Utah Auto Insurance Tips: Smart Ways to Save on Your Coverage

Utah auto insurance rates are among the highest in the country, with drivers paying an average of $1,456 annually for full coverage. The good news is that you have real control over what you pay.

We at Direct Insurance Services have helped thousands of Utah drivers cut their premiums through smart strategies and informed choices. This guide shows you exactly how to do the same.

How Utah Drivers Actually Lower Their Auto Insurance Bill

Bundle Your Policies for Real Savings

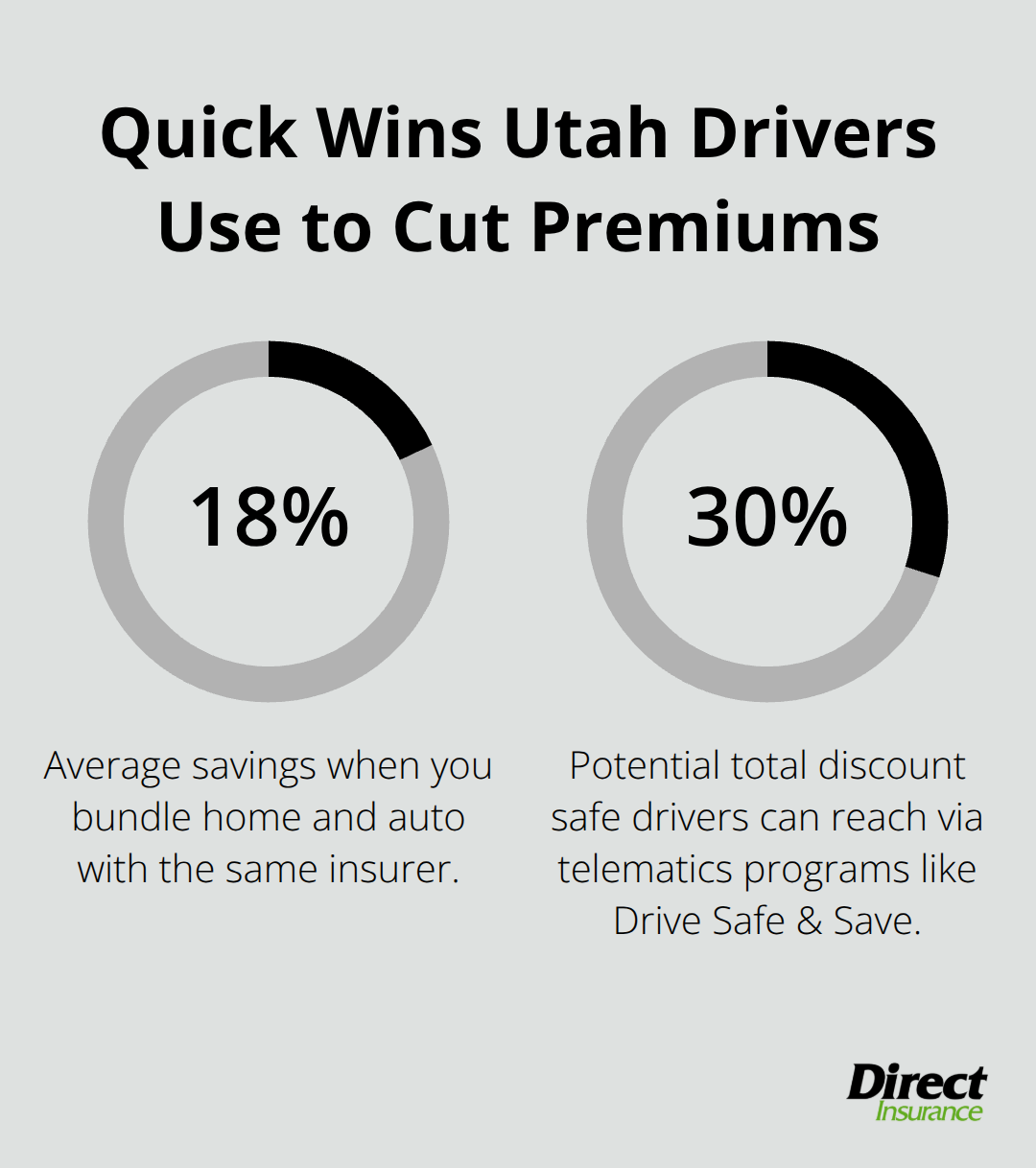

Bundling your home and auto policies with the same insurer typically cuts your premium by an average of 18 percent. This approach works as your first move because it’s the easiest way to trim costs without changing your coverage. Most Utah insurers apply this discount automatically at renewal, but you need to ask for it explicitly to make sure it applies to your account.

If you’re already bundled elsewhere, the math still works in your favor to shop around-a bundled quote from a different company might beat what you’re paying now, even after factoring in switching friction.

Prove Your Low Mileage and Earn Discounts

Low-mileage discounts reward Utah drivers who genuinely don’t log heavy miles. If you work from home, carpool, or use public transit several days a week, you could qualify for savings of 10 to 30 percent. State Farm’s Drive Safe & Save program uses telematics to track your actual driving patterns and delivers initial discounts just for enrollment, with potential total savings reaching 30 percent for safe drivers. This matters because insurers know that fewer miles on the road means lower accident risk. When you apply for a new policy, state your annual mileage honestly-underestimating to save a few dollars now backfires if you file a claim and the insurer discovers you drove way more than you stated.

Your Driving Record Determines Your Real Rate

A clean driving history is worth more than any single discount. Utah drivers with no accidents or violations in the past three to five years pay substantially less than those with incidents on their record. One at-fault accident or moving violation raises your premium by 20 to 40 percent, and that penalty lasts years. The inverse is also true: if you’ve had violations in the past but stay clean going forward, your rates drop significantly at renewal. Some Utah insurers offer accident forgiveness for your first incident, so ask about that when shopping quotes. Safe driving saves more money than juggling discounts ever will.

The strategies above address what you control directly. What you can’t control-your age, vehicle type, and location-shapes your baseline rate just as much.

Factors That Affect Your Utah Auto Insurance Rates

Your age, vehicle choice, and location form the foundation of what insurers charge you. Understanding these factors helps you make smarter decisions about coverage and where to shop.

Age Creates the Biggest Rate Divide

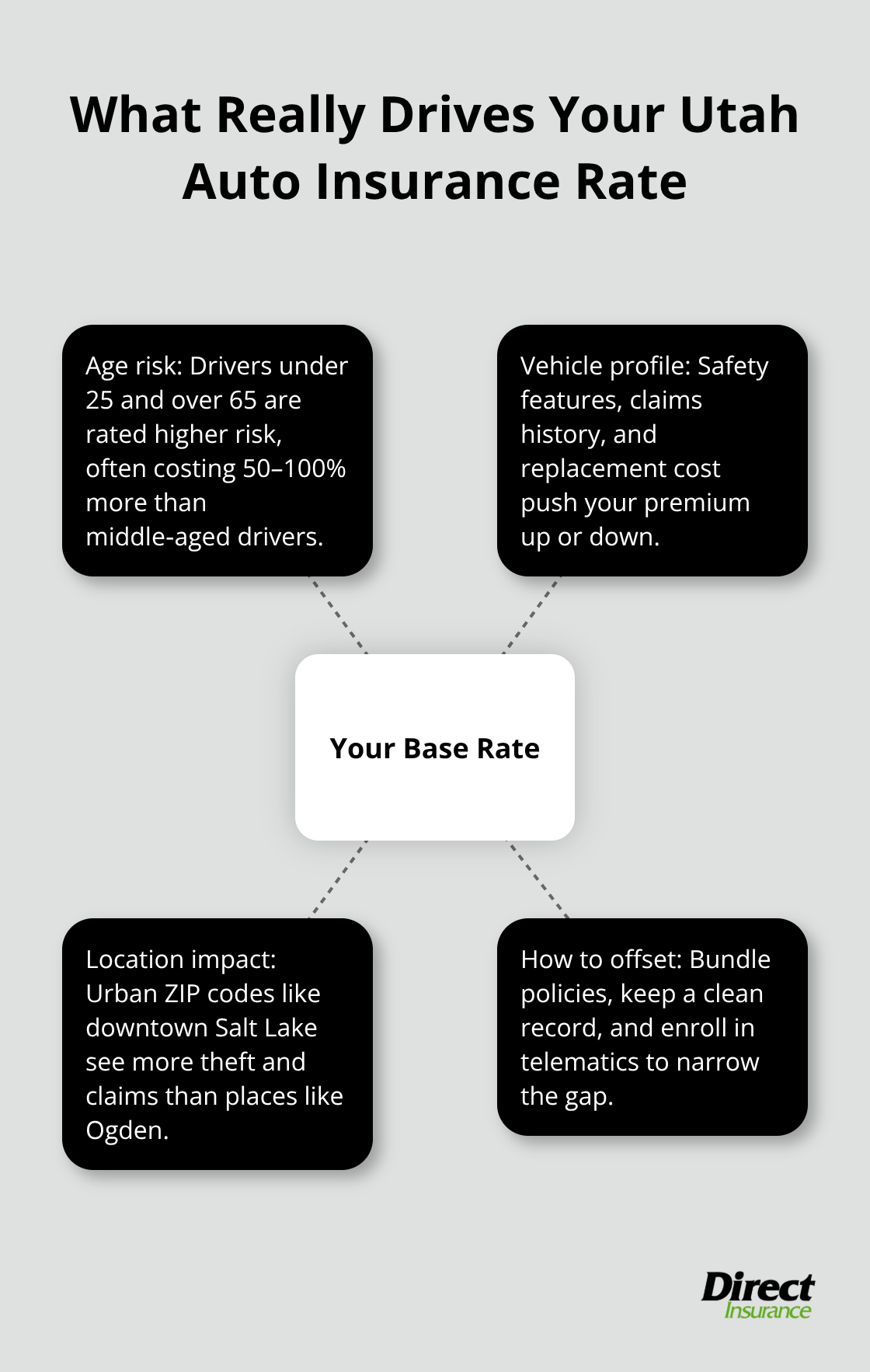

Utah insurers treat drivers under 25 and over 65 as higher risk, charging them 50 to 100 percent more than drivers aged 30 to 50. The math is brutal but honest-younger drivers have statistically higher accident rates, so the premium reflects that reality. If you’re a young driver, State Farm’s Steer Clear Safe Driver Program for drivers under 25 can trim hundreds from your annual bill if you complete the training. Conversely, if you’re over 55, Utah Code Annotated 31A-19a-211 allows you to qualify for a Defensive Driving Discount by taking an approved accident-prevention course, which reduces your premium for three years from completion.

Your Vehicle’s History and Features Matter More Than You Think

A 2024 sedan with modern safety technology and a strong claims record costs less to insure than a 2015 truck with a poor track record, even if you own both outright. Your vehicle’s claims history, safety features, and replacement cost directly impact your rate. If you drive an older vehicle worth less than $10,000, paying for comprehensive and collision coverage often doesn’t make financial sense-the premium you’ll pay over several years may exceed what the vehicle is worth.

Location in Utah Determines Your Baseline Cost

Where you live in Utah determines your rate as much as anything else. Salt Lake City drivers pay more than those in rural Weber County because urban areas have higher theft rates, more accidents, and more frequent claims. A driver in Ogden might pay 15 to 25 percent less than an identical driver in downtown Salt Lake, simply because of ZIP code risk profiles that insurers use. If you’re considering relocating within Utah, get quotes for your new address before the move-you might discover that moving to a suburb cuts your premium noticeably.

How These Factors Work Together

These three factors interact with your choices, which means you can’t eliminate them but you can work around them. A young driver in Salt Lake City with a practical sedan has three strikes against them, but bundling policies, maintaining a clean record, and enrolling in telematics programs narrows the gap significantly. Shopping multiple insurers matters more in your situation because rates vary wildly by company for the same risk profile. The next section shows you exactly how to compare quotes and find the coverage that actually fits your needs and budget.

How to Shop for Utah Auto Insurance the Right Way

Compare Quotes from Multiple Insurers

Utah insurers price risk differently, meaning the company that quotes you $89 per month might charge your neighbor $120 for identical coverage. Obtain quotes from at least three Utah insurers before making any decision, and request the same coverage limits across all quotes so you’re comparing apples to apples. When you gather quotes, provide accurate information about your annual mileage, driving history, and vehicle details-insurers verify these facts through databases and motor vehicle records, so inflating or deflating numbers now creates problems later. Most Utah insurers offer online quote tools that take 10 to 15 minutes.

Provide Accurate Information to Avoid Problems Later

Insurers verify your mileage, driving history, and vehicle details through official databases and motor vehicle records. Understating your annual miles to lower your quote backfires if you file a claim and the insurer discovers you drove significantly more than you stated. The same applies to your driving history-insurers pull your record from the Utah DMV, so omitting a violation or accident surfaces immediately during the claims process. Accurate information now prevents claim denials and rate increases later.

Review Your Coverage Every Two Years

Your life circumstances change, and your coverage should change with them. Getting married, paying off your vehicle, or moving to a different Utah neighborhood all affect what coverage you actually need. If you paid off your car loan, dropping collision and comprehensive coverage on an older vehicle with low market value often makes financial sense because the premium you save exceeds the protection you gain.

Utah’s new minimum liability limits of 30/65/25 took effect January 1, 2025, meaning all existing policies automatically renewed at these higher thresholds, which may have increased your premium. Ask your agent about discounts you might have missed during your last renewal, particularly Utah-specific ones like the Defensive Driving Discount for drivers over 55 or the Steer Clear Safe Driver Program for those under 25.

Uncover Hidden Discounts Most Drivers Miss

Many Utah drivers overlook discounts for safety features like anti-theft systems, alarm devices, or telematics enrollment because they don’t think to ask. These discounts reduce your premium by 5 to 15 percent depending on the insurer. Safety device discounts apply to vehicles equipped with alarms, anti-theft systems, or tracking devices.

Telematics programs track your actual driving patterns and reward safe habits with measurable savings.

Ask your agent about multi-car discounts if your household has multiple vehicles, and inquire about loyalty discounts or limited-time promotions your current insurer offers. The difference between asking and not asking can amount to hundreds of dollars annually.

Final Thoughts

Utah auto insurance tips work best when you take action on what you control. Bundling policies saves you an average of 18 percent, telematics programs reward your safe driving with measurable discounts, and a clean driving record keeps your baseline rate stable. Utah drivers who compare quotes from multiple insurers and ask about missed discounts typically save 25 to 40 percent compared to those who ignore their renewal notices.

The new 30/65/25 minimum liability limits that took effect January 1, 2025, mean your premium likely increased at your last renewal, making this the perfect moment to shop around. Age, vehicle type, and location set your foundation, but smart shopping and accurate information narrow the gap between what you pay and what you should pay. We at Direct Insurance Services shop multiple top-rated insurance companies on your behalf, which means you get competitive quotes without spending hours on the phone.

Contact Direct Insurance Services today and let us show you what you’re actually paying for and where you can save. Our team understands Utah’s unique risks and local insurance landscape because we live here. Getting your personalized quote takes one conversation.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation