How to Get Auto Insurance Gap Protection

Your car loses value the moment you drive it off the lot. If you finance or lease that vehicle, you could end up owing more than it’s worth after an accident.

Auto insurance gap protection covers this gap between what you owe and what your car is actually worth. At Direct Insurance Services, we see this coverage protect drivers from thousands in unexpected costs every year.

What Gap Insurance Actually Covers

Gap insurance pays the difference between your car’s actual cash value and your remaining loan or lease balance when your vehicle is totaled or stolen. Here’s the practical reality: standard auto insurance pays only what your car is worth at the time of loss. If you owe $25,000 on a financed sedan but it’s worth $20,000 after depreciation, your standard insurance cuts you a check for $20,000. You’re left responsible for the remaining $5,000, which gap insurance covers. This matters because depreciation happens fast. According to Edmunds, cars lose value over a five-year period. If you put down a small down payment or financed your vehicle for 72 months or longer, you’re especially vulnerable to this gap. The average new car loan is now $32,480, and with longer terms becoming standard, more drivers find themselves owing more than their car’s worth during the critical early years of ownership.

When the Gap Grows Widest

The gap between what you owe and what your car is worth expands most dramatically in your first few years of ownership. If you financed a vehicle with less than a 20% down payment, you almost certainly have negative equity right now. Roll negative equity from a trade-in into your new loan, and the problem compounds immediately. Americans currently carry more than $1.2 trillion in auto debt, with loan-to-value ratios reaching 120% or higher in many cases. A total loss during these high-gap years can leave you paying thousands out of pocket. Gap insurance eliminates this financial shock and covers exactly what standard insurance won’t. Some gap policies even reimburse your deductible up to $1,000, which means you could walk away from a total loss with zero out-of-pocket costs and potentially $1,000 in equity toward a replacement vehicle.

How Gap Insurance Works With Your Standard Claim

Gap insurance is supplementary, not a replacement for collision and comprehensive coverage. You must file a claim with your standard auto insurance first. Your insurer assesses the vehicle’s actual cash value and pays that amount minus your deductible. Only then does gap insurance activate to cover what remains on your loan. This two-step process protects both you and your lender. Your lender has a stake in gap protection because it reduces their charge-off risk when borrowers face negative equity situations. That’s why many lenders require gap coverage for financed vehicles, especially those with higher loan-to-value ratios. Leased vehicles almost always require gap coverage because the leasing company protects its residual value investment. Without gap protection on a lease, you’re personally responsible for any shortfall between the insurance payout and what the lessor says the car should have been worth at lease end.

What Gap Insurance Does Not Cover

Gap insurance covers the loan-to-value shortfall only. It does not pay for repairs, rental car costs, damage to other property, or injuries to people. It also does not cover finance charges, excess mileage fees on leases, or mechanical failures. Some gap policies cap coverage at 25% of the vehicle’s value, so you need to verify your specific policy limits. Understanding these boundaries helps you plan for other coverage types that address repairs and liability separately. Your standard collision and comprehensive policies handle those needs, while gap insurance handles only the depreciation gap itself.

Timing Matters for Maximum Protection

You should purchase gap insurance at or before you take possession of your vehicle. The gap is widest in the first year when depreciation is steepest. Waiting months after purchase means you’ve already lost significant equity, and the gap has already narrowed. If you financed your vehicle, your lender may require gap coverage before you drive off the lot. Leasing companies typically include gap protection in the lease agreement itself. If you’re considering gap insurance for a vehicle you already own, check your current loan-to-value ratio first. Once your loan balance drops below your car’s actual cash value, gap insurance becomes unnecessary and you can drop it. This is especially true for longer loan terms (72–84 months), where the gap persists longer but eventually closes as you pay down principal.

When You Need Gap Protection

Calculate Your Loan-to-Value Ratio

Gap protection becomes essential the moment your loan-to-value ratio climbs above 80 percent. Calculate your full LTV by adding financed taxes, fees, and add-ons to your loan amount, then divide by the vehicle’s actual cash value. A large down payment doesn’t guarantee you’re safe from negative equity, especially if you rolled negative equity from a trade-in into your new loan. This calculation reveals your true exposure to depreciation risk and determines whether gap insurance makes financial sense for your situation.

Depreciation Outpaces Your Loan Payoff

Cars that depreciate fastest in their first year create the widest gaps. According to Edmunds, vehicles lose approximately 24 percent of their value in year one alone, then another 15 percent annually. This rapid depreciation means a $30,000 car drops to $22,800 after year one while your loan balance barely budges. If you financed that vehicle with less than 20 percent down, you’re almost certainly underwater already.

The problem intensifies with longer loan terms. New auto loans now average over 70 months, and used car loans run around 65 months. These extended terms mean you make payments while depreciation is steepest, creating a dangerous window where the gap between what you owe and what your car is worth reaches its maximum. Wholesale used-vehicle values fell approximately 12 percent in mid-April 2024, signaling accelerated depreciation risk across the market. When used-car values decline while loan amounts rise, the gap widens significantly.

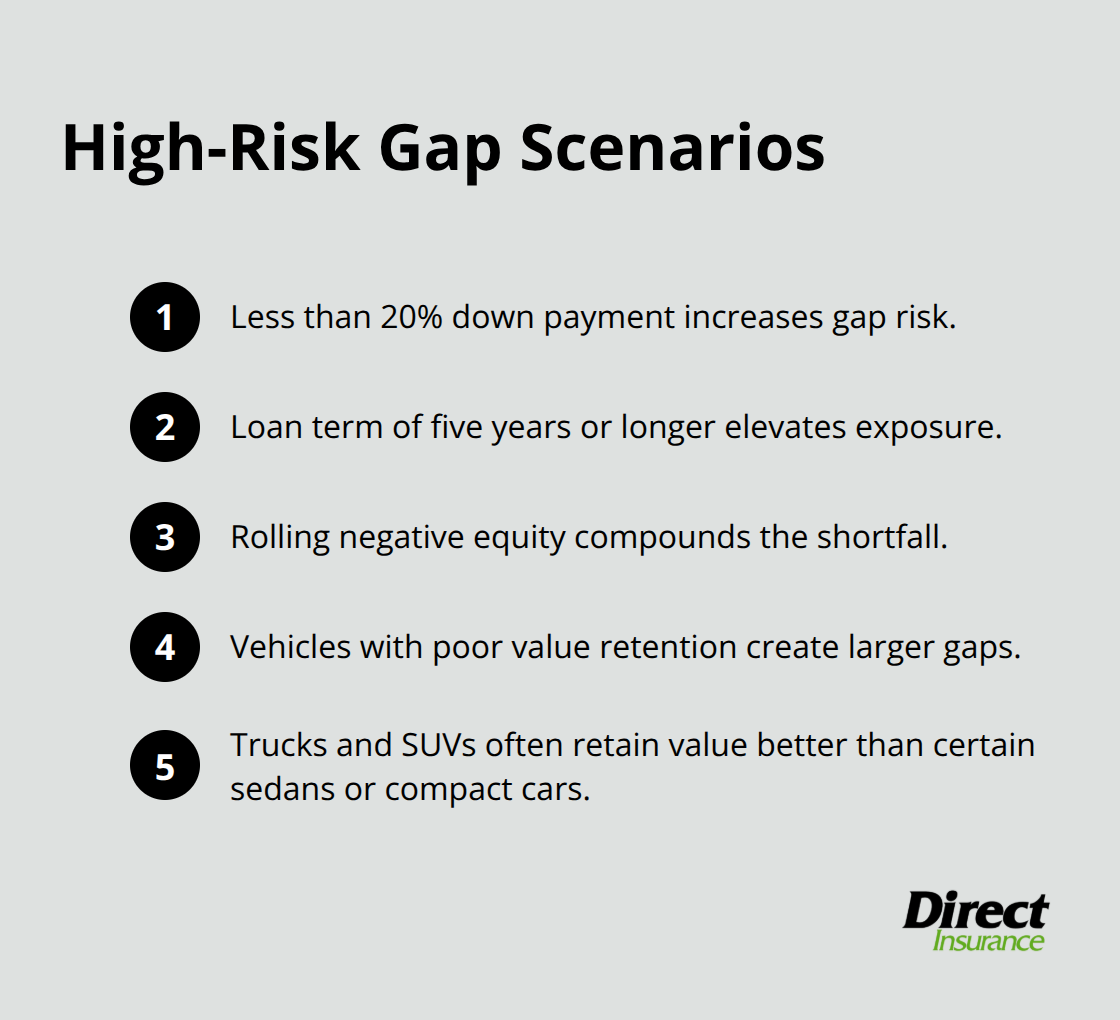

Identify Your High-Risk Scenarios

Vehicles that hold value poorly-certain sedans, compact cars, and older models-create larger gaps than trucks or SUVs. If you finance for five years or longer, you enter the danger zone regardless of vehicle type. If your down payment was below 20 percent, gap protection becomes necessary.

If you have negative equity rolled into your current loan, gap insurance protects you immediately.

The average monthly auto payment now sits at $550 for new cars and $393 for used cars, with Americans carrying over $1.2 trillion in total auto debt. These figures show how deeply financed most drivers are, making negative equity scenarios increasingly common. Leased vehicles require gap protection by default because leasing companies protect their residual value investments. Your lease agreement almost always includes gap coverage, but confirm this before signing.

Know When Gap Coverage Becomes Unnecessary

Once your loan balance drops below your car’s actual cash value, you can eliminate gap coverage and reduce your insurance costs. This typically happens in the later years of your loan term, but calculate your specific timeline based on your loan amount, interest rate, and vehicle depreciation rate. If you’re financing a vehicle with an LTV between 80 and 120 percent, gap insurance isn’t optional-it’s financially necessary.

The real indicator that you need gap protection is straightforward: if depreciation outpaces your loan payoff, you need coverage. Understanding whether gap protection applies to your situation sets the stage for exploring how to actually purchase it and what options exist in the marketplace.

How to Purchase Gap Insurance

Choose Your Source Wisely

You have three main paths to obtain gap coverage, and the route you choose significantly affects both your cost and protection level. Purchase gap insurance through your insurance company rather than at the dealership because dealer-placed gap often gets added to your loan balance and charges interest over the life of your loan. Contact your insurer directly or work with an independent agent who can quote gap coverage as a separate add-on to your existing policy. Progressive’s loan or lease payoff coverage caps protection at 25 percent of vehicle value in most states, so verify your specific state limits before committing.

When you call your insurer or get an online quote, have your loan amount, vehicle’s current market value, and loan term ready. This information lets the agent calculate your exact gap exposure and recommend appropriate coverage limits. Most insurers quote gap coverage within minutes, and you can activate it immediately, sometimes even before you take possession of the vehicle. If your lender requires gap insurance as a condition of financing, ask whether they accept coverage purchased through your insurance company. Many lenders accept gap coverage from your insurer, which keeps you in control of the policy and prevents unnecessary interest charges.

Act Before You Drive Off the Lot

Timing your gap purchase for maximum benefit means acting before or immediately upon taking possession of your vehicle. The gap between what you owe and what your car is worth peaks in year one when depreciation hits hardest, so waiting even a few weeks after purchase means you’ve already lost thousands in vehicle value. Your monthly cost for gap coverage typically runs between $15 and $25, depending on your vehicle type, loan amount, and location, making it far cheaper than the potential shortfall it protects against.

Once your loan balance falls below your vehicle’s actual cash value, you can drop gap coverage and eliminate this expense entirely. Calculate this timeline by comparing your loan payoff schedule against typical depreciation rates for your vehicle model. For a 72-month loan on a vehicle with high depreciation, you might carry the gap for four to five years. For a 36-month loan or a vehicle that holds value well, the gap closes faster. Some gap policies offer prorated refunds if you pay off your loan early, so verify this feature before purchasing.

Compare Insurance Company Options Against Dealer Plans

Insurance company gap coverage costs less upfront, avoids interest charges, and provides clearer claim processes because it integrates with your existing policy rather than sitting as a separate dealership product. The cost difference between purchasing through your insurer versus the dealership can exceed $200 over your loan term, making the insurance route clearly superior for most borrowers. When comparing options, ignore dealer-placed gap unless your lender absolutely requires it through that channel (and even then, ask if your lender accepts independent coverage instead).

Final Thoughts

Gap insurance protects you from a financial disaster that standard auto insurance won’t cover. If you finance or lease a vehicle, the gap between what you owe and what your car is worth during the early years of ownership represents real money you could lose in a total loss scenario. The math is straightforward: cars depreciate fastest when loan balances are highest, creating a window of vulnerability that auto insurance gap protection closes completely.

Your decision comes down to three concrete factors. First, calculate your loan-to-value ratio-if it exceeds 80 percent, gap protection becomes financially necessary rather than optional. Second, assess your vehicle’s depreciation rate and your loan term, since longer financing periods combined with rapid depreciation create the widest gaps. Third, consider your down payment size and whether you rolled negative equity into your current loan, as both signal that you need coverage.

The cost of gap coverage runs between $15 and $25 monthly, making it one of the cheapest insurance additions you can purchase. Contact us at Direct Insurance Services to discuss whether auto insurance gap protection fits your specific situation and to get an accurate quote for your vehicle and loan. We shop multiple top-rated insurance companies to find you the best coverage at competitive rates.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation