How to Find the Cheapest Auto Insurance in Utah

Utah drivers pay an average of $1,247 per year for auto insurance, but rates vary wildly based on your driving history, vehicle type, and coverage choices. Finding the cheapest auto insurance in Utah means understanding what factors push your premiums up and knowing exactly where to look for better deals.

At Direct Insurance Services, we help Utah drivers cut through the noise and find coverage that actually fits their budget. This guide walks you through the specific steps to compare quotes, spot discounts, and lower what you pay each month.

What Really Drives Your Auto Insurance Costs

Your Driving History Matters Most

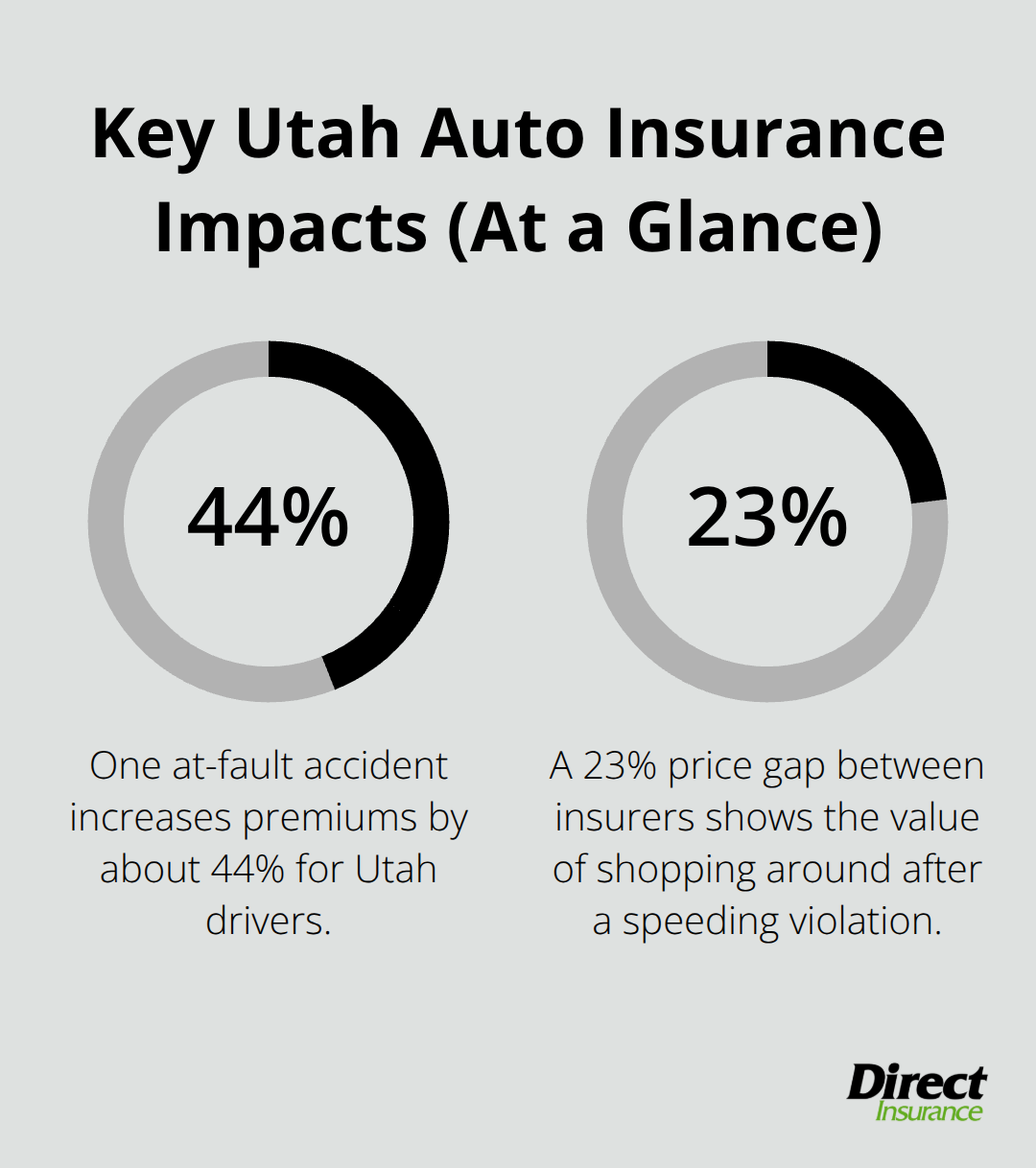

Your driving history impacts much more than your driving record, including insurance premiums, employment opportunities, and legal consequences. A speeding ticket alone adds roughly $200 to $300 annually to your premium, according to NerdWallet data from March 2026. One at-fault accident bumps your costs up by about 44%, while a DUI can skyrocket your rate by 104% or more-some drivers end up paying over $4,000 per year after a DUI conviction.

The good news is that your driving record improves over time. Once three years pass without a violation, many insurers start to forget about old infractions, so your focus should be on keeping a clean record going forward. If you already have marks on your record, quotes from multiple carriers matter even more because insurers weight driving history differently.

USAA charges roughly $1,680 for a driver with one speeding violation, while Geico comes in around $2,160 for the same scenario, according to Quadrant Information Services data. This 23% difference shows that shopping around can save hundreds even after a mistake.

Vehicle Type, Location, and Credit Score

Your vehicle choice, age, location, and credit score round out the major rate factors. A BMW 330i costs about $2,661 per year to insure in Utah versus a Toyota Camry at $2,188, based on Quadrant data-that $473 gap reflects both repair costs and theft risk.

Utah’s average full coverage runs $2,188 per year, which is genuinely cheaper than the national average of $2,697, but where you live in Utah matters tremendously. Salt Lake City drivers pay around $198 per month for full coverage, while Saint George residents pay $166 per month-a $384 annual swing just from location. Your credit score can widen that gap further; poor credit adds roughly $1,000 or more to annual premiums compared to good credit.

Age and Coverage Limits

Age is the largest driver of price differences in the state-a 20-year-old pays roughly $3,824 per year for full coverage while a 50-year-old with the same insurer might pay $1,407, according to NerdWallet. The coverage limits you select also reshape your bill significantly. Minimum coverage in Utah averages $831 per year, while full coverage runs $2,188-a difference of nearly $1,400 annually.

Since these factors stack on top of each other, a young driver in Salt Lake City with one speeding ticket and poor credit faces a dramatically different rate than a 50-year-old with clean driving in Saint George and excellent credit. Understanding which factors you can control-and which ones you cannot-sets you up to make smarter choices when you start comparing quotes from different insurers.

How to Compare Quotes and Find Real Savings

Request Quotes from Multiple Carriers

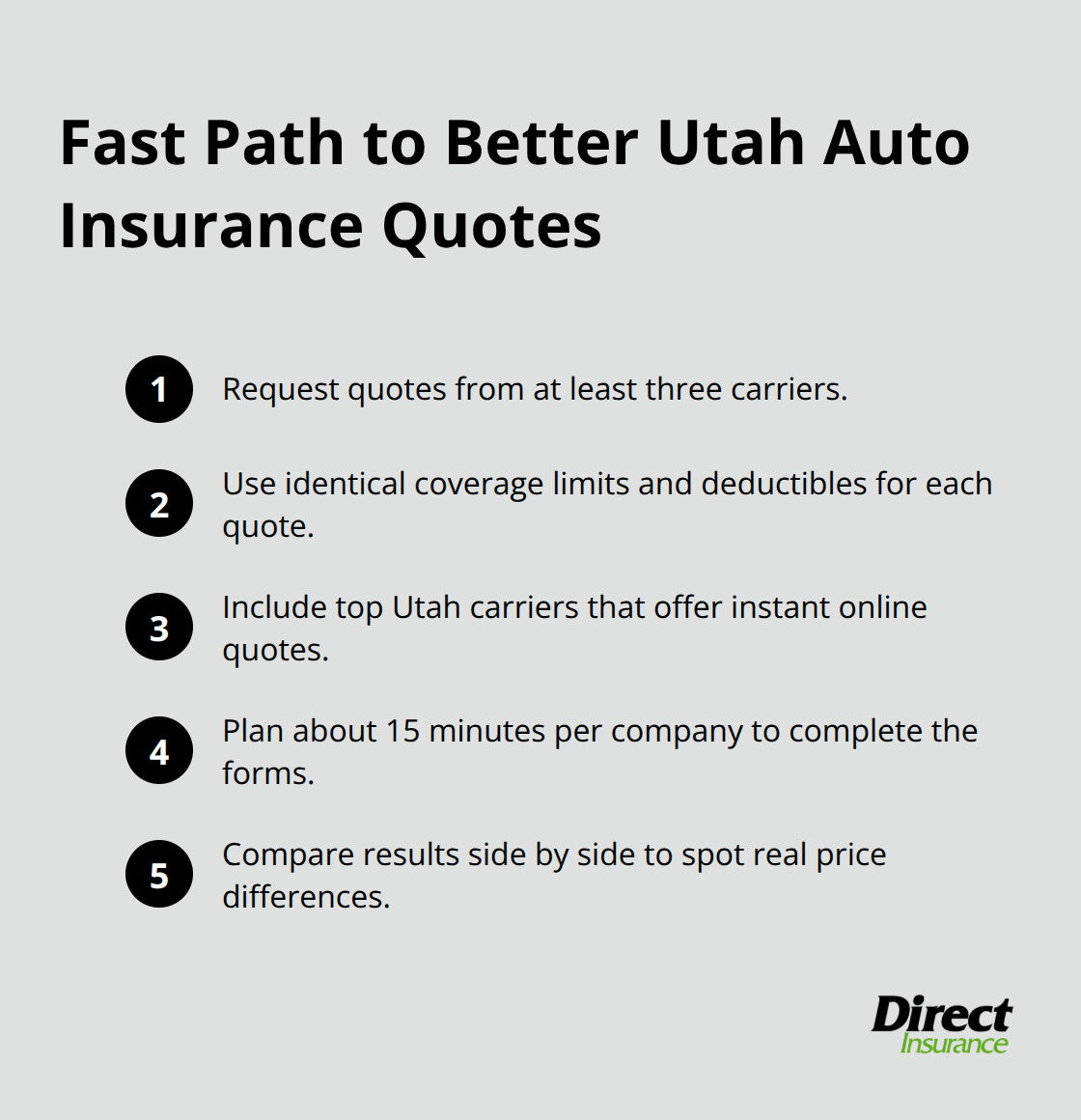

Gathering quotes from multiple insurers stands as the single most effective way to cut your Utah auto insurance bill, yet fewer than half of American drivers actually do it each year. Most people stay locked into their current policy out of pure inertia, which costs them hundreds annually. Start by requesting quotes from at least three carriers with identical coverage limits and deductibles-this apples-to-apples comparison reveals genuine price differences rather than just variations in what you’re buying.

Progressive, Allstate, Liberty Mutual, USAA, Geico, and Auto-Owners all offer instant online quotes in Utah, and the process takes roughly 15 minutes per company. The math is straightforward: if you find a quote that’s $300 cheaper per year, that’s $300 in your pocket for clicking a few buttons. NerdWallet data shows that Utah’s cheapest full-coverage options run about $1,312 annually with USAA, $1,562 with Geico, and $1,920 with Auto-Owners, but your personal rate depends entirely on your specific situation-age, location, driving history, and credit score all shift the final number.

Understand How Your Details Shape Each Quote

This is why comparison shopping beats any single recommendation; your 20-year-old in Salt Lake City with one speeding ticket will see vastly different quotes than a 50-year-old with clean driving in Saint George. Each insurer weights your risk factors differently, so one carrier’s quote might be $400 cheaper than another’s for the exact same coverage. The only way to know which insurer values your profile most favorably is to request quotes and compare them side by side.

Look Beyond Price to Claims Support

When you’re comparing quotes, look past the lowest price to verify that customer service and claims handling match your priorities. Auto-Owners ranks highest for claims satisfaction in Utah according to J.D. Power’s 2024 Regional Customer Satisfaction Study, while Geico, AAA, and State Farm also perform well in the state. A policy that’s $200 cheaper but leaves you on hold for two hours during a claim creates real frustration when you need help most.

Some insurers like Progressive and Nationwide offer monthly payment options with no penalties, which reduces the risk of accidentally letting your policy lapse. Ask each carrier about accident forgiveness programs, which shield you from rate spikes after your first at-fault claim-availability and rules vary, so read the fine print carefully.

Work with an Agency to Simplify the Process

Utah’s regulatory environment and the state’s relatively affordable rates compared to national averages mean you can often find solid coverage at competitive prices, but only if you invest time in the comparison process. An independent agency can handle this comparison work for you, shopping multiple top-rated carriers to surface the best coverage at rates that fit your budget. This approach saves you the legwork while guaranteeing you’re not overpaying. Once you’ve identified your best quote options, the next step involves understanding which discounts and coverage adjustments can push your premium even lower.

Cut Your Premium Without Cutting Coverage

Bundle Your Auto and Home Insurance

Bundling your auto and home insurance policies ranks as one of the fastest ways to lower what you pay each month. Most Utah insurers offer bundling discounts that range from 10 to 25 percent on combined premiums, according to industry data. If you’re currently paying $182 per month for full-coverage auto insurance in Utah, a 15 percent bundling discount saves you roughly $27 monthly or $324 annually-money that adds up fast when you apply it year after year. The secondary benefit is simpler billing; instead of managing separate policies and renewal dates, bundling consolidates everything into one payment. Start by asking your current home insurance provider whether they offer auto coverage, then request a bundled quote. Many carriers make the process seamless, and you might discover that switching your home policy to gain the bundling discount actually saves you more than staying with your existing homeowner insurer.

Raise Your Deductible Strategically

Raising your deductible from $500 to $1,000 typically cuts your annual premium by 10 to 15 percent, provided you have the cash reserves to cover the higher out-of-pocket cost if you file a claim. This strategy works best if you’re a safe driver with a clean record; high-risk drivers should think carefully before accepting higher deductibles. Utah’s cheapest insurers like USAA and Geico offer accident forgiveness programs that prevent your rate from spiking after your first at-fault claim, which makes accepting a higher deductible less risky because one mistake won’t destroy your premium.

Claim Every Discount Available

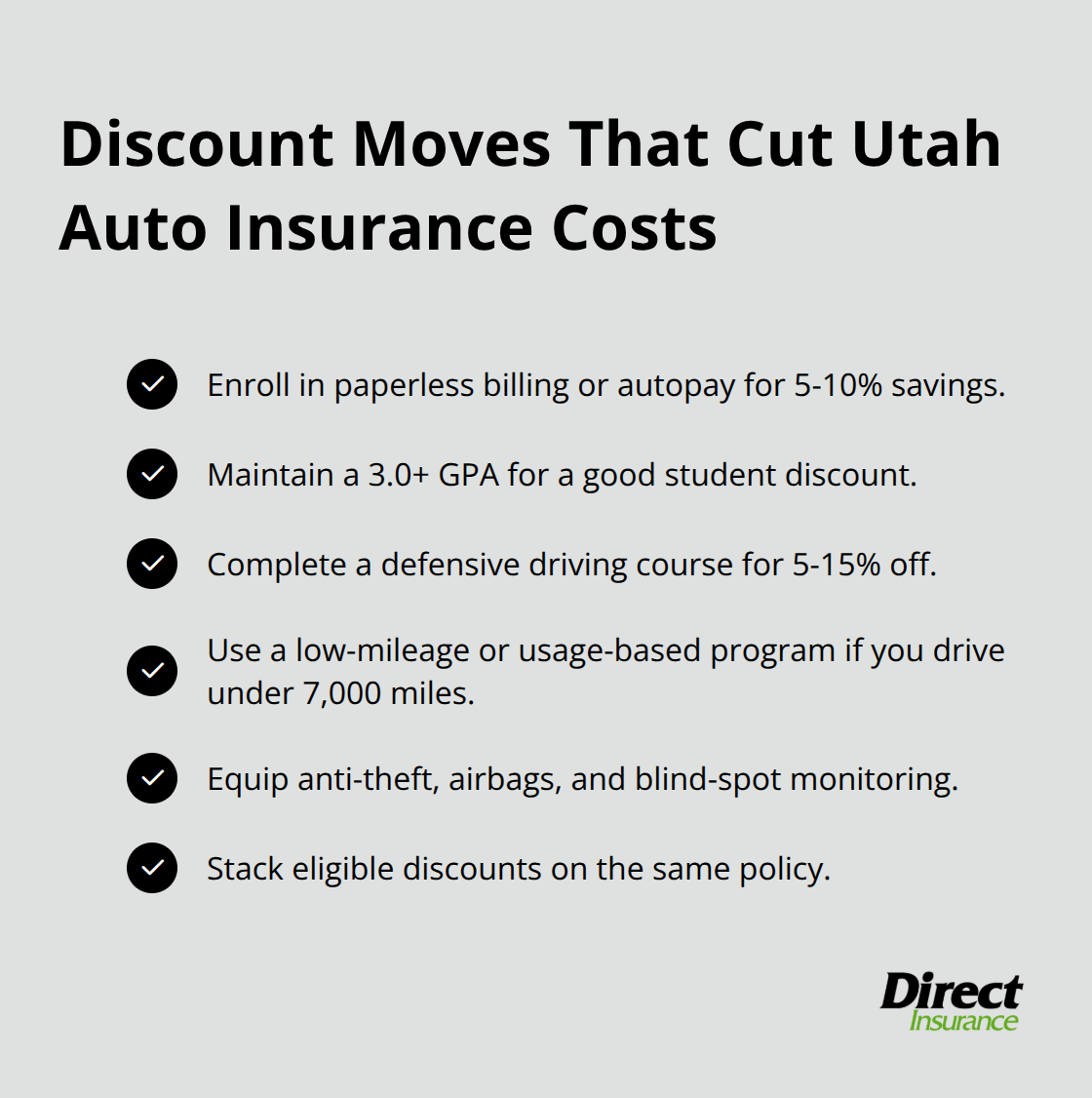

Discounts beyond bundling include paperless billing or autopay (5 to 10 percent savings), good student discounts for drivers with a 3.0 or higher GPA, defensive driving course certificates (5 to 15 percent), and usage-based programs for drivers logging fewer than 7,000 miles annually. Vehicle safety features like anti-theft systems, airbags, and blind-spot monitoring also reduce rates. Stack multiple discounts together to maximize your savings; many carriers allow you to combine paperless billing with good student and bundling discounts on the same policy.

Review Coverage After Life Changes

Review your coverage annually, especially after major life changes like purchasing a home, changing jobs, or relocating within Utah. Your ZIP code shift alone could lower your premium by hundreds of dollars; a driver moving from Salt Lake City to Saint George might see their six-month premium drop by roughly $160 just from the location change. These adjustments take minutes to request but deliver real savings over time.

Final Thoughts

Finding the cheapest auto insurance in Utah requires you to take three concrete actions: compare quotes from multiple carriers with identical coverage, stack every discount you qualify for, and review your policy annually when life changes. Age, driving history, location, and credit score drive most of your premium, but shopping around reveals $300 to $500 in annual savings even within the same risk category. Bundling home and auto policies, raising your deductible, and claiming discounts for safe driving compress your costs further without sacrificing protection.

We at Direct Insurance Services have helped Utah drivers find affordable coverage since 1973, and we understand Utah’s unique insurance landscape as locals. Rather than spending hours requesting quotes individually, you work with us and receive personalized service that accounts for your specific age, location, driving history, and budget constraints (we shop multiple top-rated carriers to surface the best rates and coverage options tailored to your situation). We offer flexible payment options and build long-term relationships focused on keeping your costs down year after year.

Your next step is straightforward: reach out to Direct Insurance Services for a personalized quote comparison. Provide your basic information, and we handle the rest, presenting you with side-by-side options from carriers like USAA, Geico, and Auto-Owners so you can see exactly where you stand. The difference between staying with your current insurer and switching to a better rate often covers months of premiums, and that money stays in your pocket instead of going to an insurer that doesn’t value your business.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation