Renters Insurance Utah: Protecting Your Personal Property

Renters insurance in Utah is often overlooked, yet it’s one of the smartest financial decisions you can make. Your landlord’s insurance covers the building, not your belongings-leaving your personal property completely unprotected without your own policy.

At Direct Insurance Services, we’ve helped countless Utah renters understand what coverage they actually need. This guide walks you through the essentials, from what’s covered to how you’ll find the right policy for your situation.

What Your Renters Insurance Actually Covers

Personal Property Protection

Your renters policy protects three critical areas that your landlord’s insurance completely ignores. Personal property coverage protects your personal belongings including furniture, electronics, clothing, appliances, and everyday valuables. This covers everything from your laptop and sound system to furniture, clothing, and kitchen appliances, whether they sit inside your apartment or someone steals them from your car. According to MoneyGeek’s 2024 data, the typical Utah renters policy includes around $20,000 in personal property coverage, though you can adjust this based on what you actually own.

A personal property calculator helps you inventory your belongings and determine realistic replacement costs. Most Utah renters significantly underestimate how much their possessions are worth until they need to replace them after a loss. This tool takes the guesswork out of coverage amounts and prevents you from carrying too little protection.

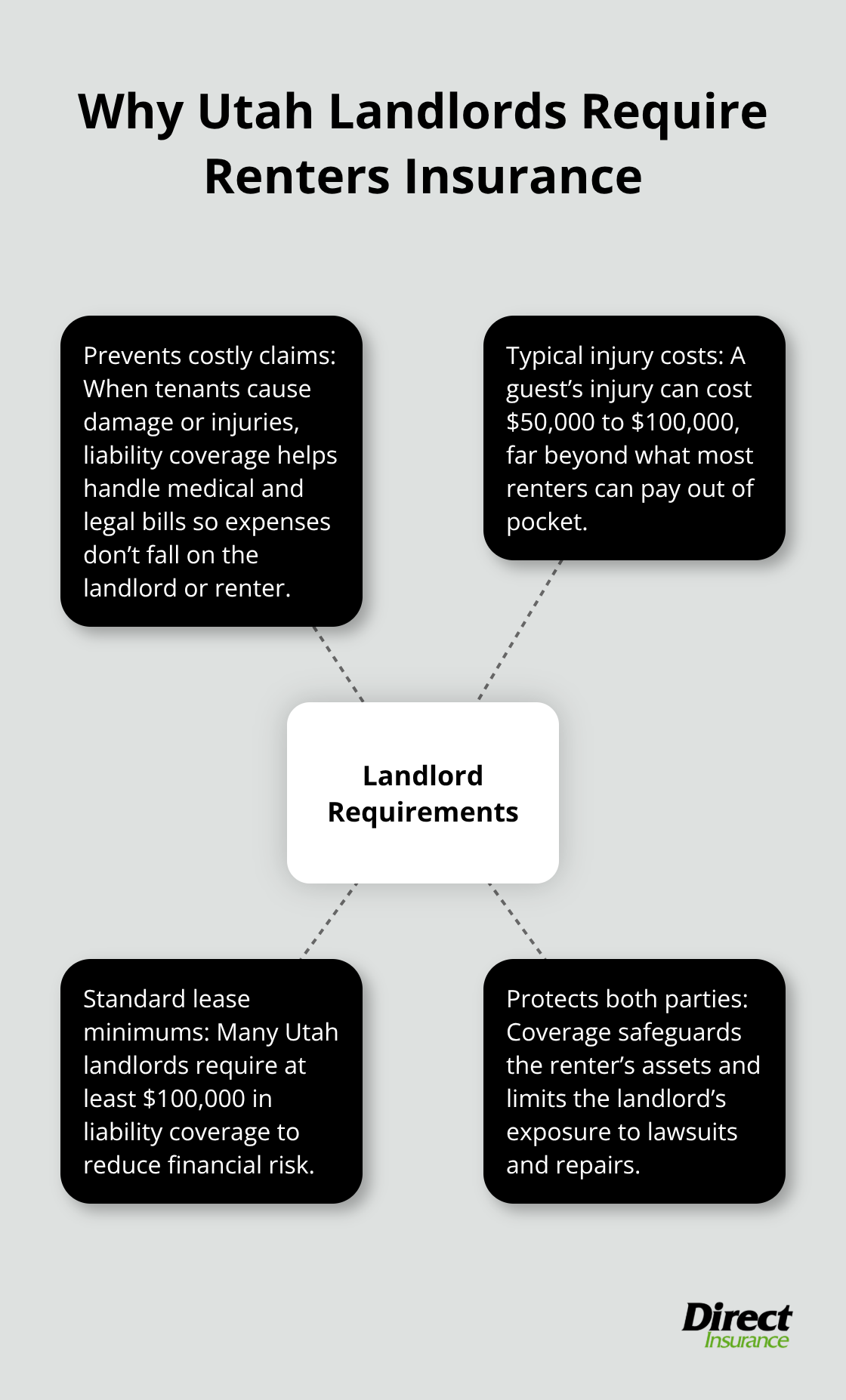

Liability Coverage for Accidents

Liability coverage is equally important and often undervalued. This protection covers medical expenses and legal fees if you become legally responsible for someone else’s injuries or property damage. If a guest slips in your apartment and breaks their arm, or you accidentally damage a neighbor’s property, your liability coverage handles their medical bills and any lawsuit costs. Utah landlords commonly require at least $100,000 in liability coverage, and for good reason-medical expenses and legal fees can easily exceed $50,000.

The financial stakes are real. A single accident can create liability that extends far beyond what most renters expect to pay out of pocket. Liability coverage protects your personal assets from claims that could otherwise devastate your finances.

Additional Living Expenses and Affordability

Additional living expenses coverage pays for temporary housing, meals, and other costs if a covered loss forces you out of your apartment. If a fire makes your unit uninhabitable, this coverage covers hotel stays and restaurant meals until you can move back or find a new place. In Utah, renters insurance costs as little as $8 per month through State Farm or around $10 per month through Auto-Owners and Allstate, making comprehensive protection surprisingly affordable.

Important Coverage Gaps

One critical limitation exists: standard policies don’t cover flood damage. If you live in a flood-prone Utah area, you’ll need separate flood insurance through the National Flood Insurance Program. This gap in coverage matters significantly for renters in certain regions, and understanding your specific location’s flood risk helps you make informed decisions about additional protection.

Your coverage needs depend on what you own and where you live. The next section explains why Utah renters specifically benefit from this protection and what financial risks you face without it.

Why Utah Renters Actually Need This Protection

The Real Cost of Replacing Your Belongings

Replacing your belongings after a loss costs far more than most renters expect. A laptop runs $800 to $1,500, a bedroom set costs $2,000 to $4,000, and kitchen appliances add another $1,500 to $3,000. Add clothing, electronics, furniture, and everyday items, and your total replacement cost easily exceeds $15,000 to $30,000. MoneyGeek’s data shows the typical Utah renter carries around $20,000 in personal property, yet most people have never calculated what their actual belongings are worth.

Without renters insurance, you’d pay every dollar of that replacement cost yourself after a fire, theft, or other covered loss. Insurance companies won’t replace your belongings. Your landlord’s policy covers only the building structure, not what’s inside. That gap between what you own and what’s protected is exactly where renters insurance steps in.

Why Landlords Require Coverage

Utah landlords increasingly require renters insurance as a lease condition, and this isn’t just paperwork. Landlords mandate coverage because they understand the financial exposure when a tenant causes property damage or someone gets injured in the unit. If a guest slips on your floor and breaks their leg, medical costs can reach $50,000 to $100,000. Without liability coverage, you’d face a lawsuit and potential wage garnishment.

Most Utah landlords specifically require at least $100,000 in liability coverage for exactly this reason. This requirement protects both you and your landlord from catastrophic financial consequences.

Affordable Protection Against Financial Disaster

Affordable renters insurance in Utah starts with State Farm at $13.04 per month, making it an accessible option for most renters. That monthly investment protects you from catastrophic financial loss. The reality is stark: one accident or one theft without insurance can cost more than you’d spend on premiums over the next five years.

Utah renters who skip this protection are gambling with their financial security, betting they won’t experience a fire, theft, or liability claim. The odds aren’t in your favor. Understanding what coverage options exist and how they fit your specific situation helps you make the right decision. The next section walks you through how to select the right policy for your needs and budget.

Selecting the Right Coverage for Your Budget

Calculate What You Actually Own

Choosing renters insurance in Utah requires comparing three specific factors: what coverage limits match your belongings, what deductible you can afford to pay out of pocket, and which insurer offers the best premium for that combination. State Farm charges $8 per month for $20,000 in personal property coverage with $100,000 in liability, while Auto-Owners runs $10 per month and Allstate $10 per month for the same baseline protection, according to MoneyGeek’s 2024 data. The difference between $8 and $10 monthly adds up to $24 annually, but it matters far less than whether you’re actually covered for what you own.

Start with MoneyGeek’s Personal Property Coverage Calculator to total your actual belongings-furniture, electronics, clothing, kitchen items, and everything else. Most Utah renters discover they own between $25,000 and $40,000 in personal property, not the $20,000 baseline. Once you know your real number, request quotes from at least three insurers using that specific coverage amount.

Compare Quotes and Deductible Options

State Farm remains Utah’s cheapest option at roughly $33 per month for $250,000 in personal property coverage with $300,000 in liability, making it the clear winner if you own significant valuables. Your deductible choice directly impacts your monthly premium-selecting a $500 deductible instead of $250 typically saves $2 to $4 monthly, but only choose the higher deductible if you genuinely have that much cash available for an emergency replacement cost.

Request personalized quotes by calling 1-866-749-7436, or work directly with a Utah agent who understands local risks like winter storms and wildfire smoke damage. Your actual coverage needs vary significantly based on whether you live near the University of Utah in Salt Lake City versus a rural area near Veyo, where premiums range from $151 to $173 annually due to location-specific risks.

Add Optional Coverage for High-Value Items

Beyond base coverage, Utah renters should strongly consider water backup coverage, scheduled personal property coverage for jewelry or electronics exceeding policy limits, and personal injury coverage for slander or defamation claims. Water backup coverage protects against sewer and drain backups or sump pump discharge, which standard policies explicitly exclude. If you own jewelry worth more than $2,500 or electronics exceeding $3,000, scheduled personal property coverage adds those items individually to your policy at their full replacement value rather than applying standard limits.

Maximize Savings Through Bundling and Discounts

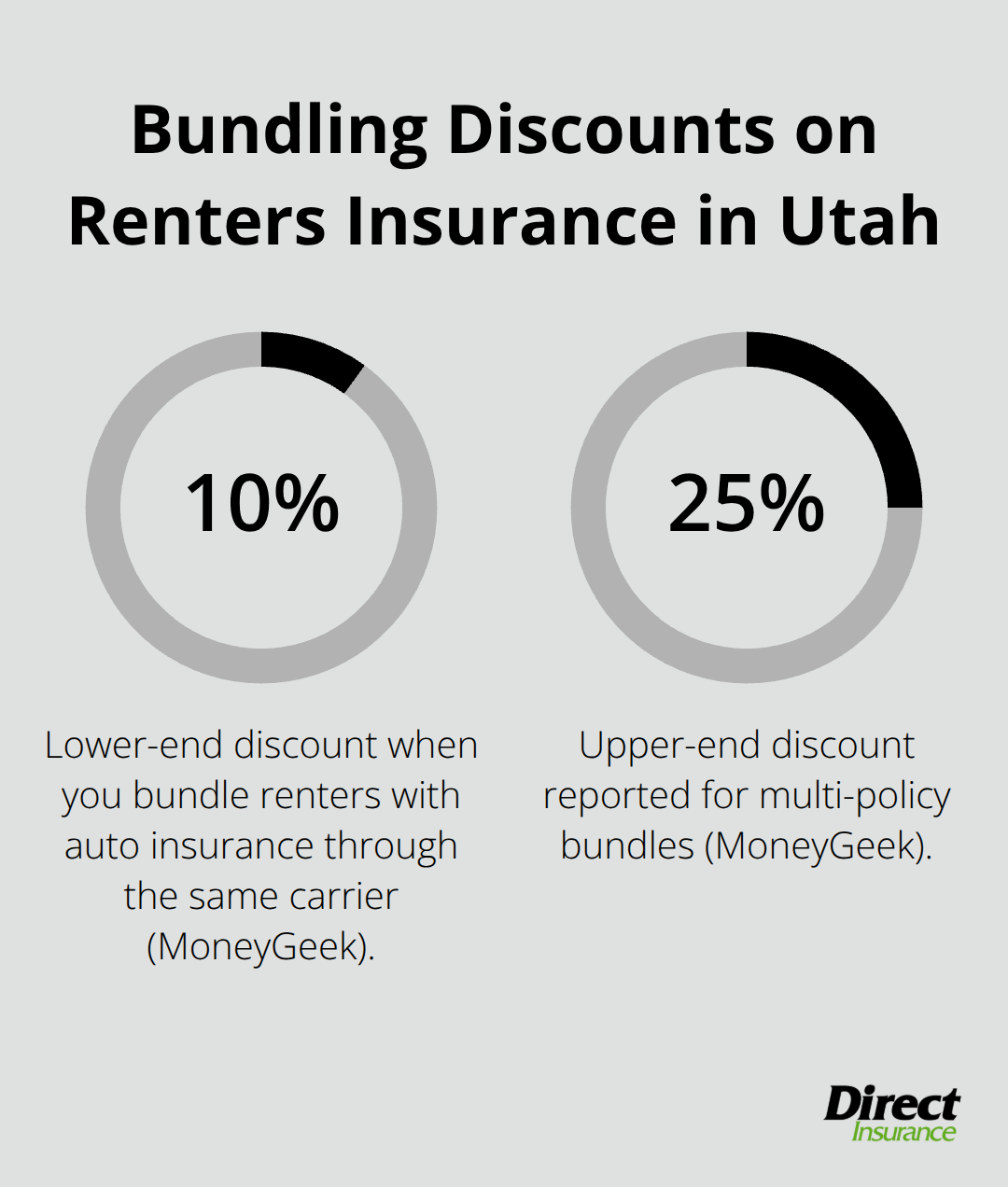

Multi-policy bundling delivers the largest savings-combining renters with auto insurance through the same carrier cuts renters premiums by 10 to 25 percent according to MoneyGeek, meaning that $10 monthly Auto-Owners policy drops to roughly $7.50 to $9 if you already insure your vehicle there. Security systems, smoke detectors, and automatic payment setup also reduce premiums across most Utah insurers. These discounts stack quickly, transforming an already affordable policy into exceptional value for comprehensive protection.

Final Thoughts

Renters insurance in Utah protects what matters most-your personal belongings and your financial security against unexpected losses. Replacing your possessions after a fire or theft costs thousands of dollars, liability claims can exceed $100,000, and comprehensive coverage starts at just $8 monthly through State Farm. Without this protection, a single accident leaves you paying out of pocket for everything.

Calculate your actual belongings using a personal property calculator, then request quotes from at least three insurers for that specific coverage amount. State Farm, Auto-Owners, and Allstate all offer competitive rates in Utah, and bundling with auto insurance cuts your premium by 10 to 25 percent. Most renters discover they can afford solid protection for less than the cost of a daily coffee.

Contact Direct Insurance Services today for a free quote and take the first step toward genuine financial protection. Our team helps Utah renters find coverage that actually matches what they own and their budget. Spending $100 to $150 annually on renters insurance eliminates the risk of losing thousands in personal property or facing a devastating liability claim.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation