Home Insurance for Condominium: Complete Guide

Condo owners often assume their building’s master insurance policy covers everything inside their unit. That assumption costs them thousands in uncovered losses every year.

At Direct Insurance Services, we’ve seen firsthand how gaps in master policies leave owners vulnerable. Home insurance for condominiums fills those gaps and protects what matters most to you.

Why Condo Insurance Differs From Home Insurance

Homeowners insurance and condo insurance sound similar, but they protect fundamentally different things. HO-3 homeowners insurance covers your entire house structure, roof, exterior walls, and everything inside. HO-6 condo insurance covers only your interior unit and personal belongings, leaving the building’s exterior and common areas to the association’s master policy. This distinction matters because many condo owners in Utah buy too much dwelling coverage or assume they need none at all. Neither approach works. Your liability exposure is real, your personal property is at risk, and the master policy has hard limits on what it pays.

Where Master Policies Fall Short

The condo association’s master policy covers the building’s exterior, roof, common hallways, elevators, lobbies, parking areas, and shared grounds. It does not cover what happens inside your unit. If a pipe bursts in your walls and damages your flooring, cabinets, and appliances, the master policy ignores it. If someone slips on your kitchen floor and sues you, the master policy does not defend you. If a fire starts in your unit and spreads to adjacent units, you face personal liability claims the association’s policy will not cover. Many Utah condo owners discover these gaps only after a loss, when they learn their master policy has a deductible they must pay or coverage limits that do not match their needs. The association may also assess all unit owners for shared damage if the master policy’s deductible is high or its limits are exceeded.

How HO-6 Closes the Gaps

HO-6 insurance protects your interior, your belongings, and your liability exposure where the master policy stops. Interior water damage from a burst pipe, fire damage to your unit’s contents, and theft of your possessions all fall under HO-6 coverage. Your personal liability protection kicks in when someone is injured in your unit or you accidentally damage another owner’s property. Utah law holds condo owners personally responsible for injuries or damage they cause, regardless of whether the association has insurance. This is where the master policy leaves you exposed.

Personal Property and Liability Protection

Personal property coverage in an HO-6 policy reimburses you for stolen or damaged belongings up to your policy limit. A break-in that takes your electronics, furniture, and clothing triggers a claim that replaces them. Standard policies limit certain high-value items like jewelry or art, so valuable pieces require a scheduled personal property endorsement to receive full coverage. Liability coverage protects you when someone is injured in your unit or you accidentally damage another owner’s property. Additional living expenses coverage pays for hotel bills, meals, and other costs if a covered loss makes your unit uninhabitable. These protections exist because the master policy simply does not include them for individual unit owners.

Understanding Your Coverage Needs in Utah

Utah condo owners face specific risks that shape insurance needs. Winter weather can cause pipe bursts and water damage inside units. Older buildings in Salt Lake City and surrounding areas may have outdated plumbing or electrical systems that increase interior damage risk. Your personal belongings represent significant value that only your HO-6 policy protects. The next step is assessing exactly what coverage limits you need and comparing quotes from multiple insurers to find the right fit for your situation.

Types of Coverage Available for Condo Owners in Utah

Dwelling Coverage for Interior Improvements

Dwelling coverage for your interior creates confusion for most Utah condo owners. Your HO-6 policy covers improvements and upgrades you’ve made inside your unit, but only if the master policy doesn’t already cover them. If your condo association’s master policy is bare walls coverage, it protects common areas and shared features in multi-family residential buildings, leaving you responsible for everything from drywall inward. You need dwelling coverage limits that match what you’ve actually installed or upgraded.

If you’ve renovated your kitchen with custom cabinetry, replaced flooring, or upgraded fixtures, those improvements become your responsibility to insure. Many Utah owners with older buildings in Salt Lake City and Ogden face this exact situation because their associations opted for bare walls policies to keep master policy premiums low. The master policy simply won’t cover your interior work, so your HO-6 dwelling coverage must fill that gap.

Personal Property Coverage and High-Value Items

Your personal property coverage is separate from dwelling coverage and covers your belongings, not the building itself. A standard HO-6 policy typically limits individual items like jewelry or art to around $2,500, far below their actual value. If you own engagement rings, watches, or artwork worth more than that, you need a scheduled personal property endorsement that lists items individually with their appraised values. This matters because a single loss could otherwise leave you thousands of dollars short.

Liability Protection in Utah

Your liability coverage protects you when someone is injured in your unit or you accidentally damage another owner’s property. Utah law makes you personally liable for those claims regardless of what the association’s master policy covers. Standard liability limits start at $100,000, but if you have significant assets or income, $300,000 or higher makes sense to protect yourself from lawsuit judgments.

Additional Living Expenses and Loss Assessment

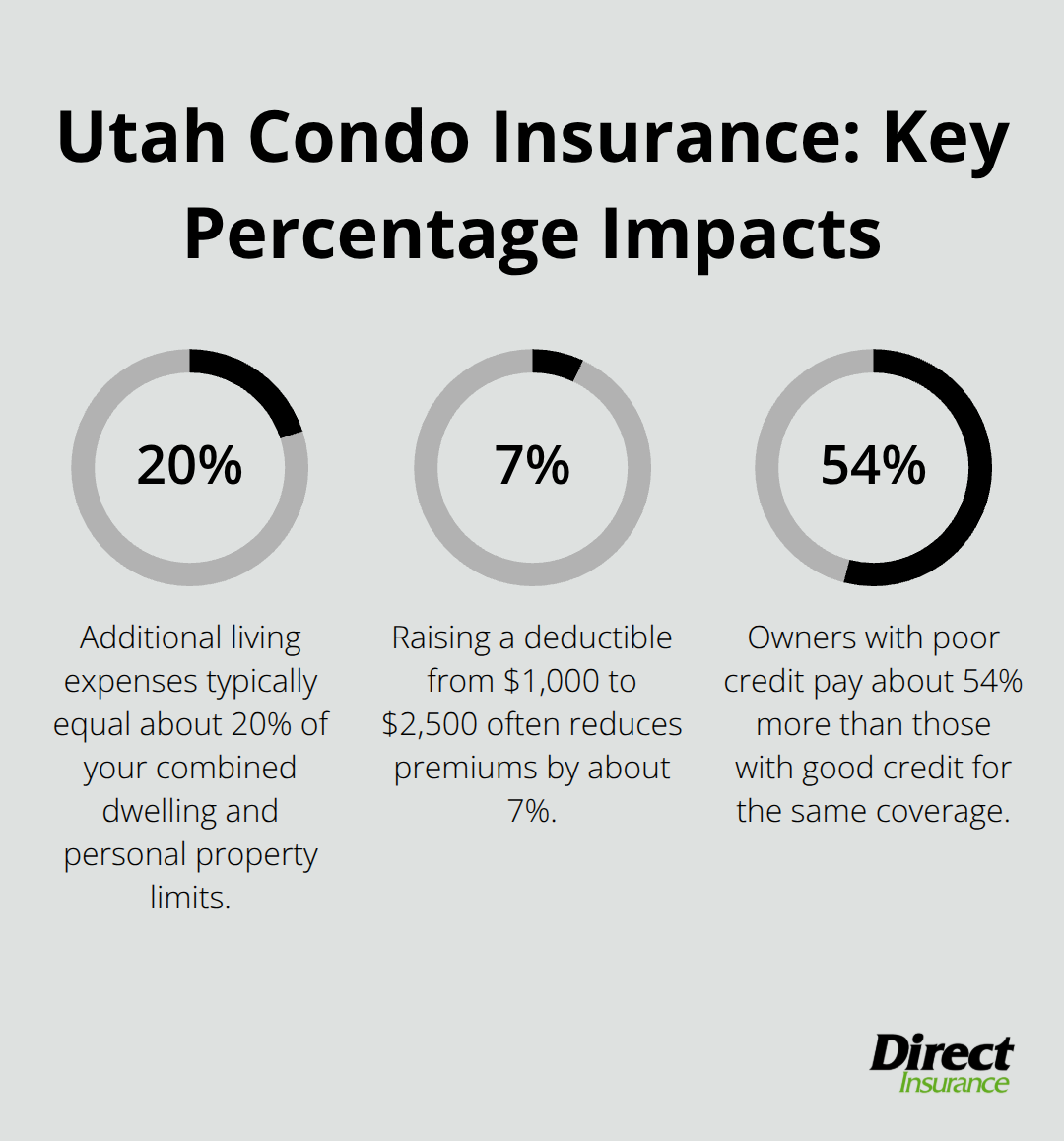

Additional living expenses coverage pays for hotel stays, meals, and other costs if a covered loss makes your unit uninhabitable while repairs happen. This coverage typically equals about 20 percent of your combined dwelling and personal property limits, so if you carry $100,000 in dwelling plus $75,000 in personal property, you’d get roughly $35,000 in additional living expenses coverage.

One coverage many Utah condo owners overlook is loss assessment protection. If the association’s master policy has a high deductible or its limits are exceeded after a major loss to common areas, the association can assess all unit owners to cover the gap. Loss assessment coverage starts at around $1,000 and can be increased through endorsements to protect you from unexpected bills. This protection proves particularly important in Utah’s climate where winter weather damage to roofs and pipes can trigger large shared losses that exceed master policy limits. Understanding these four core coverage types positions you to make informed decisions about your specific situation and move forward with selecting the right policy for your needs.

Selecting Coverage That Matches Your Utah Condo

Calculate Your Personal Property Coverage

Start by inventorying everything you own inside your unit. Walk through each room and note your furniture, electronics, appliances, clothing, and valuables. Add up the replacement cost at today’s prices, not what you paid years ago. Most Utah condo owners underestimate this number significantly. If your belongings total $85,000, you need at least $85,000 in personal property coverage. This is not optional math-it’s the difference between being fully protected and facing out-of-pocket losses after a covered event.

Determine Your Dwelling Coverage Limits

Measure what you’ve actually upgraded or improved inside your unit. If you’ve replaced flooring, installed custom cabinetry, or upgraded appliances, those improvements need coverage limits that reflect their current value. Check your condo association’s master policy to confirm whether it covers bare walls only or includes some interior elements. This step determines how much dwelling coverage you actually need.

Set Your Liability and Loss Assessment Protection

Liability coverage should reflect your assets and income. The standard $100,000 limit works for modest situations, but if you own your unit outright plus have savings and investments, $300,000 or $500,000 makes more sense. Utah courts award significant judgments in personal injury cases, and your liability coverage protects your assets from those claims.

Loss assessment coverage should start at $2,500 to $5,000 in Utah, given how winter weather damage to roofs and shared plumbing can trigger large association assessments. Many owners skip this coverage entirely, then face unexpected bills when the master policy’s deductible or limits are exceeded after a major loss to common areas.

Compare Quotes From Multiple Insurers

Request quotes from at least three different insurers with identical coverage limits and deductibles so you compare apples to apples. According to NerdWallet’s analysis of over 450 million rates from more than 100 insurers, State Farm averages around $360 per year for condo coverage while American Family averages about $835 per year for the same coverage. That $475 annual difference applies to identical protection.

In Utah specifically, costs vary dramatically by location. Salt Lake City and Park City face different risk profiles than smaller towns, which affects your quote. When comparing quotes, raise your deductible from $1,000 to $2,500 and note the savings. NerdWallet’s data shows this typically reduces premiums by about 7 percent.

Only make this choice if you can actually cover the higher deductible from savings without financial strain.

Unlock Discounts and Improve Your Rate

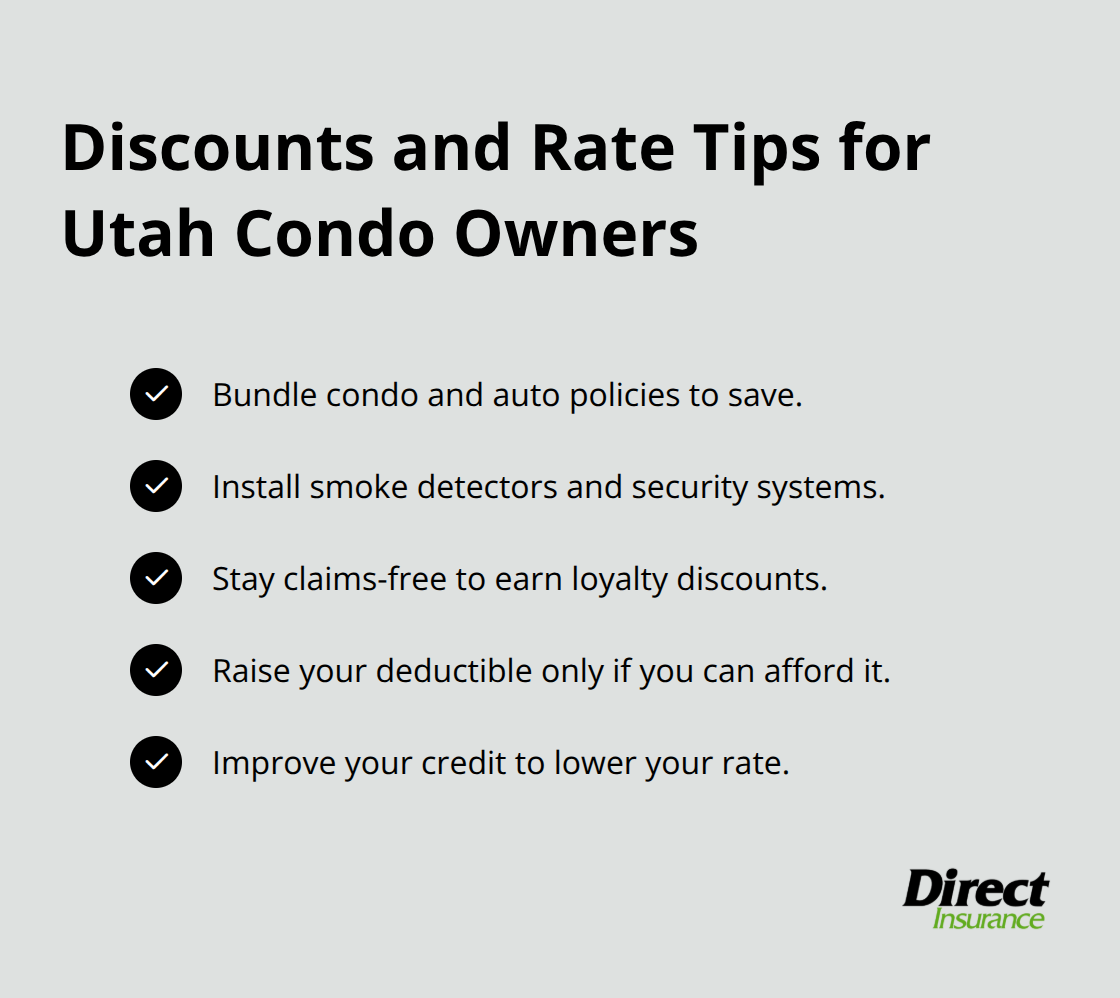

Look for discounts you qualify for. Bundling your condo insurance with auto insurance often saves 10 to 25 percent. Installing smoke detectors or security systems can lower rates. Staying claims-free rewards you with loyalty discounts. Poor credit scores significantly impact your premium-NerdWallet found that owners with poor credit pay about 54 percent more than those with good credit for identical coverage.

If your credit needs work, improving it before shopping for insurance pays dividends. Direct Insurance Services, an independent agency based in Salt Lake City, shops multiple top-rated insurance companies on your behalf to find the coverage and rates that fit your specific Utah situation and budget.

Final Thoughts

Condo insurance protects what a master policy cannot, and your personal belongings, interior improvements, and liability exposure require coverage that only an HO-6 policy provides. Utah condo owners who skip this protection face thousands in uncovered losses when water damage, theft, or liability claims strike. A burst pipe damages your flooring and cabinetry, someone slips in your unit and sues, or a fire spreads to neighboring units-without home insurance for condominium, you pay these costs yourself.

Inventory your belongings and calculate their replacement cost, then review your condo association’s master policy to understand what it covers and what gaps remain. Determine your dwelling coverage needs based on interior improvements you’ve made, set liability limits that match your assets and income, and request quotes from multiple insurers with identical coverage so you compare actual rates. Look for discounts through bundling, safety devices, and claims-free history to reduce your premium.

Utah’s climate and older building stock create specific risks that standard coverage addresses, and the right condo insurance policy accounts for these local realities. We at Direct Insurance Services understand Utah’s unique insurance landscape and shop multiple top-rated insurance companies to find coverage and rates that fit your specific situation. Contact Direct Insurance Services to discuss your condo insurance requirements and get quotes that reflect your Utah home and budget.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation