Landlord Liability Coverage Utah: Understanding Your Responsibilities

Owning rental property in Utah comes with real financial exposure. A single lawsuit from an injured tenant or guest can cost you tens of thousands of dollars-or more.

At Direct Insurance Services, we help landlords protect their assets with proper landlord liability coverage in Utah. This guide walks you through what you need to know about your responsibilities and how to choose the right protection for your situation.

What Landlord Liability Coverage Actually Protects

Landlord liability coverage shields you from third-party claims when someone gets injured on your property or you accidentally damage their belongings. This protection stands separate from the dwelling coverage that protects your building itself. The Insurance Information Institute reports that attorney fees in liability cases typically range from $162 to $392 per hour, which means even a small dispute can accumulate thousands in legal costs before settlement.

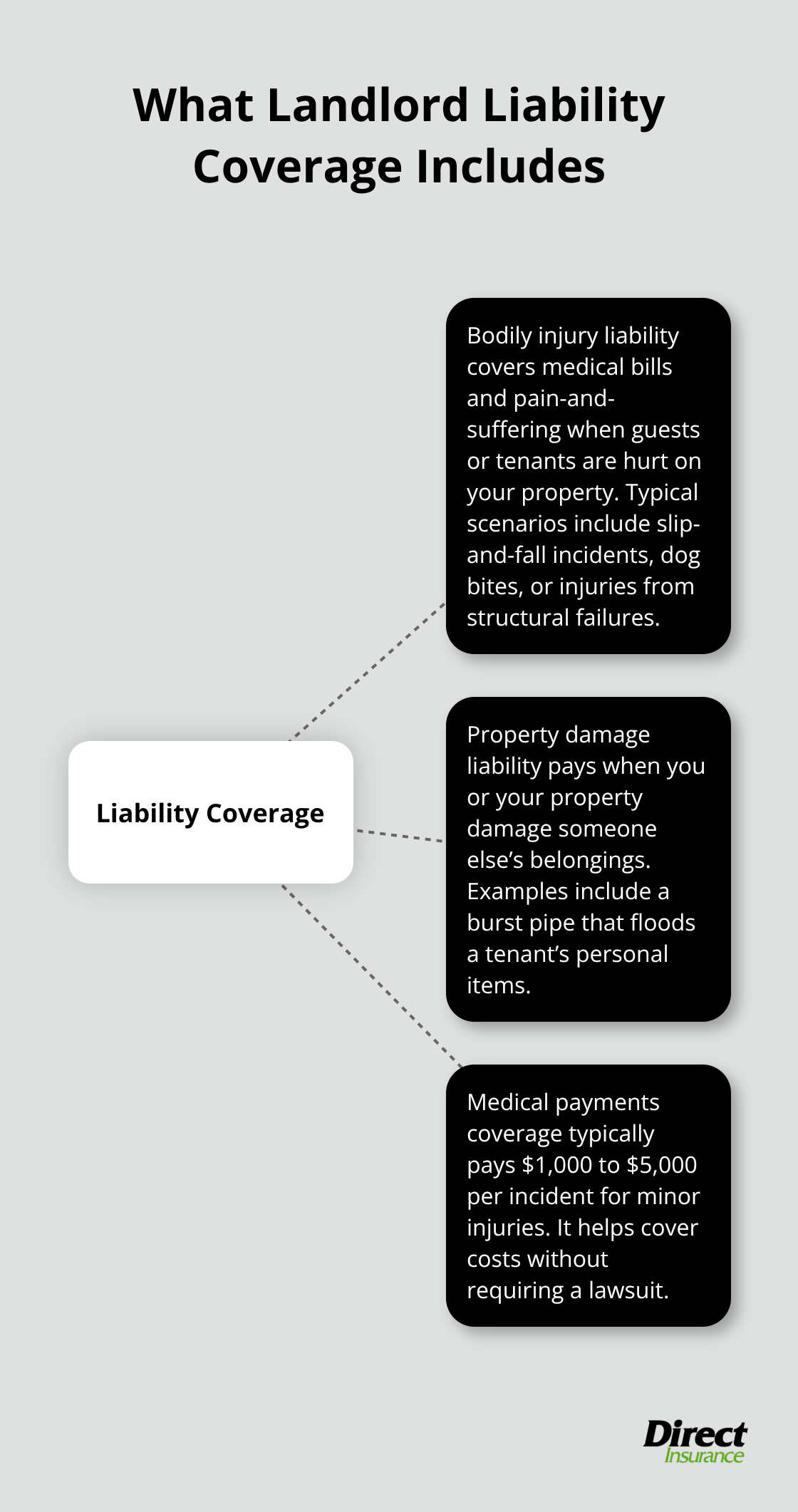

Two Types of Liability Protection

Your landlord liability policy covers two distinct areas. Bodily injury liability handles medical bills and pain-and-suffering claims when a guest or tenant gets hurt on your property-slip-and-fall injuries from ice or broken stairs, dog bites from animals on the premises, or injuries from structural failures like a ceiling collapse are common examples. Property damage liability covers situations where you or your property damage someone else’s belongings, such as a burst pipe that floods a tenant’s personal items.

Most policies also include medical payments coverage, typically $1,000 to $5,000 per incident, which pays smaller injury expenses without requiring a lawsuit. Standard liability limits start around $300,000 per occurrence for a single-family rental, but the Insurance Information Institute recommends $1 million or more for multi-unit buildings or high-value properties. A single serious injury can easily exceed $50,000 in medical bills alone, and jury awards in negligence cases often reach six figures, which is why underestimating your limits exposes you to real financial danger.

Utah’s Legal Requirements and Lender Expectations

Utah does not legally require landlords to carry liability insurance, which means some property owners skip it entirely and expose themselves to catastrophic financial risk. However, most lenders require it as a condition of your mortgage. The real protection comes from requiring your tenants to carry renters insurance with their own liability coverage-this transfers significant risk away from you.

When a tenant has liability coverage, their insurer handles claims for guest injuries or accidental damage rather than your policy footing the bill. Typical renters insurance costs tenants about $15 to $30 per month in Utah, making it an inexpensive way for them to protect themselves and reduce your exposure. Your lease should explicitly require renters insurance and name you as a certificate holder, so you can verify coverage remains active.

Building a Two-Layer Protection System

Combining your landlord liability policy with tenant liability coverage creates a two-layer protection system that proves far more effective than relying on either one alone. This approach means that when injuries or property damage occur, multiple insurance policies can respond to claims, protecting both your assets and your tenants’ interests. The next section examines the specific liability risks that Utah landlords face most often and how your coverage responds to each scenario.

What Liability Risks Actually Cost Utah Landlords

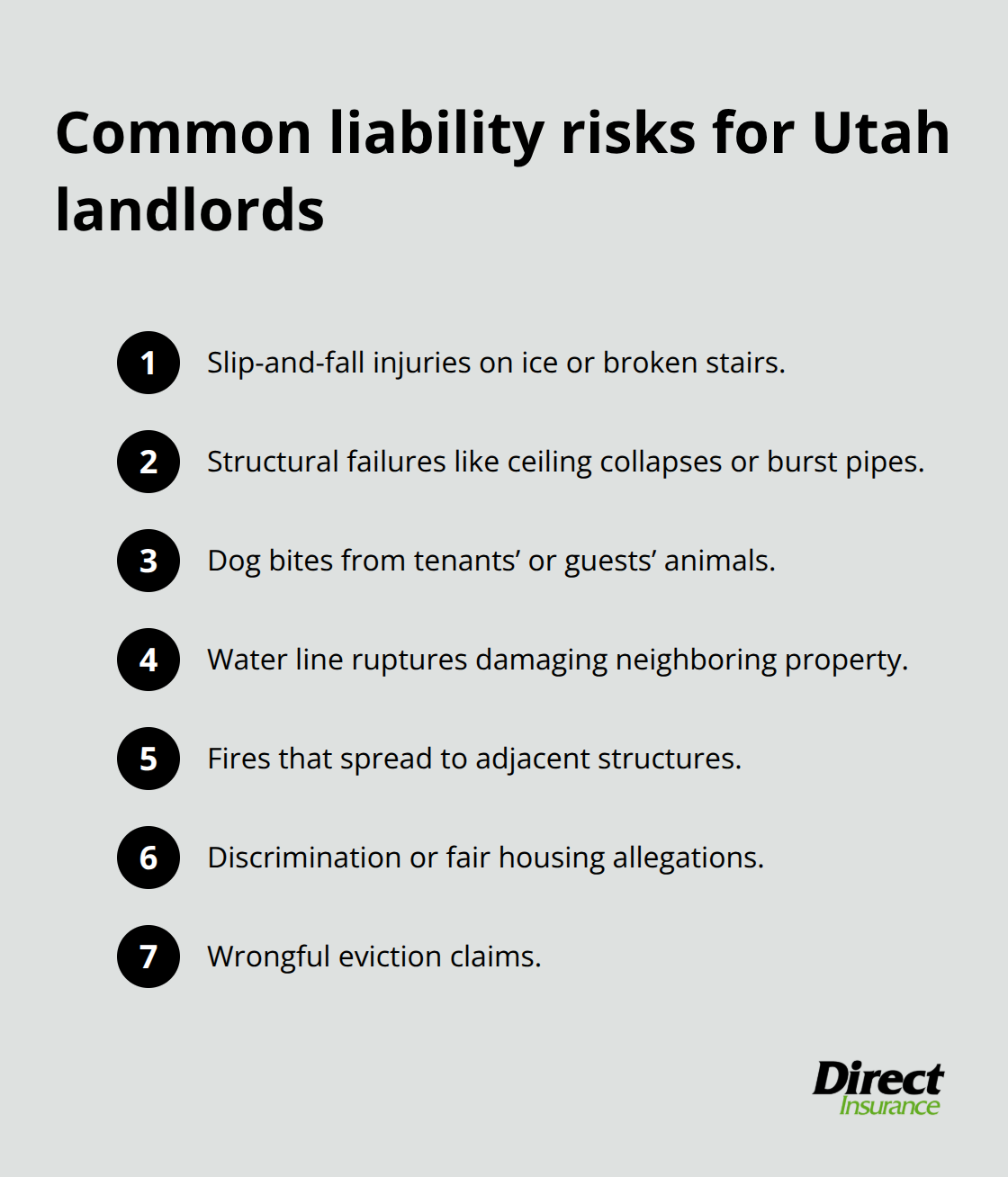

Slip-and-Fall Injuries: The Most Common and Expensive Claims

Slip-and-fall injuries represent the most frequent liability claim landlords face, and they cost far more than most property owners expect. A guest slips on ice near your entryway or trips on a broken stair, and you face medical bills, legal defense costs, and potential settlement demands. Serious slip-and-fall cases regularly exceed $50,000 in medical expenses alone. When attorneys enter the picture at $162 to $392 per hour, even a straightforward case accumulates $10,000 to $15,000 in legal fees before any settlement occurs.

Structural failures like ceiling collapses or burst pipes create similar exposure-a burst pipe that floods a guest’s belongings or causes injury puts your liability coverage directly at risk. Dog bites from animals on your property rank as another frequent claim, especially if you allow tenants to keep pets without strict restrictions. These incidents strike fast, and without adequate liability limits, a single occurrence depletes your personal assets within months.

Property Damage Claims and Neighbor Disputes

Property damage claims often escape the attention of landlords who focus only on bodily injury scenarios. A water line rupture that damages a neighbor’s foundation, or a fire that spreads to an adjacent structure, triggers claims well beyond what standard coverage provides. These situations expose you to liability that extends beyond your property line and into your neighbors’ homes and assets. The costs mount quickly when structural damage or environmental contamination enters the picture, making adequate property damage limits essential for protecting your financial security.

Discrimination and Fair Housing Violations

Discrimination and fair housing violations represent a distinct category of liability that many Utah landlords underestimate. Wrongful eviction claims, housing discrimination allegations, or violations of fair housing laws create significant legal exposure. Personal injury coverage protects against discrimination and wrongful eviction allegations, typically costing only an extra $50 to $100 annually but shielding you from serious financial exposure. Many Utah landlords skip this endorsement, assuming it won’t apply to them, then face devastating costs when a tenant alleges discrimination. Liability strikes without warning-it emerges from tenant disputes, guest accidents, or property conditions you didn’t recognize as risks. Your liability limits must reflect actual injury costs in today’s healthcare environment, not outdated assumptions about medical expenses. Understanding these real-world costs shapes how you approach coverage limits and endorsements, which leads directly to the critical decision of selecting the right protection for your specific property and risk profile.

How to Choose the Right Landlord Liability Coverage for Your Utah Property

Calculate Your Real Exposure Before Selecting Limits

The gap between what landlords think they need and what actually protects them financially is where most coverage decisions fail. Utah landlords often accept whatever limit appears in an online quote without calculating their real exposure. Start by knowing your property’s replacement value-not what you paid for it, but what it would cost to rebuild today. Then multiply that number by 1.5 to account for construction cost inflation and unexpected complications. If your property would cost $400,000 to rebuild, you need liability limits that reflect potential claims exceeding medical bills alone.

A serious injury case with surgery, ongoing physical therapy, and pain-and-suffering damages reaches $100,000 to $300,000 fast. The Insurance Information Institute data shows that attorney fees alone consume $162 to $392 per hour, meaning even straightforward disputes accumulate $10,000 to $20,000 in legal costs before settlement. For single-family rentals, starting at $300,000 per occurrence leaves you dangerously exposed. Increasing limits to $500,000 or $1 million costs roughly $20 to $40 annually more than baseline coverage-a trivial expense compared to the financial catastrophe of an underinsured claim.

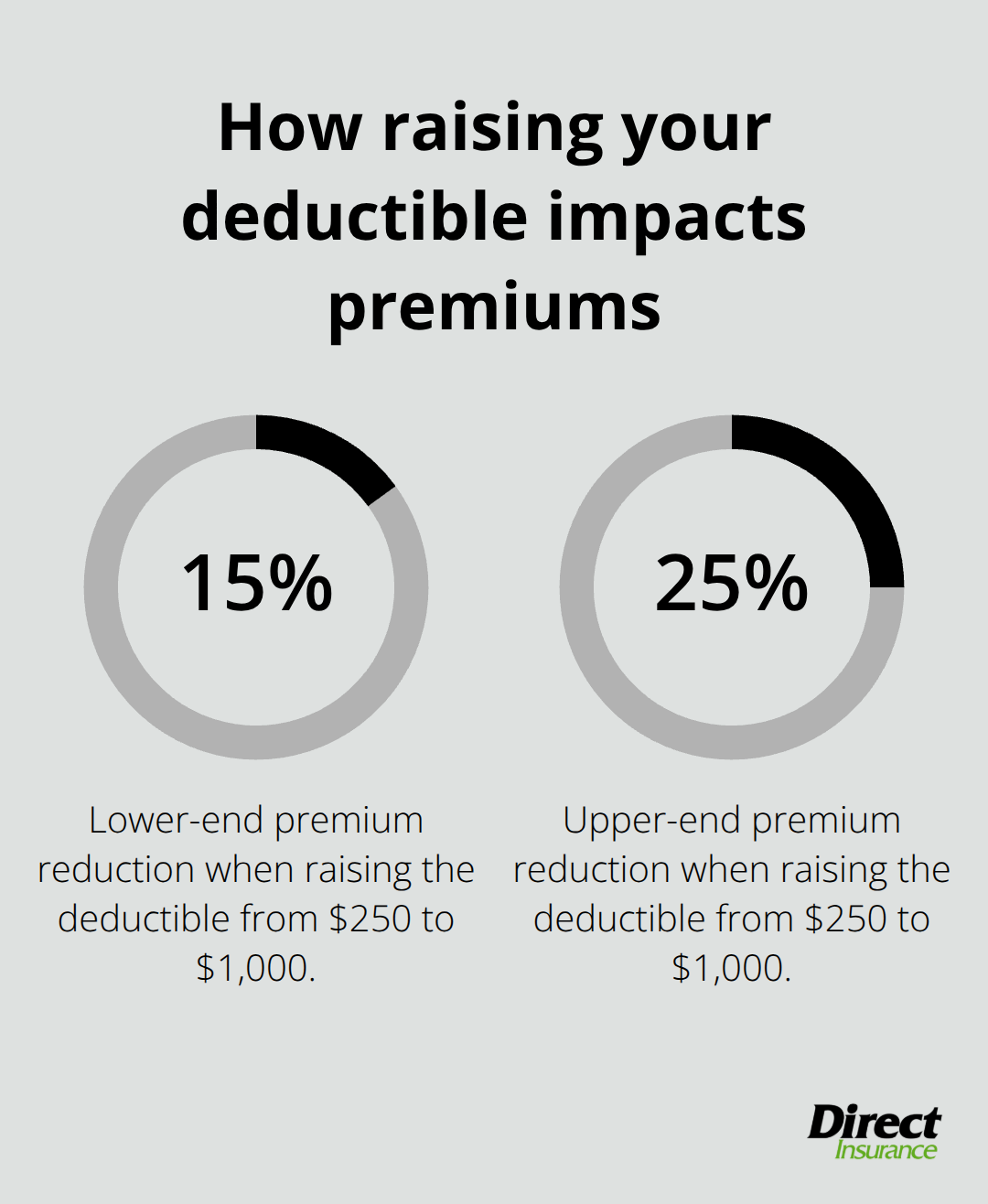

Multi-unit properties and those with pools, trampolines, or other high-risk features demand $1 million minimums. Your deductible directly impacts your out-of-pocket exposure during claims. Raising your deductible from $250 to $1,000 cuts premiums by 15 to 25%, but only choose this strategy if you can actually write a check for $1,000 when a claim hits. Most landlords cannot absorb $5,000 to $15,000 in defense costs before settlement, which is why low deductibles protect your cash flow even when they cost slightly more in premiums.

Understand Policy Forms and Coverage Gaps

Online insuretech platforms deliver cheap quotes by stripping away coverage you actually need. These services quote standard DP-2 forms when your property qualifies for DP-3 Special Form coverage, which provides replacement cost rather than actual cash value. The difference matters enormously when you file a claim-DP-3 reimburses replacement cost while DP-2 deducts depreciation, potentially reducing payouts by 30 to 50 percent.

Utah-specific risks like winter storms, wildfires, and earthquake exposure require endorsements that online tools miss entirely. Personal injury coverage protecting against discrimination and wrongful eviction claims costs $50 to $100 annually but shields you from six-figure legal exposure. Service line insurance covering sewer and water line repairs runs $10 to $15 monthly through providers like HomeServe yet prevents catastrophic replacement costs exceeding $10,000. Comparing policies requires examining the form type, endorsements included, actual coverage limits, and deductible structure-not just the premium amount.

Work with Local Agents Who Understand Utah Rental Risks

Agents who work with Utah landlords regularly know which carriers offer the best rates for duplexes versus single-family rentals, which underwriters accept aggressive dogs without exclusions, and how to structure coverage so claims actually get paid. They understand the specific property type, occupancy, and risk profile in ways that no algorithm can replicate. Schedule a policy review annually or whenever you make renovations, acquire additional properties, or experience tenant turnover. Your coverage from three years ago does not reflect today’s construction costs, medical inflation, or changes to your property’s condition.

Require your tenants to carry renters insurance with liability limits matching their actual exposure, then request certificates of insurance annually to verify active coverage. This two-layer protection system means claims get distributed across multiple policies instead of concentrating risk on your landlord policy alone. When a tenant has liability coverage, their insurer handles claims for guest injuries or accidental damage rather than your policy footing the bill. Typical renters insurance costs tenants about $15 to $30 per month in Utah, making it an inexpensive way for them to protect themselves and reduce your exposure.

Final Thoughts

Landlord liability coverage in Utah protects your financial security when injuries or property damage claims strike your rental property. A single lawsuit costs tens of thousands in legal fees and settlements, which is why accepting an online quote without understanding your actual exposure leaves you financially vulnerable. Your coverage decision determines whether a claim depletes your personal savings or gets handled by insurance, so calculate your real exposure by knowing your property’s replacement value and the medical costs associated with serious injuries in today’s healthcare environment.

A $300,000 liability limit for a single-family rental leaves you dangerously exposed when serious injury cases regularly exceed $100,000 in medical bills alone. Increasing limits to $500,000 or $1 million costs only $20 to $40 more annually-a trivial expense compared to the financial catastrophe of underinsurance. Require your tenants to carry renters insurance with adequate liability limits and request certificates of insurance annually, since this two-layer protection system distributes claims across multiple policies instead of concentrating risk entirely on your landlord policy.

Work with an insurance professional who understands Utah rental risks rather than relying on algorithm-driven quotes that strip away essential coverage. Online platforms deliver cheap quotes by omitting endorsements like personal injury coverage protecting against discrimination claims or service line insurance covering sewer and water line repairs-additions that cost $50 to $100 annually but shield you from six-figure legal exposure. Contact us at Direct Insurance Services to shop multiple top-rated insurance companies and find landlord liability coverage in Utah that actually protects your assets at competitive rates.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation