Does Your Auto Insurance Cover Rental Cars?

Your auto insurance might cover rental cars-or it might not. The answer depends on your specific policy, coverage type, and the circumstances surrounding why you need a rental.

At Direct Insurance Services, we’ve helped countless customers navigate this confusion. We’ll walk you through what your policy actually covers, when rental car protection kicks in, and how to strengthen your coverage.

What Your Auto Insurance Actually Covers for Rentals

Your personal auto policy’s liability coverage travels with you to rental cars just as it does to your own vehicle. If your policy includes liability, comprehensive and collision coverage with the same limits and deductibles you carry on your primary vehicle, those protections apply to most rental situations within the United States and Canada. However, many people face gaps when they need them most.

When Your Policy Extends to Rentals

Forbes Advisor reports that if you rent for business purposes, some personal auto policies explicitly exclude coverage. You must contact your insurer before booking to verify protection. The same applies if you travel outside North America-your policy likely won’t cover you abroad, and you’ll need supplemental liability insurance from the rental agency or a third-party provider.

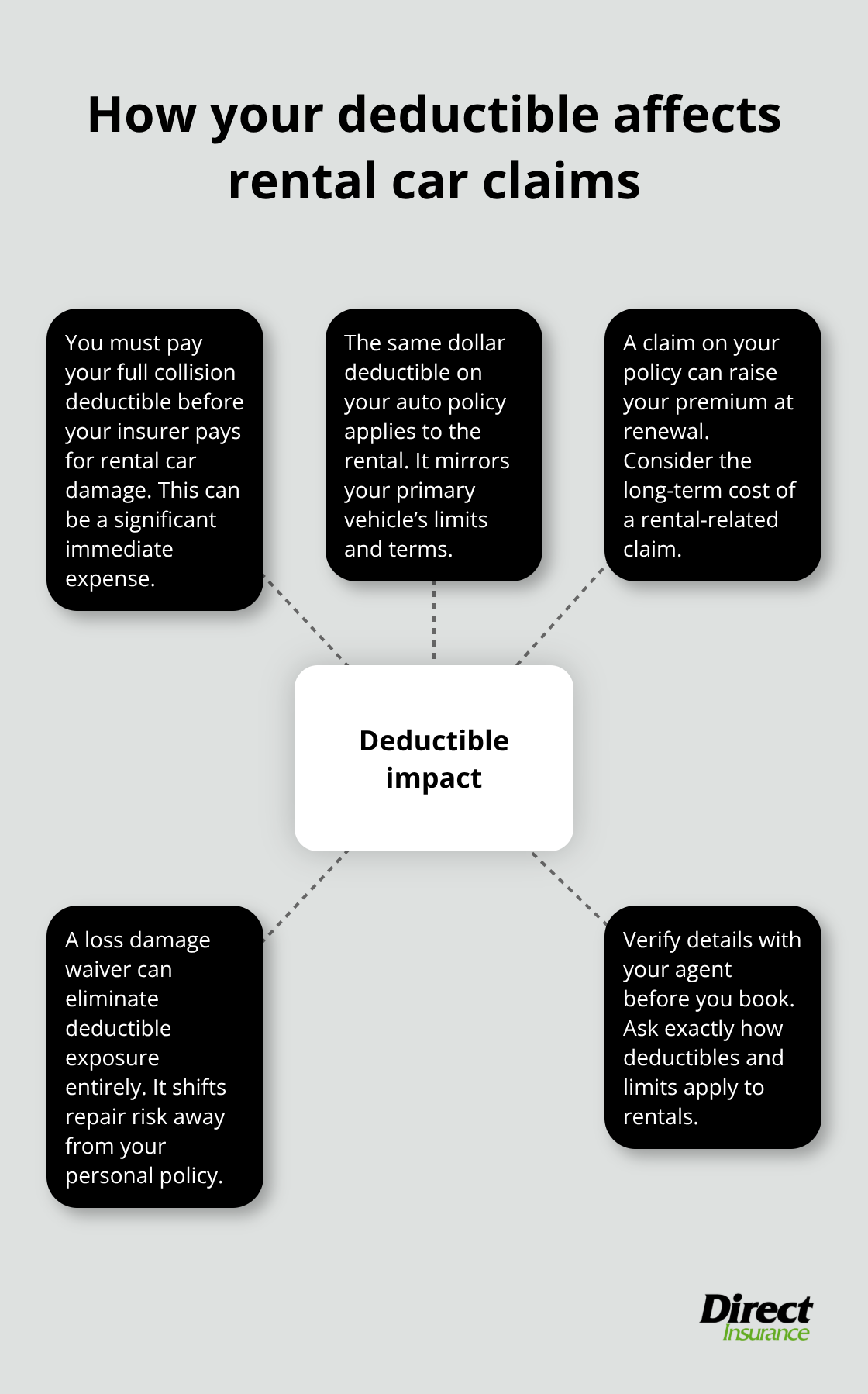

Your deductibles matter significantly here. If your auto policy carries a $1,000 collision deductible, that same $1,000 applies to rental car damage under most policies. This creates real financial exposure. If you damage a rental car and file a claim through your personal policy, you’ll pay that deductible out of pocket, and the claim could impact your premium at renewal.

Comprehensive Versus Collision Coverage

Comprehensive coverage protects against theft, weather, vandalism, and other non-collision damage. Collision coverage handles accidents and impact damage. Both typically extend to rentals, but only if you carry them on your personal policy. Many drivers carry only liability coverage to save money, which means rental cars receive zero protection for physical damage.

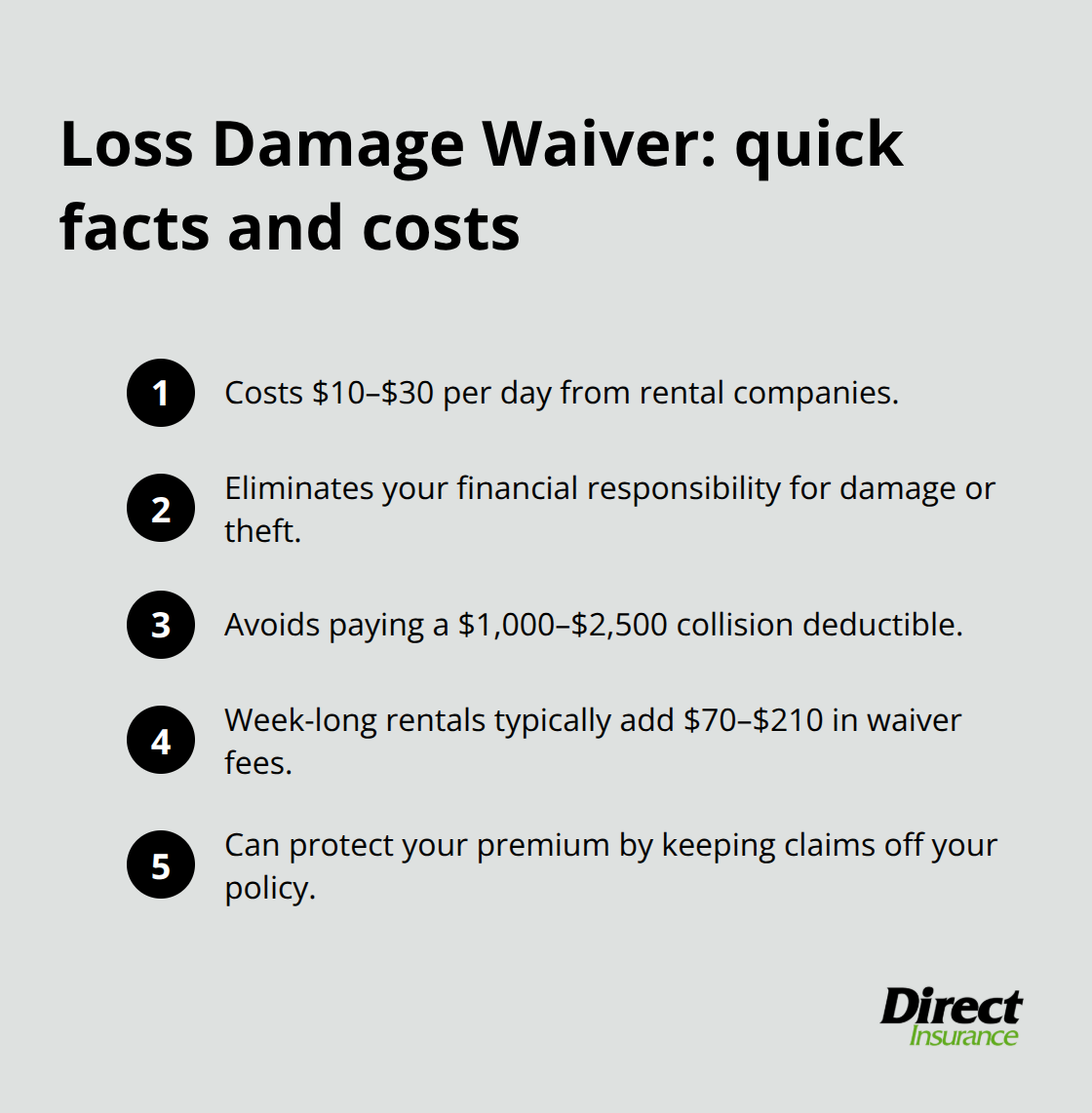

If this describes your situation, the rental company’s loss damage waiver becomes essential, not optional. The waiver costs roughly $10 to $30 per day according to Forbes Advisor, but it eliminates your financial responsibility if the car is damaged or stolen.

Credit Card Coverage and Its Limitations

Credit card rental car insurance can fill some gaps, but here’s the critical limitation: most credit card coverage is secondary, meaning your auto insurance pays first, then the card covers what remains. Some premium cards like the Venture X card offer primary coverage, which pays before your auto policy. You need to verify this directly with your card issuer before relying on it.

The bottom line is straightforward-review your actual policy documents, not just your memory of what you think you have. Call your agent and ask explicitly whether collision and comprehensive extend to rentals at the same limits and deductibles you carry on your primary vehicle. Once you understand what your current policy covers, you can identify whether you need additional protection through rental reimbursement or other add-ons.

When Rental Coverage Actually Applies

Your auto policy’s collision and comprehensive coverage extend to rental cars, but only in specific situations. If you experience an accident with a rental vehicle and carry collision coverage, your policy pays for repairs after you satisfy your deductible. The same applies to comprehensive claims like theft or weather damage. However, this protection has boundaries you need to understand before problems arise.

Business Rentals and Policy Exclusions

Business rentals often fall outside coverage entirely. If you rent a car for work purposes, your personal auto policy typically won’t cover accidents or damage. This distinction matters because many people assume their coverage follows them everywhere. Contact your insurer before any work-related rental to confirm whether your policy includes business use protection.

International Rentals and Geographic Limits

International rentals create another gap. Your U.S. auto policy stops working the moment you cross into Mexico, Canada coverage varies by insurer, and traveling further abroad leaves you completely unprotected. You’ll need to purchase supplemental liability insurance from the rental company or a third-party provider to drive legally outside North America.

State-Specific Requirements That Override Your Policy

Some states impose additional requirements that override what your personal policy provides. California and Texas require rental agencies to offer liability coverage if you don’t have your own, meaning you cannot decline protection at the counter without proving you’re already insured. State minimum liability coverage requirements vary significantly by location. If your auto policy carries limits below your state’s requirements for rentals, the rental company’s supplemental liability insurance becomes mandatory, not optional.

Deductible Exposure and Loss Damage Waivers

Your deductible exposure demands serious attention when damage occurs. If your collision deductible is $1,000 and you damage a rental car, you pay that $1,000 directly before your insurer covers anything beyond it. This claim also hits your driving record and can increase your premium at renewal. The rental company’s loss damage waiver, costing $10 to $30 daily, eliminates this deductible exposure entirely.

High-deductible policies make rental waivers financially sensible. If you carry a $2,500 deductible on your personal vehicle, accepting a loss damage waiver on a week-long rental costs roughly $70 to $210 but protects you from a catastrophic out-of-pocket expense if something happens.

Credit Card Coverage and Primary Versus Secondary Protection

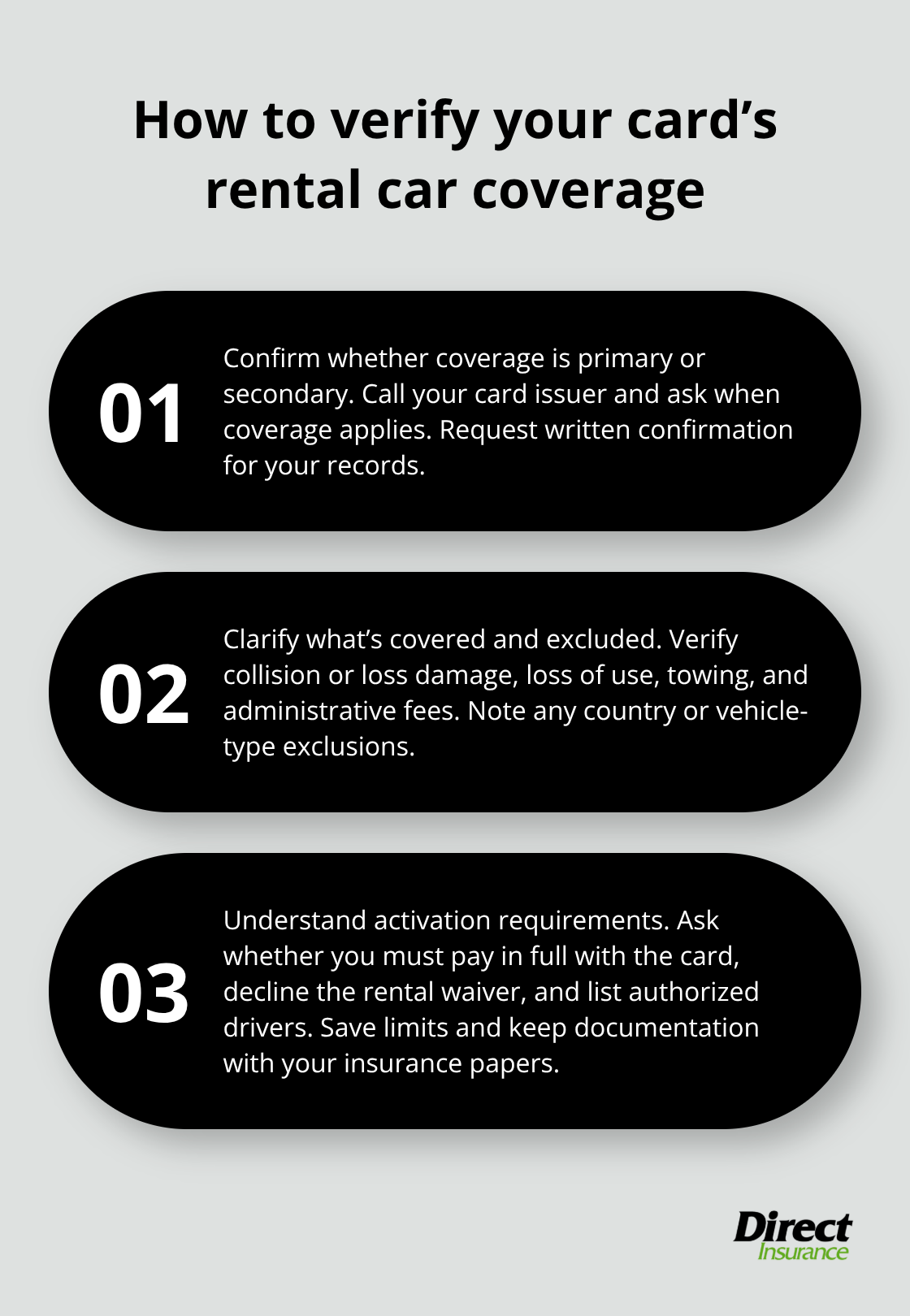

Credit card coverage provides another layer, but with significant restrictions. Most cards offer secondary coverage only, meaning your auto insurance pays first and the card covers gaps afterward. Premium cards like the Venture X offer primary coverage, paying before your auto policy activates. You must contact your card issuer directly to confirm whether your specific card provides primary or secondary protection and whether it covers loss of use charges that rental companies often impose when a damaged vehicle sits in the shop.

Understanding these boundaries before you arrive at the rental counter prevents expensive mistakes. The next step involves identifying which additional protections make sense for your situation and how to add them to your policy before you need them.

How to Strengthen Your Rental Coverage Before You Need It

Adding rental reimbursement to your auto policy costs between $10 and $15 annually but solves a specific problem: it covers the daily rental cost while your own vehicle sits in the repair shop after an accident. This differs fundamentally from rental car damage coverage. Rental reimbursement pays for your transportation expenses during repairs, typically covering $30 to $50 per day up to a specified limit. If you carry collision coverage with a high deductible, this add-on protects you from unexpected rental costs that pile up quickly. A week of repairs can easily cost $210 to $350 in rental fees, and rental reimbursement eliminates that expense entirely. Contact your agent and ask specifically whether your current policy includes this coverage-many policies don’t, and the minimal annual cost makes it worth adding immediately.

Credit card coverage requires verification before you rely on it

Your credit card might provide rental car protection, but most cards offer only secondary coverage, meaning your auto insurance pays first and the card covers remaining gaps. This creates complications when filing claims because you manage two insurers instead of one. Premium cards like the Venture X offer primary coverage, which activates before your auto policy, but you must confirm this directly with your card issuer rather than assuming. Additionally, credit card coverage often excludes loss of use charges that rental companies impose when a damaged vehicle remains in the shop, potentially leaving you with significant out-of-pocket costs. Call your card issuer today and request written confirmation of exactly what your card covers for rental cars, including whether it covers loss of use, towing, and administrative fees. Write down the coverage limits and keep this documentation with your insurance documents.

Third-party rental car insurance costs less than rental counter options

The rental company’s loss damage waiver costs $10 to $30 daily, which adds $70 to $210 for a week-long rental. Third-party providers like Allianz Global Assistance offer primary coverage for collision and loss damage through products like OneTrip Rental Car Protector, often for less than half the rental counter price and covering amounts up to $75,000. Stand-alone rental car insurance also works internationally, protecting you in countries where your U.S. auto policy provides zero coverage. If you rent cars frequently or travel internationally, purchase annual travel insurance plans that cover rental car damage, baggage loss, and other benefits more affordably than buying coverage at each rental counter. Compare quotes from Allianz, Bonzah Rental Cover, and Sure before your next rental rather than making a decision under pressure at the counter. These third-party options provide primary coverage, meaning they pay first without involving your personal auto policy or credit card, protecting your driving record and premium from rental-related claims.

Final Thoughts

The answer to whether your auto insurance covers rental cars depends entirely on what you actually carry in your policy and where you’re renting. Most drivers assume they’re protected, then discover gaps when damage occurs. Your liability coverage travels with you to rental cars, but collision and comprehensive protection only extend to rentals if you’ve purchased them on your personal policy, with deductibles that apply the same way as your primary vehicle.

The financial stakes matter significantly. Accepting a loss damage waiver at the rental counter costs $10 to $30 daily but eliminates deductible exposure entirely. For week-long rentals, this protection ranges from $70 to $210, which sounds expensive until you face a $1,000 or $2,500 deductible on actual damage. Credit card coverage provides another layer, though most cards offer only secondary protection, meaning your auto insurance pays first. Premium cards like the Venture X offer primary coverage, but you must verify this directly with your issuer rather than guessing.

We at Direct Insurance Services understand that rental car coverage creates real confusion for Utah drivers. Our team can review your current policy, identify gaps in your protection, and recommend affordable add-ons that fit your situation. Contact us today at saltlakeinsurance.com to schedule a policy review and ensure you’re protected before your next rental.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation