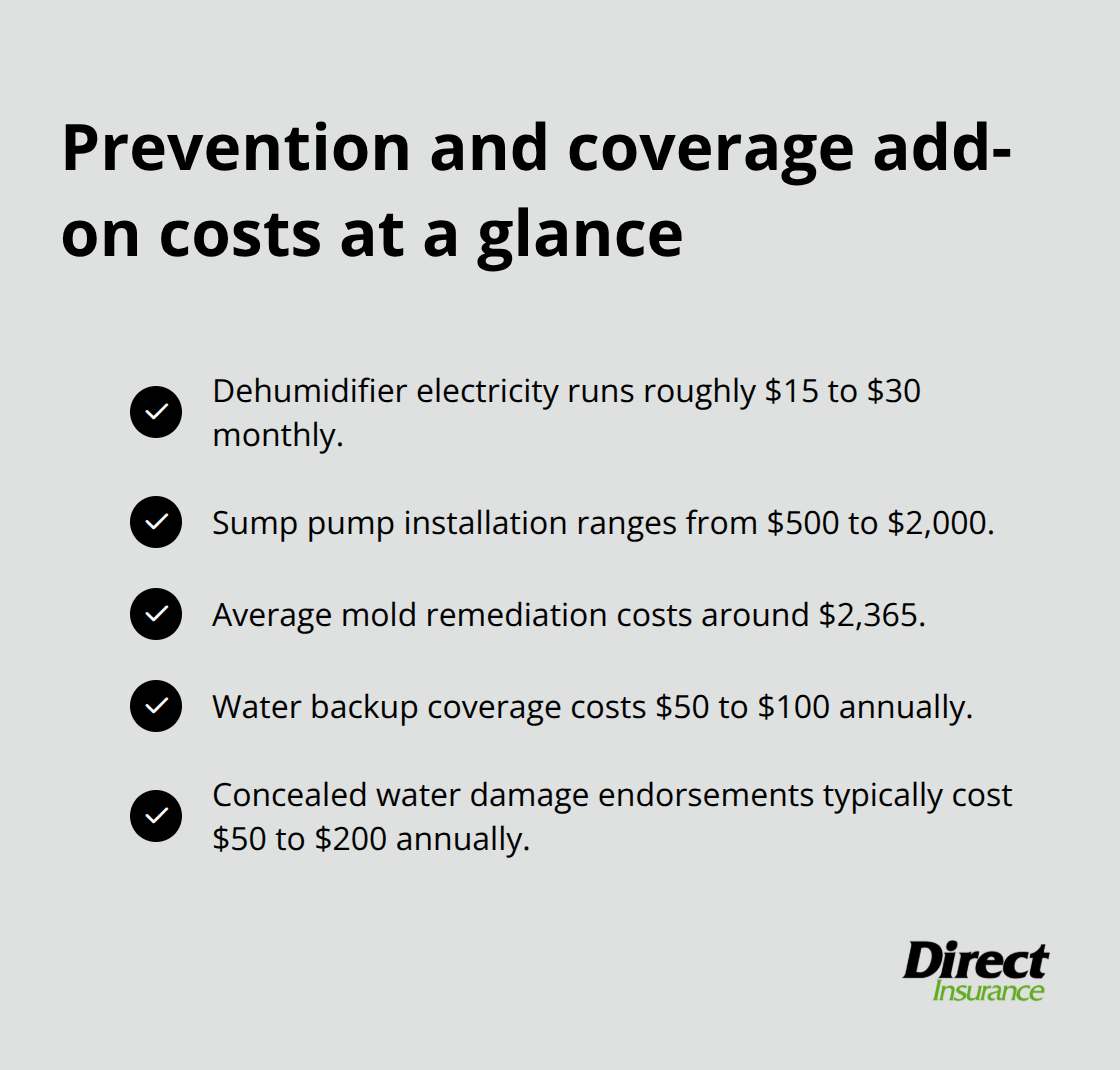

Your standard homeowners policy covers mold only when it results from a sudden, unexpected event that the policy itself covers. This is the critical distinction most homeowners miss. If a pipe bursts and water floods your basement, and mold develops within days, you likely have coverage for the mold remediation. The same applies to sudden toilet overflows, failed water heaters, or fire damage extinguished with hose water. According to Angi data, average mold remediation costs around $2,365, with projects typically ranging from $373 to $7,000 depending on the affected area. When coverage applies, your insurer may cover these remediation costs up to your policy limits after you pay your deductible.

What Triggers Actual Coverage

The peril itself must be covered under your policy for mold coverage to activate. Most standard policies are all-risk policies, meaning they cover sudden damage unless specifically excluded. This works in your favor for sudden water events. However, the moment mold develops from ongoing moisture, poor ventilation, or a slow leak you neglected to fix, coverage disappears entirely. The first 48 hours after water damage are critical for preventing mold growth. If you ignore a damp basement for weeks, your insurer will deny the claim because the mold resulted from your inaction, not a covered peril. This is why acting quickly matters more than most homeowners realize.

Coverage Limits Create Real Gaps

Even when mold is covered, your policy includes specific limits on how much the insurer will pay. Many policies cap mold coverage at $5,000 or $10,000 per claim, according to guidance from state regulators examining minimum coverage standards. If your remediation bill reaches $8,000 and your limit is $5,000, you pay the remaining $3,000 out of pocket.

Some policies exclude mold entirely unless you purchase an optional mold damage rider. Water backup coverage and concealed water damage endorsements can extend your protection, but they cost extra. Most homeowners discover these limitations only after filing a claim, which is too late. You need to review your declarations page now to understand whether mold is excluded, capped, or covered without restrictions.

Additional Coverage Options Worth Exploring

Water backup coverage protects you when sewer backups or sump pump failures allow water to enter your home and create mold conditions. Concealed water damage endorsements cover mold that results from hidden leaks inside walls or under floors (areas you cannot see until damage appears). These add-ons vary by insurer and state, so contact your agent to learn what options apply to your specific policy. Some insurers offer standalone mold policies or higher mold limits for an additional premium. The cost of these endorsements typically ranges from $50 to $200 annually, far less than the thousands you might spend on remediation. Comparing these costs against potential out-of-pocket expenses makes the decision straightforward for most homeowners.

Understanding what your policy covers sets the foundation for protection, but coverage alone won’t prevent mold from taking hold in your home. What you do in the days and weeks after water damage occurs determines whether mold ever becomes a problem at all.

Why Insurers Won’t Pay for Mold You Could Have Prevented

Insurance exists to cover unexpected disasters, not problems you create through inaction. This is why mold falls outside standard coverage so consistently. When mold develops because you ignored a slow leak under your sink, failed to fix a roof that has been dripping for months, or never ran a dehumidifier in your damp basement, your insurer views this as negligence on your part, not a covered loss. The distinction matters legally and financially.

Maintenance Failures Trigger Claim Denials

Insurers argue that homeowners have a responsibility to maintain their properties and address moisture issues as they arise. A leaky faucet that drips for weeks before you fix it creates the exact conditions for mold growth, and the insurer will not pay for damage that stems from your delay. This isn’t harsh policy language-it’s fundamental to how insurance works. You pay premiums to protect against sudden, unforeseeable events, not to cover damage from maintenance failures you could have prevented.

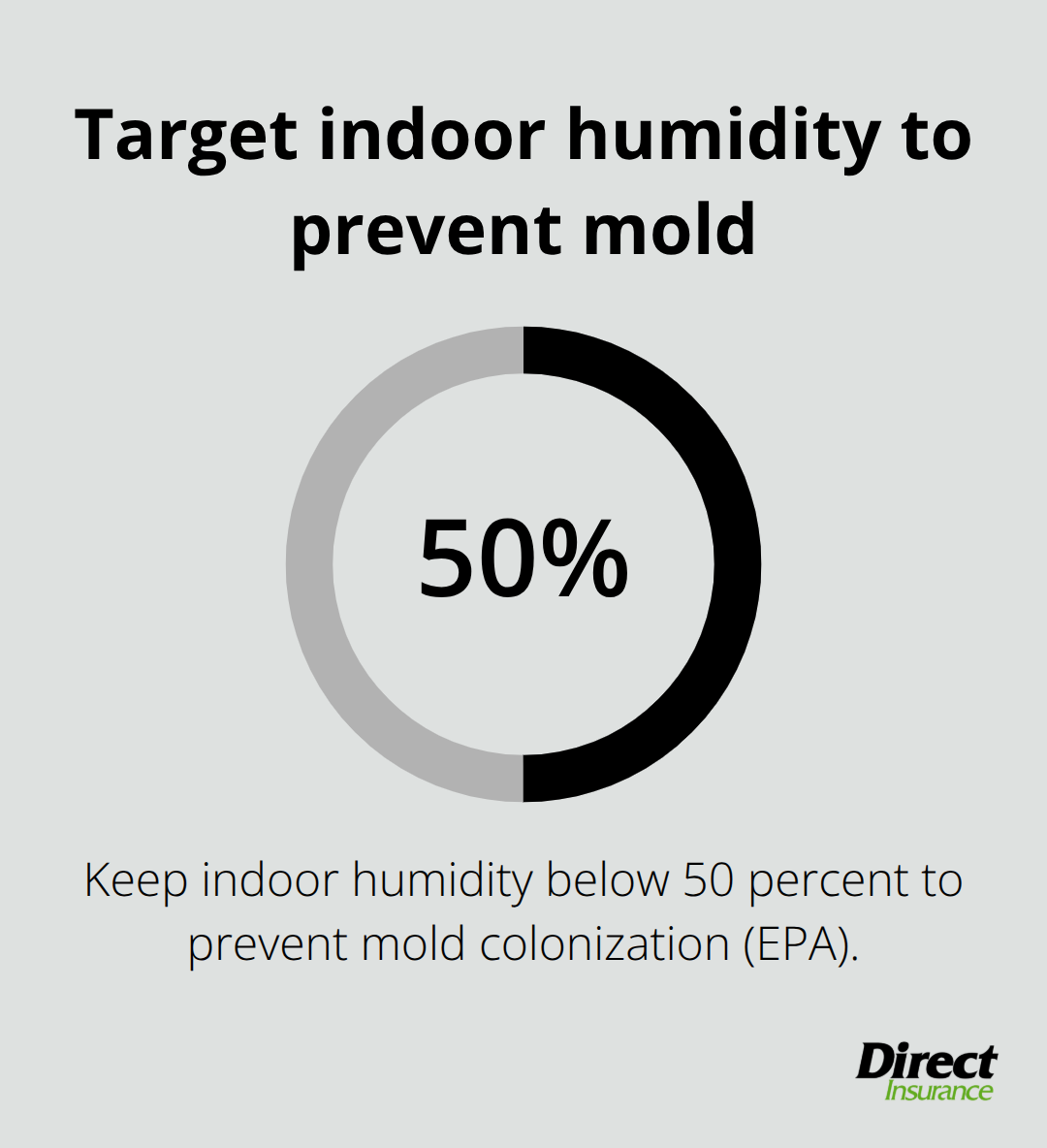

The EPA recommends addressing any water intrusion within 24-48 hours to prevent mold colonization, which means homeowners have a clear, achievable window to act. If you miss that window, the responsibility shifts entirely to you. Your policy covers the burst pipe; it does not cover the mold that develops because you never inspected your basement for water intrusion or invested in proper drainage.

Long-Term Moisture Problems Fall on You

Long-term moisture problems represent the largest category of denied mold claims, and insurers treat them as maintenance issues rather than insurable losses. Condensation that builds up on basement walls over months, poor ventilation in bathrooms that creates persistent humidity, or gutters clogged with debris that allows water to seep into your foundation all fall into this category. These aren’t sudden events-they’re conditions you can observe and correct with routine home maintenance.

Insurers have data showing that most mold claims result from ongoing moisture buildup rather than single catastrophic events, which reinforces their position that prevention lies within your control. The cost of preventive measures-a dehumidifier running 24/7 costs roughly $15 to $30 monthly in electricity, and a sump pump installation ranges from $500 to $2,000-is far less than typical remediation expenses. Insurers view homeowners who fail to invest in these protections as accepting the risk themselves.

Your Choices Determine Your Exposure

If you live in a flood-prone area or your basement tends toward dampness, you’re essentially choosing to bear the mold risk when you refuse to address underlying moisture conditions. The next section covers the specific steps that protect your home and strengthen your insurance position when water damage does occur.

How to Protect Your Home and Improve Coverage

Act Within 48 Hours of Water Damage

The most effective mold prevention strategy starts the moment water enters your home. You cannot afford to wait and see if mold develops over the next few weeks. The first 24 to 48 hours after water intrusion determine whether mold takes hold or gets stopped entirely. If a pipe bursts, a toilet overflows, or your washing machine hose fails, your immediate response decides your insurance claim outcome and your home’s condition.

Stop the water source first, then dry everything aggressively. Run dehumidifiers, open windows if weather permits, and use fans to force air circulation through affected areas. Pull up wet carpet, move furniture away from walls, and remove wet drywall if saturation reaches more than a few inches up the wall. Document every step with photos and timestamps because your insurer will want proof that you acted decisively. If you delay drying by even three days, mold colonies begin forming, and insurers will argue you failed to mitigate damage, which can reduce or eliminate coverage entirely.

Control Moisture in High-Risk Areas

Basements and bathrooms create persistent moisture problems that lead to claim denials because they represent ongoing conditions you can address through maintenance. Install a dehumidifier in your basement and keep indoor humidity below 50 percent; the EPA recommends this threshold specifically to prevent mold colonization. A mid-range dehumidifier costs $200 to $400 and runs roughly $15 to $30 monthly in electricity, yet prevents remediation bills exceeding $2,000.

Check your gutters quarterly and ensure downspouts direct water at least four to six feet away from your foundation. Clogged gutters cause water to seep into your home’s structure, creating the exact conditions insurers cite when denying mold claims. Inspect under sinks, around water heater connections, and behind washing machines monthly-these areas develop slow leaks that homeowners miss until mold appears. Repair dripping faucets and leaking supply lines immediately; a dripping faucet costs roughly $35 to fix but creates mold conditions if ignored for weeks.

If your basement floods regularly or your foundation shows signs of water intrusion, install a sump pump system, which ranges from $500 to $2,000 installed. This single investment demonstrates to insurers that you take moisture prevention seriously and can be the difference between coverage approval and denial when water damage occurs. Add water backup coverage to your policy, which costs $50 to $100 annually and covers mold resulting from sewer backups or sump pump failures. This endorsement closes a major coverage gap for homeowners in areas prone to heavy rainfall or aging municipal sewer systems.

Build a Maintenance Record That Strengthens Claims

Photograph your home’s condition quarterly, focusing on areas prone to moisture like basements, crawlspaces, and bathroom corners. Take photos of your gutters, foundation, and grading around your home’s perimeter. Keep receipts for any maintenance work you complete-gutter cleaning, sump pump installation, dehumidifier purchases, roof repairs, or plumbing fixes. Store these records digitally in cloud storage so they survive home disasters.

When you file a mold claim, insurers scrutinize whether you maintained the property responsibly. Proof that you invested in preventive measures and addressed water issues promptly strengthens your position significantly. If an adjuster questions whether the mold resulted from your negligence, you can demonstrate a pattern of responsible maintenance. Conversely, if you have no documentation of maintenance efforts, the insurer assumes you neglected the property and denies the claim.

This documentation also matters when you purchase additional coverage or seek quotes from other insurers. When agents review your maintenance history, they gain confidence in your ability to prevent future losses, which can result in better rates and higher coverage limits. Some insurers offer modest premium discounts for homeowners who install moisture control systems or maintain documented maintenance records, though you must ask about these discounts specifically-they are rarely advertised.

Final Thoughts

The answer to whether home insurance covers mold remains straightforward: standard policies cover mold only when a sudden, covered peril like a burst pipe or failed water heater causes it, and even then, coverage limits often fall short of actual remediation costs. Mold from maintenance failures, long-term moisture, or negligence stays your financial responsibility entirely. This reality makes prevention and maintenance your primary defense strategy against expensive damage.

The steps outlined in this guide work because they address mold at its source before it becomes a claim. Acting within 48 hours of water damage, controlling moisture in basements and bathrooms, and maintaining detailed records of your preventive efforts protect your home’s structure and health while positioning you favorably if a covered water event occurs. Insurers reward homeowners who demonstrate responsibility through documented maintenance and swift action after water intrusion.

Contact your insurance agent and ask specifically about water backup coverage and concealed water damage endorsements-these add-ons cost between $50 and $200 annually but can mean the difference between a covered claim and thousands in out-of-pocket expenses. If your current insurer cannot offer the protection you need, we at Direct Insurance Services shop multiple top-rated insurance companies to find coverage that matches your home’s specific risks. Contact Direct Insurance Services to discuss your mold coverage options with a local agent who understands Utah’s unique moisture challenges.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation