Utah Auto Insurance Rates: What Affects Your Premium

Utah auto insurance rates vary dramatically based on where you live, how you drive, and what vehicle you own. At Direct Insurance Services, we’ve seen firsthand how small changes in your situation can shift your premium by hundreds of dollars each year.

This guide breaks down exactly what insurers look at when they calculate your costs and shows you concrete ways to pay less.

What Drives Your Utah Auto Insurance Premium

Your Driving Record Sets the Foundation

Your driving record is the single most important factor insurers examine. Maintaining a clean driving record can lower your premiums and make you eligible for discounts. A bad driving record can result in higher premiums. The message is clear: avoiding tickets and accidents directly translates to savings annually.

Age, Gender, and Life Circumstances

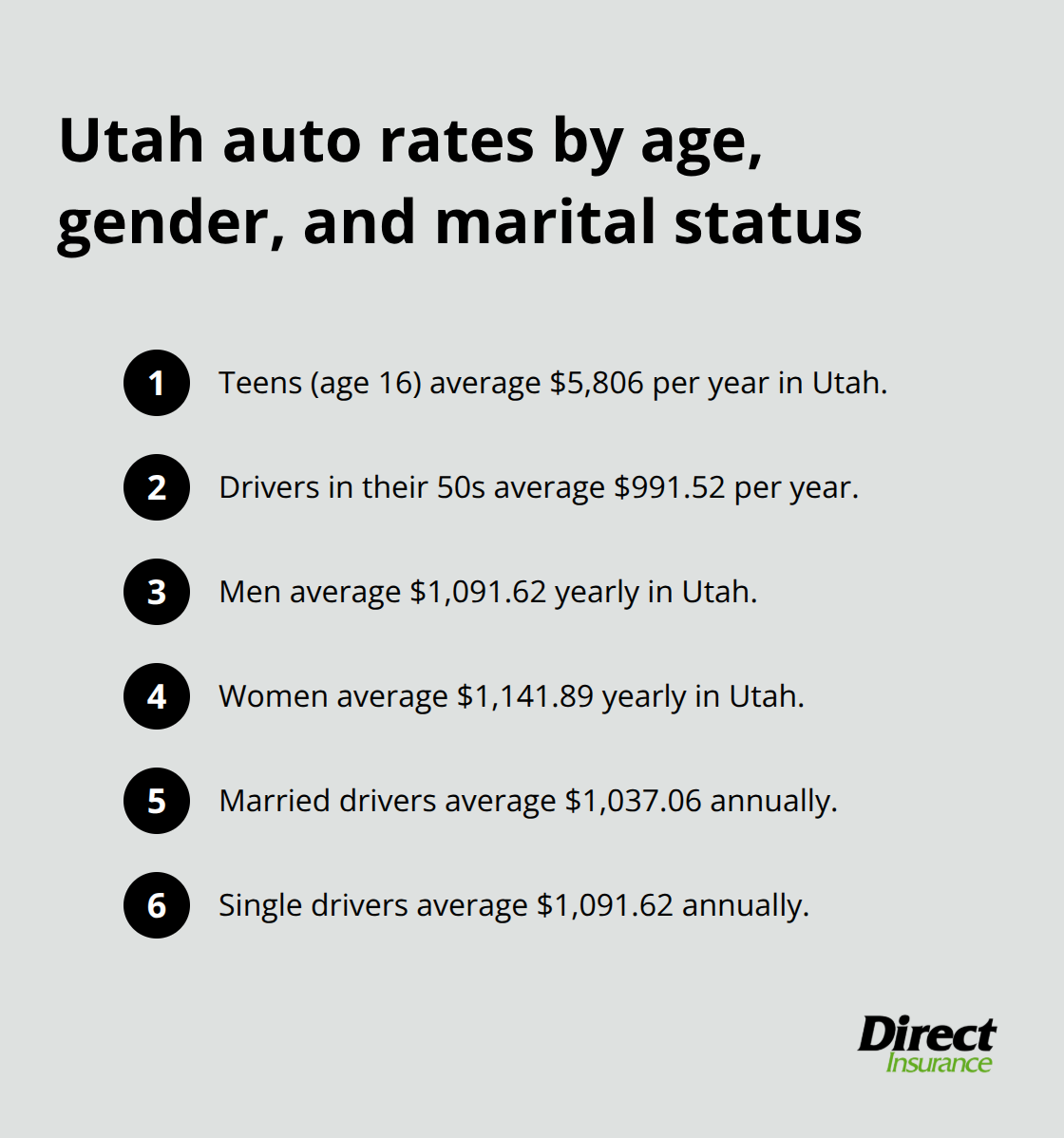

Age matters dramatically, but not equally across the board. A 16-year-old driver in Utah pays approximately $5,806 per year on average, while a driver in their 50s pays around $991.52 per year, according to The Zebra. This gap reflects genuine risk differences and explains why teen insurance costs so much. Gender differences exist but are smaller than most people assume-men in Utah average about $1,091.62 yearly while women average $1,141.89, per The Zebra data.

Marital status also shifts your rate slightly, with married drivers averaging $1,037.06 annually compared to single drivers at $1,091.62.

Vehicle Type, Location, and Credit History

Your vehicle type directly affects pricing based on repair and replacement costs. A high-performance car or luxury vehicle costs more to insure than a practical sedan because parts and labor are expensive. Location within Utah matters too-living in Salt Lake City’s denser traffic versus a rural area changes your premium because accident frequency and repair shop costs vary. Where you garage your vehicle also influences your rate since some neighborhoods experience higher theft or accident rates.

Credit history stands out as a massive lever most drivers overlook. The Zebra shows that drivers with exceptional credit (800–850) average $917.99 annually, while those with very poor credit (300–579) average $2,260.47. That’s a $1,342 annual difference driven entirely by credit score. Good credit (670–739) averages $1,423.92 per year, so improving your credit profile pays real dividends on your insurance bill.

Mileage, Safety Features, and Coverage Choices

Annual mileage affects premiums because more time on the road increases accident exposure. Low-mileage discounts exist at many carriers, and pay-per-mile programs let you align your costs with actual usage. Safety features on your vehicle matter as well-modern anti-collision systems and stability control can lower your premium at some insurers.

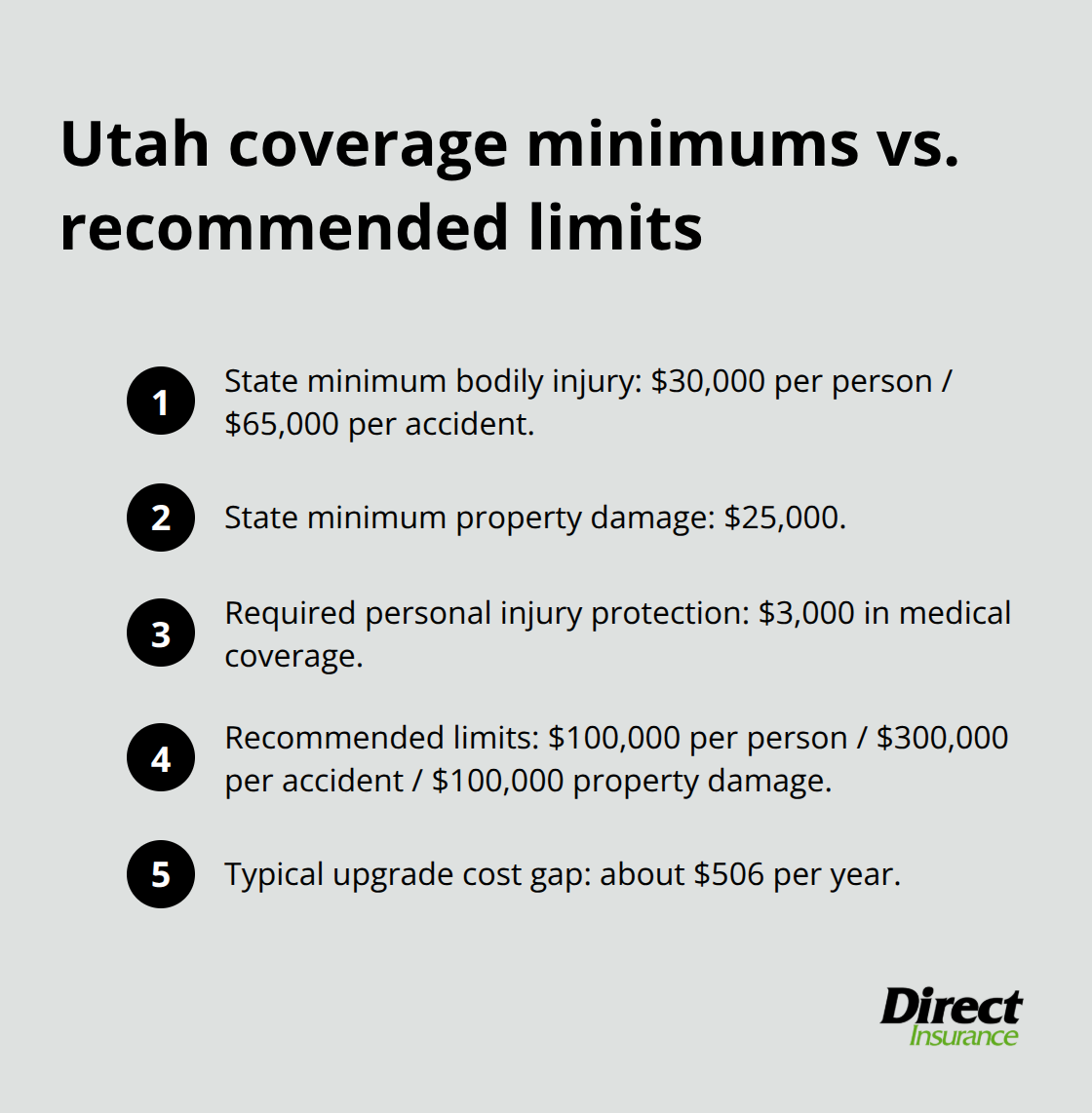

Utah requires $30,000 per person and $65,000 per accident for bodily injury liability, plus $25,000 for property damage and $3,000 in personal injury protection, but carrying these minimums leaves you significantly underprotected. Insurance experts generally recommend at least $100,000 per person and $300,000 per accident for bodily injuries plus $100,000 for property damage.

The coverage gap between state-minimum liability-only and comprehensive coverage with a $500 deductible is about $506 per year, according to The Zebra, so upgrading your protection doesn’t cost as much as you’d expect. Understanding these specific factors positions you to make smarter choices about what coverage actually makes sense for your situation and budget.

Why Utah’s Insurance Market Works Differently

Utah’s geography and local insurance landscape create premium pressures that differ significantly from national averages. Understanding these Utah-specific dynamics helps you recognize where your premium comes from and where you have real leverage to negotiate better rates.

Winter Weather and Mountain Terrain Drive Claim Costs

Utah’s mountain terrain means winter weather poses genuine risks. Snow and ice on mountain passes increase accident frequency and severity, which insurers factor into their calculations. The National Weather Service recorded multiple significant winter storms across Utah in recent years, driving up claim costs for carriers operating in the state. These weather patterns directly influence what insurers charge across the entire state, even in areas that experience milder winters.

Traffic Density Varies Dramatically Across Regions

Salt Lake City’s growing population has intensified traffic density in the valley, particularly along the I-15 and I-80 corridors, where accident rates climb during rush hours. Rural areas like Carbon County or Rich County experience lower accident frequencies, which translates to lower premiums for drivers in those regions. This geographic variation means two drivers with identical records and vehicles can pay substantially different premiums simply based on whether they live in Provo’s suburbs or a smaller community outside Moab.

Utah’s No-Fault System and State Minimum Requirements

Utah’s no-fault insurance system requires all drivers to carry personal injury protection covering medical costs up to their policy limit, which adds a mandatory expense that doesn’t exist in tort-based states. State minimum liability of $30,000 per person and $65,000 per accident sounds sufficient until you face a serious multi-vehicle accident where medical bills exceed these thresholds. Insurers price their policies knowing these minimums exist, but competition among Utah carriers-USAA, Liberty Mutual Direct, Root, and GEICO all operate aggressively in the state-means you can find meaningful rate variation by shopping quotes.

How Carrier Competition Creates Real Savings Opportunities

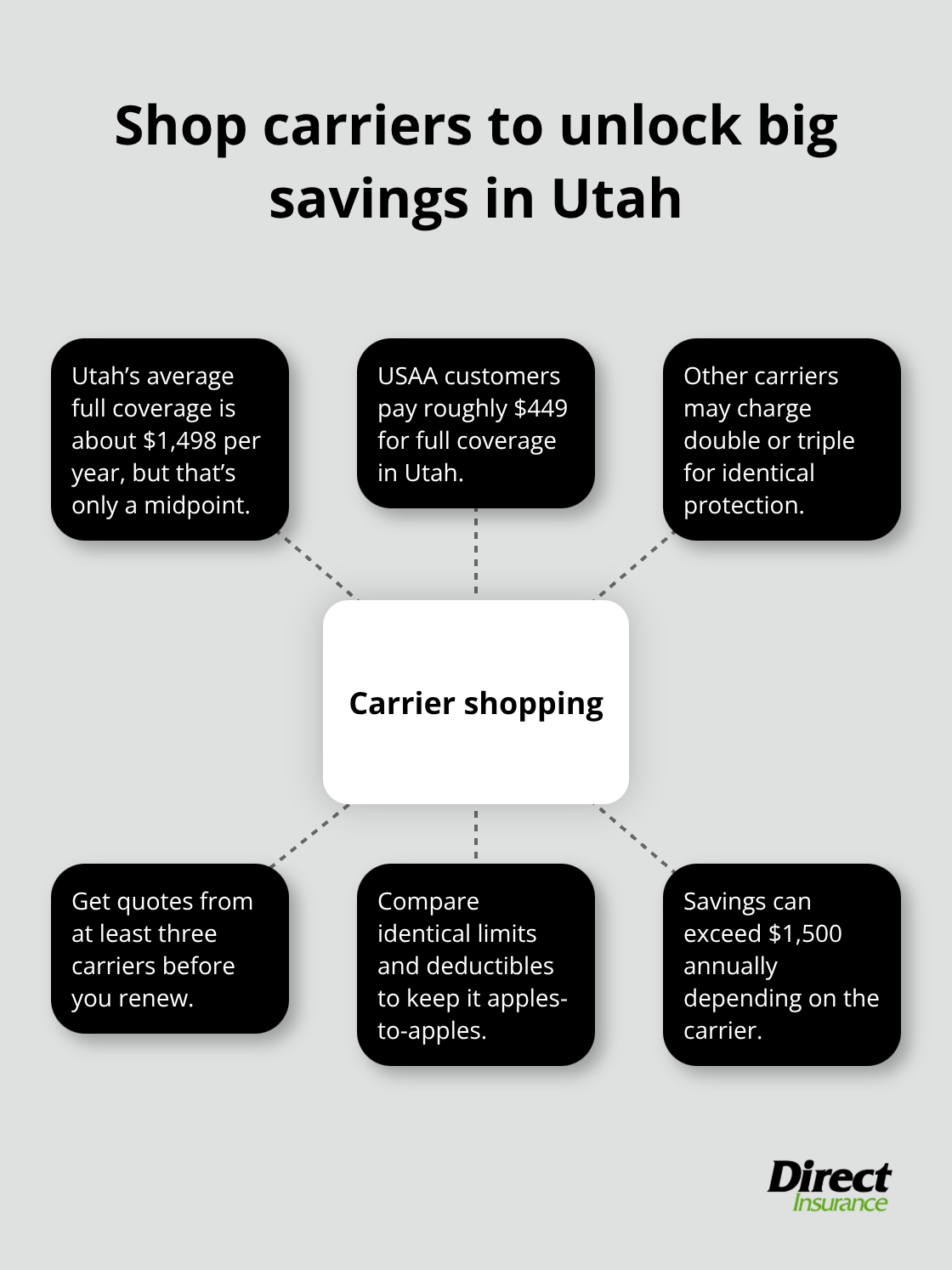

The Zebra’s analysis of over 83 million insurance rates shows Utah’s average full-coverage cost sits around $1,498 annually, which positions the state as relatively affordable compared to national trends. However, this average masks significant differences: USAA customers in Utah pay roughly $449 per year for full coverage, while other carriers charge double or triple that amount for identical protection. This disparity reflects each insurer’s underwriting philosophy and operating costs, not differences in coverage quality.

When you shop for quotes in Utah, you’re not just comparing prices-you’re comparing which carrier’s risk assessment and cost structure align best with your specific situation. Getting quotes from at least three carriers matters before you buy, and the variation you’ll find (sometimes hundreds of dollars annually) makes the effort worthwhile. Your next step involves identifying which specific discounts and coverage adjustments can lower your costs even further.

How to Cut Your Utah Auto Insurance Premium

Fix What You Control First

Your driving record directly determines your trajectory. Eliminate tickets and accidents over the next 24 to 36 months, and you’ll produce the single largest premium reduction available to you. The Zebra’s data shows a clean record averages $2,059 yearly in Utah while a single incident jumps you to $2,473, meaning one accident costs roughly $414 per year in perpetuity until that incident ages off your record. This isn’t theoretical-every ticket you avoid is money in your pocket.

Credit history delivers the second-fastest payoff. If you carry poor credit, dedicate three to six months to paying down balances and making on-time payments. Your score can shift enough to lower your premium by $400 to $600 annually. The Zebra confirms that exceptional credit (800–850) costs $917.99 yearly versus very poor credit at $2,260.47, so this lever works regardless of your age or location.

Restructure Your Coverage Strategically

Coverage restructuring offers immediate savings without waiting months for results. Raise your deductible from $500 to $1,000 on comprehensive and collision coverage, and you’ll typically reduce your premium by 15 to 30 percent, depending on your vehicle’s value and your financial cushion. State-minimum liability-only coverage costs around $502 yearly according to The Zebra, while adding $1,000 comprehensive and collision jumps that to $902. If your car is paid off and worth less than $8,000, dropping collision coverage entirely makes financial sense.

Bundling your auto policy with homeowners or renters insurance produces 10 to 25 percent savings across both policies at most carriers. This discount applies immediately without waiting for anything to change on your driving record.

Shop Aggressively Across Carriers

Shop for quotes from at least three carriers before you renew. USAA, Liberty Mutual Direct, Root, GEICO, and Clearcover all compete aggressively in Utah, and rate variation exceeds $1,500 annually for identical coverage. The Zebra analyzed over 83 million rates and found USAA customers pay approximately $449 for full coverage while other carriers charge significantly more, confirming that your current insurer’s quote doesn’t represent your only option.

Request quotes using identical coverage limits and deductibles across each carrier so you’re comparing apples to apples. Don’t settle for the first reasonable price you find. The variation you’ll discover (sometimes hundreds of dollars annually) makes the effort worthwhile.

Final Thoughts

Your Utah auto insurance rates reflect a mix of factors you control and factors you cannot. Your driving record, credit history, and coverage choices sit squarely in your hands, while age, location, and vehicle type shape your premium from the outside. The concrete path forward starts with eliminating tickets and accidents over the next two to three years-this produces the largest premium reduction available. Improving your credit score if it sits below 740 saves you over $1,300 annually compared to poor credit, and restructuring your coverage by raising deductibles and dropping unnecessary add-ons on older vehicles delivers immediate savings without waiting for anything to change.

Utah’s specific conditions-winter weather, mountain terrain, traffic density in Salt Lake City, and the state’s no-fault system-create premium pressures that differ from national averages. Local carriers compete aggressively here, which means your shopping effort yields meaningful results. USAA, Liberty Mutual Direct, Root, and GEICO all operate in Utah with substantially different pricing, sometimes varying by over $1,500 annually for identical protection. Bundling your auto policy with homeowners or renters insurance produces 10 to 25 percent savings across both policies at most carriers.

We at Direct Insurance Services understand Utah’s unique insurance landscape because we’ve served this community since 1973. As locals, we know how mountain winters affect claims, where traffic density spikes, and which carriers offer the best rates for your specific situation. Contact us to review your policy and discover where you’re overpaying on Utah auto insurance rates.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation