Utah Personal Umbrella Insurance: Extra Peace of Mind

A single accident on your property or a vehicle collision can expose you to liability claims that exceed your home and auto insurance limits. Utah personal umbrella insurance fills that gap, protecting your assets when the unexpected happens.

At Direct Insurance Services, we’ve seen how quickly financial security can disappear without proper coverage. This guide walks you through what umbrella policies cover, how much protection you actually need, and real situations where this coverage has saved Utah families from devastating losses.

Understanding Umbrella Insurance and Why Utah Needs It

Personal umbrella insurance is a liability policy that activates after your home and auto insurance limits are exhausted. When a lawsuit or claim exceeds what your standard policies cover, your umbrella kicks in to pay the difference, up to your chosen limit. Most umbrella policies start at $1 million in coverage and typically cost between $300 and $500 per year for that level of protection, according to reports from Forbes and ACE Private Risk Services. The policy covers legal defense costs, judgments, and settlements across multiple underlying policies-your car, home, and other insured assets. It also covers claims your standard policies exclude, such as libel, slander, false arrest, and landlord liability if you own rental property. What umbrella insurance does not cover is your own injuries, your own property damage, or liability you assume through a contract.

Utah’s Accident and Injury Landscape

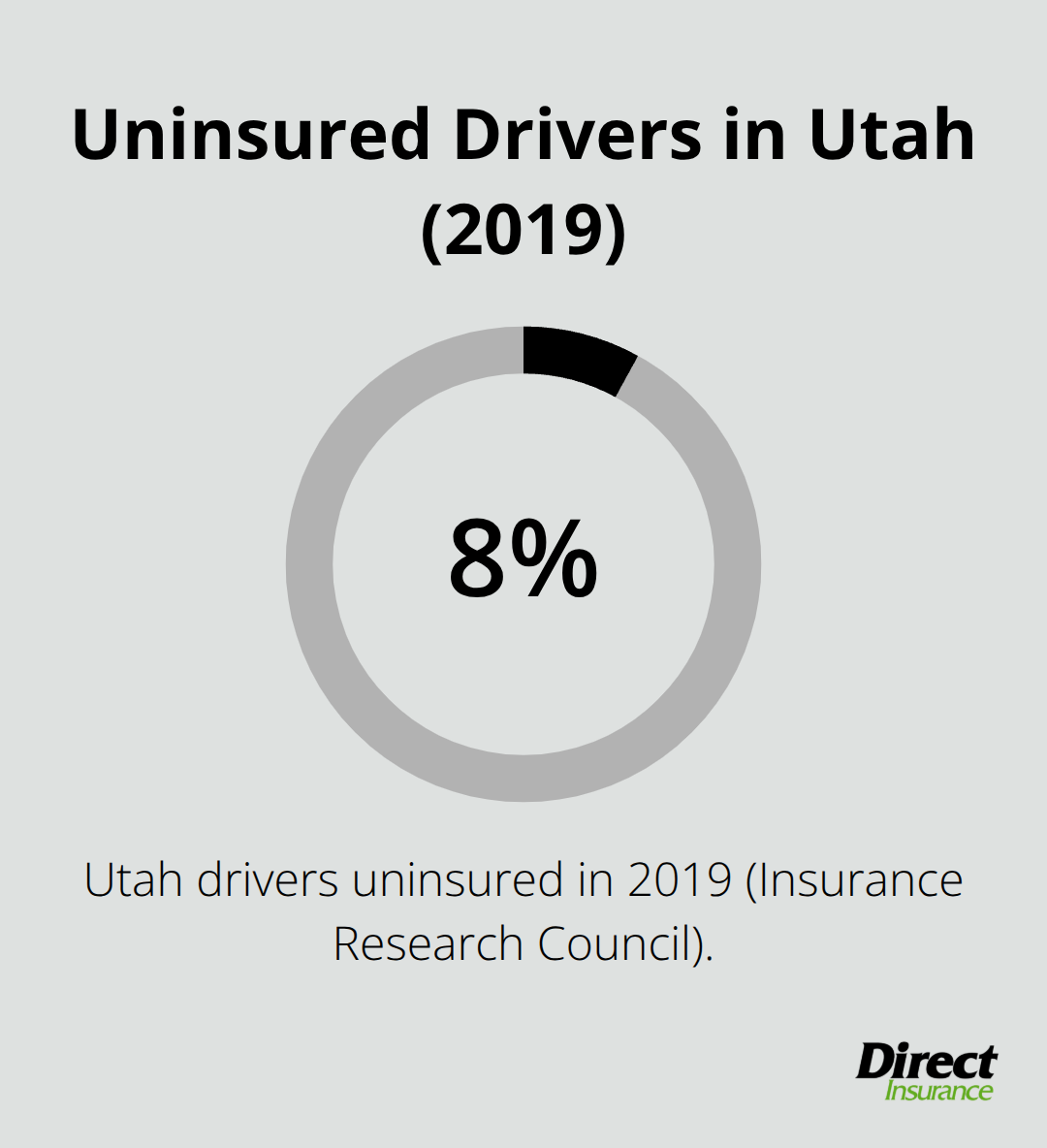

Utah residents face specific liability risks that make umbrella coverage essential rather than optional. Accidental injuries are the leading cause of death for Utah residents aged 1 to 44, according to the Utah Department of Health. In 2019 alone, Utah recorded 17,930 traumatic injury cases and 2,042 deaths from injuries. Beyond accidents, the Insurance Research Council reported that 8.2% of Utah drivers were uninsured in 2019, meaning one in twelve drivers on Utah roads carries no liability protection. If an uninsured driver hits you and causes significant damage, your own umbrella policy cannot help-but if you cause the accident, your umbrella protects your assets from their claims.

Outdoor recreation defines Utah’s culture, and activities like hiking, skiing, and water sports increase exposure to accidents involving guests and family members on your property.

How Umbrella Fills the Gaps Your Current Policies Leave

Your homeowners and auto policies have built-in limits. Standard homeowners liability typically caps at $300,000 to $500,000, while auto liability often sits at $250,000 to $500,000. A single serious injury claim can shatter these limits instantly. A 2025 Utah settlement in a high-speed rear-end crash reached $4.3 million, and a birth-injury verdict that same year topped $950 million-verdicts and settlements that dwarf standard policy limits. Utah law caps non-economic damages in medical malpractice cases at $450,000, but economic damages for medical costs, lost wages, and future care multiply quickly. An umbrella policy raises your car or homeowner insurance liability limits based on your total assets and risk exposure. If your auto liability is $300,000 and a claim reaches $500,000, your umbrella covers the remaining $200,000. The cost to add that extra protection is far cheaper than raising your underlying policy limits across multiple policies.

Assessing Your Actual Exposure

Your assets, property, vehicles, and lifestyle determine how much umbrella coverage you actually need. Someone with significant savings, a home, and multiple vehicles faces greater exposure than a renter with minimal assets. Utah’s outdoor culture means many residents host gatherings on their property, increasing the risk of guest injuries. If you own rental property, landlord liability exposure adds another layer of risk. The right coverage amount protects your wealth without forcing you to pay for unnecessary limits. Utah families benefit from working with an agency that understands local risks and can match coverage to their specific situation rather than applying generic formulas.

How Much Umbrella Coverage Do You Actually Need

Calculate Your Assets First

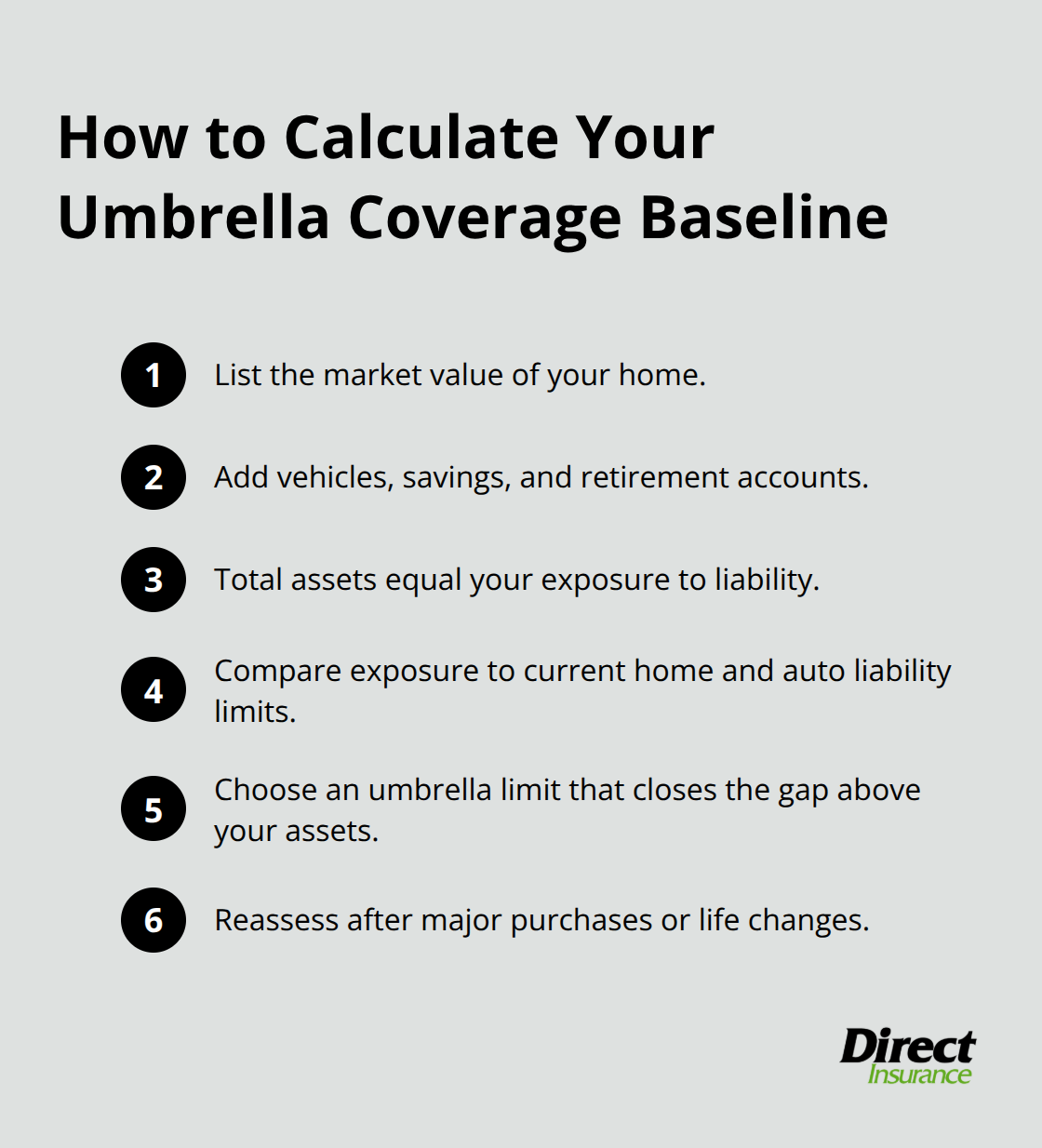

Starting at $1 million in liability protection, umbrella policies force you to make a deliberate choice about your coverage amount rather than defaulting to whatever feels safe. Calculate your actual exposure first. Add up your home value, vehicles, savings, and retirement accounts-this is what you’re protecting. If you own a $400,000 home, two vehicles, and have $200,000 in savings, you’re looking at roughly $600,000 in assets that could be at risk from a single lawsuit.

A umbrella policy costs around $250 to $550 annually, making it the most cost-effective way to shield that wealth.

Why $1 Million Often Falls Short

Jumping to $2 million in coverage typically costs only about $75 more per year, which undercuts the price of raising your underlying auto and home liability limits separately. Utah’s 2025 verdicts and settlements prove that modest coverage amounts disappear fast-the $4.3 million rear-end settlement and nearly $950 million birth-injury verdict show how real claims explode beyond standard homeowner and auto limits. Your underlying policies usually sit at $300,000 to $500,000 in liability, so anything above that threshold flows directly to your umbrella. Most Utah families with homes and multiple vehicles should consider $1 million to $2 million as their minimum baseline, with higher amounts for those hosting frequent gatherings or owning rental property.

What Drives Your Premium in Utah

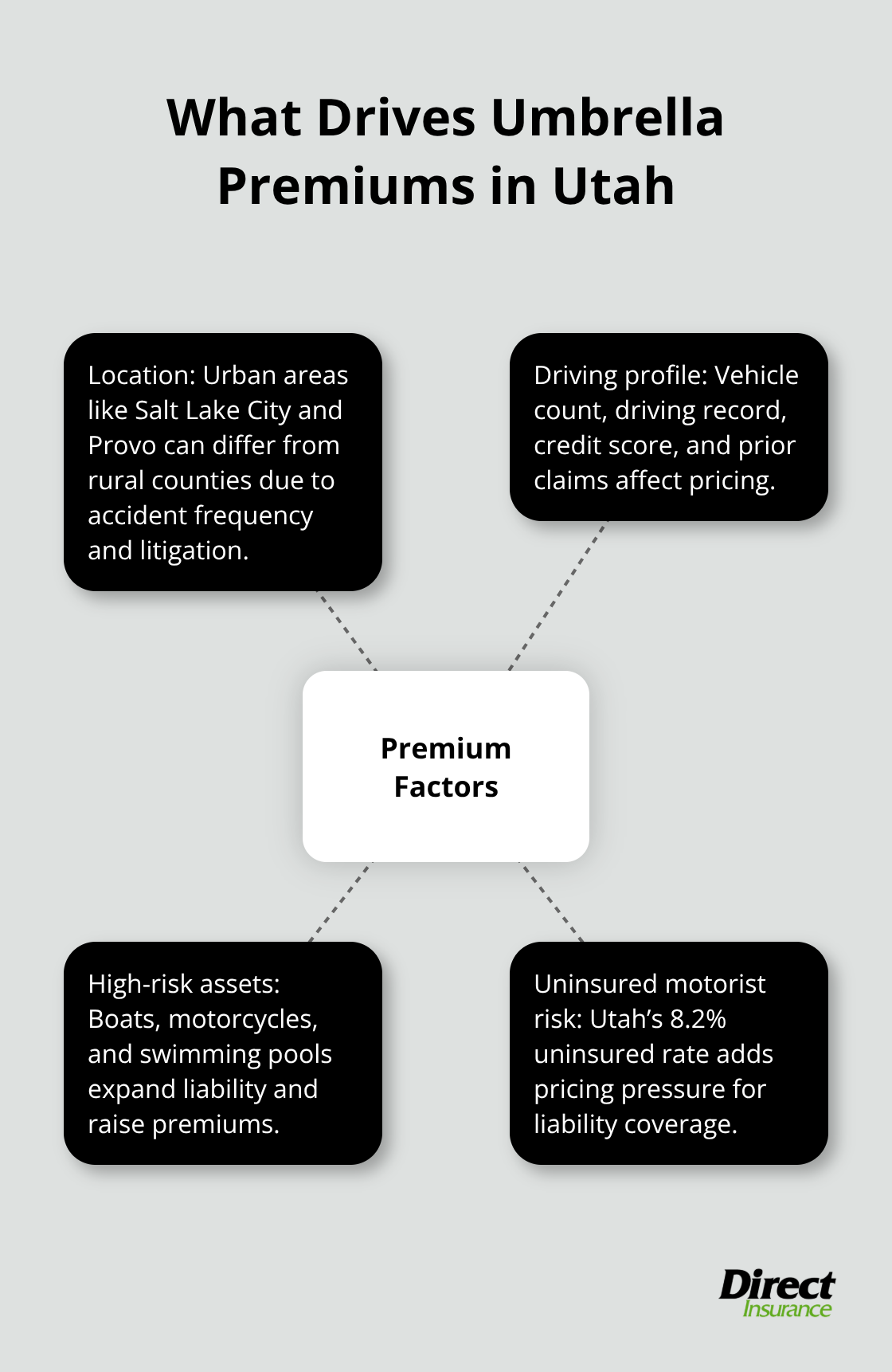

Your specific premium hinges on factors that vary dramatically across Utah’s geography and lifestyle. Location matters significantly-urban areas like Salt Lake City and Provo may see different rates than rural counties due to accident frequency and litigation patterns. The number of vehicles you insure, your driving history, credit score, and claims history all influence what you’ll pay.

Owning multiple high-risk assets like boats, motorcycles, or swimming pools increases premiums because they expand your liability exposure. Utah’s uninsured motorist rate of 8.2% according to the Insurance Research Council means you face genuine risk from underinsured drivers, which insurers factor into pricing.

Shop Multiple Carriers for Better Rates

When comparing quotes, don’t just look at the annual premium-verify what minimum underlying policy limits each insurer requires before attaching their umbrella. Some carriers demand $500,000 in auto liability and $500,000 in homeowner liability before qualifying for umbrella coverage, while others set lower thresholds. The differences between providers can be substantial, so shopping multiple insurers rather than accepting your current agent’s quote alone could save you hundreds annually while securing better terms. An independent agency that works with multiple top-rated insurance companies ensures you get competitive pricing matched to your actual risk profile rather than a one-size-fits-all approach.

Understanding Minimum Coverage Requirements

Before you finalize your umbrella limits, your insurer will specify the minimum underlying coverage you must maintain. These thresholds protect the umbrella carrier from excessive claims on weak foundations. Verify these requirements early in your shopping process, as they directly affect your total insurance costs and the protection you actually receive. Once you understand your asset exposure and the minimum requirements your chosen carrier imposes, you’re ready to explore the real-world situations where umbrella coverage makes the difference between financial stability and devastating loss.

Real-World Scenarios Where Umbrella Insurance Protects Utah Families

Property Accidents and Guest Injuries

A guest slips on ice outside your home and breaks their leg. Medical bills reach $180,000, and they file a lawsuit claiming permanent nerve damage. Your homeowners liability limit is $300,000, so you think you’re safe. But the plaintiff’s attorney argues for non-economic damages related to chronic pain, lost wages, and reduced quality of life. The final judgment comes in at $680,000. Without umbrella coverage, you owe $380,000 out of pocket. This scenario plays out regularly across Utah. In 2023, a Utah case awarded $150,747 with $84,000 in past medical expenses alone, showing how quickly medical costs drive up claim values. In 2020, a single-vehicle crash produced a $750,000 verdict when the claimant developed post-traumatic stress disorder.

Vehicle Collisions and Multi-Passenger Claims

You turn left at an intersection when another car runs a red light and t-bones your vehicle. Three passengers in the other car suffer injuries. The at-fault determination is clear, but damages aren’t. One passenger needs spinal fusion surgery costing $120,000. Another develops chronic headaches requiring ongoing treatment. A third experiences anxiety and depression from the accident. Combined, their claims total $520,000. Your auto liability is $500,000. Your umbrella policy covers the remaining $20,000, protecting your home, savings, and future earnings. A 2025 Utah settlement in a high-speed rear-end crash reached $4.3 million, which exceeded most standard auto policy limits by a massive margin. Even more modest cases add up fast. A 2019 Utah verdict involved a FedEx van in a rear-end collision that produced a $30,000 verdict initially, but the claimant later needed a spinal cord stimulator, escalating total treatment costs substantially.

Dog Bites and Pet Liability

Dog bites and pet-related incidents represent another major category where umbrella policies prevent financial catastrophe. Utah dog bite law follows a broad liability framework, meaning you’re responsible for injuries your dog causes regardless of the animal’s prior behavior or your intent. A dog bite requiring reconstructive facial surgery can cost $50,000 to $100,000 in immediate medical care. Add infection complications, psychological counseling for trauma, and permanent scarring claims, and you’re easily at $200,000 to $300,000 in damages. Your homeowners policy typically covers dog bites up to your liability limit, but anything exceeding that threshold falls to your umbrella.

Swimming Pools, Trampolines, and Catastrophic Claims

Swimming pools and trampolines on your property create similar exposure. A child guest drowns or suffers a spinal injury from a trampoline accident. Wrongful death claims or permanent disability claims routinely exceed $1 million in Utah. The 2017 Utah nursing home bedsores case yielded $1,833,000, and a death following aortic dissection at a hospital reached $2,940,250, illustrating how Utah juries and judges value serious injury and death claims. You cannot predict which accident will be the one that devastates your finances. What you can control is whether you have adequate coverage when it happens.

Final Thoughts

Utah personal umbrella insurance protects your assets when a single accident or lawsuit threatens everything you’ve built. The scenarios throughout this guide aren’t hypothetical-they’re based on real Utah verdicts and settlements that prove standard homeowners and auto policies fall short. A $4.3 million rear-end settlement, a $750,000 verdict from post-traumatic stress disorder, and a $1.8 million nursing home case all demonstrate that liability exposure in Utah is substantial and unpredictable.

The financial math is straightforward. A $1 million umbrella policy costs $300 to $500 annually, while raising your underlying auto and homeowner liability limits separately would cost significantly more. Adding $2 million in coverage typically runs only $75 extra per year. For most Utah families with homes, multiple vehicles, and property where guests gather, $1 million to $2 million in umbrella coverage represents the minimum baseline protection that makes sense for your situation.

Contact Direct Insurance Services to get a quote and discover exactly what coverage you need. We’ve helped Utah families and businesses find the right protection at competitive rates since 1973, and our local expertise means we understand how outdoor recreation, uninsured motorist rates, and Utah’s litigation environment affect your actual exposure.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation