Home Insurance Deductible Utah: What To Expect

Your home insurance deductible in Utah directly affects how much you pay when you file a claim. A higher deductible lowers your monthly premium, but it means you’ll pay more out of pocket if something happens.

We at Direct Insurance Services help Utah homeowners understand these tradeoffs so you can pick the deductible that fits your budget and risk tolerance. This guide walks you through what deductibles actually cost and how to choose wisely.

Understanding Your Deductible in Utah

What Your Deductible Actually Is

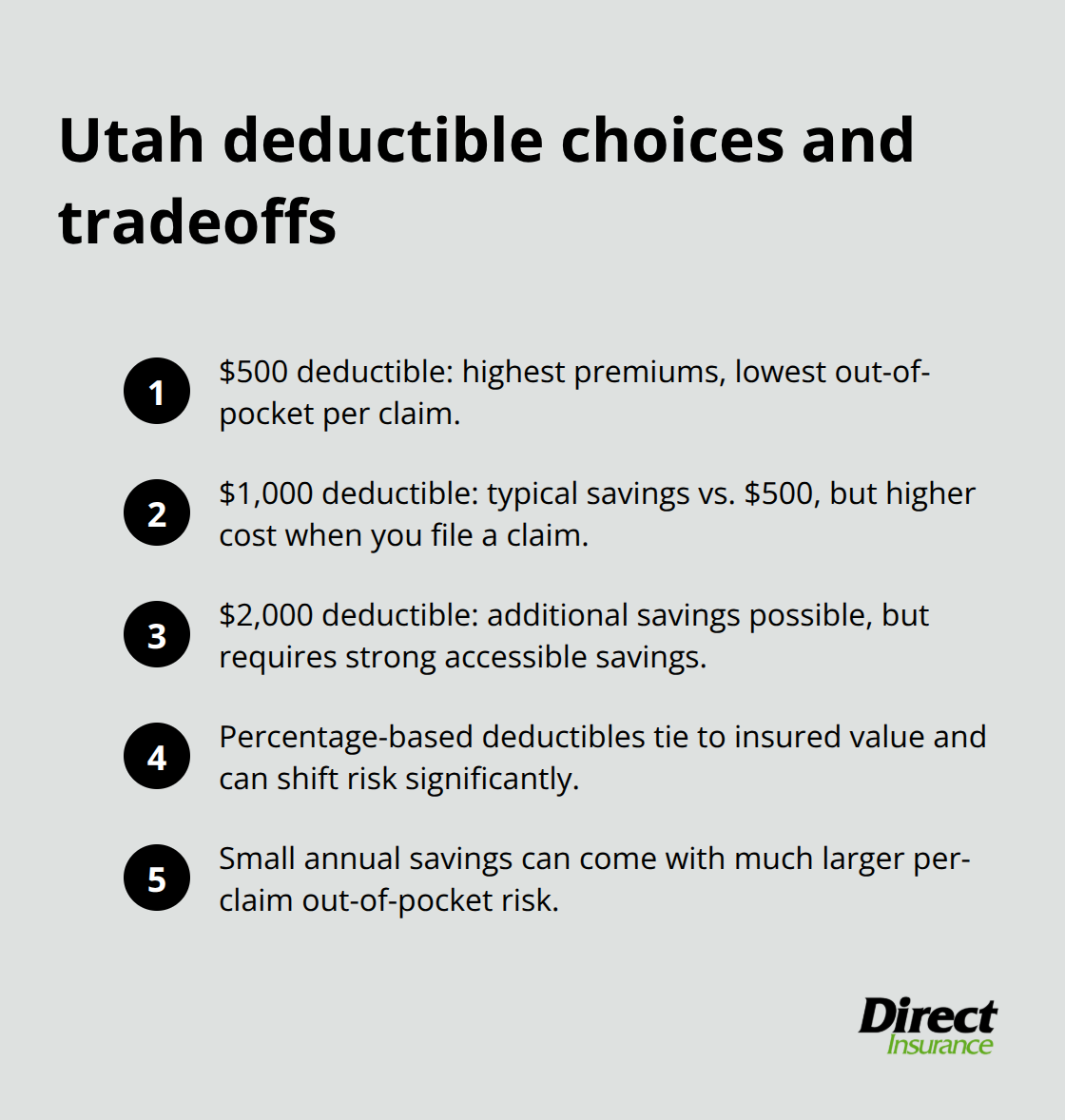

A deductible is the amount of money you pay out of your own pocket when you file a claim before your insurance company pays anything toward the damage. In Utah, standard deductible options typically range from $500 to $2,000 as flat dollar amounts, though some homeowners choose percentage-based deductibles tied to their home’s insured value. The deductible choice directly controls what you pay monthly-selecting a $1,000 deductible instead of a $250 deductible will noticeably lower what you pay each month.

The tradeoff matters significantly. If a pipe bursts and causes $5,000 in water damage, you cover the first $1,000 yourself, and your insurer covers the remaining $4,000. This isn’t a yearly threshold; the deductible applies to each individual claim you file. If you have two separate losses in one year, you pay the deductible twice. Many Utah homeowners underestimate this reality and end up surprised when they file their first claim and realize they must pay thousands before their coverage kicks in.

How Your Deductible Activates

The deductible is separate from your insurance premium and only activates when you actually file a claim. You don’t pay it upfront or monthly-it applies only after a covered loss occurs. This distinction confuses some homeowners who think a higher deductible means they’re paying more overall, when actually they’re paying less monthly but risking more in a single event.

According to the NAIC, Utah residents should honestly assess their ability to cover their chosen deductible amount from savings or emergency funds. A higher deductible lowers your home insurance premium, but only if you can actually pay it out of pocket when a claim happens. If you choose a $2,000 deductible but have only $1,500 in emergency savings, you’ve created a financial vulnerability. The right deductible isn’t about picking the lowest premium; it’s about selecting an amount you can genuinely afford to pay without derailing your finances if damage occurs.

Weather Events and Your Financial Readiness

Weather events in Utah-hail, wind, or wildfire-can happen without warning, so your deductible choice should reflect realistic financial circumstances, not wishful thinking about never filing a claim. Your out-of-pocket risk depends entirely on the deductible you select and your actual ability to cover it when loss strikes. Understanding this connection between your deductible choice and your financial security sets the stage for making the right decision about which deductible amount works for your household.

What Deductibles Actually Cost Utah Homeowners

Standard Deductible Options and Premium Savings

Most Utah homeowners face deductible choices between $500, $1,000, and $2,000 as flat dollar amounts, though some insurers allow percentage-based options tied to your home’s insured value. The NAIC reports that selecting a $1,000 deductible instead of $500 typically saves 10 to 15 percent on your annual premium, while jumping to $2,000 can save an additional 10 to 20 percent depending on your insurer and home characteristics. This sounds attractive until you realize that saving $200 annually on premiums means you accept $1,500 more in out-of-pocket risk per claim.

How Utah Weather Shapes Your Deductible Risk

Utah weather patterns matter significantly. Hail damage and wind-driven losses occur regularly across the state, and these events often trigger claims between $3,000 and $8,000. If you choose a $2,000 deductible to save money monthly, you personally cover that entire $2,000 before your insurer pays anything toward a hail claim. The math only works if you actually have $2,000 sitting in accessible savings. A Federal Reserve survey on emergency savings capacity found that 40 percent of Americans cannot cover a $400 emergency expense, which means choosing a deductible higher than your realistic emergency fund is financially reckless regardless of the premium savings.

Location and Home Characteristics Drive Deductible Decisions

Weather and location drive deductible decisions more than most homeowners realize. Homes in areas with higher wildfire risk, frequent hail corridors, or older roofing materials often face higher insurance costs, making a lower deductible more appealing even if it increases your monthly payment. Conversely, newer homes in lower-risk areas with metal roofs and updated electrical systems may justify higher deductibles because claims are statistically less likely.

Reassessing Your Deductible When Life Changes

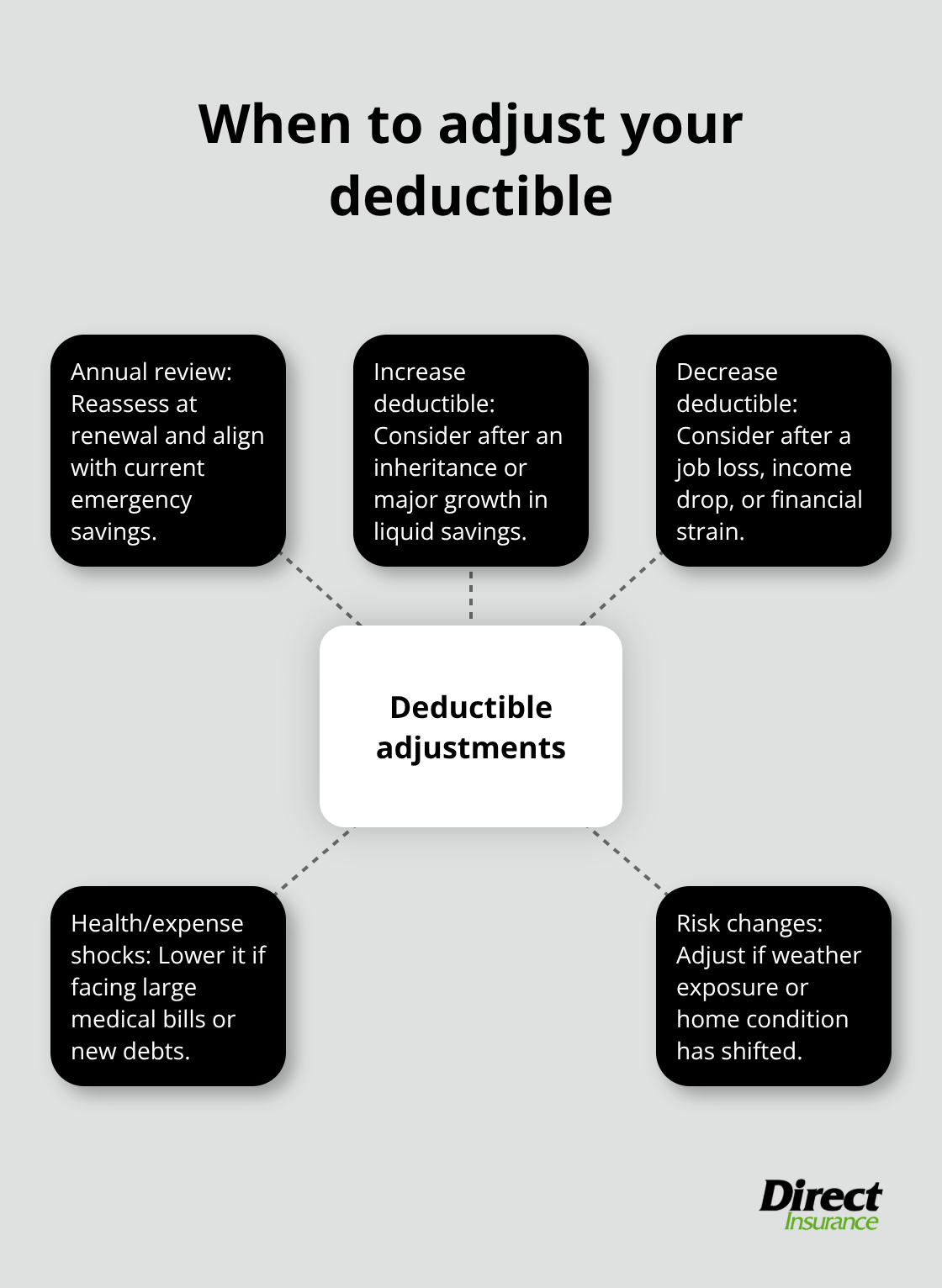

The Utah Insurance Department recommends reviewing your deductible annually because your financial situation changes. A household that could barely afford a $1,500 deductible five years ago might now have $5,000 in emergency savings and could safely shift to a higher deductible for better monthly rates. The inverse is equally true-job loss, medical expenses, or other financial strain means you should lower your deductible even if it costs more monthly, because you cannot safely cover a large out-of-pocket payment if damage occurs.

The Math Behind Selecting Your Deductible

Comparing deductible options requires honest math, not wishful thinking. Calculate what you can realistically pay within 30 days if a claim happens, then select a deductible at or below that amount. This honest assessment of your financial capacity directly influences which deductible option actually protects your household. Once you understand what you can afford to pay out of pocket, you’re ready to explore how different deductible amounts interact with the specific perils that threaten Utah homes most frequently.

Pick Your Deductible Based on What You Can Actually Afford

The most honest way to choose your deductible is to stop thinking about monthly savings and start thinking about real money. Open your savings account right now and ask yourself what amount you could pull out within 30 days without destroying your household finances. That number is your deductible ceiling, period. If you have $3,000 in emergency savings, a $2,000 deductible makes sense. If you have $1,200, a $1,000 deductible is the maximum you should consider. This isn’t conservative thinking; it’s basic financial self-defense.

The Federal Reserve found that 55 percent of adults had set aside money for three months of expenses in an emergency savings fund, which means many Utah families are selecting deductibles they cannot actually afford to pay. When hail damage hits your roof or a pipe bursts, you need cash available immediately. Your insurance company will not wait while you sell stocks, borrow from family, or take out a loan.

Stop Chasing Premium Discounts You Cannot Afford

The $100 to $200 monthly premium difference between a $500 deductible and a $2,000 deductible sounds meaningful until you realize you are essentially betting that you will never file a claim. Most Utah homeowners will file at least one claim during their 20-year tenure in a home, according to insurance industry data. If you save $150 monthly by selecting a $2,000 deductible instead of $500, you need to go 13 months without any claim whatsoever just to break even financially.

Weather events in Utah occur randomly and frequently enough that this bet fails for most households. The smarter calculation compares your likely out-of-pocket costs against your monthly savings. If raising your deductible from $1,000 to $2,000 saves you $120 annually but increases your maximum out-of-pocket risk by $1,000 per claim, you need to be absolutely certain you will not file a claim for five years to come out ahead. Life does not work that way.

Job changes, health crises, aging vehicles, and home maintenance surprises happen unpredictably. Your deductible selection should reflect the world as it actually exists, not as you hope it will be.

Adjust Your Deductible When Your Finances Change

Your deductible is not permanent. The Utah Insurance Department explicitly states that you can adjust your deductible during your annual renewal or by contacting your insurer. Many homeowners lock into a deductible choice and never revisit it, even when their circumstances change dramatically.

If you received an inheritance, sold a rental property, or built up your emergency fund substantially, you might safely increase your deductible now. Conversely, if you experienced a job loss, faced unexpected medical bills, or your household income declined, lowering your deductible immediately protects you even though your premium rises. This requires annual honesty about your financial position.

Schedule a conversation with your agent every January to review your deductible alongside your overall emergency savings capacity. A household with $10,000 in liquid savings can handle a $2,000 deductible with confidence. The same household with only $2,000 in savings absolutely cannot, regardless of premium savings. Treat your deductible review as a core financial health checkup, not just an insurance question.

Final Thoughts

Your home insurance deductible in Utah comes down to one honest question: what can you actually afford to pay out of pocket when damage happens? Stop calculating deductibles based on monthly premium differences alone. Instead, assess your emergency fund honestly, pick a deductible you can realistically pay within 30 days, and revisit that choice annually as your financial situation changes.

We at Direct Insurance Services understand that Utah homeowners face real weather risks and real financial constraints. As an independent agency based in Salt Lake City since 1973, we work with multiple top-rated insurance companies to find coverage that matches both your protection needs and your budget. Our team are locals who understand the specific risks of living in Utah, from hail corridors to wildfire zones.

Getting the right home insurance deductible in Utah takes more than an online calculator. Contact Direct Insurance Services today to discuss your deductible options and get a personalized quote that reflects your actual needs and financial reality.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation