Utah Water Damage Coverage: Safeguarding Your Home From Leaks and Floods

Water damage ranks among the costliest homeowner insurance claims in Utah, with winter pipe bursts and spring flooding creating thousands of dollars in repairs annually. At Direct Insurance Services, we’ve helped countless Utah homeowners understand their water damage coverage options and protect their properties before disaster strikes.

Your home faces unique water risks depending on where you live in Utah-from basement seepage in older neighborhoods to flash flooding in canyon areas. The right Utah water damage coverage can mean the difference between a manageable claim and financial hardship.

What Water Threats Does Utah Actually Face

Utah’s water damage risks extend far beyond what most homeowners expect, and the problem intensifies during specific seasons. Salt Lake City experienced significant flooding in 2021 in areas residents never thought vulnerable, proving that water damage doesn’t respect traditional flood zone boundaries. Winter brings a different threat entirely-when temperatures drop below freezing, water trapped in pipes expands and ruptures, causing thousands of dollars in damage to homes across the state. These pipe bursts happen in walls, basements, and crawl spaces where homeowners can’t see them until water starts pooling on floors or appearing as dark stains on ceilings. Spring snowmelt combines with heavy precipitation to create flash flooding in canyon areas and low-lying neighborhoods, while summer monsoons dump inches of rain in minutes. The National Flood Insurance Program reports that from 2014 to 2018, over 40 percent of flood insurance claims occurred outside high-risk areas, which means your home faces real danger even if it’s not in an official flood zone.

Winter Pipe Damage Costs Real Money

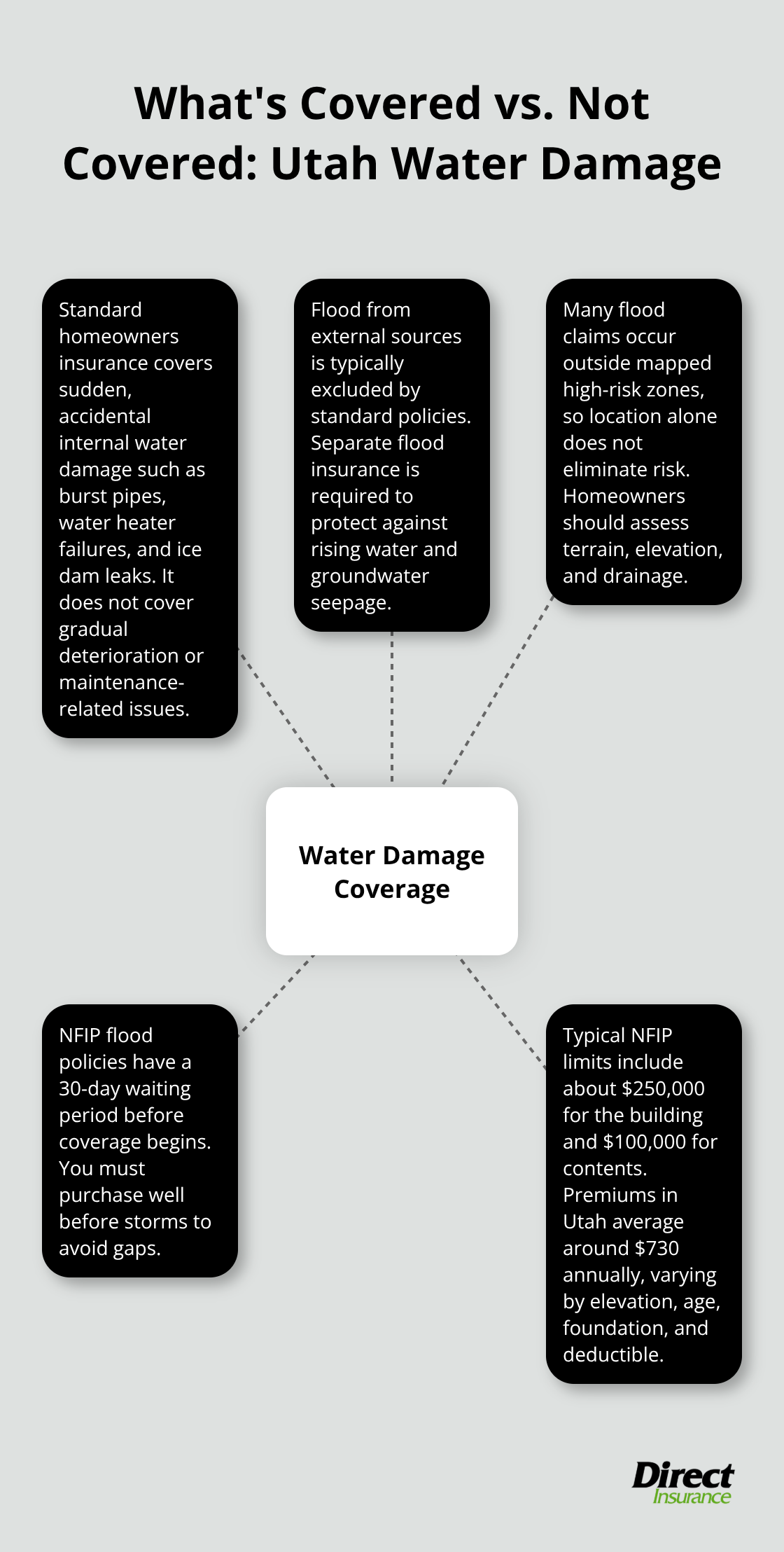

A single burst pipe causes $5,000 to $70,000 in damage depending on location and how long water flows before you notice it. Older homes with copper or galvanized steel pipes face particular vulnerability, and homes in uninsulated crawl spaces or exterior walls experience burst pipes far more frequently than well-insulated properties. Standard homeowners insurance covers internal water damage from burst pipes, but only if the damage results from a sudden, accidental event-not from gradual deterioration or lack of maintenance. Homes without proper insulation around pipes (especially those built before 1980) face the highest winter risk.

Foundation Seepage and Basement Problems

Foundation cracks develop naturally as homes settle, but Utah’s freeze-thaw cycles accelerate the process. Water seeping through foundation cracks or basement walls causes mold growth, structural weakening, and damage to stored items. Just one inch of floodwater causes up to $25,000 in damage according to FEMA data, making even minor basement seepage a serious financial threat. Homes with older foundations or those built on clay soils experience the worst seepage problems because water doesn’t drain away quickly.

Why Your Location Matters More Than You Think

Even homes outside mapped flood zones face significant water damage risk from multiple sources. Heavy rainfall, rising water, and groundwater seeping through foundations trigger flood coverage regardless of your address. Utah’s terrain (canyon proximity, elevation, and soil composition) determines how quickly water moves toward your property and how effectively it drains away. Understanding your specific location’s water behavior helps you select appropriate coverage limits and prevention measures.

Understanding Your Water Damage Coverage

What Standard Homeowners Insurance Actually Covers

Standard homeowners insurance covers water damage from sudden, accidental events inside your home-burst pipes, water heater failures, and ice dam leaks qualify for protection. However, flood damage from external sources like rising water, heavy rainfall, or groundwater seeping through your foundation is typically not covered on a standard homeowners insurance policy. This distinction matters enormously in Utah because homeowners often discover too late that their standard policy leaves them exposed to the water threats most likely to affect their properties.

The National Flood Insurance Program reports that over 40 percent of flood claims from 2014 to 2018 occurred outside mapped high-risk zones, meaning your home could face serious flood risk regardless of its location. Standard policies also exclude gradual damage from poor maintenance, slow leaks, or moisture accumulation over time-only sudden events trigger coverage.

Why Flood Insurance Fills the Gap

Separate flood insurance is your solution, and Utah residents need to understand how it works before disaster strikes. The National Flood Insurance Program offers policies that cover structure damage, personal belongings, and cleanup costs, with typical building limits around $250,000 and contents coverage around $100,000. The average annual cost in Utah runs approximately $730, though your specific premium depends on elevation, flood risk location, building age, foundation type, and your chosen deductible.

The 30-Day Waiting Period Changes Everything

Here’s the critical part: flood policies have a 30-day waiting period before coverage takes effect, so purchasing now protects you against future floods while waiting for your policy to activate. This waiting period means you cannot wait until storm clouds gather or heavy rain forecasts arrive-you must act in advance to avoid coverage gaps when water threatens your home.

Customizing Your Flood Coverage

You can customize coverage by selecting structure-only protection, contents-only coverage, or both, and you can increase limits beyond standard amounts if your home or belongings warrant higher protection. Choosing a higher deductible lowers your premium significantly but increases your out-of-pocket costs after a flood occurs.

Shopping for the Best Rates and Coverage

Independent agents give you access to multiple providers instead of settling for a single insurer’s rates, which means comparing 50 or more top-rated options to find the best value for your specific situation and risk profile. This comparison process reveals significant premium differences between providers-sometimes hundreds of dollars annually for identical coverage-making the shopping effort worthwhile. Your elevation, terrain, building materials, and foundation type all influence which insurers offer the best rates for your property, so working with an agent who understands Utah’s unique geography and water risks matters far more than you might expect.

How to Stop Water Before It Enters Your Home

Maintain Your Roof and Gutters as Your First Defense

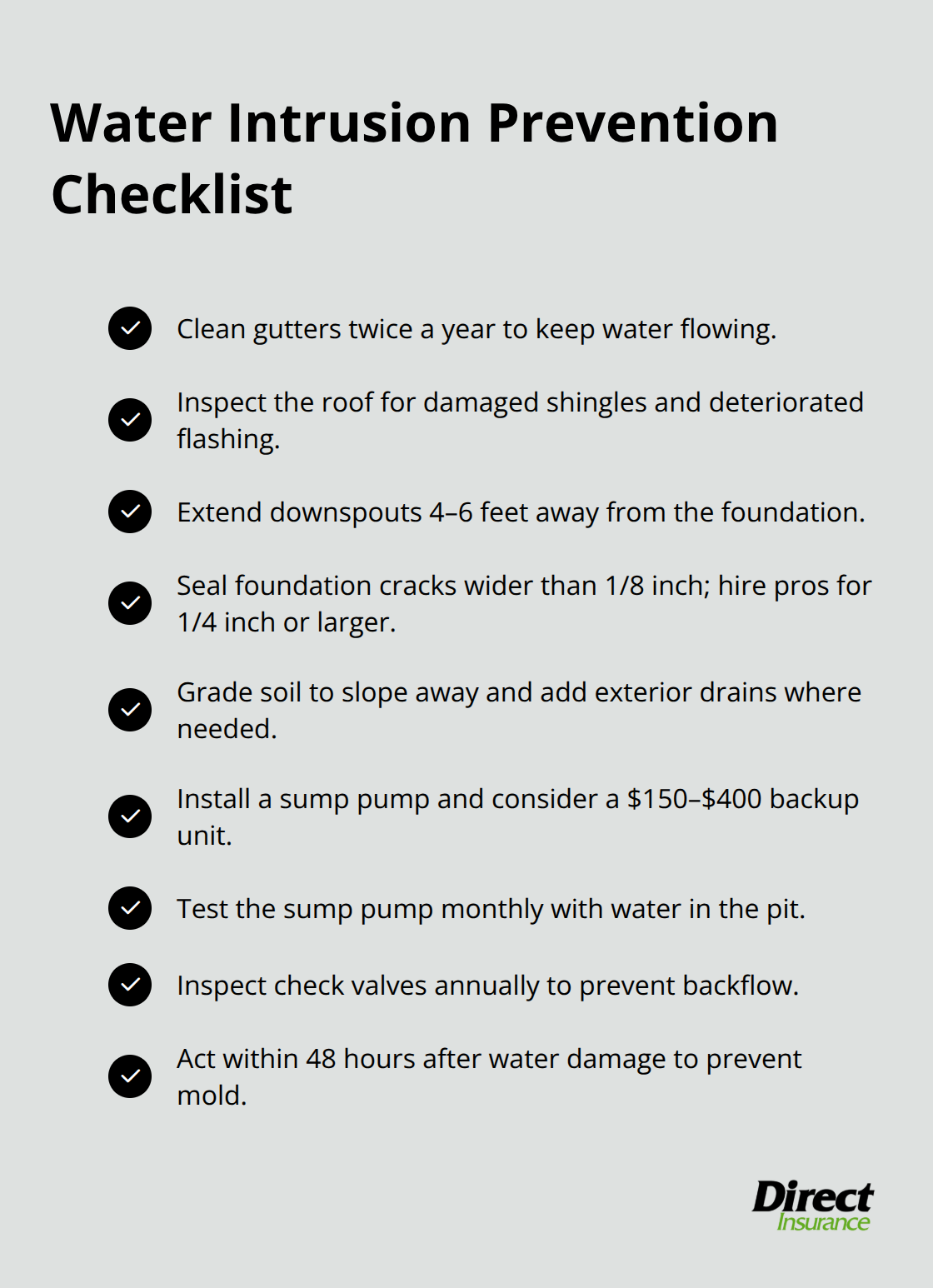

Your roof and gutters form the first line of defense against water damage, yet most Utah homeowners neglect them until leaks appear inside their homes. Gutters clogged with debris force water to back up under roofing materials, creating the perfect conditions for slow seepage into attics and walls where damage goes unnoticed for months. You should inspect gutters at least twice yearly-once after spring winds clear pollen and debris, and again before winter to prevent ice dam formation that forces water under shingles. Look for sagging sections, missing fasteners, and areas where water pools instead of flowing toward downspouts; these spots indicate improper slope that allows standing water to penetrate your roof structure. Downspouts must extend at least four to six feet away from your foundation to direct water away from basement walls and crawl spaces. Utah’s dry climate makes homeowners complacent about gutter maintenance, but when heavy rain or snowmelt arrives, inadequate drainage channels water directly toward your foundation where it causes the expensive seepage problems discussed earlier.

Roof inspections should focus on missing or damaged shingles, deteriorated flashing around chimneys and vents, and granule loss that indicates aging roofing materials losing their water-shedding ability. If your roof exceeds 15 years old, hire a professional for inspection before winter arrives, particularly if you live in areas prone to heavy snow or ice dams.

Seal Foundation Cracks and Prevent Basement Seepage

Foundation cracks and basement seepage require a different prevention strategy because water moves through soil toward your foundation regardless of roof condition. Walk around your foundation perimeter and look for visible cracks wider than one-eighth inch; these openings allow groundwater and surface runoff to enter your basement directly. Seal cracks yourself using concrete caulk for small gaps, but hire a professional for cracks wider than one-quarter inch or cracks that show water seeping through them currently. Interior waterproofing solutions like sump pumps and drainage systems work after water enters, but exterior solutions prevent water from reaching your foundation in the first place-grading soil away from your foundation, installing exterior drain tile, and directing downspouts away from the house all cost less than fixing interior water damage.

Install Sump Pumps and Drainage Systems

If you live in a basement-level home or an older property with clay soil that drains poorly, sump pump installation becomes essential rather than optional. A backup sump pump typically costs $150 to $400, plus installation fees-a small investment compared to the potential expense of water damage repairs. Test your sump pump monthly by pouring water into the pit to confirm it activates and drains properly; many homeowners discover their pumps are broken only after water starts pooling on basement floors. Check valves on sump pump discharge lines prevent floodwater from backing up into your pump through the discharge pipe, so inspect these valves annually to confirm they open and close freely. Without these three prevention layers-maintained gutters and roof, sealed foundation cracks, and functioning drainage systems-you leave your home vulnerable to water damage rather than actively protecting against it.

Act within 48 hours of water damage to prevent mold growth and additional complications.

Final Thoughts

Water damage threatens Utah homes year-round, but you don’t have to face this risk alone. The prevention steps we’ve covered-maintained gutters, sealed foundations, and functioning drainage systems-form your first defense, yet they work best alongside proper insurance coverage. Your standard homeowners policy leaves gaps that flood insurance fills, and the 30-day waiting period means acting now protects you when water threatens later.

At Direct Insurance Services, we understand how elevation, terrain, and location shape your water damage risk. We shop multiple top-rated insurance companies to find Utah water damage coverage that matches your specific situation and budget. Contact Direct Insurance Services today to discuss your water damage coverage options and identify any gaps in your current protection.

Our agents will review your current policies, explain what flood insurance actually covers, and help you choose protection that fits your home and budget without overpaying for unnecessary coverage. We’re locals who understand Utah’s unique water threats, from winter pipe bursts to spring flooding in unexpected areas.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation