Utah Auto Insurance Tips: Save Money And Stay Covered

Utah drivers face distinct challenges that most other states don’t. Mountain passes, winter storms, and remote roads all push insurance costs higher and create real coverage gaps.

We at Direct Insurance Services know that generic auto insurance tips won’t cut it here. That’s why we’ve put together Utah auto insurance tips specifically designed for the conditions you actually drive in.

Why Utah’s Terrain Drives Up Your Insurance Costs

Winter driving creates measurable risk in Utah isn’t just an inconvenience-it directly impacts what you pay for auto insurance. The state experiences significant seasonal variation, with mountain passes regularly closing and valley roads becoming hazardous during heavy snow. Insurance companies factor this into their rates because winter conditions affect premiums. Your insurer knows that drivers navigating switchbacks at elevation face different hazards than drivers on flat highways. This is why a driver in Salt Lake City typically pays more than someone in Arizona, even with an identical driving record. The terrain itself is baked into your premium calculation.

Mountain passes demand higher coverage limits

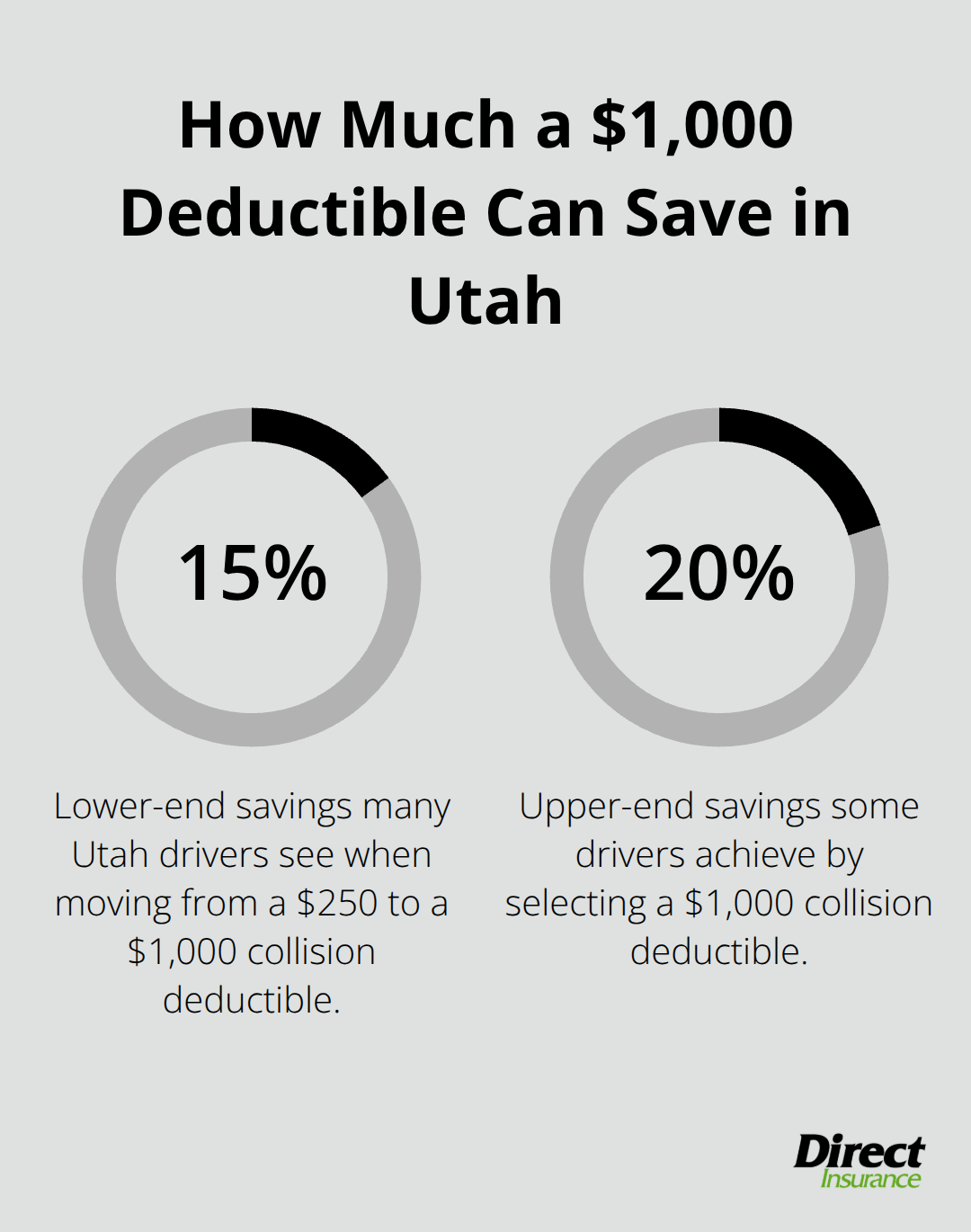

The real cost of Utah terrain shows up when you need comprehensive and collision coverage. If you drive a vehicle worth $20,000 and you collide with wildlife or slide off a mountain road, that damage claim hits quickly. Insurance companies have claims data showing that comprehensive claims-which cover weather, wildlife, and theft-occur at higher rates in Utah than in flat states. A collision on I-80 near Parley’s Canyon can total a vehicle in seconds. This means skimping on collision coverage to save $30 per month is genuinely risky. Rural routes like US-191 heading toward the Uinta Basin see fewer accidents overall but more severe ones when they occur, partly because emergency services respond slower. Your deductible choice matters enormously here. A $1,000 deductible saves roughly 15–20% on collision premiums compared to a $250 deductible, but only if you can afford to pay that amount out-of-pocket after an accident.

Altitude and vehicle maintenance raise long-term costs

High-altitude driving in Utah accelerates wear on engines, transmissions, and brakes. Vehicles that operate regularly above 8,000 feet experience faster component degradation, leading to higher repair costs when claims are filed. Insurance companies adjust rates based on expected repair costs in your area. Northern Utah’s elevation means brake jobs, transmission fluid flushes, and engine work cost more than in lower-elevation states. This feeds back into your premium over time. Additionally, winter salt on roads corrodes undercarriages faster at altitude, increasing the likelihood of rust-related damage that comprehensive coverage would address.

Remote roads require strategic coverage choices

Remote areas of Utah-from the Uinta Basin to the San Rafael Swell-have limited emergency infrastructure. If you break down on a rural highway, towing costs are substantially higher because the nearest shop might be 50 miles away. Standard towing coverage usually caps at $100–$150, which barely covers a 30-mile tow in rural Utah. Adding uninsured motorist coverage becomes genuinely valuable in these areas because you encounter uninsured drivers more frequently on remote roads, and your own coverage protects you when they cause an accident. These terrain-specific risks mean your coverage strategy must account for where you actually drive, not just your driving record or vehicle type. The next section shows you exactly how to lower what you pay while maintaining the protection Utah’s conditions demand.

How to Cut Your Utah Auto Insurance Costs Without Sacrificing Protection

Lowering your auto insurance premium in Utah requires a different strategy than what works in other states. Generic cost-cutting tactics often leave Utah drivers underinsured for the exact risks we outlined earlier. Too many drivers save $20 per month by dropping comprehensive coverage, only to file an $8,000 wildlife damage claim on a remote highway.

Bundle your home and auto policies for immediate savings

The most impactful way to reduce your premium is combining your auto policy with homeowners or renters insurance. State Farm data shows bundled customers save roughly 15–25% on their total insurance costs, and Progressive reports similar savings when customers combine auto with home coverage. If you own your home in Utah, this single move delivers the largest financial benefit.

A homeowner paying $1,200 annually for home insurance might cut that to $1,000 while simultaneously reducing auto premiums by $150–$300 per year. Insurers reward loyalty and reduced administrative costs. Shop this bundled rate explicitly-many drivers don’t realize they’re eligible until they ask.

Raise your deductible strategically based on your driving patterns

Your deductible choice deserves hard analysis because Utah’s terrain changes the math compared to flat states. A $500 deductible costs roughly 10–15% more annually than a $1,000 deductible, translating to $120–$180 extra per year. If you have six months of emergency savings and drive mountain passes regularly, the $1,000 deductible makes financial sense. You essentially self-insure the first $1,000 of damage in exchange for lower premiums.

However, if you drive primarily in Salt Lake City valley and rarely venture into high-risk terrain, the lower deductible provides better protection relative to cost. Rural drivers and those with older vehicles worth under $15,000 should seriously consider raising deductibles because collision claims on low-value cars often approach your deductible amount anyway.

Capture discounts for safety features and low mileage

Modern vehicles with forward collision warning, automatic emergency braking, and lane-keeping assist qualify for vehicle safety discounts that reduce premiums by 5–10%. If you drive a 2020 or newer vehicle with these features, request the safety discount explicitly-many drivers miss this because insurers don’t automatically apply it.

Low-mileage discounts apply if you drive under 10,000–12,000 miles annually, which matters for rural Utah residents who work from home or live close to their workplace. Progressive and State Farm both offer these discounts, typically reducing premiums by 5–15% depending on your actual mileage. If you’ve shifted to remote work, contact your insurer immediately to report lower mileage and capture this savings.

Use telematics programs to reward safe driving behavior

Telematics programs like Progressive’s Drive Safe & Save can deliver up to 30% or 40% discount if you’re a genuinely safe driver, though this requires installing a monitoring app that tracks acceleration, braking, and speeding. Rural drivers often benefit most from telematics because your actual driving behavior (not accident frequency in your area) determines the discount.

Document your current premium and the exact coverage limits you carry, then shop competing quotes from at least three carriers while specifying identical deductibles and limits. Comparing $100/month quotes across different deductibles or coverage amounts is worthless-apples-to-apples comparison requires matching every variable. Utah’s geography means your current insurer’s rate may jump significantly at renewal even with a clean driving record, so shopping every two years protects you against this creep. Once you’ve identified your best rate and coverage combination, the next step involves understanding which coverage types actually matter most for Utah’s specific driving environment.

Coverage That Actually Protects Utah Drivers

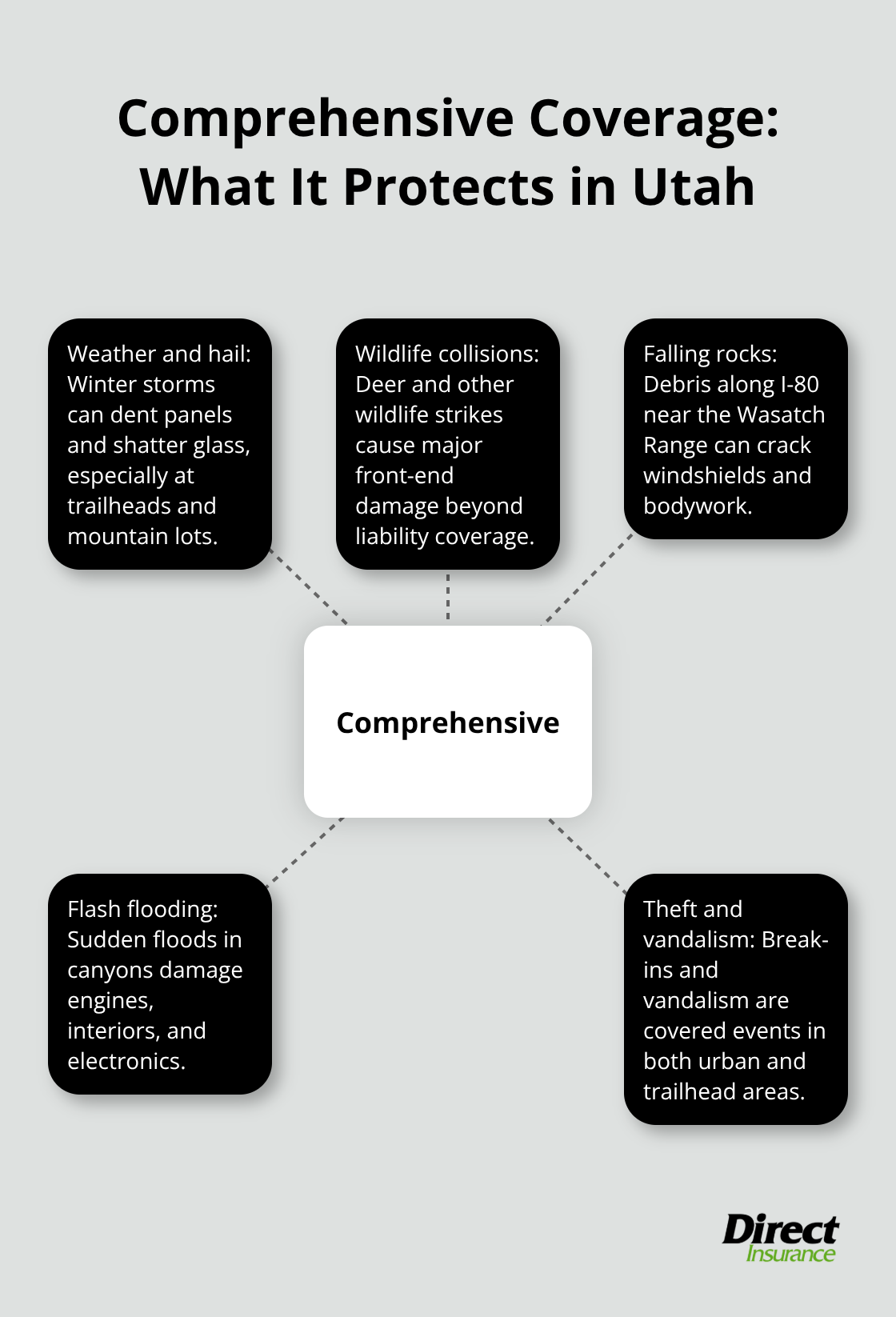

Comprehensive coverage stops being optional the moment you drive regularly in Utah’s mountains or remote areas. This coverage pays for weather damage, wildlife collisions, theft, and vandalism-the exact scenarios that occur constantly on Utah roads. A mule deer collision at 60 mph on US-191 causes significant damage, far exceeding what liability coverage addresses. Winter storms dump hail on your vehicle while parked near a trailhead, falling rocks strike I-80 near the Wasatch Range, or flash flooding sweeps through slot canyons-all trigger comprehensive claims. If you own a vehicle worth more than $10,000 and drive outside Salt Lake City regularly, dropping comprehensive coverage to save $40 monthly is financially reckless. The math is simple: one wildlife collision wipes out five years of premium savings.

Why comprehensive coverage matters more in Utah terrain

Rural Utah residents should set comprehensive deductibles at $250 or $500 rather than $1,000 because comprehensive claims occur more frequently in mountain and remote terrain than collision claims. Your insurer knows this through their own claims data, which is why they price comprehensive lower than collision in high-elevation areas. The frequency of weather events, wildlife encounters, and theft in Utah’s backcountry means you’ll file comprehensive claims more often than drivers in flat states. Setting a lower deductible on comprehensive coverage specifically (while keeping collision deductible higher) lets you protect against frequent, smaller claims while self-insuring larger collision risks.

Uninsured motorist coverage in remote areas

Uninsured motorist coverage becomes genuinely critical in rural Utah where enforcement is limited and uninsured driver rates exceed state averages. If an uninsured driver hits you on a remote highway, your uninsured motorist coverage pays for your medical bills, lost wages, and vehicle damage up to your policy limit. Utah law requires this coverage, but many drivers choose minimum limits of $15,000 to $25,000 when they should carry $50,000 or more given Utah’s terrain and accident severity. A serious injury claim from a multi-vehicle pile-up on I-80 during a snowstorm easily exceeds $100,000 in medical costs. The isolation of rural Utah means emergency response times stretch longer, injuries worsen during transport, and medical bills climb faster than in urban areas.

Liability limits that match your actual financial exposure

Liability limits deserve the same scrutiny because Utah’s asset protection laws don’t shield you from judgments above your policy limits. If you cause an accident and carry only the state minimum of $25,000 in bodily injury liability, a settlement exceeding that amount becomes your personal responsibility. Utah drivers need liability limits of at least $100,000 per person and $300,000 per accident to match their actual financial exposure. A $15 monthly increase to jump from $25,000 to $100,000 in bodily injury liability is the cheapest risk management available. Higher limits protect your home, savings, and future wages if you’re found liable for a serious accident.

Final Thoughts

Utah’s terrain, weather patterns, and remote roads demand auto insurance strategies that differ fundamentally from generic advice. Your coverage must match where you actually drive, not just your driving record or vehicle type. Bundling policies, raising deductibles strategically, and capturing safety discounts work together to lower your premium while comprehensive and uninsured motorist coverage protect you against the specific risks Utah presents.

The challenge most Utah drivers face isn’t understanding what coverage matters-it’s finding the right balance between cost and protection while navigating quotes from multiple carriers. Each insurer prices risk differently, and what works for your neighbor may cost significantly more for your situation. We at Direct Insurance Services have been helping Utah residents apply these Utah auto insurance tips since 1973, and our team understands the unique risks of living here because we live here.

Your next step is straightforward: review your current policy and compare it against the coverage principles outlined in this post. Then contact Direct Insurance Services to shop your coverage across multiple carriers. We’ll match your exact deductibles and limits across quotes so you’re comparing apples to apples, and we’ll identify discounts you’re currently missing.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation