Rent Property Insurance Utah: Is It Right for Your Landlord Needs?

Owning rental property in Utah comes with real financial exposure. Weather damage, tenant injuries, and unexpected vacancies can drain your profits fast.

Standard homeowners insurance won’t protect your rental income or cover liability from tenants. At Direct Insurance Services, we help landlords get rent property insurance Utah that actually matches their risks.

What Landlord Insurance Actually Covers in Utah

Landlord insurance protects the building itself, your liability when someone gets injured on the property, and your rental income if the place becomes uninhabitable. The dwelling coverage pays for structural damage from fire, wind, theft, or vandalism-but only the building, not tenant belongings. You also receive liability protection that covers medical bills and legal costs if a tenant or visitor sues you for injuries. Loss-of-rental-income coverage reimburses you for lost rent while repairs happen, typically for 12 to 24 months. If you own furnished rentals or leave equipment on-site for tenant use (like lawnmowers or tools), that personal property coverage extends to those items too.

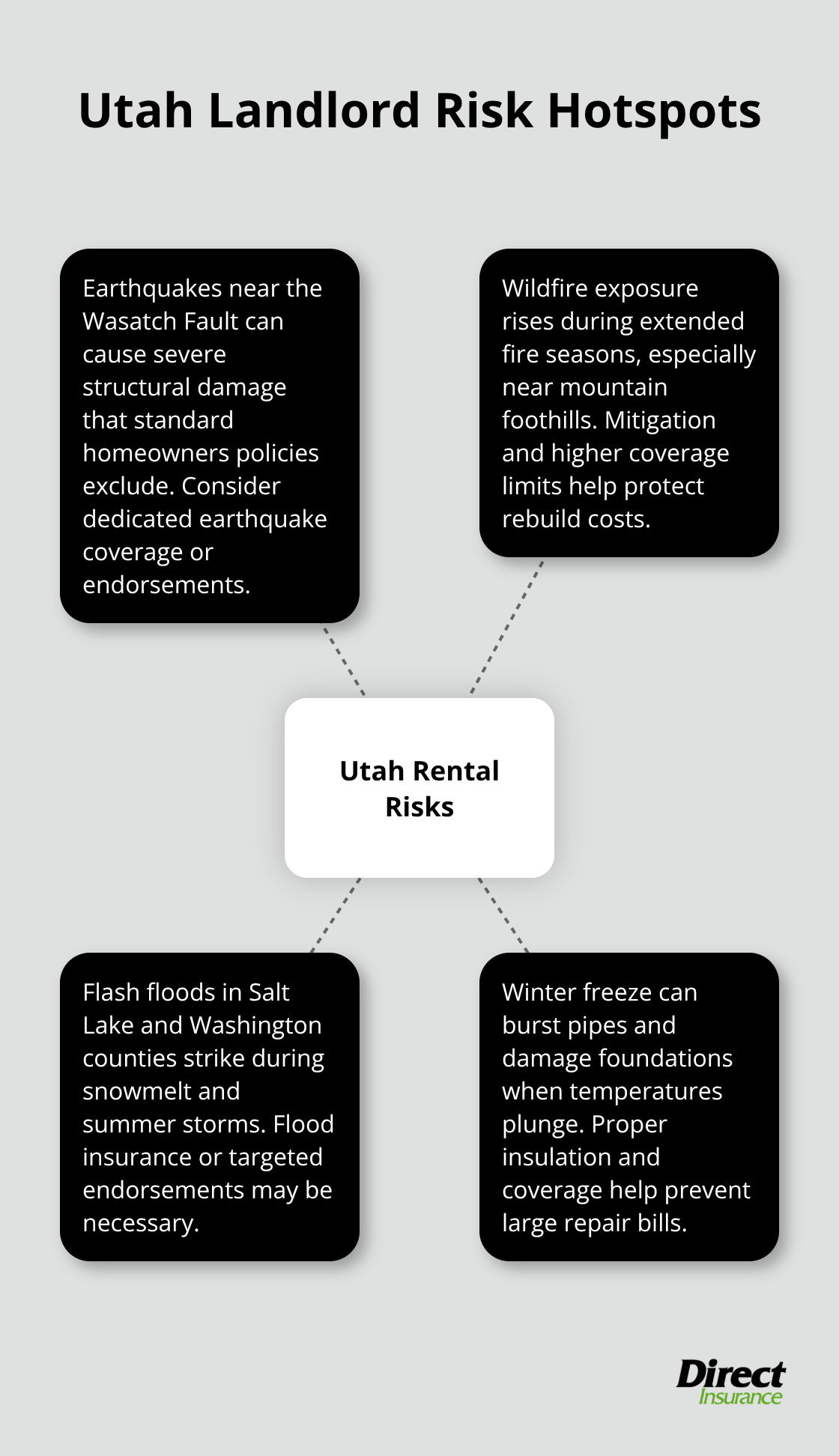

Utah’s Unique Geographic Risks

Utah landlords face specific risks that standard policies ignore: earthquake exposure near the Wasatch Fault, wildfire danger from nearby mountains, flash floods in Salt Lake and Washington counties, and winter freeze damage. According to BiggerPockets analysis, Utah landlord insurance costs about $913 per year on average, making it one of the five most affordable states in the country. St. George averages around $700 yearly, while Moab runs about $650, both well below the national median of $1,300.

How Landlord Policies Differ from Homeowners Coverage

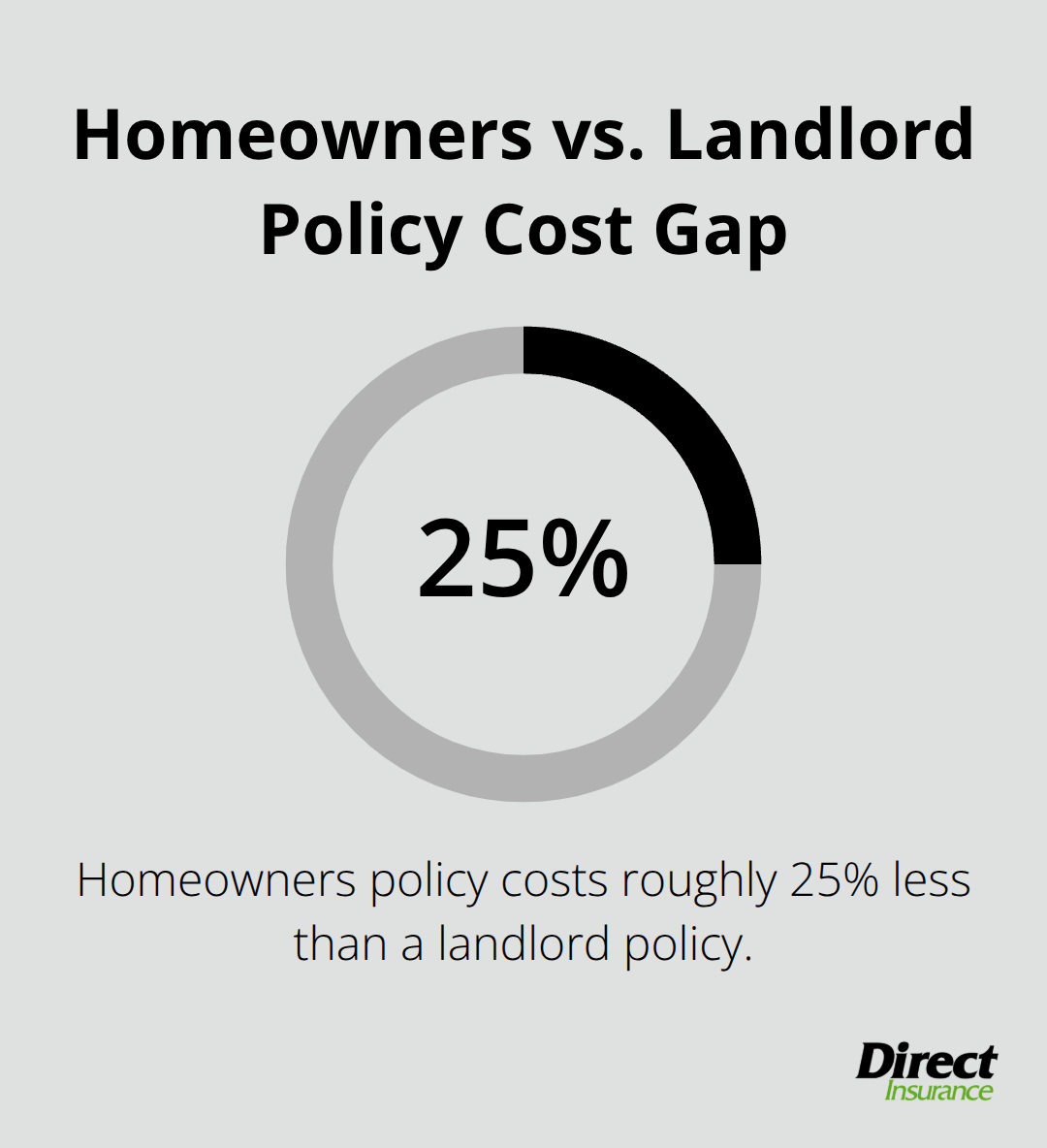

Standard homeowners insurance explicitly excludes rental income loss and tenant-caused damage. If a tenant punches a hole in the wall or floods the kitchen, your homeowners policy will deny the claim. Landlord policies cover exactly these scenarios because they account for the fact that someone else lives there and uses the space differently. Liability limits also differ significantly-homeowners policies typically cap out at $300,000, but Utah landlords should carry at least $1 million in liability protection given that average claims run around $47,000 per incident. A homeowners policy costs roughly 25% less than a landlord policy, but that savings disappears the moment a tenant-related claim gets denied and you foot the bill yourself.

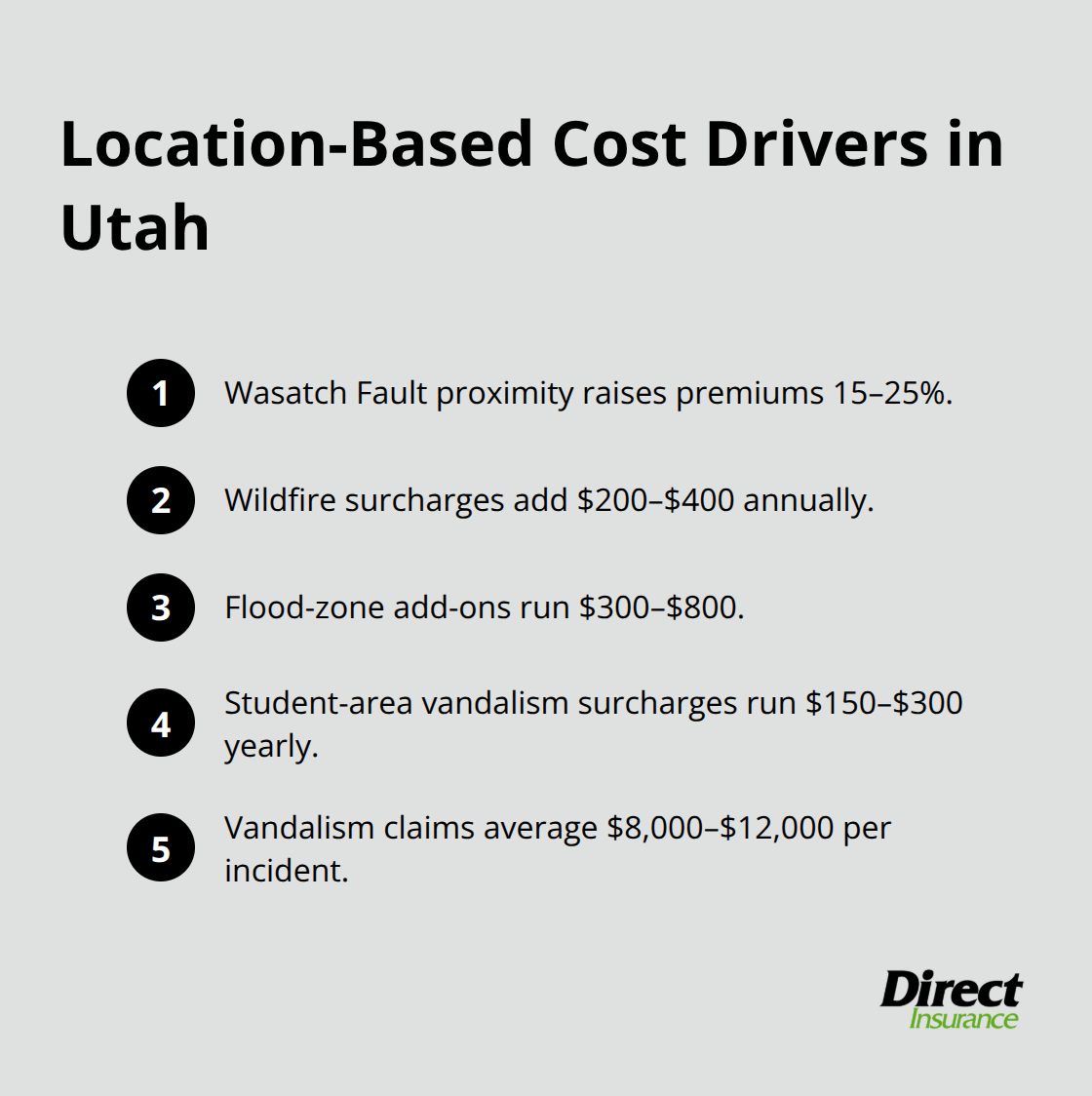

Location-Based Premium Factors

Utah’s geography creates insurance costs that vary wildly by location. Properties near the Wasatch Fault see premiums jump 15 to 25% higher than those in safer zones. Wildfire surcharges add $200 to $400 annually for properties in exposed areas, while flood-zone add-ons run $300 to $800 depending on risk. Vandalism surcharges in student rental areas like Salt Lake City run $150 to $300 per year because claims average $8,000 to $12,000 per incident.

Property Condition and Tenant Screening Impact

Property age and construction materials shift costs dramatically-homes built before 1980 face premiums 20 to 35% higher than newer construction. Brick veneer generally insures better than wood frame, and galvanized plumbing adds about $200 yearly while roofs older than 15 years raise rates another 10 to 20%. Tenant screening impacts your rate too: thorough tenant screening yields 5 to 15% premium discounts, and requiring renters insurance with at least $300,000 in liability can cut your premiums 10 to 25%. These variables mean your actual cost depends on what you own and who you rent to-not just where you own it.

What Threatens Your Utah Rental Income Most

Weather and Natural Disasters Drain Rental Properties Fast

Weather and natural disasters pose the most immediate threat to Utah rental properties, and the costs are far from theoretical. The Wasatch Fault runs directly through populated rental areas, creating earthquake risk that standard homeowners policies won’t touch. Wildfire season in Utah now extends into fall, with properties near the Wasatch Mountains facing real burn exposure. Flash flooding hits Salt Lake and Washington counties regularly during spring snowmelt and summer storms.

Winter freeze damage cracks pipes and ruins foundations when temperatures plummet. Vandalism claims in student rental areas can result in significant losses, which means a single destructive tenant can wipe out months of profit. These aren’t rare edge cases-they’re predictable costs in Utah’s rental market. Standard homeowners policies exclude most tenant-caused damage, so you absorb the full expense yourself unless you have landlord coverage.

Liability Claims Hit Harder Than Most Landlords Expect

Liability claims from tenant injuries strike with force that catches many landlords off guard. A tenant slips on ice in winter, breaks a leg, and sues for lost wages plus medical bills. A guest at a tenant’s party falls down poorly lit stairs and demands $100,000 in damages.

These scenarios happen regularly, and your liability limits disappear fast when legal costs stack up alongside injury payouts. Utah landlords should carry at least $1 million in liability coverage, with umbrella policies of $1 to $2 million if you own multiple units. Medical payments coverage of $5,000 to $10,000 can actually prevent formal lawsuits by covering minor injuries without triggering liability claims.

Loss of Rental Income Creates Cash Flow Crises

Loss of rental income represents the third major threat that landlords often underestimate. A fire makes the property uninhabitable, and you lose rent for months while repairs happen. Loss-of-rental-income coverage reimburses you for 12 to 24 months of rent, but typical restoration takes 4 to 6 months for fire damage and 2 to 3 months for water damage. Without this coverage, you pay the mortgage and property taxes while earning nothing, draining cash flow when you need it most.

The financial impact compounds quickly across multiple properties. A single $2,000 monthly rental income loss over six months costs you $12,000 in unreimbursed expenses. When you multiply that across a portfolio, the gap between adequate coverage and inadequate coverage becomes staggering. Understanding these three threats-property damage, liability exposure, and income loss-shapes what coverage limits you actually need.

How to Choose the Right Landlord Insurance Policy

Document Your Property and Tenant Profile

Start by listing exactly what you own and who will live there, because these details determine your actual insurance needs. Walk through your rental property and record the dwelling’s square footage, construction year, materials, and roof condition. Note whether you’ll furnish it, what appliances or equipment you’ll leave on-site, and what type of tenant you’ll accept. A long-term single-family rental to a stable family carries different risks than a furnished mid-term unit renting to transient professionals or a short-term rental in a high-vandalism zone.

Your dwelling coverage should reflect current reconstruction costs, not the purchase price-many Utah landlords underinsure by 20 to 40 percent because they anchor to what they paid years ago. If your property cost $400,000 but would cost $500,000 to rebuild today with current labor and materials, you need $500,000 in dwelling coverage. For furnished rentals or properties with expensive equipment, set personal property coverage at $25,000 to $50,000 depending on what you leave there.

Set Liability and Income Protection Limits

Liability limits should start at $1 million for a single property and climb to $1 to $2 million in umbrella coverage if you own multiple units. Loss-of-rental-income coverage should span 12 to 24 months since Utah restoration times run 4 to 6 months for fire and 2 to 3 months for water damage. Location matters enormously-properties near the Wasatch Fault need earthquake consideration, wildfire-prone areas warrant extra hazard protection, and student housing zones require higher vandalism limits.

Your tenant screening practices and property age also shift costs; thorough screening yields 5 to 15 percent discounts, while homes built before 1980 face 20 to 35 percent higher premiums than newer construction.

Compare Quotes Across Multiple Carriers

Once you know what you need, shop multiple carriers because rates vary dramatically across insurers even for identical properties. Utah’s median landlord insurance runs $913 yearly, but individual quotes can swing from $650 in Moab to $1,200 in higher-risk areas-and that’s just the geographic spread. Different carriers price earthquake, wildfire, and flood exposure differently, so one company might charge $400 extra for Wasatch Fault proximity while another charges $150.

Online quote tools can speed this up, but talk directly with an agent who understands Utah-specific risks rather than relying on automated systems alone. An independent agency based in Salt Lake City can shop multiple top-rated carriers to find competitive rates tailored to your exact property and tenant situation.

Choose Your Deductible Strategically

Compare deductibles carefully because a $2,500 deductible cuts your premium but leaves you exposed to that out-of-pocket cost on every claim. For rental properties where tenant damage happens regularly, a $1,000 deductible often makes more financial sense than saving $200 annually with a $2,500 deductible. Calculate your break-even point: if vandalism claims average $8,000 to $12,000 in student rental areas, a lower deductible protects cash flow better than premium savings.

Final Thoughts

Rent property insurance Utah protects your investment when weather, tenants, and liability claims threaten your cash flow. Standard homeowners policies leave you exposed to exactly the losses that hurt most-tenant damage, lost rental income, and liability gaps that can cost tens of thousands. The right landlord policy fills those gaps and keeps your rental business running even when disaster strikes.

Utah’s geography creates specific risks that demand specific coverage. Earthquake exposure near the Wasatch Fault, wildfire danger, flash flooding, and winter freeze damage aren’t theoretical concerns-they’re predictable costs in our market. Your property age, construction materials, tenant screening practices, and location all shift your actual premium and coverage needs. A $650 policy in Moab looks cheap until you realize it underinsures your dwelling or carries inadequate liability limits.

Shopping multiple carriers matters because rates vary dramatically even for identical properties. One insurer might charge $400 extra for Wasatch Fault proximity while another charges $150. Contact us at Direct Insurance Services for a custom quote on your rental property and stop guessing whether your coverage is adequate.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation