Does Home Insurance Cover Plumbing Issues?

A burst pipe or leaky fixture can wreak havoc on your home and your wallet. Many homeowners assume their standard policy covers all plumbing damage, but the reality is far more complicated.

At Direct Insurance Services, we’ve seen countless claims denied because policyholders didn’t understand what their coverage actually includes. The truth is that home insurance covers some plumbing issues-but not all of them.

What Your Policy Actually Covers

Home insurance covers sudden and accidental plumbing damage, but this distinction matters far more than most homeowners realize. A burst pipe that floods your basement overnight qualifies. A slow leak that drips behind your walls for months does not. According to FEMA, mold can develop within 24 to 48 hours after water exposure, which is why the timing and nature of the damage determine whether your claim receives approval or rejection. When a pipe ruptures unexpectedly, your policy typically pays for water damage to your home’s structure, flooring, drywall, and personal belongings up to your coverage limits, minus your deductible.

Events that trigger coverage

Sudden pipe bursts, frozen pipes in properly heated homes, and failed water heater tanks all qualify as covered events. A malfunctioning water heater, a burst appliance hose, or frozen pipes that thaw and leak fall into this covered category. If your neighbor’s plumbing damage leaks into your unit, your homeowners liability coverage may help pay for their repairs. A slab leak caused by a burst pipe underneath your foundation can receive coverage, though foundation damage from flooding typically does not. The critical factor is that the damage must result from an event you couldn’t have prevented through reasonable care.

Material and appliance complications

Homes with outdated plumbing materials like polybutylene or galvanized steel often face denial from standard policies because insurers consider these materials inherently risky. If an appliance malfunctions suddenly and causes water damage to your belongings, that damage is usually covered up to your policy limits, though the appliance itself may require a separate electrical and mechanical breakdown rider. Your policy pays for the water damage itself; it does not pay the cost to fix or replace the faulty plumbing.

What your policy explicitly excludes

Gradual leaks, seepage, and water damage from neglected pipes receive flat exclusion. If you knew about a leak and failed to repair it, your claim will face denial. Claims for sewer backups and sump pump failures typically receive exclusion unless you purchase a water backup coverage endorsement. Mold damage receives severe limitation under basic policies, though a mold damage rider can extend coverage for hidden leaks. Flood damage remains entirely uncovered by standard homeowners insurance regardless of the cause; you need separate flood insurance through the National Flood Insurance Program.

The maintenance question that determines everything

The distinction between sudden and gradual damage is absolute. One claim receives payment; the other receives rejection outright. Your insurer will scrutinize whether you maintained your plumbing system and addressed known issues promptly. This reality makes understanding what constitutes negligence in your insurer’s eyes essential before a problem strikes your home.

When Your Insurer Rejects Plumbing Claims

Your homeowners insurance won’t cover plumbing damage if your insurer determines the problem developed gradually or resulted from your failure to maintain the system. Insurers distinguish sharply between sudden failures and deteriorating conditions, and this distinction controls whether you receive payment or face outright denial.

Gradual damage and wear-and-tear exclusions

If a pipe leaks slowly behind your walls for months before you notice it, your claim will be denied because the damage did not occur suddenly. Insurers view this as a maintenance issue, not an insurable event. The same applies to corrosion, rust, or mineral buildup that weakens pipes over years-these are wear-and-tear problems that fall squarely outside coverage. When an adjuster investigates your claim, they’ll look for evidence that you knew about the problem and ignored it. If a plumber previously identified a failing section of pipe or you observed water stains months before filing a claim, your insurer will use that against you.

Homes with outdated plumbing materials like polybutylene pipes face systematic denials because insurers classify these materials as inherently defective. If your home has this type of plumbing, many standard policies won’t cover water damage at all, regardless of whether the failure was sudden or gradual.

Negligence and the failure to act

Insurers expect homeowners to take reasonable preventive steps. Annual professional pipe inspections cost between $150 and $300 and can identify problems before they cause damage. If you skip inspections and later file a claim, your insurer may argue you failed to exercise reasonable care. Frozen pipes present a specific challenge-if your home wasn’t adequately heated when pipes froze, your claim faces denial even though the rupture itself was sudden. This means you must maintain consistent heating during winter months and insulate exposed pipes, particularly in crawl spaces and exterior walls.

If you discover a leak, stopping it immediately matters legally as well as practically. Continuing to operate a home with a known leak strengthens your insurer’s argument that you were negligent. Document your response: take photos showing when you first noticed the problem, record the date you contacted a plumber, and keep receipts proving you took action. This documentation protects you if your insurer later questions whether you addressed the issue promptly.

Sewer backups and sump pump failures

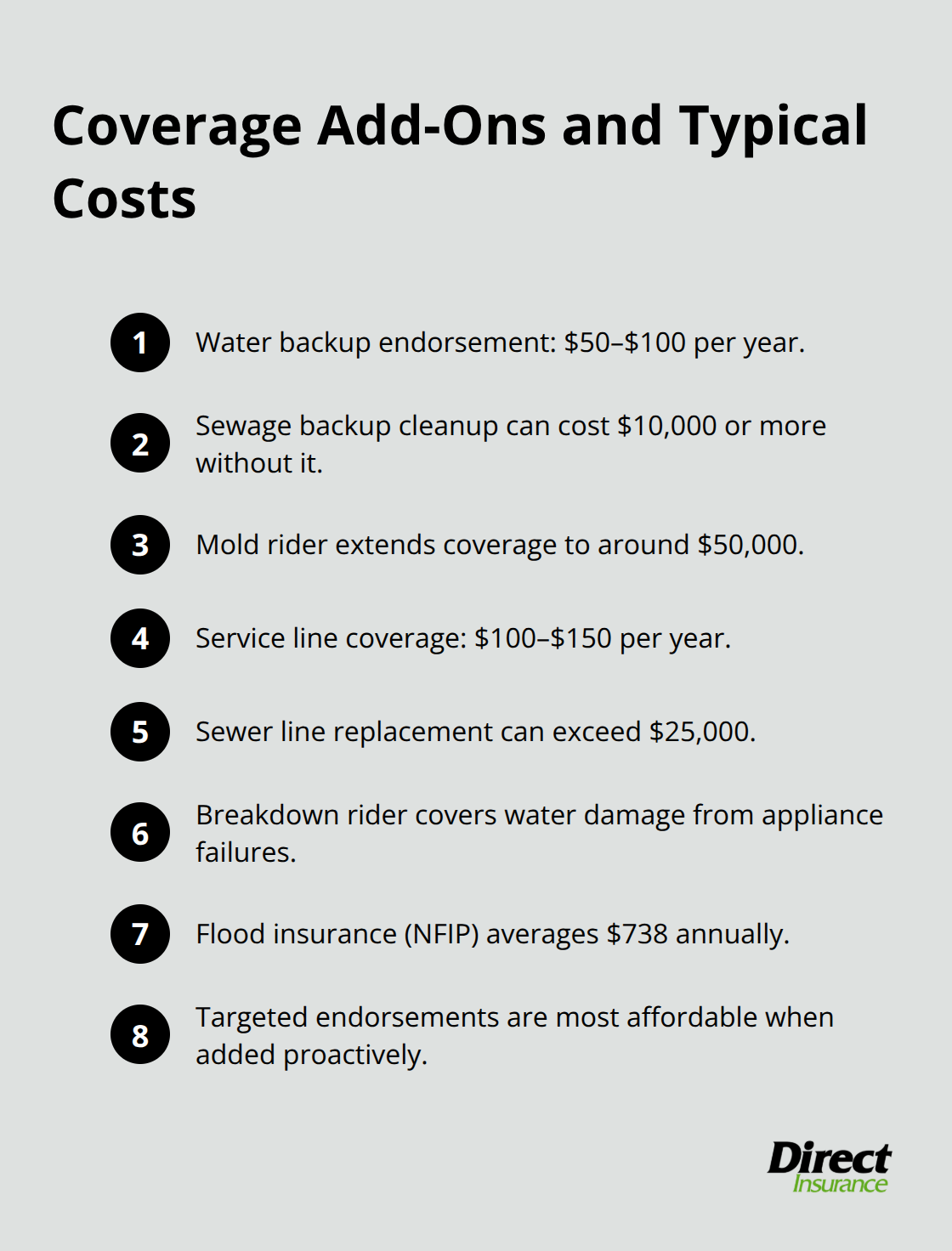

Sewer backups and sump pump failures typically receive blanket exclusion from standard policies because insurers classify these as maintenance and drainage problems rather than sudden accidents. Adding a water backup coverage endorsement costs roughly $50 to $100 annually and covers exactly these scenarios. Without it, a sewage backup that damages your basement receives zero coverage, leaving you responsible for cleanup and repairs that can exceed $10,000.

Understanding these exclusions reveals why your next step should focus on identifying which coverage gaps exist in your current policy and how to fill them before a plumbing emergency strikes. If standard insurers have rejected your application due to plumbing concerns or other risk factors, specialized carriers may still provide the protection you need.

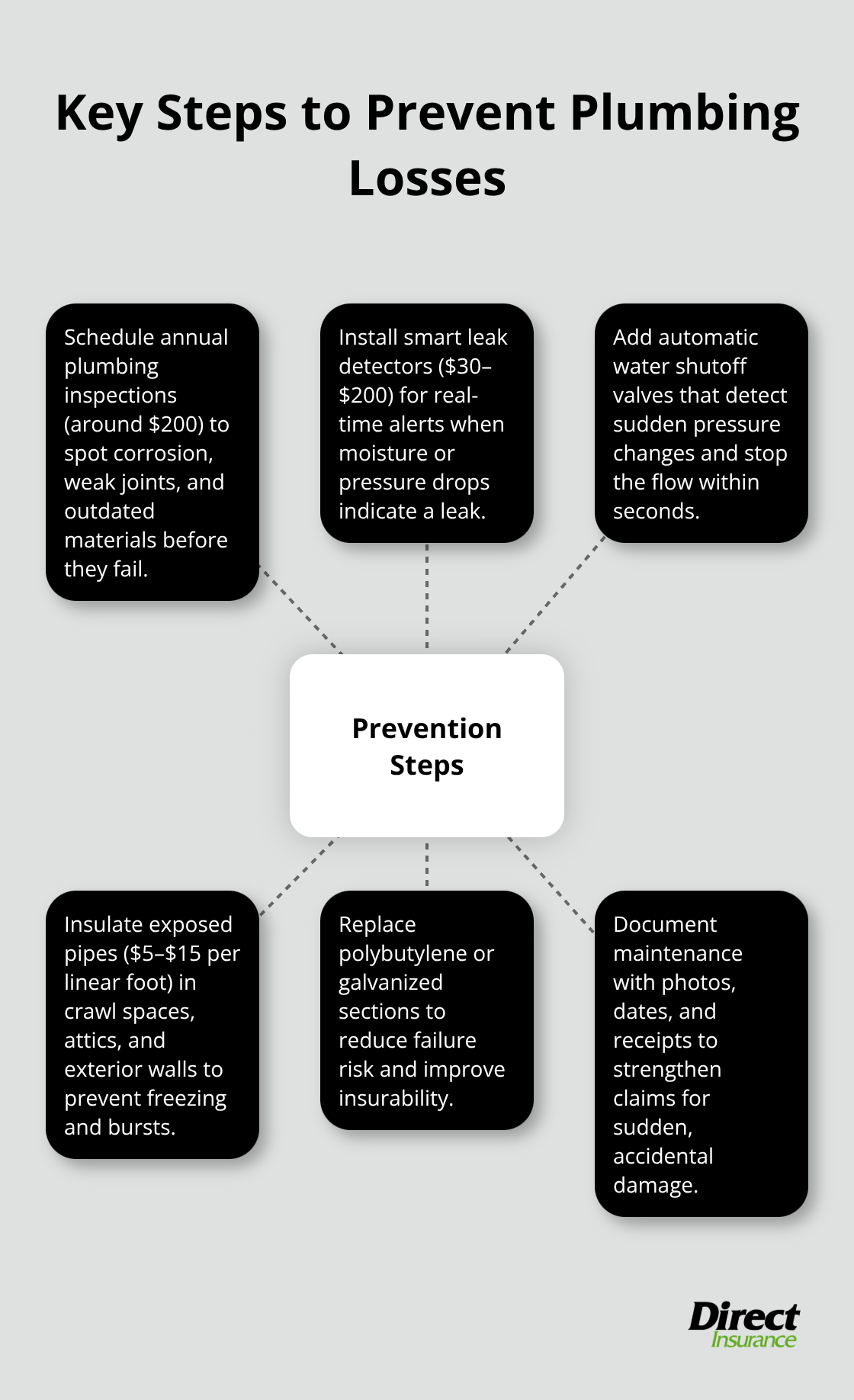

Stop Plumbing Problems Before They Drain Your Bank Account

Annual professional pipe inspections cost around $200 and identify deteriorating pipes, corrosion, and structural weaknesses long before they cause damage. A plumber can spot polybutylene pipes, galvanized steel, or mineral buildup that will eventually fail.

This single investment often costs less than your insurance deductible and prevents claims that can raise your premiums by hundreds of dollars annually. Schedule inspections every year, particularly if your home is over 30 years old or you’ve never had a professional assessment. Document everything the inspector finds, keep written records, and address flagged issues immediately. This documentation protects you when filing a claim because insurers cannot deny coverage for sudden failures in systems you actively maintain.

Install water detection technology before disaster strikes

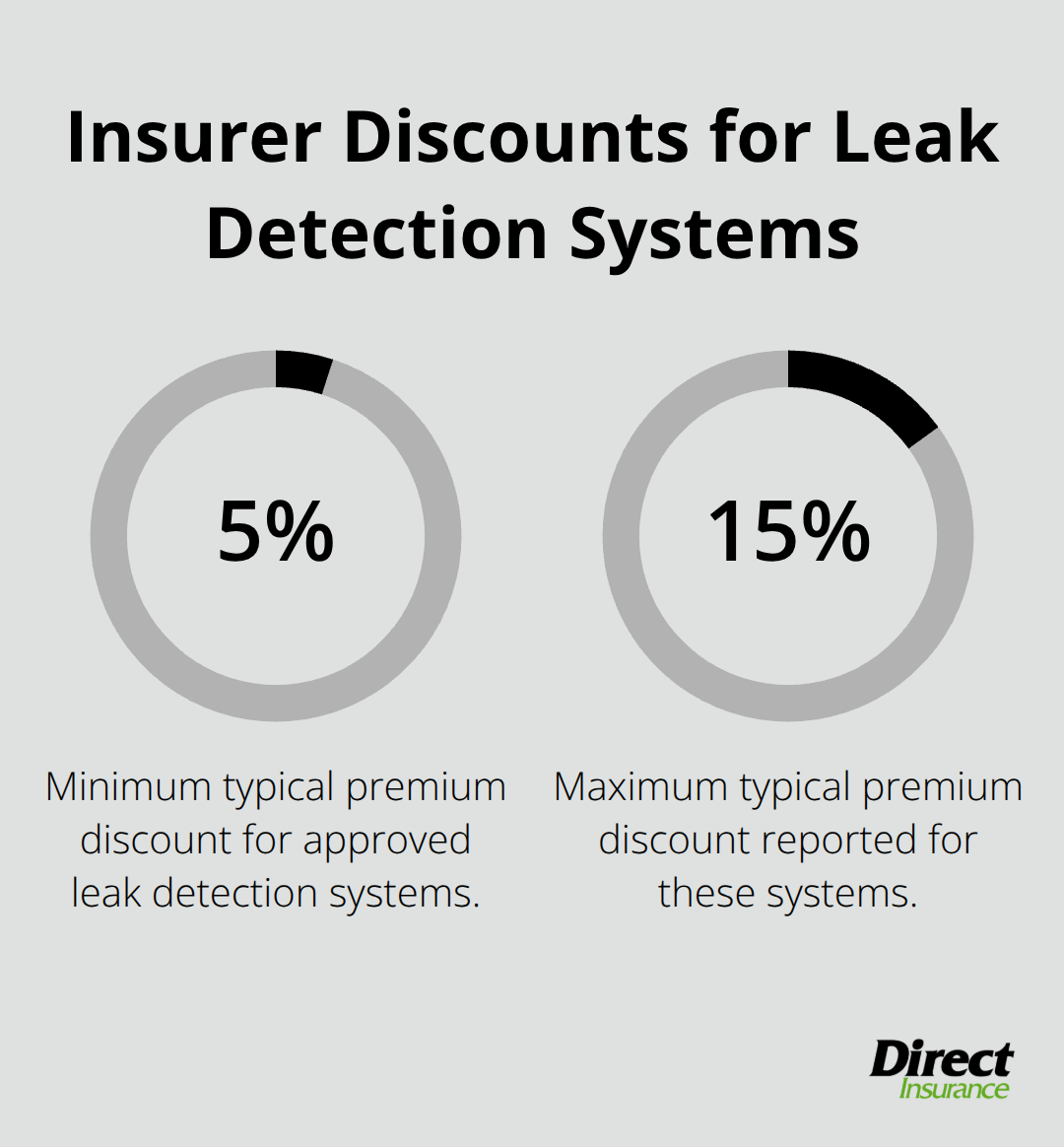

Smart leak detectors cost between $30 and $200 per unit and alert you the moment water appears where it shouldn’t. These devices detect pressure drops in your water line or moisture beneath sinks, in crawl spaces, and around water heaters. Many insurers offer discounts of 5 to 15 percent on premiums when you install these systems, which means the technology pays for itself within one or two years.

Automatic water shutoff valves represent another critical investment. When a pipe ruptures, these valves detect the sudden pressure change and close within seconds, stopping water flow before thousands of gallons flood your home. The combination of detection and automatic shutoff transforms plumbing emergencies from catastrophic to manageable. Homes in cold climates benefit from pipe insulation in crawl spaces, attics, and exterior walls, which prevents frozen pipes that burst when temperatures drop. This costs $5 to $15 per linear foot and eliminates the most common trigger for water damage claims.

Upgrade plumbing materials that insurers refuse to cover

If your home contains polybutylene pipes, galvanized steel, or other outdated materials, replacing them becomes necessary if you want insurance coverage. Many standard policies explicitly exclude water damage from these materials regardless of whether the failure is sudden or gradual. Full plumbing replacement costs between $1,500 and $15,000 depending on your home’s size and complexity, but this investment removes a major barrier to coverage approval. Partial replacement focusing on the most vulnerable sections costs less and provides immediate risk reduction. Your plumber can identify which sections deteriorate fastest and prioritize those replacements. Some homeowners tackle this incrementally, replacing one section per year rather than replacing everything at once. This approach spreads costs across multiple years while steadily reducing your risk profile. Once you complete upgrades, notify your insurer because improved plumbing systems often qualify for premium reductions. Water heaters fail after 8 to 12 years on average, so if yours is older than 10 years, replacement prevents a major claim trigger. Modern units include safety pans and overflow protection that older models lack.

Customize your policy to fill the coverage gaps you now understand

Water backup coverage endorsements cost $50 to $100 annually and cover sewer backups, sump pump failures, and drain overflows that standard policies exclude entirely. Without this endorsement, a single sewage backup can cost $10,000 or more in cleanup and repairs, making this endorsement one of the cheapest insurance decisions you’ll make. Mold damage riders extend mold coverage from the severe limitations in basic policies to around $50,000, protecting you if hidden leaks develop mold before you notice them.

Service line coverage protects water, sewer, and drain lines outside your home for roughly $100 to $150 annually, which matters because replacing a sewer line can exceed $25,000. An electrical and mechanical breakdown rider covers water damage from appliance failures, protecting you when a washing machine hose bursts or a dishwasher malfunctions. Flood insurance through the National Flood Insurance Program averages $738 annually and becomes essential if your home sits in a flood-prone area or has experienced flooding previously. When you understand what your base policy excludes, adding targeted endorsements becomes straightforward and affordable.

Final Thoughts

The answer to whether home insurance covers plumbing issues is straightforward: yes, but only for sudden and accidental damage. Your policy protects you when a pipe bursts without warning or a water heater fails unexpectedly, yet it does not protect you from gradual leaks, neglected maintenance, or deteriorating materials. This distinction determines whether your claim receives approval or rejection.

Your homeowners policy likely contains gaps you haven’t considered. Sewer backups, sump pump failures, and mold damage fall outside standard coverage unless you add specific endorsements, and water backup coverage costs just $50 to $100 annually to prevent a single sewage backup from costing you thousands out of pocket. Mold riders, service line protection, and electrical breakdown coverage fill additional gaps that standard policies leave exposed, and these additions are affordable when purchased proactively but become expensive regrets when purchased after a claim denial.

We at Direct Insurance Services work with homeowners throughout Utah to identify coverage gaps and customize policies that actually protect against the risks your home faces. Contact Direct Insurance Services today to review your current coverage and identify which endorsements would protect you from costly plumbing surprises.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation