Rental Property Insurance Utah: Coverage for Landlords and Investors

Owning rental property in Utah comes with real financial exposure. Weather damage, tenant injuries, and income loss can drain your profits fast.

At Direct Insurance Services, we help landlords protect their investments with the right rental property insurance in Utah. This guide walks you through the coverage types you actually need, how to assess your property’s value, and what gaps most investors miss.

What Landlords Face in Utah

Utah’s rental property market demands specific insurance protections that generic homeowners policies simply don’t provide. The state’s geography creates concentrated risks: properties within two miles of the Wasatch Fault face seismic premiums roughly 15-25% higher than non-seismic zones, according to industry data. Wildfire-prone areas near the Wasatch Mountains can add surcharges of $200-$400 annually. Winter freeze damage to pipes and HVAC systems happens regularly across the state, making adequate coverage non-negotiable. Student rentals around universities carry dramatically higher vandalism risk, with claims averaging $8,000-$12,000 per incident according to Stillwater Insurance data. Location matters tremendously: Salt Lake City landlords pay about $580 per year on average for landlord insurance, while Centerville averages around $456 per year. These aren’t minor differences-they reflect real exposure variations that standard policies miss entirely.

Dwelling coverage that actually protects you

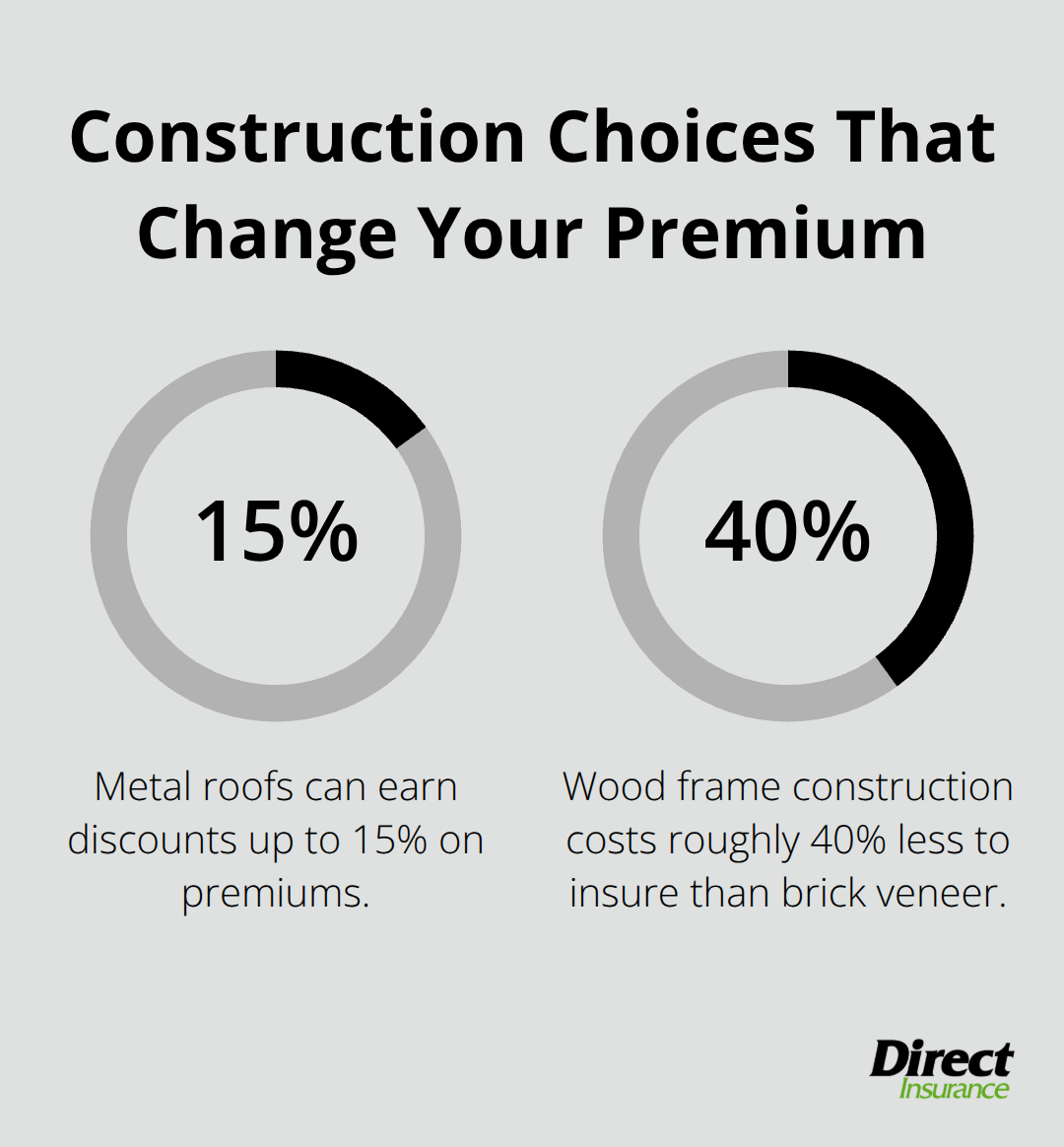

Most Utah landlords severely underestimate replacement costs. Current construction expenses demand dwelling limits that reflect today’s rebuild prices, not yesterday’s purchase price. Properties in high-value areas commonly require limits up to $1 million to cover full reconstruction. If you carry only 50% of replacement cost, coinsurance clauses proportionally reduce payouts after a loss. Older homes built before 1980 see 20-35% premium increases due to outdated electrical and plumbing systems. Wood frame construction costs roughly 40% less to insure than brick veneer, but masonry homes built after 1990 earn fire-resistance discounts. Roofing age matters: asphalt shingles over 15 years old trigger 10-20% rate increases, while metal roofs can earn discounts up to 15%. Galvanized steel plumbing adds surcharges; copper or PEX plumbing typically yields lower rates. You should document upgrades to wiring, plumbing, roofing, and safety systems-these directly lower premiums by reducing underwriter risk.

Liability and income protection aren’t optional

Utah law doesn’t mandate landlord insurance, but the financial consequences of skipping it are catastrophic. A single tenant injury claim can exceed $1 million in medical and legal costs. We recommend liability minimums of $300,000 per property, with umbrella coverage of $1-2 million for owners with multiple units. Medical payments coverage of $5,000-$10,000 handles minor tenant injuries without triggering formal liability claims. Loss of rental income coverage replaces 12-24 months of rent when a covered event renders the property uninhabitable during repairs-fire damage typically requires 4-6 months to repair, while water damage takes 2-3 months. Tenants who carry renters insurance with at least $300,000 liability reduce landlord premiums by 10-25% and create a second layer of protection. Tenant screening and professional property management yield premium discounts of 5-15%.

What separates smart landlords from the rest

The difference between staying profitable after a loss and losing everything comes down to three decisions. First, you must align your dwelling limits with actual reconstruction costs in your area. Second, you need liability protection that matches your exposure-one injury claim can wipe out years of rental income.

Third, you should require tenants to carry renters insurance and maintain solid screening practices. These aren’t luxury add-ons; they’re the foundation of financial stability. Your next step involves assessing your specific property value and understanding what replacement actually costs in today’s Utah market.

Coverage Types That Actually Protect Your Utah Rental

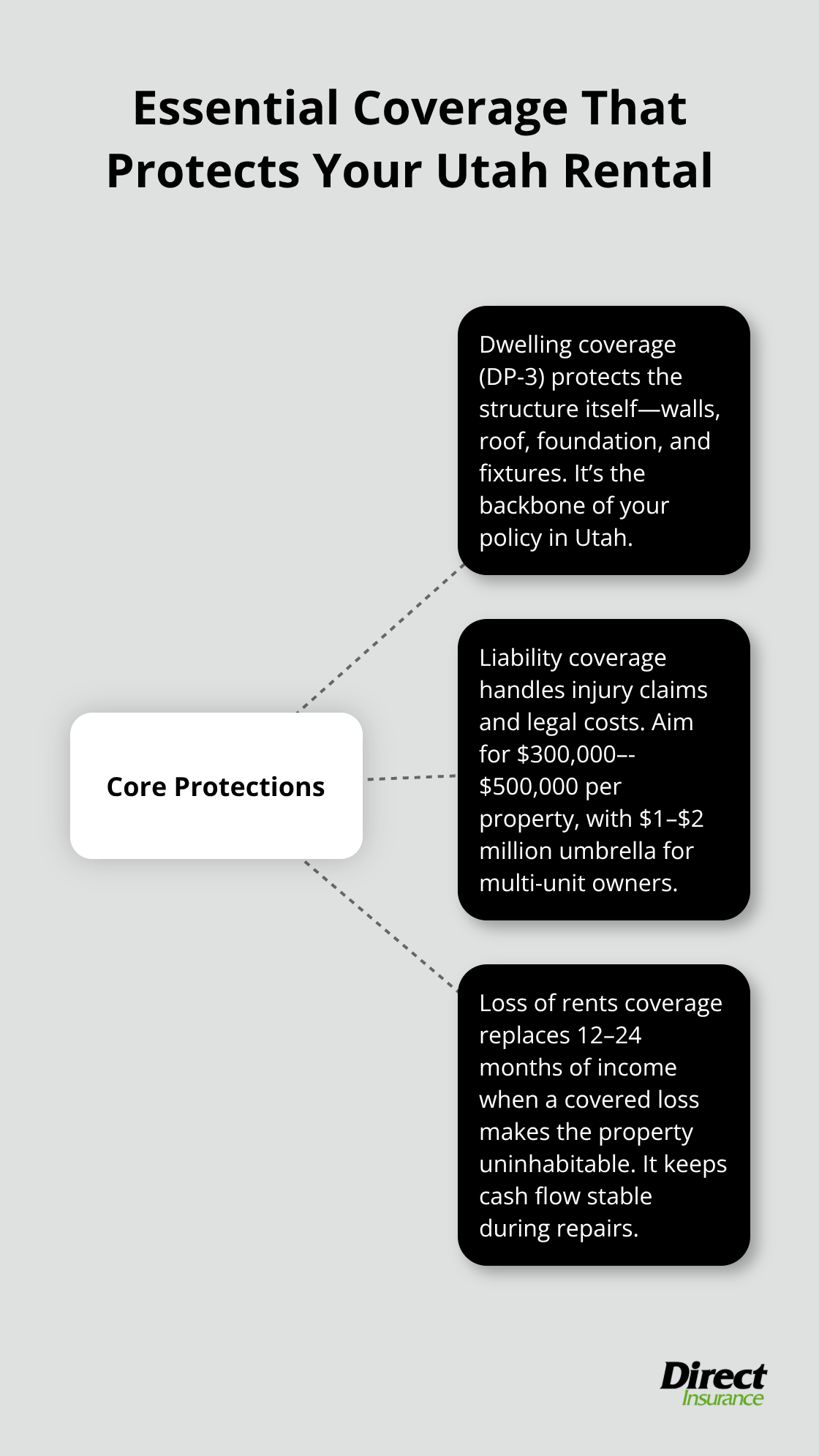

Rental property insurance in Utah breaks down into three essential components, and understanding what each one does separates landlords who recover from losses and those who face financial ruin. Dwelling coverage protects the physical structure itself-the walls, roof, foundation, and permanent fixtures. This isn’t optional; it’s the backbone of your protection. In Utah, you’ll typically encounter DP-3 Special Form coverage, which is the broadest standard option available for landlords and covers most perils except floods and earthquakes.

Dwelling Coverage Demands Accurate Replacement Costs

The critical mistake most Utah landlords make is setting their dwelling limit based on what they paid for the property, not what it costs to rebuild today. If your rental cost $350,000 five years ago but would cost $500,000 to rebuild now due to inflation and material costs, carrying only $350,000 in dwelling coverage creates a coinsurance penalty. Insurance companies pay claims proportionally to the coverage you actually carry versus what you should have carried. Properties in high-value areas around Salt Lake City and Park City commonly need limits up to $1 million.

Document every upgrade-new wiring, plumbing, roofing, HVAC systems-because these directly reduce your premiums by demonstrating reduced risk to underwriters. Metal roofs earn discounts up to 15%, while asphalt shingles over 15 years old trigger rate increases of 10-20%. Older homes built before 1980 see 20-35% premium increases due to outdated electrical and plumbing systems. Wood frame construction costs roughly 40% less to insure than brick veneer, but masonry homes built after 1990 earn fire-resistance discounts.

Liability Coverage Protects Against Catastrophic Claims

Liability coverage protects you when a tenant or visitor gets injured on your property and sues. Utah law doesn’t require landlord insurance, but a single injury claim routinely exceeds $1 million in medical expenses and legal fees. Try carrying $300,000 to $500,000 in liability coverage per property, with umbrella policies of $1-2 million if you own multiple units. Medical payments coverage of $5,000-$10,000 handles minor injuries without requiring formal liability claims, which keeps your claims history clean and premiums lower.

When tenants carry renters insurance with you listed as a certificate holder, your premiums drop 10-25% because the liability exposure shifts partially to their policy. Tenant screening and professional property management yield premium discounts of 5-15%, turning risk management into direct savings on your insurance bill.

Loss of Rents Coverage Protects Your Cash Flow

Loss of rents coverage is where most landlords face brutal financial consequences when they skimp. Fire damage typically requires 4-6 months to repair; water damage takes 2-3 months. During that time, your tenant moves out, you collect no rent, but your mortgage, taxes, and maintenance costs continue. Loss of rents coverage replaces 12-24 months of rental income, protecting your cash flow during the reconstruction period. This protection separates landlords who stay solvent after a major loss from those who face financial hardship. Your specific property’s location, age, and condition all influence which coverage limits make sense for your situation.

How to Choose the Right Rental Property Insurance Policy

Calculate Your Actual Replacement Cost

Selecting rental property insurance in Utah starts with one critical number: your actual replacement cost, not your purchase price. Contact a local contractor or use the National Association of Insurance Commissioners rebuild cost estimator to determine what reconstruction truly costs today. A $400,000 purchase five years ago might require $550,000 in dwelling coverage now due to material inflation and Utah labor costs. This figure becomes your baseline for dwelling limits.

Once you have this number, document every property upgrade: new roof, updated electrical wiring, plumbing replacements, HVAC systems, and safety features like monitored alarms or water leak sensors. These upgrades directly lower your premiums because they reduce risk. A metal roof earns discounts up to 15%, while asphalt shingles over 15 years old add 10-20% to your costs. Older homes built before 1980 face 20-35% premium increases, so upgrading electrical and plumbing systems pays for itself through insurance savings alone.

Shop Multiple Carriers for Competitive Rates

Comparing quotes from multiple carriers prevents overpaying and exposes significant price variations. The typical Utah landlord insurance cost runs around $913 annually, but actual premiums swing wildly based on your specific property and location. A Salt Lake City property averages $580 per year while Centerville averages $456 per year according to Steadily Insurance data. Properties within two miles of the Wasatch Fault face 15-25% higher premiums due to seismic risk, and wildfire-prone areas near the Wasatch Mountains add $200-$400 annually.

Shopping multiple carriers reveals these variations and helps you avoid overpaying. When comparing quotes, examine deductible options carefully: higher deductibles reduce premiums but increase your out-of-pocket costs after a claim. A $1,000 deductible costs significantly less than a $500 deductible, but you need cash reserves to cover that gap if damage occurs. Balance your deductible level against your ability to absorb losses without financial strain.

Request Comprehensive Coverage in Your Quotes

Request quotes that include DP-3 Special Form coverage (the broadest standard option), $300,000-$500,000 liability per property, 12-24 months loss of rents coverage, and $5,000-$10,000 medical payments coverage. These components work together to protect your investment and cash flow during major losses. Requiring tenants to carry renters insurance with at least $300,000 liability reduces your premiums 10-25% and adds a protective layer. Tenant screening and professional property management yield additional discounts of 5-15%, turning risk management into direct savings on your insurance bill.

Final Thoughts

Protecting your Utah rental property comes down to three concrete decisions that separate landlords who recover from losses and those who face financial hardship. Align your dwelling limits with actual reconstruction costs in your area, not what you paid years ago. Carry liability coverage that matches your exposure, with $300,000 to $500,000 per property and umbrella policies for multiple units. Require tenants to carry renters insurance and maintain solid screening practices.

Your next step involves getting accurate quotes from multiple carriers. The typical Utah landlord pays around $913 annually, but your specific property’s location, age, and condition create significant variations-a Salt Lake City property averages $580 per year while Centerville averages $456 per year. Properties near the Wasatch Fault face 15-25% higher premiums due to seismic risk. Shopping multiple carriers prevents overpaying and reveals which companies offer the best rates for your situation.

At Direct Insurance Services, we help Utah landlords find rental property insurance Utah that actually protects their investments. Our team understands the unique risks of rental properties in Utah, from wildfire exposure to winter freeze damage to tenant-related liability. Contact us today to compare your options and secure the coverage your rental property needs.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation