What Is Average Auto Insurance Cost?

Auto insurance costs vary wildly depending on where you live, what you drive, and your driving history. Most drivers pay somewhere between $1,200 and $2,000 annually, but your actual premium could be much higher or lower.

At Direct Insurance Services, we help drivers understand what influences their rates and find ways to pay less. This guide breaks down the factors that shape your premium and shows you concrete steps to reduce what you’re paying.

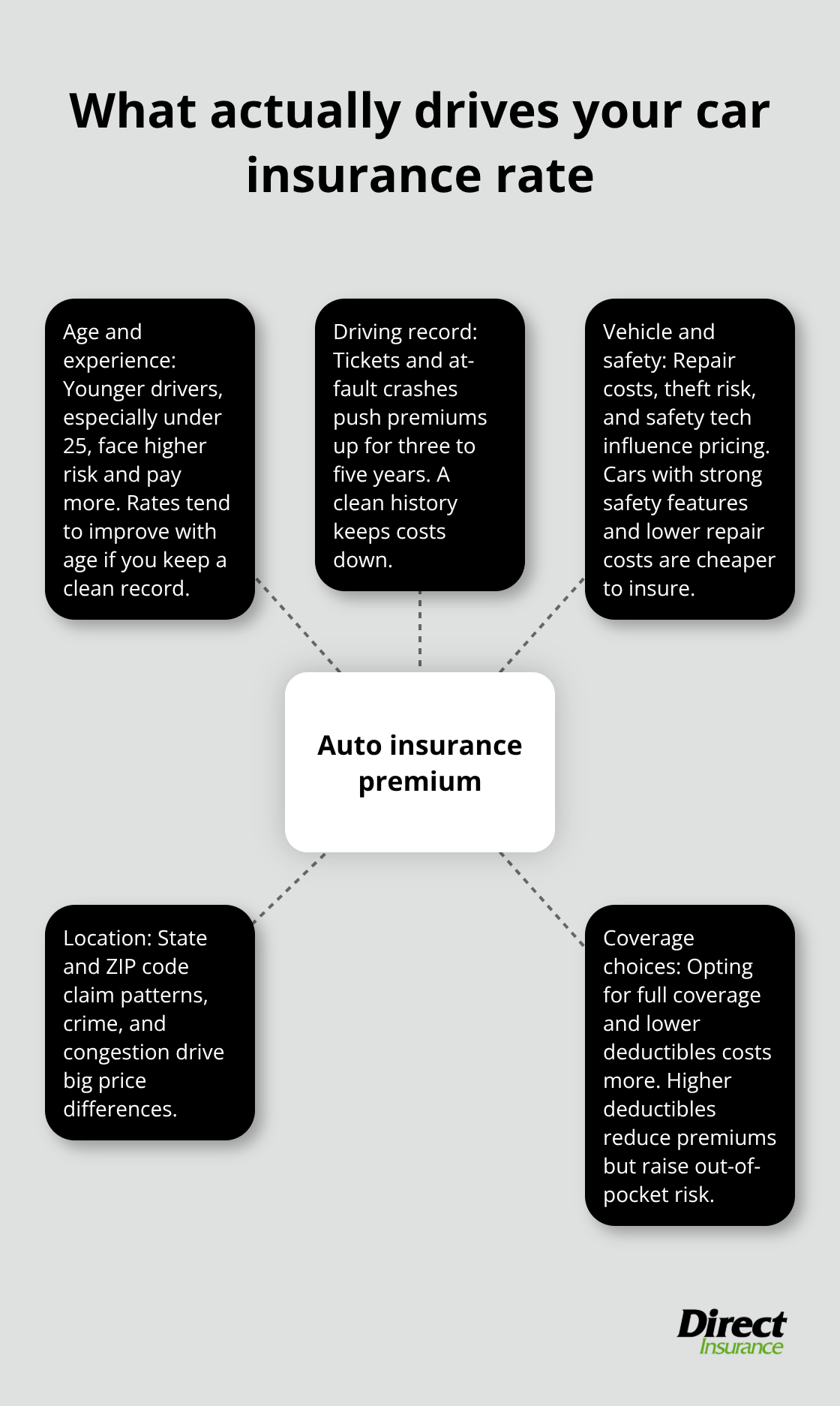

What Actually Drives Your Insurance Premium

Your age, vehicle, and driving history form the three pillars that determine what you pay for car insurance, and they matter far more than most drivers realize. A 16-year-old pays roughly $5,740 per year for full coverage according to Bankrate data, while a 40-year-old with the same vehicle and clean record pays around $2,697 annually. That’s a difference of $3,043 simply because of age and inexperience behind the wheel. Young drivers under 25 represent the highest-risk group statistically, so insurers charge accordingly. Rates drop sharply after age 25 and continue declining through your 40s and 50s, meaning your premium naturally improves over time if you maintain a clean driving record.

Your Driving Record Speaks Louder Than Anything Else

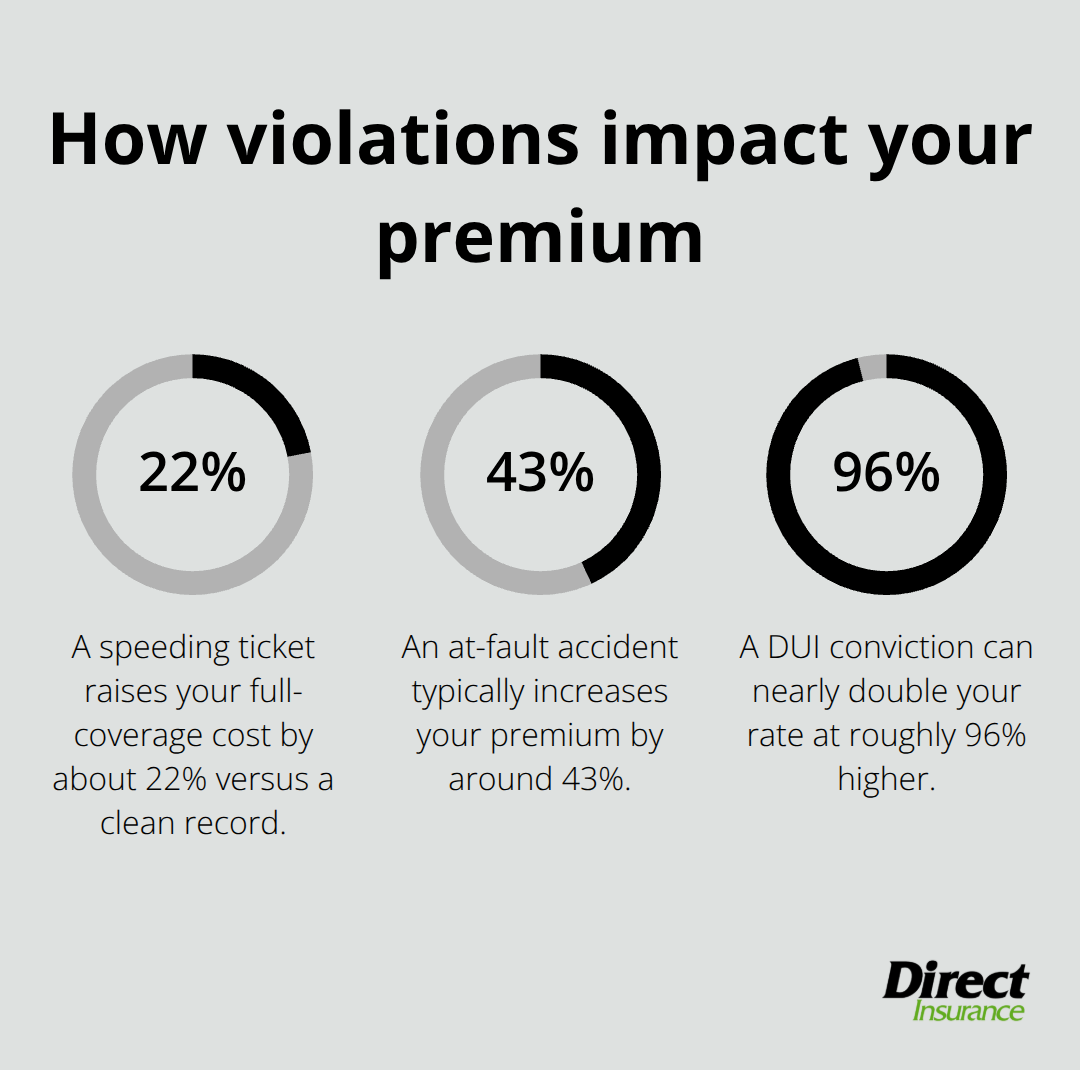

A single speeding ticket increases your full-coverage cost by approximately 22% compared to a clean record, according to Bankrate’s analysis. An at-fault accident jumps that penalty to around 43%, and a DUI conviction can nearly double your premium at roughly 96% higher. These numbers explain why maintaining a clean driving record is the fastest way to keep premiums low.

Even minor violations stick around for three to five years on your record, so the choices you make today affect what you pay for years to come. If you’ve had violations in the past, they age off your record and your rates should drop when they do.

Vehicle Type and Safety Features Impact Your Rate

The car you drive has an enormous impact on your premium. A BMW 330i costs approximately $276 per month for full coverage while a Honda Odyssey costs around $204 monthly, both based on Bankrate’s rate examples. The difference comes down to repair costs, safety ratings, and theft risk. Vehicles with advanced driver assistance systems (like automatic emergency braking and lane-keeping assist) may qualify for premium discounts because they reduce accident likelihood. High-end sports cars and luxury vehicles cost substantially more to repair, so insurers charge higher premiums to cover that risk. If you’re shopping for a used vehicle, checking insurance costs before you buy can save you hundreds annually.

How Coverage Choices Shape What You Pay

The type and amount of coverage you select directly affects your premium. Full coverage (collision and comprehensive) costs significantly more than minimum coverage, but it protects your vehicle if you finance or lease it. Raising your deductible from $500 to $1,000 lowers your monthly payment substantially, though you’ll pay more out of pocket if an accident occurs. Your coverage limits on liability also matter-higher limits protect your assets but increase your premium. These decisions require you to balance protection with affordability, and the right choice depends on your vehicle’s value and your financial situation. Understanding these trade-offs helps you find the coverage level that fits your needs without overpaying.

What You’ll Actually Pay for Auto Insurance

National Average Costs and What They Mean

The national average for full-coverage auto insurance reaches $2,697 annually according to Bankrate’s data, which translates to roughly $225 per month. Minimum coverage costs significantly less at around $820 per year or $68 monthly. These numbers establish a baseline for what’s reasonable, but your actual rate will differ substantially based on where you live and your personal risk profile. California residents pay approximately 16% above the national average due to congestion and dense traffic patterns, while Idaho drivers enjoy rates roughly 45% below average at around $1,476 annually. Louisiana sits at the opposite extreme, with full-coverage costs reaching $4,135 per year-53% higher than the national average-driven by hurricane risk, higher uninsured motorist rates, and expensive repair labor. New York and Florida round out the most expensive markets, both exceeding $3,800 annually for full coverage. Vermont offers the cheapest full-coverage rates at $1,610 per year, benefiting from lower population density and fewer theft and accident claims.

How State Location Dominates Your Premium

Location determines your rate more than most drivers realize. State-level differences prove that where you live matters far more than many other factors. Dense urban areas with heavy traffic and higher crime rates push premiums upward, while rural states with lower accident frequencies keep costs down. Insurance companies track local claim patterns, repair costs, and litigation expenses by ZIP code and state, then adjust their rates accordingly. Your state’s regulatory environment also affects pricing-some states restrict how insurers use credit scores or other rating factors, which can lower or raise premiums depending on your profile. If you’re considering a move or shopping for a vehicle in a new state, checking insurance costs beforehand reveals hidden expenses that affect your total cost of ownership.

Breaking Down Your Coverage Components

Liability coverage, which is mandatory in every state, protects other people if you cause an accident-and it’s the cheapest component of your policy. Collision coverage protects your own vehicle in accidents and typically costs substantially more, especially for newer cars. Comprehensive coverage handles theft, weather, and vandalism, and it’s often the least expensive add-on but becomes critical if you finance your vehicle. Deductible selection dramatically affects your out-of-pocket costs: a $500 deductible means you pay $500 toward repairs before insurance kicks in, while a $1,000 deductible lowers your premium but increases your risk. Most drivers try $500 or $1,000 deductibles as the practical middle ground.

When to Drop or Keep Physical Damage Coverage

If you drive an older vehicle worth less than $5,000, dropping collision and comprehensive coverage makes financial sense-you’d pay more in premiums over time than the car is worth. Conversely, if you financed or leased your vehicle, your lender requires full coverage, so you don’t have that choice. The math is straightforward: compare your vehicle’s current value against what you’d spend on collision and comprehensive premiums over several years. Once your car depreciates below a certain threshold, that coverage becomes wasteful. However, if you still owe money on your vehicle, your lender won’t allow you to make this decision-they protect their financial interest by requiring full coverage until you own the car outright.

Why Shopping Multiple Quotes Reveals Dramatic Price Differences

The same driver might pay $1,200 annually with one insurer and $1,800 with another for identical coverage, making comparison shopping non-negotiable before signing any policy. Different carriers weigh risk factors differently and apply their own underwriting standards, which creates substantial variation in what they charge. Some insurers specialize in certain driver profiles (young drivers, high-risk drivers, or safe drivers) and price accordingly, while others maintain broader pricing strategies. You won’t know your best option until you request quotes from multiple companies and compare them side by side. This process takes time but saves hundreds of dollars annually and reveals which carriers value your specific risk profile most favorably.

How to Cut Your Auto Insurance Costs

Bundle Policies for Immediate Savings

Bundling your auto policy with home or renters insurance at the same carrier delivers immediate savings that outpace everything else you can do. Carriers like State Farm, Geico, and Allstate typically discount bundled policies by 15-25%, meaning a driver paying $225 monthly for auto coverage alone could drop that to roughly $170-190 after adding home insurance to the same company. This works because insurers view bundled customers as less likely to leave, so they reward loyalty with aggressive discounts. The math makes bundling the single most effective cost-reduction strategy available to most drivers.

Leverage Discounts and Monitoring Programs

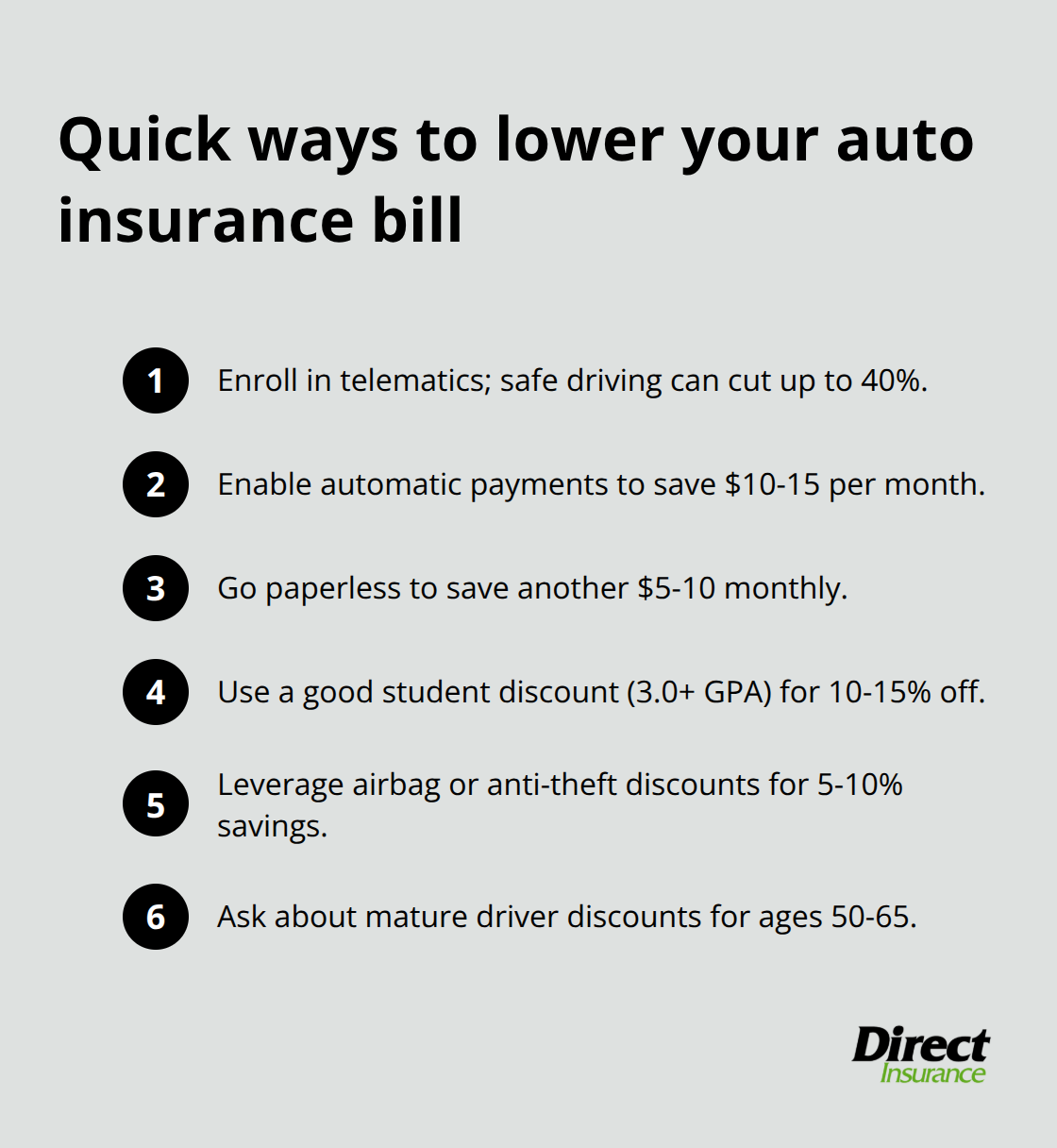

Taking advantage of available discounts separates smart shoppers from people leaving money on the table. Telematics programs that monitor your driving habits can reduce premiums by as much as 40% if you maintain safe driving patterns, though this requires installing an app or device. Automatic payment discounts typically save $10-15 monthly, paperless billing saves another $5-10, and good student discounts (for drivers under 25 with a 3.0 GPA or higher) can cut costs by 10-15%. Safety equipment discounts for airbags or anti-theft devices add modest savings of 5-10%, while mature driver discounts for those aged 50-65 recognize lower accident rates with similar reductions. Ask your insurer specifically which discounts apply to your profile rather than assuming you qualify for standard ones.

Maintain a Clean Driving Record

Your driving record remains the fastest lever to pull for long-term savings because violations and accidents directly inflate your premium for years. A speeding ticket costs you an extra 22% annually, but that penalty ages off after three to five years depending on your state, so avoiding new violations preserves the discount you’ve already earned. If you’ve had an at-fault accident adding 43% to your rate, the math becomes clear: safe driving habits over the next few years will save more than any other strategy combined. Each year without a violation or accident strengthens your rate advantage.

Adjust Deductibles and Coverage Strategically

Raising your deductible from $500 to $1,000 immediately lowers your monthly payment, though you’ll absorb more cost if an accident happens. The practical calculation works like this: if your full-coverage premium drops $20-30 monthly by increasing your deductible, you break even on that decision after 33-50 months without a claim. Most drivers can comfortably absorb a $1,000 deductible, making this the smart choice if you have emergency savings. For older vehicles worth less than $5,000, dropping collision and comprehensive coverage entirely makes financial sense because you’d spend more in premiums over time than the car is worth. However, if you financed your vehicle, your lender requires full coverage until you own it outright, so this option only applies to paid-off cars.

Shop Multiple Quotes Regularly

Shopping quotes from multiple insurers every two to three years prevents rate creep as your insurer slowly raises your premium. The same driver often pays 30-50% less with a different carrier, yet most people renew automatically without checking alternatives. This simple habit of comparing options every few years protects you from overpaying and reveals which carriers value your specific risk profile most favorably.

Final Thoughts

Your auto insurance premium reflects a complex mix of factors-your age, driving record, vehicle type, location, and coverage choices all shape what you pay. Understanding what is average auto insurance cost in your state and how your personal situation compares gives you the foundation to make smarter decisions. The national average of $2,697 annually for full coverage provides a useful benchmark, but your actual rate depends heavily on where you live and your individual risk profile.

The strategies that work best for reducing your premium are straightforward and actionable. Bundling your auto policy with home or renters insurance delivers the fastest savings, often cutting 15-25% off your costs immediately, while maintaining a clean driving record compounds your savings over years because violations and accidents inflate your premium for three to five years after they occur. Raising your deductible, shopping multiple quotes every few years, and taking advantage of available discounts like telematics programs or automatic payments all contribute to meaningful reductions without sacrificing protection.

Shopping around remains non-negotiable because the same driver pays dramatically different rates across carriers. You won’t find your best option without requesting quotes from multiple companies and comparing them directly. We at Direct Insurance Services shop multiple top-rated insurance companies on your behalf to secure the best possible rates and coverage for your situation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation