Home Insurance Comparison Made Simple

Home insurance can feel overwhelming when you’re comparing policies and trying to understand what actually protects your property. The good news is that a home insurance comparison doesn’t have to be complicated.

We at Direct Insurance Services help homeowners cut through the confusion by breaking down coverage types, rate factors, and comparison strategies into simple steps. This guide walks you through everything you need to make an informed decision.

Understanding Home Insurance Coverage Types

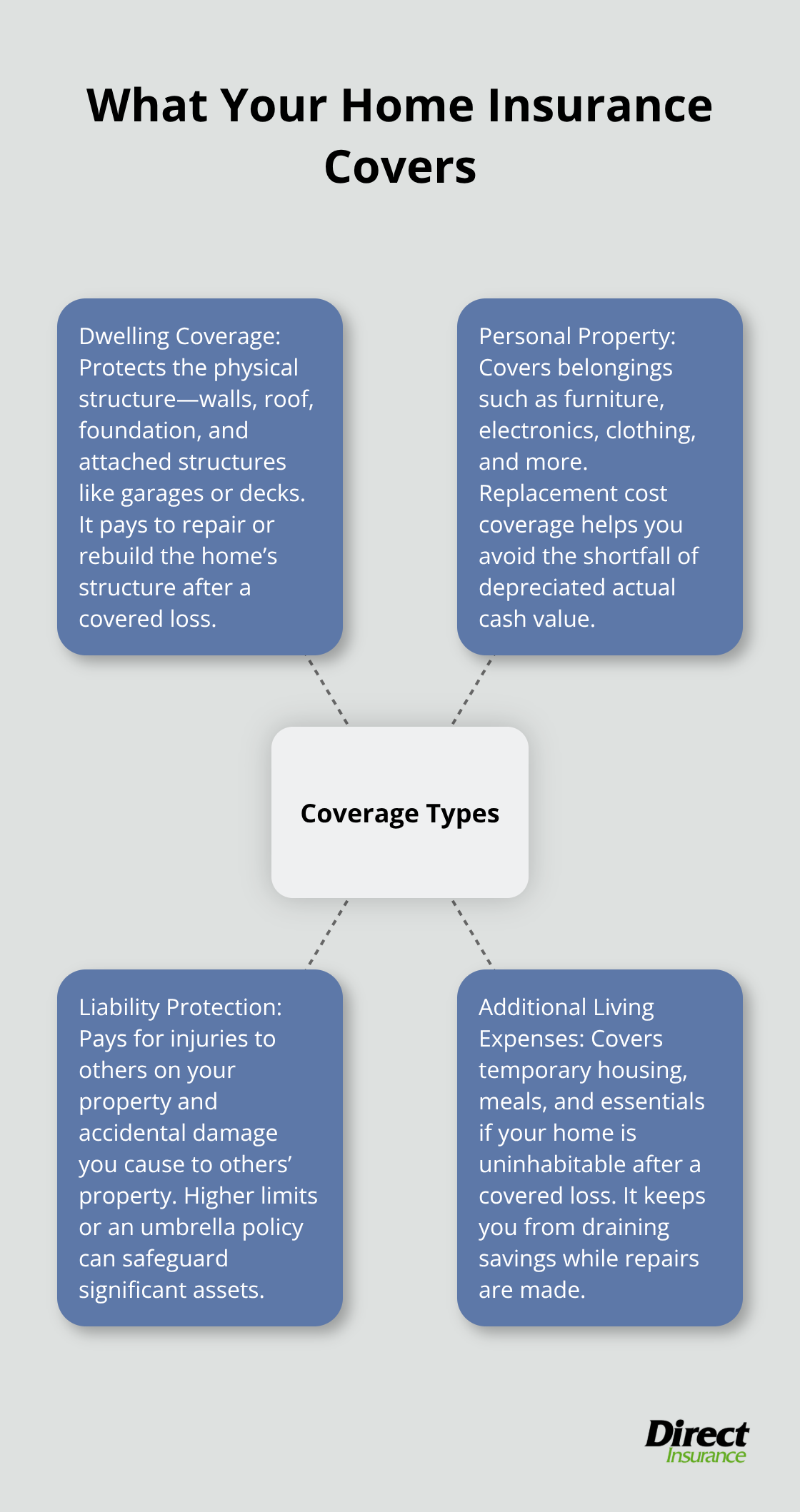

Dwelling Coverage: Protecting Your Home’s Structure

Dwelling coverage protects the structure itself-your walls, roof, foundation, built-in appliances, and attached structures like garages or decks. Many homeowners mistakenly believe dwelling coverage protects everything inside their home, but it only covers the building itself. If a fire damages your home’s frame or a storm tears off your roof, dwelling coverage pays to rebuild or repair those structural elements.

Your dwelling coverage limit must match your home’s replacement cost, not its market value. If your home would cost $450,000 to rebuild today but you only have $300,000 in dwelling coverage, you’ll face a significant gap when you file a claim. Many lenders require at least 80% of replacement cost coverage, but try for full replacement cost to avoid underinsurance.

Personal Property Coverage: Protecting Your Belongings

Personal property coverage protects your belongings inside the home-furniture, electronics, clothing, and other possessions. This coverage typically pays the replacement cost of your items, which matters because actual cash value (the depreciated amount) often falls far short of what you’d spend to replace things.

Standard policies come with sub-limits on specific items like jewelry, cameras, or collectibles. If you own a watch worth $8,000 or artwork worth $15,000, your standard policy might only cover $1,500 of that value. You’ll need to add scheduled personal property endorsements to cover high-value items properly.

Liability Protection: Covering Injuries and Damage Claims

Liability protection covers you when someone is injured on your property or when you accidentally damage someone else’s property. A basic homeowners policy typically includes $100,000 to $300,000 in liability coverage, but if you have significant assets or a swimming pool, that limit is dangerously low. Legal judgments for serious injuries regularly exceed $500,000, which is why umbrella liability insurance starting at $1 million makes sense-it costs only a few hundred dollars annually and protects you beyond your homeowners policy limits.

Additional Living Expenses: Covering Temporary Housing

Additional living expenses coverage pays for temporary housing, meals, and essentials if your home becomes uninhabitable after a covered loss. This coverage is often overlooked but genuinely matters. If a fire forces you out for six months while your home is rebuilt, your insurer covers your hotel, restaurant meals, and other temporary living costs rather than forcing you to drain your savings.

Now that you understand what each coverage type protects, the next step is recognizing which factors actually drive your insurance rates up or down-and why your location and home characteristics matter far more than you might think.

Key Factors That Affect Your Home Insurance Rates

Location and Climate Risk in Utah

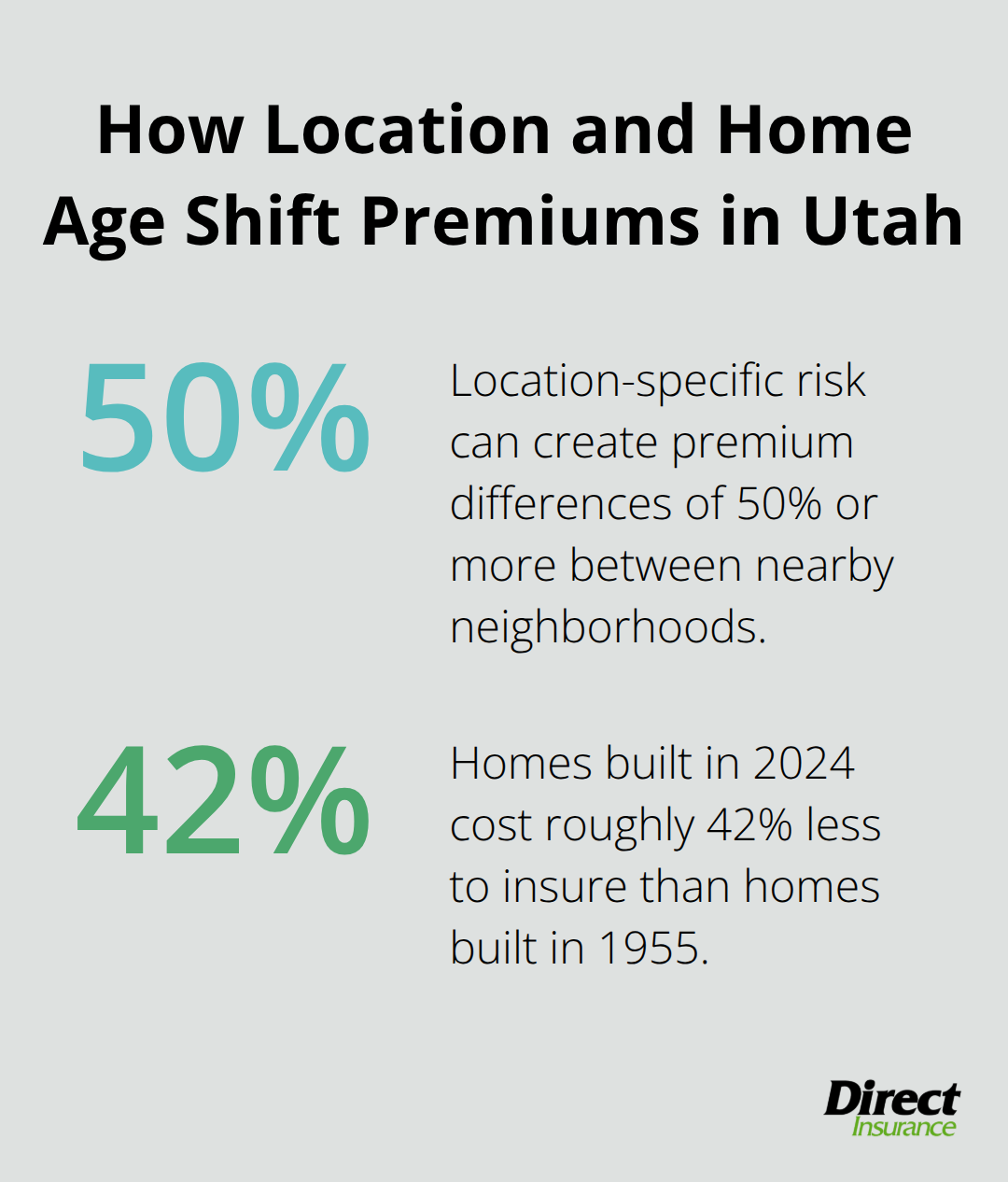

Your location in Utah matters more than almost any other factor when determining your home insurance premium. Utah’s climate brings distinct risks that insurers price accordingly. While Utah generally avoids the extreme hurricane and flood zones that plague coastal states, wildfire risk has become increasingly serious in recent years. The state experiences significant wind events, hail damage, and occasional severe winter weather that push premiums higher in mountain communities and rural areas prone to wildfires. The Zebra reports that location-specific risk assessment is the strongest predictor of your final rate, often creating premium differences of 50% or more between neighborhoods just miles apart.

If you live in a wildfire-prone area near Park City, Ogden, or the Wasatch Front, you’ll pay substantially more than someone in Salt Lake City’s urban core.

Home Age, Size, and Construction Materials

Your home’s age and construction directly impact what insurers charge. Newer homes built with modern materials and updated electrical, plumbing, and roofing systems cost significantly less to insure because they present lower risk of damage and cost less to repair. A home built in 2024 costs roughly 42% less to insure than a home built in 1955, according to NerdWallet’s analysis. Homes built before 1980 often require additional scrutiny for outdated wiring or plumbing that increases claim likelihood.

Larger homes naturally cost more to insure because they contain more property to protect and cost more to rebuild, but the relationship isn’t linear-a 4,000-square-foot home doesn’t cost twice as much to insure as a 2,000-square-foot home. Construction materials matter significantly: wood-frame homes cost more to insure than concrete or steel construction because they’re more vulnerable to fire and weather damage.

Your Claims History and Credit Score

Your claims history and credit score are the two financial factors that most directly affect your rates, and both are entirely within your control. The Zebra reports that filing even one claim raises your annual premium by roughly 9%, and multiple claims can trigger nonrenewal or rate increases of 20% or more. This doesn’t mean you should avoid filing legitimate claims, but it does mean you should carefully evaluate small losses before submitting them to your insurer.

Credit score creates the most dramatic rate difference: homeowners with poor credit pay an average of 137 percent more for home insurance than homeowners with excellent credit. Improving your credit score by even one tier can save approximately 32% on premiums. Utah allows credit scores in insurance pricing, so your financial responsibility directly translates to lower insurance costs. Review your credit report annually and address errors before shopping for insurance. Payment history, credit utilization, and overall debt levels all factor into your score. If your credit needs improvement, focusing on that challenge over the next six to twelve months will yield far greater savings than negotiating premium discounts.

Rising Construction Costs and Coverage Limits

Building costs have surged dramatically since 2019, with construction labor costs rising approximately 40% and materials rising about 40% according to the U.S. Bureau of Labor Statistics. This explains why dwelling coverage limits require regular reassessment rather than remaining static. As rebuild costs climb, your coverage limits must climb with them to protect against underinsurance. Understanding these rate drivers positions you to make smarter decisions when you compare quotes-and that’s where the real work of finding the right policy begins.

How to Compare Home Insurance Quotes Effectively

Match Coverage Limits Across All Quotes

Comparing home insurance quotes requires discipline. Most homeowners grab three quotes, glance at the premium prices, and pick the cheapest option-then wonder why their coverage falls apart when they file a claim. The real comparison happens when you strip away the marketing language and look at what you’re actually buying.

Request quotes with identical dwelling coverage limits, personal property amounts, and liability protection across all insurers. If one quote shows $300,000 dwelling coverage and another shows $350,000, you’re not comparing apples to apples, and the premium difference tells you nothing useful. Contact insurers directly or work with an independent agent who can pull quotes with matching specifications. This takes an extra twenty minutes but prevents catastrophic mistakes.

Evaluate Deductible Choices and Premium Impact

Deductible choice creates massive premium swings that most homeowners overlook. Moving from a $1,000 deductible to a $2,500 deductible typically saves around 12 percent on your annual premium according to NerdWallet data. That translates to roughly $250 to $400 yearly, but you need to honestly assess what you can afford if a claim happens.

A $2,500 deductible saves money upfront, but if a hail storm damages your roof and you face a $5,000 repair bill, that deductible becomes painful. The math only works if you have emergency savings to cover the higher out-of-pocket cost. Once you’ve matched coverage and deductibles across quotes, the real work of evaluation begins.

Assess Claims Handling and Financial Strength

Examine the insurer’s actual track record with customers. Consumer Reports surveyed nearly 24,000 homeowners about their claims experiences, and claims handling speed ranked second only to premium level in determining satisfaction. Check how quickly each insurer responds to claim calls, whether they offer online claim filing, and what percentage of claims get approved without disputes.

An insurer charging $50 more annually but processing claims in three days instead of two weeks delivers better value than saving that $50 and fighting bureaucracy when you need help. Look up each company’s financial strength rating through A.M. Best to confirm they can actually pay claims when disasters hit. This verification step separates insurers that will stand behind their promises from those that might struggle during major claim periods.

Final Thoughts

Home insurance comparison requires matching coverage limits across all quotes to prevent underinsurance mistakes that cost you thousands when claims happen. Your deductible choice creates real premium swings-moving from $1,000 to $2,500 typically saves around 12 percent annually-so balance the upfront savings against what you can actually afford out-of-pocket after a loss. Claims handling speed and financial strength matter more than premium alone because an insurer’s actual performance during a loss determines whether your coverage delivers real protection.

Location, home age, and construction materials drive your rates far more than negotiating discounts ever will. Your claims history and credit score represent the two factors entirely within your control, and improving either one delivers savings that dwarf any premium negotiation. Understanding these rate drivers positions you to make smarter decisions when you compare quotes and avoid the trap of selecting coverage based solely on price.

We at Direct Insurance Services shop multiple top-rated insurance companies to find coverage that actually fits your Utah home and budget. Our independent agents understand Utah’s unique wildfire risks and weather patterns, and we’ve helped local homeowners navigate these decisions since 1973. Contact us today to start your home insurance comparison with an agent who knows your community.