Complete Auto Insurance Coverage Benefits

Most drivers think basic auto insurance is enough. But one accident or lawsuit can expose gaps that leave you financially vulnerable.

At Direct Insurance Services, we’ve seen how complete auto insurance coverage protects what matters most. This guide shows you exactly what full coverage includes and why it’s worth the investment.

What Complete Coverage Actually Protects

Complete auto insurance coverage combines several layers of protection that work together to cover both your liability and your vehicle. Liability coverage is mandatory in nearly every state and covers damages or injuries you cause to others-this is non-negotiable. Most states require minimum liability limits, but these minimums are dangerously low. According to the Insurance Information Institute, many states set limits around 25/50/25, meaning $25,000 per person and $50,000 per accident for bodily injury, plus $25,000 for property damage. A single serious accident with multiple injuries can exceed these limits in minutes. Medical costs have surged, with bodily injury claim severity rising 9.2% year-over-year according to the LexisNexis Risk Solutions 2025 U.S. Auto Insurance Trends Report. If you cause an accident that injures multiple people, you become personally liable for amounts beyond your policy limits. Your wages, home, and savings face vulnerability. Higher liability limits cost only slightly more-increasing from minimum coverage to 100/300/100 might add just $10–20 monthly to your premium, but it protects substantially more of your assets.

Collision and Comprehensive Fill Critical Gaps

Collision coverage pays for damage to your own vehicle after a crash, regardless of fault, minus your deductible. Comprehensive coverage protects against theft, fire, weather, vandalism, and other non-collision events. If you financed or leased your vehicle, your lender requires both. Even if you own your car outright, skipping these coverages means you pay full replacement costs from your own pocket. For a vehicle worth $15,000, a collision claim could mean $12,000–14,000 out-of-pocket after your deductible. Property damage severity climbed 2.5% year-over-year, reflecting rising repair costs from advanced vehicle technology. Modern cars cost significantly more to repair than older models. Raising your deductible from $200 to $500 can cut your collision and comprehensive premiums by 15–30%, according to the Insurance Information Institute-a practical way to lower costs while maintaining protection.

Gap insurance adds another layer by covering the difference between your loan balance and your car’s actual cash value if it’s totaled (critical if you financed a newer vehicle or made a small down payment).

Uninsured Drivers Are More Common Than You Think

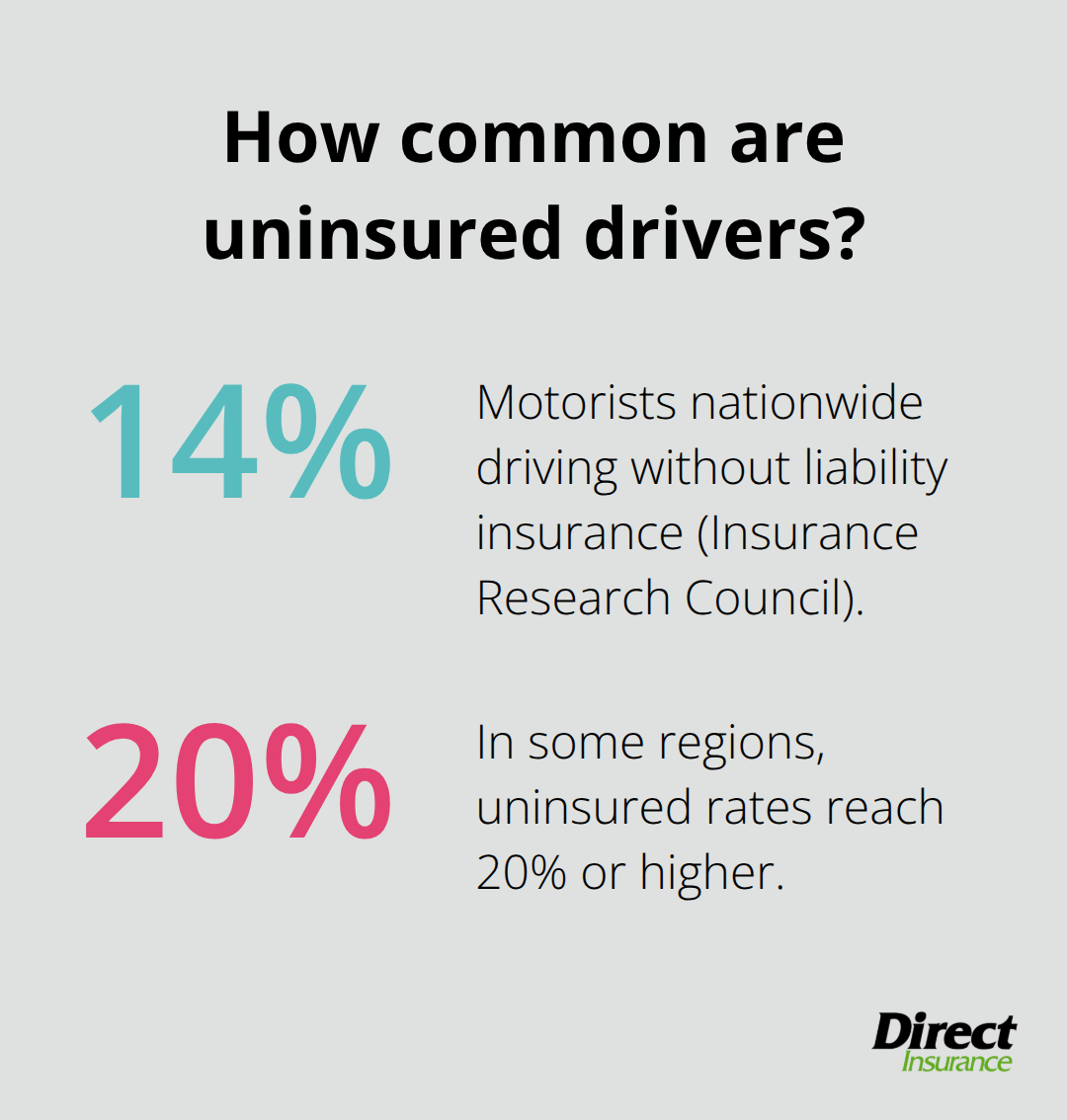

About 14% of motorists drive without liability insurance, according to the Insurance Research Council. In some regions, this number reaches 20% or higher. If an uninsured driver causes an accident, your collision coverage pays for your vehicle, but uninsured motorist coverage protects you financially for injuries and damages that driver should have covered. Underinsured motorist coverage kicks in when the at-fault driver’s liability limits don’t cover your actual damages-especially important given rising medical costs.

Utah law doesn’t mandate uninsured motorist coverage, but choosing to skip it creates serious financial risk. Most insurers allow you to set UM/UIM limits to match your liability limits, which costs very little but protects you completely. Without these coverages, you pay your own medical bills, lost wages, and vehicle repairs when hit by an uninsured or underinsured driver (even though you caused nothing wrong).

Why These Gaps Matter on Utah Roads

Utah’s weather patterns and driving conditions create specific risks that basic coverage doesn’t address. Hail storms, flash floods, and winter weather cause comprehensive claims regularly. Uninsured motorist rates vary across Utah counties, with some areas experiencing higher rates than others. Complete coverage accounts for these regional realities and protects you against the accidents most likely to happen where you live and drive. Understanding what each coverage layer does positions you to make informed decisions about your protection level and cost.

Why Complete Coverage Protects Your Financial Future

Medical Bills and Liability Limits Collide Fast

One accident exposes how quickly inadequate coverage becomes catastrophically expensive. When you cause an accident with multiple injuries, medical bills accumulate faster than most people realize. A single serious injury requiring surgery, hospitalization, and ongoing rehabilitation costs $100,000–$500,000 or more. If your liability limits sit at the state minimum of 25/50/25, you become personally responsible for everything above those thresholds. Your paycheck gets garnished. Your home becomes vulnerable to a judgment lien. Your savings disappear. Higher liability limits eliminate this risk entirely. Jumping from minimum coverage to 100/300/100 costs roughly $10–20 extra per month but shields your assets completely from medical cost inflation.

Vehicle Repair Costs Demand Collision and Comprehensive

Collision and comprehensive coverage protect your vehicle replacement costs with equal urgency. Modern vehicles with advanced safety technology and infotainment systems cost significantly more to repair than older cars. A $25,000 vehicle damaged in a collision could require $18,000–22,000 in repairs depending on parts availability and labor. Without collision coverage, you pay that entire amount yourself. Comprehensive coverage handles the scenarios you cannot control: a hailstorm in Utah’s spring season damages your roof and windshield, theft strips your car in a parking lot, or flash flooding totals your vehicle. These events happen regularly in Utah, and comprehensive claims have become increasingly common. Skipping comprehensive in Utah is financially reckless.

Gap insurance bridges another critical gap most drivers overlook. If you financed your vehicle with a small down payment and it gets totaled within the first few years, you owe more on the loan than the insurance company pays for the car’s actual cash value. Gap insurance covers that difference, preventing you from paying thousands for a vehicle you no longer own.

Uninsured Drivers Create Unexpected Financial Exposure

Uninsured motorist coverage addresses a reality that catches too many Utah drivers unprepared. Roughly 14% of motorists nationwide drive without liability insurance, and some regions experience rates above 20%. When an uninsured driver hits you, your collision coverage pays for vehicle repairs, but nothing covers your medical bills, lost wages, or pain and suffering unless you have uninsured motorist coverage. Underinsured motorist coverage extends this protection when the at-fault driver’s liability limits fall short of your actual damages, which happens frequently given rising medical costs. Utah doesn’t mandate these coverages, but that legal permission masks a dangerous gap. Most insurers let you set UM/UIM limits matching your liability limits for minimal additional cost, yet many drivers skip this protection entirely. If you’re injured by an uninsured driver and lack this coverage, you file a claim against your own health insurance with higher deductibles and copays, or you absorb the costs completely.

Legal Defense Costs Mount Without Adequate Coverage

Complete coverage also provides legal protection that extends beyond accident claims. When someone sues you for injuries or damages from a collision you caused, your liability coverage pays for your legal defense and settlement or judgment up to your policy limits. Without adequate limits, you hire your own attorney at $200–400 hourly rates and negotiate settlements from your personal funds. Adequate coverage means your insurer handles the legal process, protecting both your finances and your time.

Utah’s Weather and Regional Risks Demand Complete Protection

Driving Utah roads creates weather-specific and regional risks that demand coverage matching those conditions. Winter weather causes collision and comprehensive claims regularly. When rain, snow, or ice covers Utah roads, your tires grip the road 70% less, meaning your car needs almost three times more distance to stop. Uninsured motorist rates vary significantly across Utah counties, making complete coverage essential in higher-risk areas. Complete coverage accounts for these Utah-specific realities rather than relying on one-size-fits-all minimum state requirements. Understanding your actual exposure in your specific Utah location positions you to make informed decisions about protection levels that match your real risk-not just legal minimums.

Common Gaps in Auto Insurance Policies

Most drivers never read their declarations page until after a loss. The problem isn’t what your policy covers-it’s what it deliberately doesn’t. Standard auto insurance excludes intentional damage, mechanical breakdown, normal wear and tear, and damage from racing or off-road use. But these obvious exclusions aren’t what catches people unprepared. The real gaps emerge in specific scenarios that feel like they should be covered but aren’t.

Rideshare and Commercial Activity Exclusions

Rideshare drivers face massive coverage holes because standard personal auto policies exclude income-generating activities. If you drive for Uber or Lyft without rideshare coverage, you have zero protection while the app is active and you’re waiting for passengers. Insurify’s 2024 rideshare analysis found that rideshare drivers pay roughly $270 monthly for proper coverage versus $211 for standard drivers-but without it, a single accident during a rideshare trip leaves you completely uninsured and personally liable for everything. Similarly, if you transport people for compensation outside of rideshare platforms, your personal auto policy excludes that activity entirely. Commercial auto insurance costs $200-500 annually but prevents gaps when personal policies exclude business use.

Limited Reimbursement and Towing Gaps

Rental car reimbursement sounds like it covers your rental costs, but it actually caps daily reimbursement at specific limits, usually $30–50 per day. If you rent a vehicle that costs $75 daily while your car is being repaired, you pay the difference from your pocket. Roadside assistance sounds basic until you need a tow from Salt Lake City to Moab and discover your policy covers only 10 miles. Extended towing endorsements cost minimal amounts but prevent $500+ out-of-pocket towing bills in Utah’s remote areas.

Coverage Limits That Fall Short of Real Costs

Your policy limits are where most drivers discover their coverage was dangerously low. A $100,000 bodily injury limit per person sounds substantial until one passenger requires $200,000 in medical care from a single accident. Utah doesn’t mandate uninsured motorist coverage, so many drivers skip it entirely and then face medical bills from their own health insurance when an uninsured driver injures them. Medical payments coverage and PIP serve different purposes-your PIP covers lost wages at 60–80% of income, while medical payments covers actual medical bills. Without both, you cover wage loss from your savings.

Classic or collector vehicle owners face the harshest exclusions because standard policies treat a 1967 Chevelle like a 2024 Civic, paying actual cash value rather than the agreed-upon value that reflects what that vehicle is actually worth. If your collector car is valued at $45,000 and your standard policy pays only $18,000 actual cash value, you lose $27,000. Specialized collector car policies cost more but prevent this catastrophic underinsurance. New vehicle owners often skip new car replacement coverage, thinking full coverage is sufficient. If your brand-new $38,000 vehicle is totaled within the first year, your insurer pays depreciated value-roughly $32,000-leaving you $6,000 short if you finance a replacement. New car replacement coverage costs roughly $150–200 annually but covers that gap completely. The Insurance Information Institute notes that deductible choices directly impact what you actually pay in a claim. A $500 deductible means you pay $500 out-of-pocket; a $1,000 deductible means you pay $1,000. Many drivers choose deductibles they cannot actually afford to pay, creating a false sense of coverage.

Identifying Missing Protection in Your Current Policy

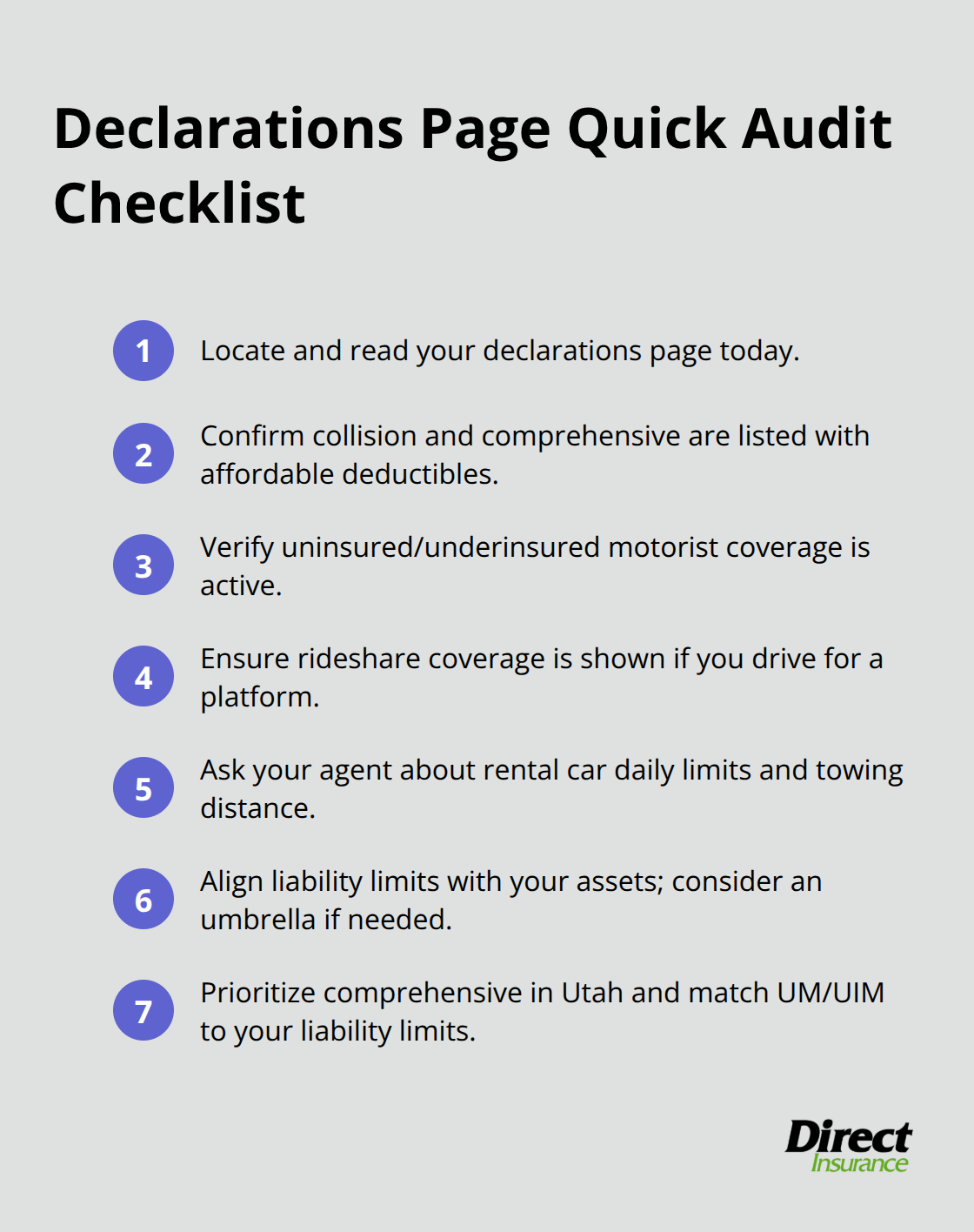

Check your declarations page right now-not next year, today. Your declarations page lists every coverage and its limits in plain language. If collision and comprehensive aren’t listed, you have zero vehicle damage protection regardless of what you thought you purchased. If uninsured motorist coverage shows $0 or isn’t listed at all, you have no protection against uninsured drivers.

If you drive for rideshare, your declarations page should explicitly state rideshare coverage; if it doesn’t, contact your agent immediately because you’re uninsured during rideshare activity.

Call your agent and ask specifically what your policy excludes, what the daily limits are for rental car reimbursement, what your towing coverage includes, and whether you have new car replacement or gap coverage. Most drivers never ask these questions and then face surprises during claims. Compare your current limits against your actual exposure: if you own a home worth $400,000, your liability limits should be at least 100/300/100 or higher, with an umbrella policy providing additional liability coverage. If you own nothing and rent, minimum coverage might technically suffice, but uninsured motorist coverage remains critical because it protects your income and future earnings. Utah’s weather creates specific coverage needs that state minimums ignore. Comprehensive coverage is absolutely essential in Utah because hail storms, flash floods, and winter weather cause regular claims. If you live in a region with higher uninsured motorist rates, UM/UIM coverage matching your liability limits costs nearly nothing but prevents financial catastrophe.

Final Thoughts

Complete auto insurance coverage protects your financial future in ways that state minimum requirements simply cannot. Pull out your declarations page today and verify what you actually have-check that collision and comprehensive appear with limits you can afford, confirm your liability limits match your assets, and verify uninsured motorist coverage is active. If you drive for rideshare, work commercially, own a collector vehicle, or financed a new car, confirm those specific coverages appear explicitly on your declarations page.

Utah’s weather patterns, regional uninsured motorist rates, and driving conditions demand coverage that goes beyond legal minimums. One accident or weather event exposes gaps that leave you paying thousands from your own pocket, which is why complete auto insurance coverage accounts for these realities rather than leaving you exposed to the accidents most likely to happen where you live. We at Direct Insurance Services understand Utah’s unique insurance needs because we live here and work with Utah drivers every day.

Contact Direct Insurance Services today for a personalized coverage review. We’ll examine your current policy, identify gaps, and show you exactly what complete protection costs for your situation.