SR-22 Auto Insurance Utah: What It Means For Your Drive

An SR-22 filing in Utah isn’t a punishment-it’s a path forward. If you’ve had a serious driving violation, your state requires this certificate of financial responsibility to get back on the road legally.

At Direct Insurance Services, we help Utah drivers navigate SR-22 requirements without overpaying. This guide walks you through what SR-22 means, how it affects your rates, and exactly how to move past it.

What Is SR-22 and Why Utah Requires It

Understanding the SR-22 Certificate

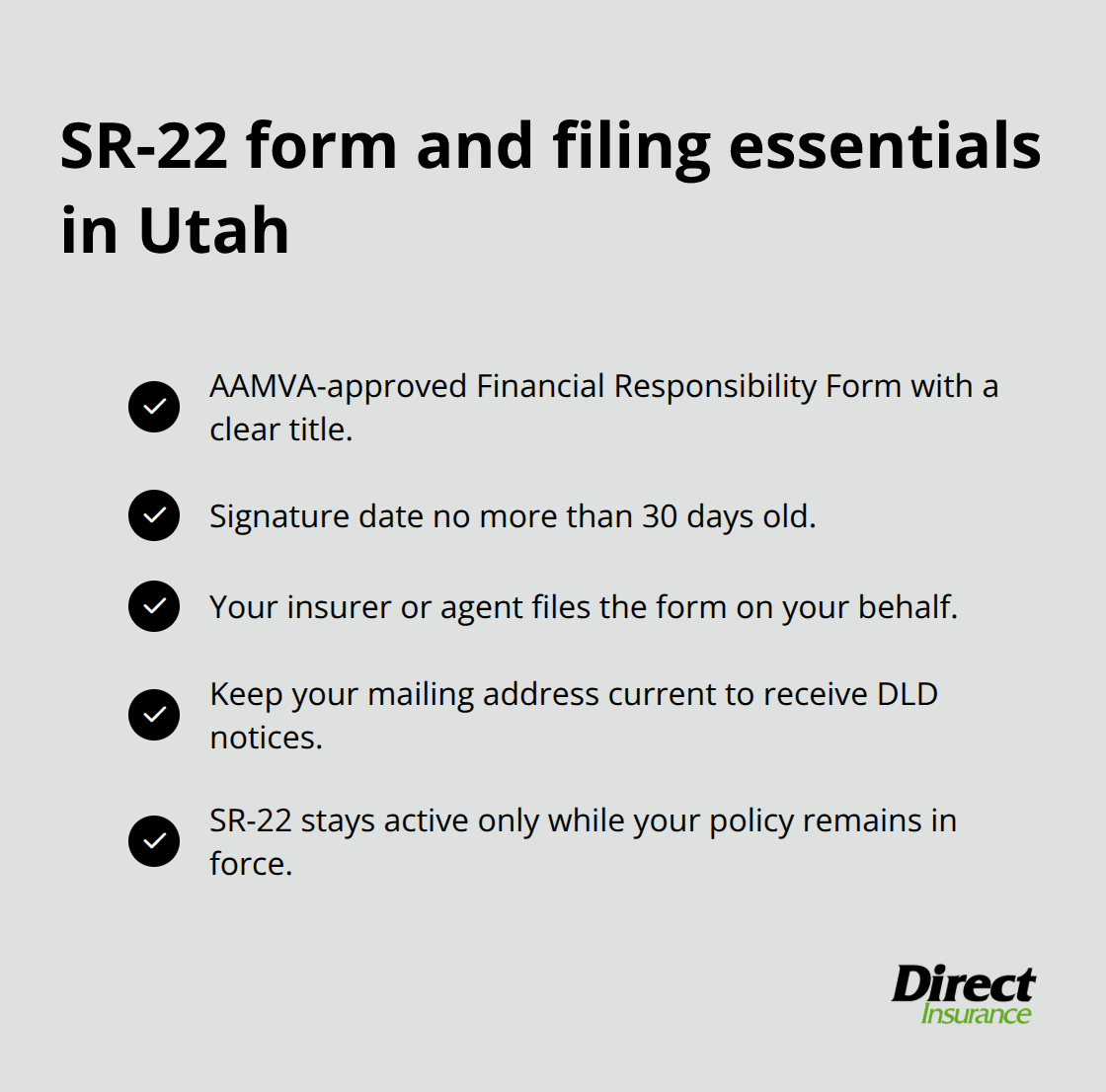

An SR-22 is a certificate of financial responsibility that your insurance company files with Utah’s Driver License Division. It’s not a separate insurance policy-it’s proof attached to your existing auto insurance that you carry the state’s minimum liability coverage. Utah requires SR-22 filings after specific violations because the state takes financial responsibility seriously. The Driver License Division mandates this form when you’ve had a conviction for driving without insurance, been involved in an uninsured accident, received a court order for damages from an uninsured incident, or failed to provide satisfactory proof of security with a Driving Privilege Card. A DUI conviction also triggers the requirement.

What the Form Requires

The form itself must be the AAMVA-approved Financial Responsibility Form, clearly titled at the top with a signature date no more than 30 days old. Your insurer or agent handles the filing-you don’t submit it yourself. The DLD will mail you a notice if you need one, so keeping your address current matters. Once filed, the SR-22 stays active only as long as your policy remains in force.

How Long You Must Maintain Coverage

Utah law specifies that you must maintain SR-22 coverage for three years from your conviction date, though the exact duration depends on your specific violation. The state’s minimum liability limits are $25,000 for bodily injury to one person, $65,000 per accident, and $25,000 for property damage, plus $3,000 in Personal Injury Protection. Your policy must meet these minimums for the SR-22 to be valid.

What SR-22 Costs You

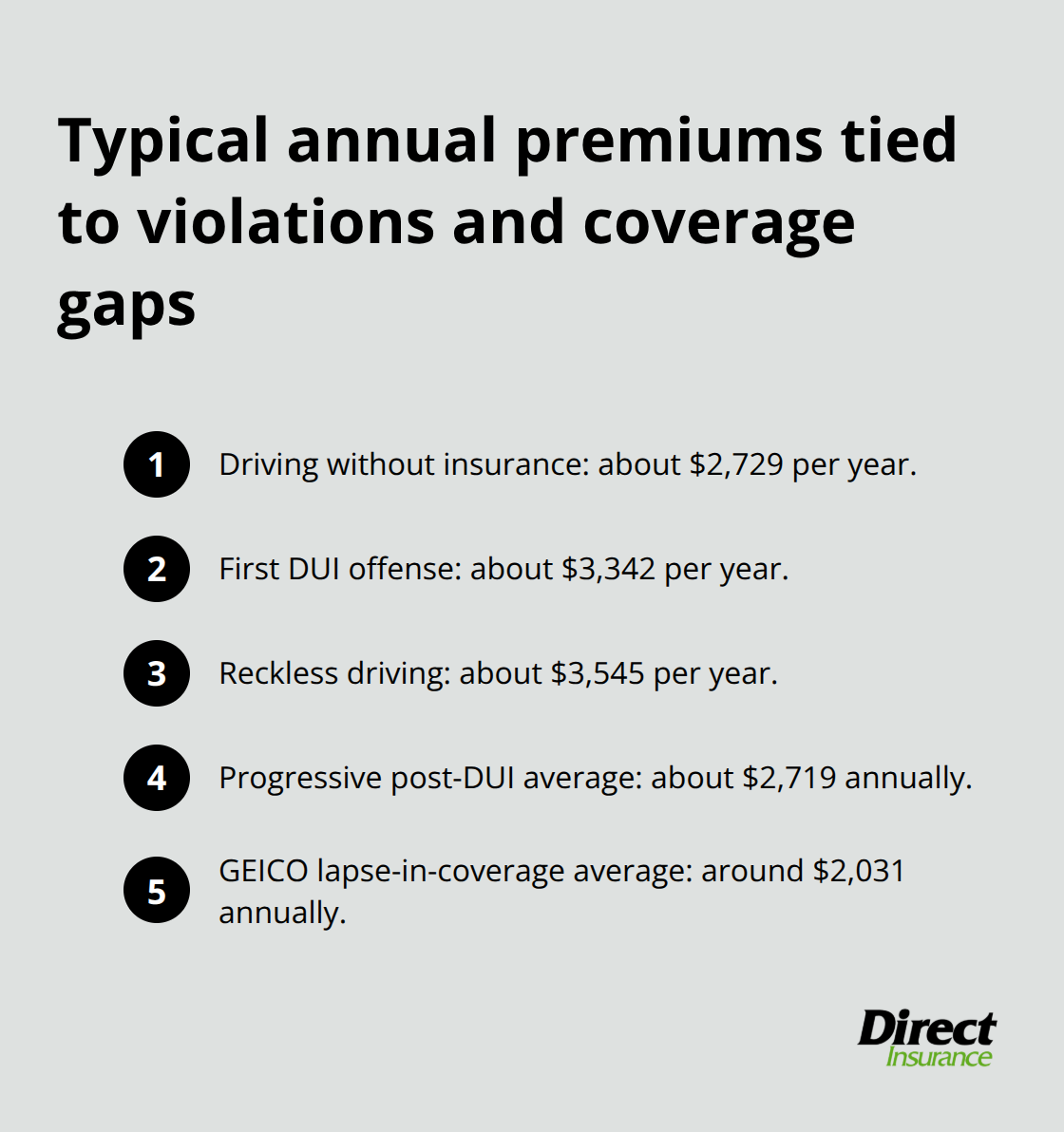

Driving without insurance costs an average of $2,729 annually according to insurance.com data, while a first DUI offense averages $3,342 per year, and reckless driving runs about $3,545 yearly. These higher premiums reflect the risk insurers assign to your driving record, not the SR-22 filing itself. If you don’t own a vehicle, non-owner SR-22 policies are available in Utah and provide liability coverage when you drive others’ cars. Shopping around saves money-Progressive averages about $2,719 annually for post-DUI drivers, while GEICO offers the lowest rates around $2,031 for those with a lapse in coverage.

Reducing Your SR-22 Expenses

Completing a defensive driving course and raising your deductible can lower costs during the filing period. You can also bundle policies or enroll in a usage-based program to qualify for additional discounts. The key is comparing quotes from multiple carriers, as rates vary significantly based on your violation type and driving history. Once you understand your costs and coverage options, the next step involves learning how SR-22 affects your insurance rates and what happens if your coverage lapses.

How SR-22 Affects Your Rates and Driving

Why Your Violation Drives Rate Increases, Not the SR-22 Filing

SR-22 does not cause rate increases-your violation does. Insurance.com data shows that a DUI conviction raises premiums, while reckless driving jumps costs to around $3,545 per year. Driving without insurance costs roughly $2,729 extra annually. The SR-22 filing itself costs about $25 and does not add to your premium, but insurers view drivers who need SR-22 as higher risk, which is why you pay substantially more. The increase depends on your ZIP code, vehicle type, driving history, and prior coverage gaps. This is why shopping multiple carriers matters-Progressive averages $2,719 for post-DUI drivers in Utah, while GEICO offers around $2,031 for drivers with lapsed coverage. Your violation type determines your rate tier, not the certificate.

Finding Coverage When Your Insurer Drops You

If your current insurer drops you after a DUI or serious violation, finding a carrier willing to file SR-22 becomes urgent. Many insurers refuse to cover drivers with recent violations, which limits your options significantly. Shopping multiple top-rated insurance companies helps you locate carriers that accept your risk profile and offer competitive rates for your situation.

What Happens When Your SR-22 Lapses

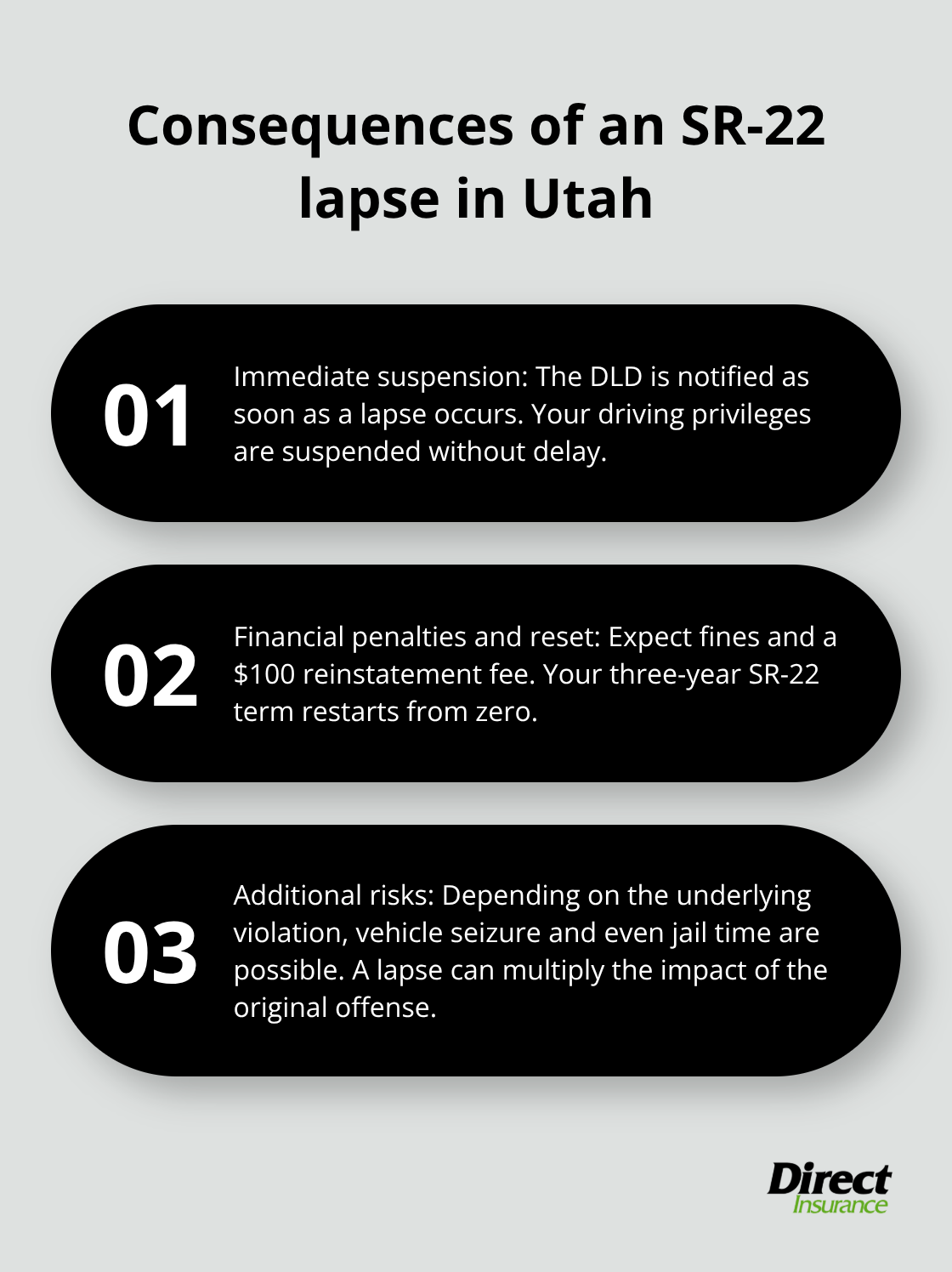

Letting your SR-22 lapse creates serious consequences that extend far beyond losing your license temporarily. If your policy lapses while you carry SR-22, the Driver License Division gets notified immediately and suspends your driving privileges. You face fines, a $100 reinstatement fee, and the SR-22 filing period restarts from zero-meaning a three-year requirement becomes three more years. Vehicle seizure and jail time are possible outcomes depending on the original violation.

Understanding Your Driving Restrictions

Utah’s Driver License Division at 801-965-4437 can confirm your exact filing duration and requirements, but the standard is three years from conviction. Driving restrictions vary by violation: a first DUI conviction triggers a 120-day suspension, while refusing a chemical test results in an 18-month suspension. Under 21? Utah’s Not-a-Drop law prohibits any detectable alcohol while driving, with suspensions of at least six months and two years if you refuse testing.

Ignition Interlock Requirements and Violations

You may also need an ignition interlock device installed by a state-certified provider if your violation was alcohol-related. Driving without one violates restrictions and costs you up to one year of additional lost privileges. The path forward requires maintaining uninterrupted coverage for your full SR-22 period without exceptions-a commitment that determines whether you move forward or face extended penalties. Understanding these restrictions helps you prepare for the next phase: securing affordable SR-22 coverage that fits your budget and keeps you compliant throughout the filing period.

Getting SR-22 Coverage That Fits Your Budget

Compare Multiple Carriers to Find Your Best Rate

Finding affordable SR-22 coverage in Utah requires shopping carriers on your behalf rather than accepting one option. Independent agencies compare quotes from multiple top-rated insurance companies to locate the best rates for your specific violation and driving history. This matters because SR-22 costs vary dramatically by carrier and ZIP code. A driver in one part of Salt Lake City might qualify for substantially lower rates than someone five miles away due to local risk factors. Shopping multiple carriers eliminates the rejection frustration many drivers face when calling insurers directly, since your violation type determines which carriers will even consider your application.

Adjust Your Deductible and Discounts

Payment flexibility matters when you already pay elevated premiums due to your violation. Raising your deductible from $500 to $1,000 typically reduces your annual cost by several hundred dollars. You understand the risk you assume when you make this choice. Defensive driving course completions, bundling home and auto coverage, and usage-based programs all qualify you for additional discounts. An independent agency identifies every discount available for your situation rather than leaving savings on the table.

Understand Your Payment Schedule Options

Some drivers need monthly payments to manage cash flow during the SR-22 period, while others prefer quarterly or semi-annual payments to reduce administrative costs. Structuring coverage around what your budget allows matters more than forcing you into standard payment schedules. An agency that works with multiple carriers can present actual options with real numbers attached, not theoretical estimates.

Ensure Your Filing Meets Utah Requirements

Your SR-22 filing must meet AAMVA standards, arrive within the required 30-day signature window, and stay active throughout your three-year obligation. The Driver License Division requires the form to be clearly titled “Financial Responsibility Form” with a signature date no more than 30 days old. Your insurer or agent handles the submission to the DLD-you don’t file it yourself. If your situation changes or you need to switch carriers during the filing period, your new insurer files the SR-22 on your behalf, but you must activate your new policy before canceling the old one to prevent a lapse that triggers license suspension.

Moving Forward

Your SR-22 filing period ends on a specific date determined by your violation type and conviction date, and you must contact your insurer to request removal of the SR-22 from your policy once that date arrives. The form does not disappear automatically, so taking this step prevents future complications. Your insurer will notify the Driver License Division that the filing is no longer required, officially closing this chapter of your driving record.

Rebuilding your driving history starts immediately, not after SR-22 ends, and every month you maintain continuous coverage without violations strengthens your record. Avoid traffic citations, speed limit violations, and any lapse in insurance during your filing period, as insurance companies track driving behavior closely and clean months accumulate faster than you might expect. A DUI from five years ago affects your rates less than one from six months ago, which means your driving choices during and after the SR-22 auto insurance Utah requirement directly determine how quickly your premiums drop.

Shopping for affordable coverage after SR-22 ends requires the same approach that worked during the filing period: comparing multiple carriers opens doors to insurers who would not consider you before. We at Direct Insurance Services help Utah drivers navigate the entire SR-22 journey and beyond by shopping multiple top-rated insurance companies to find you competitive rates whether you are currently filing or rebuilding after your requirement ends. Contact us to discuss your coverage options and start moving toward affordable insurance rates that reflect your improved driving record.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation