Utah Homeowners Insurance Tips: Practical Ways to Improve Your Policy

Utah homeowners face unique insurance challenges, from wildfire seasons to hail storms that can damage roofs and siding. Your current policy might leave gaps that cost you thousands when disaster strikes.

At Direct Insurance Services, we’ve helped hundreds of Utah homeowners strengthen their coverage and cut premiums at the same time. This guide walks you through practical Utah homeowners insurance tips that actually work.

What Makes Utah Homeowners Insurance Different

Hail, Wind, and Winter Weather Threats

Utah’s location in the Mountain West creates specific insurance challenges that differ from most other states. Hail storms regularly pummel the Wasatch Front, with spring and early summer bringing the highest risk of roof and siding damage. Wind events can exceed 50 miles per hour, particularly in canyon areas and at higher elevations. Winter brings heavy snow loads that stress roofing structures, and the combination of snow and ice creates frozen pipe risks if your home isn’t properly heated during cold snaps.

The Utah Insurance Department notes that frozen pipe damage coverage requirements may not be covered if caused by negligence, such as failing to maintain adequate heating. This isn’t just a coverage question but a maintenance responsibility. Your standard homeowners policy covers wind damage, wind-driven rain, damage from falling trees or objects, and structural collapse from ice or snow accumulation. Verify these specific perils are listed in your policy documents before relying on them.

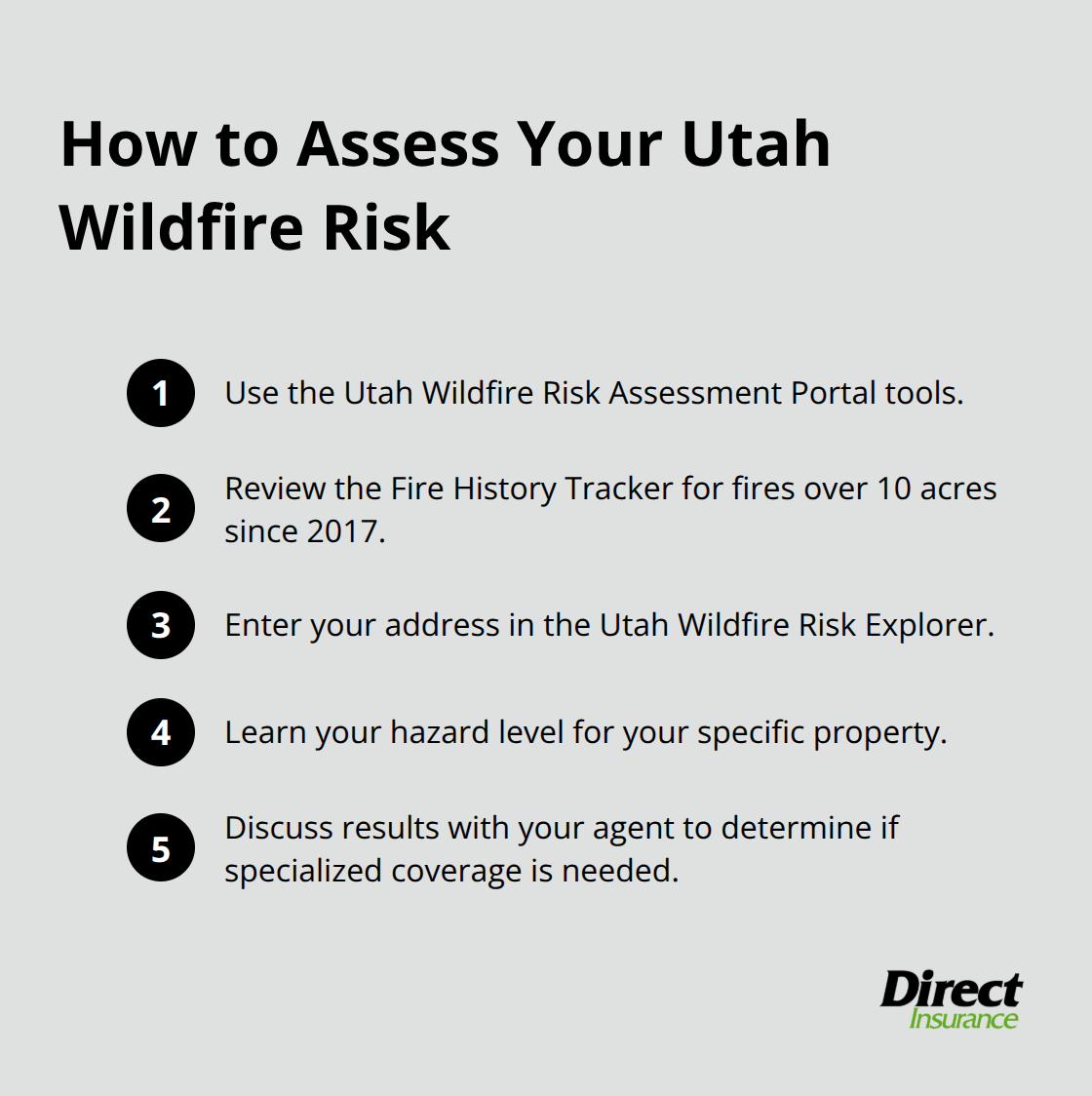

Wildfire Risk in the Wildland-Urban Interface

Wildfire risk has become the dominant concern for Utah homeowners, especially those living in or near the Wildland-Urban Interface. Utah is experiencing rapid population growth that pushes development into high-risk zones, and long-term drought combined with hazardous fuel levels across the state have elevated wildfire exposure significantly.

The Utah Wildfire Risk Assessment Portal provides free tools to assess your specific property risk. The Fire History Tracker maps wildfires over 10 acres dating back to 2017 and shows structures threatened or destroyed. Input your address into the Utah Wildfire Risk Explorer to understand your actual hazard level, then discuss this data with your insurance agent to determine whether you need specialized wildfire coverage beyond your standard policy.

Many Utah insurers now offer wildfire-specific endorsements and may provide discounts for defensible space improvements. Clear vegetation within 100 feet of your home, maintain gutters, seal gaps, and use fire-resistant landscaping materials to reduce your risk profile and potentially lower your premiums.

Location and Crime Considerations

Theft and property crime in Utah remain below national averages, but certain communities experience higher rates. Your location within Utah can meaningfully affect your premium. Insurers assess neighborhood crime data when calculating rates, so homes in lower-crime areas typically qualify for better pricing than those in higher-risk zones.

Understanding your specific community’s crime statistics helps you anticipate how your location influences your insurance costs. This information also guides conversations with your agent about what coverage levels make sense for your neighborhood. As you evaluate your policy’s adequacy, the next step involves identifying concrete ways to lower your premiums without sacrificing protection.

How to Cut Your Utah Home Insurance Costs Without Sacrificing Protection

Install Security Systems and Safety Devices

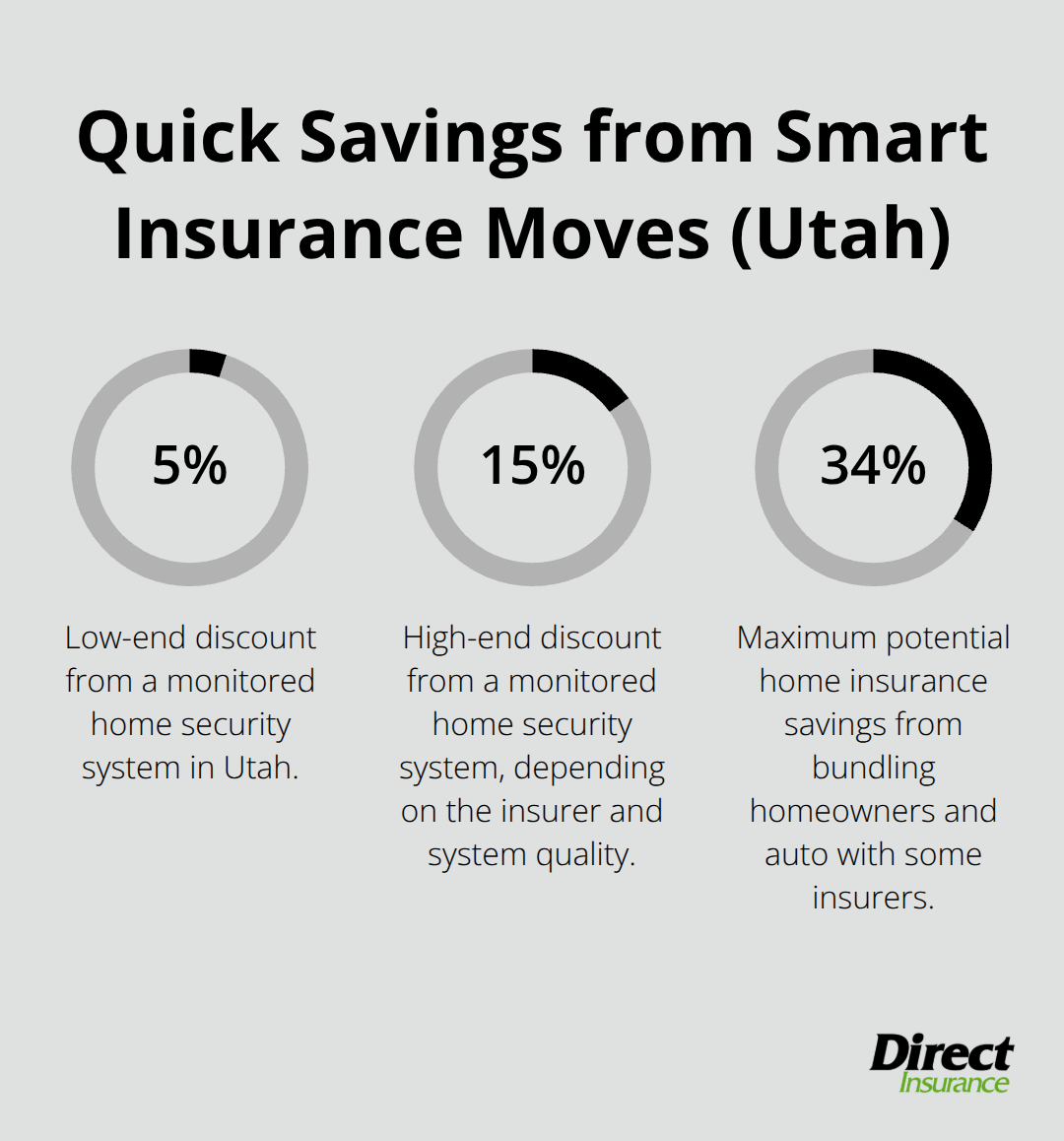

Security systems and safety devices reduce your insurance risk directly, which is why insurers reward them with real premium reductions. Dead-bolt locks, smoke alarms, fire extinguishers, and sprinkler systems all lower your claim likelihood, and many Utah insurers offer measurable discounts for these upgrades. A monitored security system can save you 5 to 15 percent on your homeowners premium depending on the insurer and system quality.

If you live in a high-wildfire zone, install ember-resistant vents and maintain defensible space around your home to signal risk reduction to underwriters. Some insurers in Utah now offer specific discounts for wildfire mitigation measures like gutter cleaning and vegetation management. The cost of a basic security system typically pays for itself within two years through premium savings alone, making it one of the smartest investments you can make for both protection and affordability.

Increase Your Deductible Strategically

Increasing your deductible represents the fastest way to lower your annual premium, but you must choose an amount you can actually afford to pay out of pocket after a loss. Moving from a $500 deductible to $1,000 typically reduces your premium by 15 to 25 percent, while jumping to $2,500 can save 30 to 40 percent or more. The math only works if you have emergency savings to cover your chosen deductible without financial strain.

According to Policygenius data on Utah rates, a home with $300,000 in dwelling coverage costs about $894 annually at a $500 deductible but drops to roughly $650 at a $1,500 deductible. This substantial difference shows why deductible selection matters so much for your overall costs.

Bundle Policies and Compare Multiple Quotes

Bundling your homeowners and auto policies with the same insurer generates the most significant savings for most Utah households. Farmers offers approximately 17 available discounts and can save bundled customers up to 34 percent on home insurance in some states. American Family averages about $620 per year in Utah with multiple discounts, while State Farm averages around $1,092 yearly and provides extensive add-ons including flood, wildfire, and earthquake coverage.

Getting quotes from at least three different insurers takes less than an hour and often reveals $200 to $500 in annual savings you didn’t know existed. Each company weights risk factors differently, so your specific home may qualify for better rates with one insurer over another. As you evaluate these quotes and consider which coverage options fit your situation, understanding what your home actually costs to replace becomes the next critical step.

Getting Your Home’s Replacement Value Right

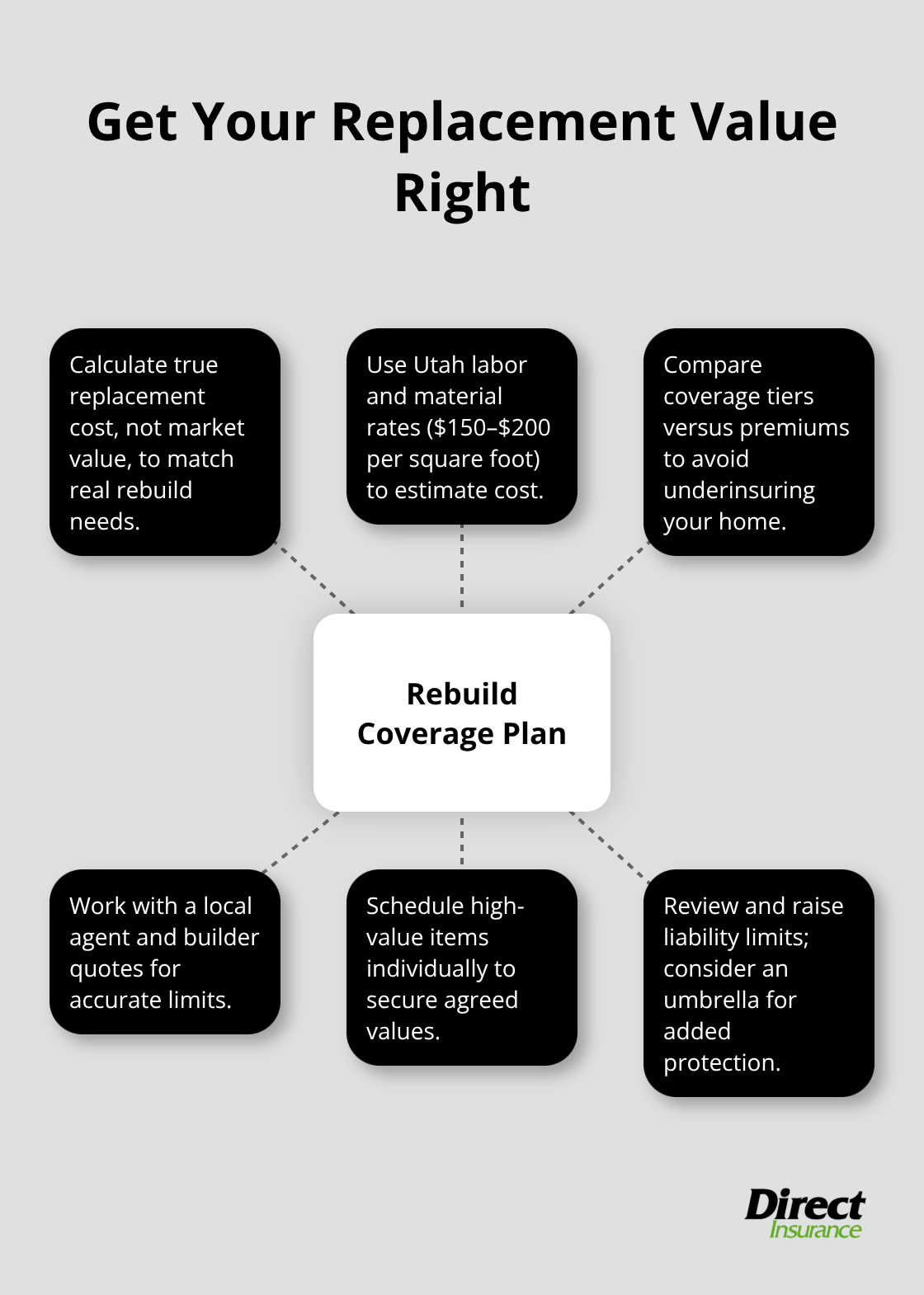

Calculate True Replacement Cost, Not Market Value

Your dwelling coverage amount determines what your insurer will actually pay to rebuild your home after a total loss, so this number must match reality, not wishful thinking. Most Utah homeowners drastically underestimate their replacement costs, which leaves them severely underinsured when disaster strikes. Policygenius data shows that a $300,000 dwelling coverage level costs about $894 annually in Utah, while $400,000 costs $1,109, and $500,000 costs $1,349. The difference between these coverage tiers is relatively small, yet the protection gap is enormous if your home actually requires $450,000 to rebuild.

Replacement cost means the actual dollars needed to rebuild your structure with new materials at current labor rates in Utah, which typically runs $150 to $200 per square foot depending on quality and finishes. A 2,500-square-foot home at $175 per square foot costs $437,500 to rebuild, yet many Utah homeowners carry only $250,000 in coverage. The Utah Insurance Department recommends reviewing your dwelling coverage annually because construction costs rise faster than most people realize.

Work with Your Agent on Local Builder Quotes

Request that your insurance agent calculate replacement cost based on local Utah builder quotes, not generic national averages. Some insurers offer guaranteed replacement cost endorsements that pay full rebuilding expenses even if costs exceed your policy limit, which costs more upfront but eliminates the risk of falling thousands of dollars short after a catastrophic loss.

Schedule High-Value Items Individually

High-value items like jewelry, artwork, and collections typically max out at $1,500 to $2,500 under standard homeowners policies, so items worth significantly more require scheduled personal property endorsements that list them individually with agreed values. If you own firearms, collectibles, or expensive electronics, add these endorsements to prevent disputes about value at claim time.

Protect Yourself with Adequate Liability Coverage

Liability coverage protects you if someone is injured on your property or if you accidentally damage someone else’s property. Utah homeowners should carry at least $300,000 in liability protection, though $500,000 is far more prudent given rising medical costs. Your liability limit applies per occurrence, so a single accident involving multiple injured parties can exhaust lower limits quickly.

Umbrella policies add an extra $1 million in liability coverage for $150 to $300 annually, which provides strong protection for any homeowner with meaningful assets. Review your liability limits every few years, especially if your home value or net worth has increased, and discuss earthquake and flood coverage additions with your agent since standard policies exclude both perils entirely and Utah faces genuine risk from both hazards.

Final Thoughts

Strengthening your Utah homeowners insurance policy requires three concrete actions that work together. First, verify that your dwelling coverage matches your actual replacement cost by working with a local agent who understands Utah construction expenses. Second, add the specific endorsements your situation demands, whether that means scheduled personal property coverage for valuables, earthquake protection given the Wasatch Front’s seismic activity, or wildfire coverage if you live in a high-risk zone. Third, implement the premium-reduction strategies that fit your financial situation, from installing security systems to raising your deductible to an amount you can genuinely afford.

A local insurance agent makes this process far simpler than shopping alone. Your agent knows which Utah insurers offer the best rates for your specific risk profile, understands how local wildfire data affects underwriting decisions, and can explain the difference between actual cash value and replacement cost in practical terms. They also stay current on Utah-specific coverage requirements and flag gaps you might otherwise miss.

We at Direct Insurance Services have spent decades helping Utah homeowners navigate these decisions and apply Utah homeowners insurance tips to their specific situations. Our team shops multiple top-rated insurance companies to find you the best coverage at competitive rates, and we understand the unique risks that come with living in Utah. Contact Direct Insurance Services to review your current coverage and get quotes from multiple insurers, and bring your policy documents and a list of any recent home improvements or high-value items you own.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation