How to Handle Home Insurance Water Damage Claims

Water damage is one of the most common and costly claims homeowners file. At Direct Insurance Services, we know that understanding your coverage and acting fast can make the difference between a smooth claim and a financial headache.

This guide walks you through what your home insurance water damage policy actually covers, the steps to take immediately after damage occurs, and how to file a claim that gets approved.

What Your Home Insurance Actually Covers for Water Damage

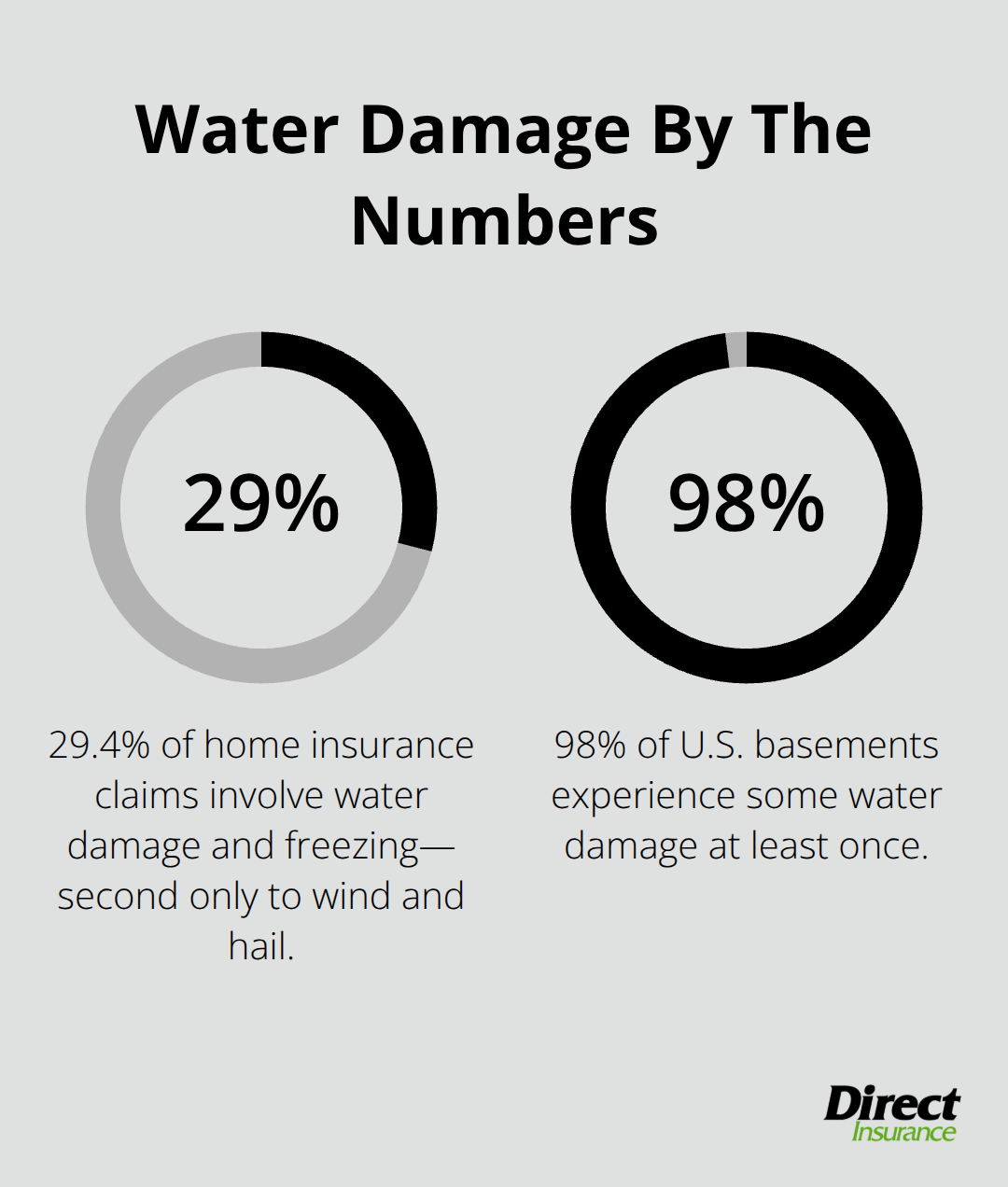

Standard homeowners insurance covers sudden, accidental water damage from burst pipes, appliance failures, roof leaks, and water used to fight fires. Water damage and freezing claims account for 29.4% of all home insurance claims, second only to wind and hail. However, your policy almost certainly excludes flood damage, which requires separate flood insurance.

This distinction matters enormously because about 98% of basements in the U.S. will experience some water damage at least once, yet most homeowners don’t realize their standard policy won’t pay for it. Your deductible applies to water damage claims just like any other claim-if you have a $1,000 deductible and $5,000 in damage, you’ll pay $1,000 out of pocket and insurance covers the remaining $4,000.

Gradual Damage Gets Rejected

Most claims fail because policies exclude slow leaks, neglect, and long-term wear and tear. If a pipe drips behind your wall for months, that’s your responsibility, not your insurer’s. Insurance companies distinguish between sudden events and gradual deterioration, and adjusters are trained to spot the difference. If you notice water stains, soft drywall, or musty smells, act immediately. The longer you wait, the harder it becomes to prove the damage was sudden rather than negligent. Fixing leaks promptly also saves money directly-the EPA reports that a typical household leak wastes up to 10,000 gallons per year, costing around $681 annually in wasted water.

Know Your Policy’s Real Limits

Most standard policies cap water damage payouts and exclude certain scenarios entirely. Pool and sump pump failures often aren’t covered unless you pay for additional endorsements. Mold damage resulting from water exposure may also fall outside your coverage. The average homeowner insurance payout for water damage is about $13,954 according to the Insurance Information Institute, but this varies dramatically based on claim class and your specific policy language. Read your actual policy document, not the summary. Call your agent and ask specifically what water damage scenarios are covered and which are excluded. Write down the answers and keep that documentation.

What Happens Next

Understanding your coverage sets the foundation for what comes after water damage strikes. The moments immediately following the incident determine whether your claim succeeds or fails, which is why the next section focuses on the critical actions you must take before you even contact your insurer.

Act Within the First 24 Hours

Water damage progresses rapidly-within minutes it absorbs into materials, within hours humidity and deterioration accelerate, and by 48 hours the situation can shift to gray water contamination from bacterial growth. Your actions in this window determine whether you recover most of your losses or face denials and secondary damage like mold.

Stop the Water and Secure Your Safety

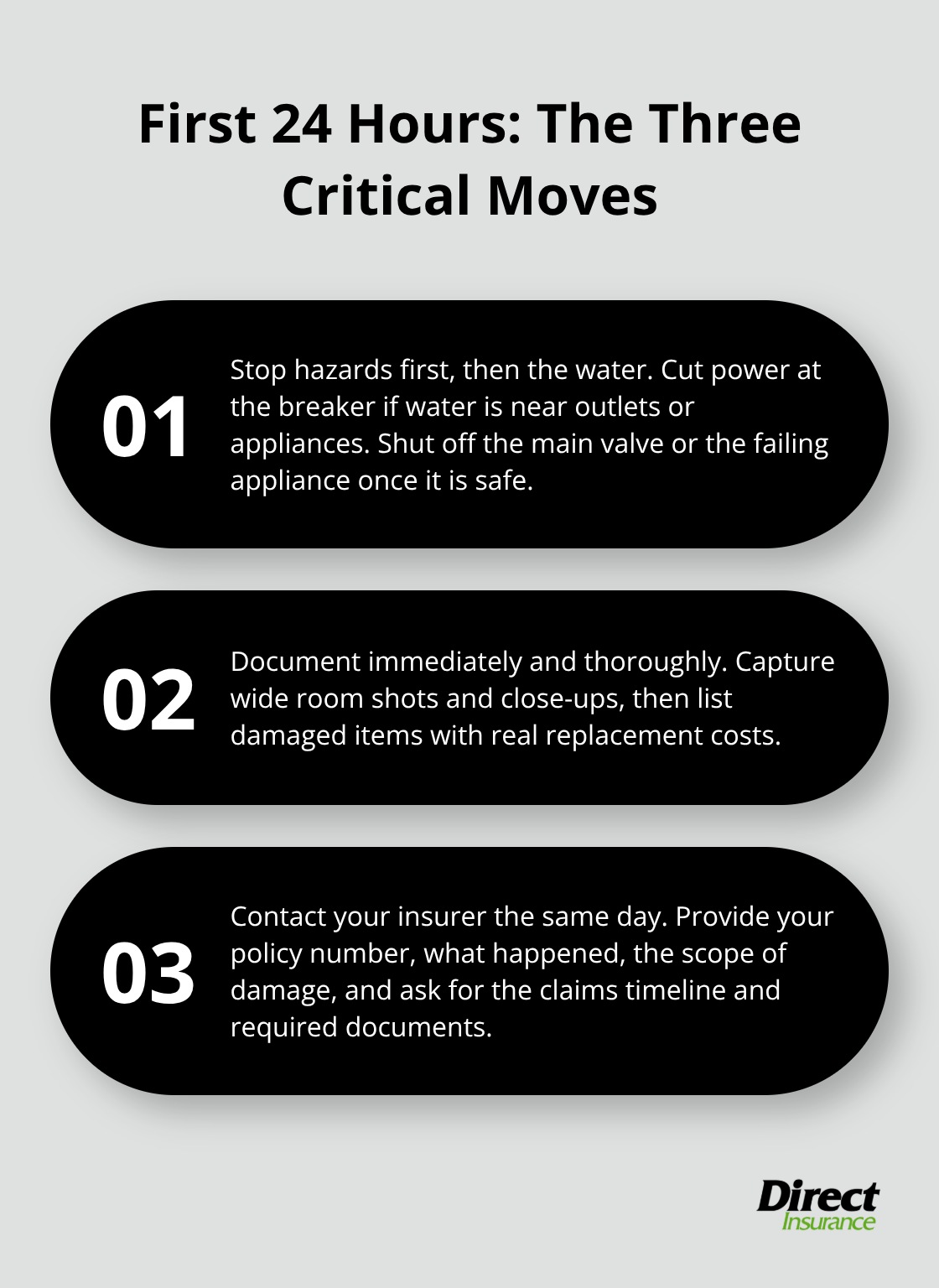

Start by turning off electricity at the breaker if water is near outlets, appliances, or standing in significant amounts. This prevents electrocution and protects your home from short circuits. Next, stop the water source if you can do so safely-shut off the main water valve for burst pipes, move items away from a roof leak, or turn off the appliance causing the failure. Do not wade into standing water or enter areas where structural damage is visible.

Document Everything on Day One

Photograph everything immediately, capturing wide shots of each affected room and close-ups of damaged materials, furniture, and personal items. Adjusters compare your claim description to what they observe on-site, so visual evidence from day one proves the damage was indeed sudden and extensive. The Insurance Information Institute emphasizes that documentation is critical because accurate photos can substantiate tens of thousands in losses. Create a detailed list of damaged items including their replacement cost-do not estimate; research actual prices online or check receipts if you have them.

Contact Your Insurer the Same Day

Contact your insurance agent on the same day, not tomorrow. Provide your policy number, describe what happened, and explain the damage scope. Ask your agent for the claims process timeline, whether the insurer will assign an adjuster, and what documentation they need. Many homeowners wait days to file, believing they need everything perfect first-this delays your claim and allows damage to worsen. File now, gather documentation second.

Preserve Your Receipts for Mitigation Work

Keep receipts for any emergency repairs or temporary mitigation you perform, as these expenses are often reimbursable under your policy’s mitigation coverage. Your quick action to prevent further deterioration demonstrates responsible claim management and strengthens your position with the adjuster. The next section covers how to organize all this documentation and work effectively with insurance adjusters and contractors to move your claim forward.

Getting Your Claim Approved and Paid

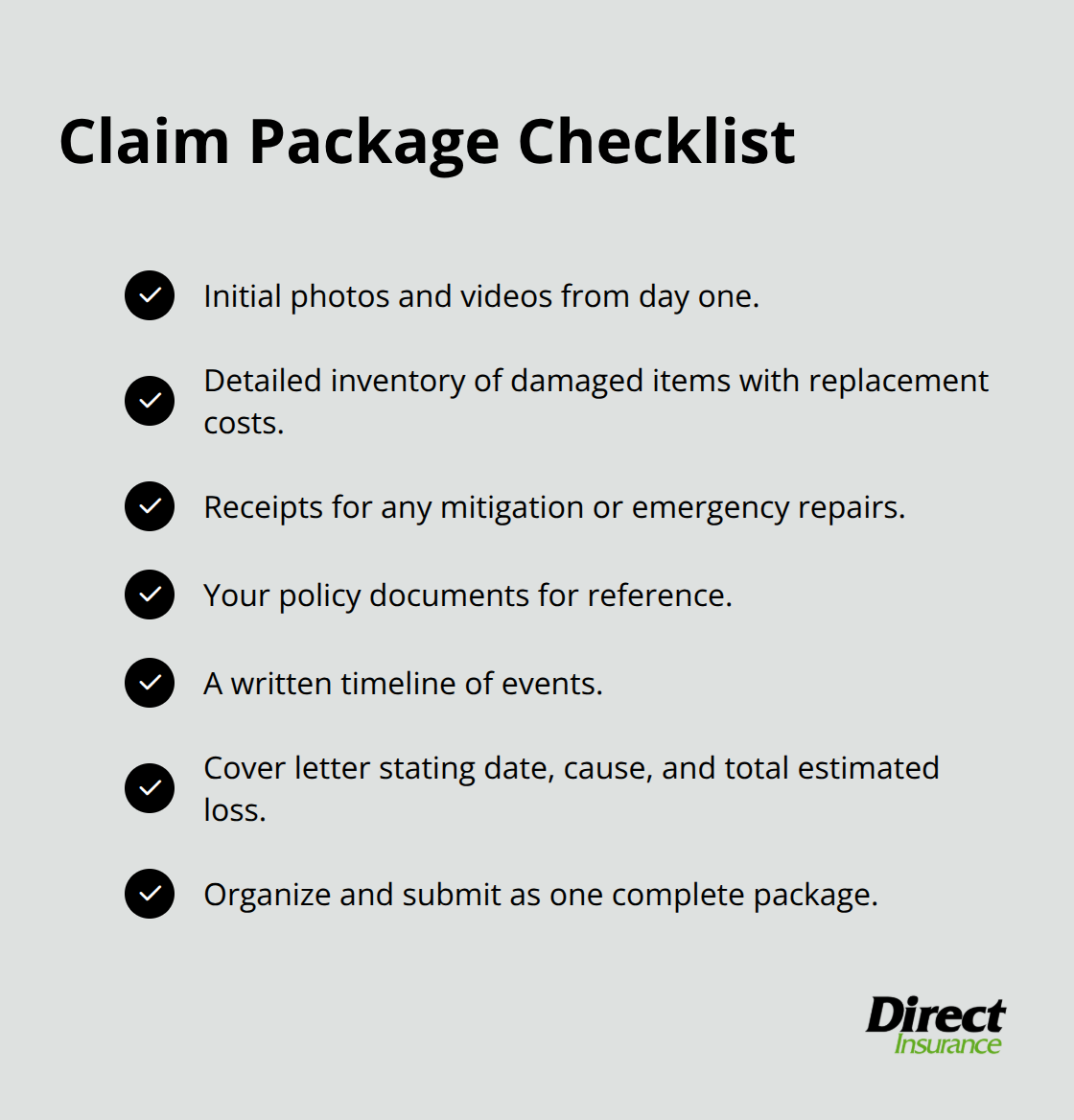

Submitting your documentation correctly makes the difference between a claim that moves forward and one that stalls for months. Organize everything into a single file or folder before you contact your adjuster. Include your initial photos and videos from day one, the detailed list of damaged items with replacement costs, receipts for any mitigation work you performed, your policy documents, and a written timeline of events. When you send this to your insurer, include a cover letter that states the date the damage occurred, what caused it, and the total estimated loss amount.

Provide a complete package upfront rather than waiting for your adjuster to ask for each piece separately; this signals that you take the claim seriously and understand the process.

Your deductible will be subtracted from the final payout, so if your damage totals $8,000 and your deductible is $1,000, you receive $7,000. Calculate this number yourself before the adjuster provides their estimate so you know exactly what to expect. The average water damage payout sits around $13,954 according to the Insurance Information Institute, but your actual recovery depends entirely on what your policy covers and how thoroughly you documented losses.

Request a Detailed Breakdown if the Estimate Seems Low

If the adjuster’s estimate falls below your documented costs, request a detailed breakdown of their calculations and ask which items or repairs they excluded and why. Do not accept vague explanations. Push for specifics about coverage denials or cost reductions. An independent appraiser or engineer can assess the damage if disputes arise over repair costs or coverage. This costs $300 to $800 but often recovers far more in additional payout than the appraisal fee.

Understand Your Adjuster’s Role and Hire Your Own Contractor

Your insurance adjuster inspects the damage, reviews your documentation, and determines what the insurer will pay. This person works for the insurance company to control costs, not to advocate for you. Hire your own restoration contractor or water damage specialist before the adjuster arrives, not after. Your contractor documents damage independently, provides a repair estimate, and can challenge the adjuster’s assessment if it seems low.

Clarify Coverage and Billing Arrangements in Writing

Do not sign anything or commit to repairs based on the adjuster’s initial estimate alone. Request written confirmation of coverage before any work begins, because coverage denial after you’ve paid for repairs leaves you with no recourse. Some restoration companies bill your insurer directly once coverage is confirmed, while others require you to pay upfront and seek reimbursement. Clarify this in writing before work starts.

Keep Organized Records of All Expenses

Keep copies of every estimate, invoice, and receipt, organized by date. When disputes arise over repair costs or coverage, these documents form your evidence. This documentation protects you if the insurer’s final offer is significantly lower than your contractor’s estimate or if questions arise about what work was actually performed.

Final Thoughts

Water damage claims succeed when you act fast, document thoroughly, and understand your coverage limits before disaster strikes. The first 24 hours determine whether you recover most of your losses or face denials and secondary damage. Your policy covers sudden, accidental water damage from burst pipes and appliance failures, but excludes flood damage and gradual deterioration from neglect.

Most homeowners underestimate how quickly water damage escalates-within 48 hours, contamination shifts from clean water to gray water with bacterial growth, and mold begins developing within days. Your speed in stopping the water source and documenting losses directly impacts your final payout, with the average water damage claim paying around $13,954. Professional guidance from restoration contractors and independent adjusters protects you from signing agreements based on unconfirmed coverage, which leaves you paying for unapproved work.

At Direct Insurance Services, we help Utah homeowners understand their home insurance water damage coverage before claims happen. Contact us to review your current policy, identify gaps, and recommend endorsements that protect you against water damage scenarios your standard policy excludes.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation